Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends longer form note…

I’ll pick up just ‘bout where I left off HERE yesterday with an updated look at the belly. Why? Dunno. It strikes ME as an interesting / funTERtaining spot on the curve with SOME duration and convexity and at same time, can / will help as a vehicle to watch and dare I say, TRADE / hedge with in / around this coming weeks FOMC meeting and press conference, Wednesday …

5yy WEEKLY: 4.00% is a level of interest — approx middle of range noted…

… momentum is overBOUGHT and correcting suggesting either HIGHER RATES and / OR time at a price … Furthermore, if you consider ‘the’ range high as 4.75, Friday’s closing level is just ‘bout 3bps NORTH of the exact ding-dong MIDDLE … Finally, in as far as rates inching HIGHER into / through / beyond FOMC (?), a couple reasonable levels to keep in mind 4.16% noted (blue) as the 50wMA followed by 4.25% — psychologically important and well, well continue ‘watching’ …

NEXT UP UoMISSagain data (the sole highlight from yesterday) …

ZH: Panicking Democrats Send UMich Inflation Expectations To Highest In 32 Years

While current economic conditions were little changed, expectations for the future deteriorated across multiple facets of the economy, including personal finances, labor markets, inflation, business conditions, and stock markets.

Many consumers cited the high level of uncertainty around policy and other economic factors; frequent gyrations in economic policies make it very difficult for consumers to plan for the future, regardless of one’s policy preferences.

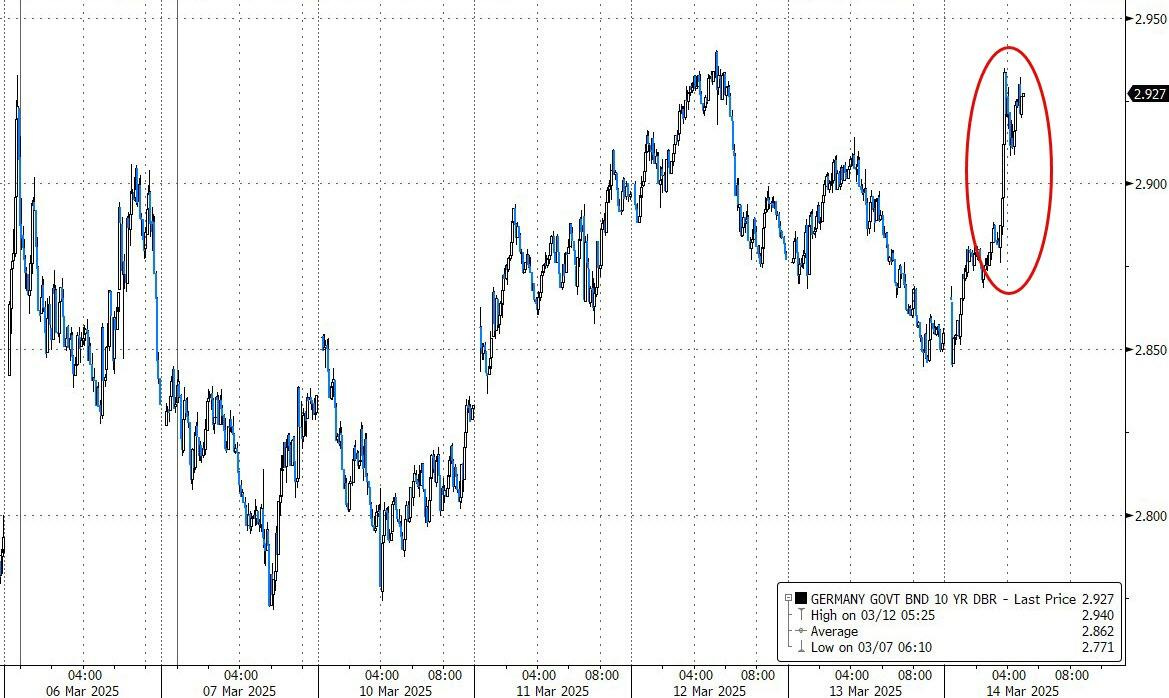

… Alrighty, then. Many out there continuing to watch developments ‘cross the pond as they may impact US RATES so …

ZH: Bund Yields Spike As Germany's Merz Reaches Debt Deal With Greens, Claims (Unironically) "Fiscal Discipline Important"

… “Game on again for the euro,” said Brad Bechtel, head of FX at Jefferies, adding that peace talks for Ukraine are adding to the currency’s momentum. “The market is cautiously optimistic that we are progressing in the right direction.”

...but bund yields are also spiking to recent highs...

Merz said late Thursday that he’s “very optimistic” that the landmark debt-spending package will be approved after a parliamentary debate on Thursday laid bare a deep rift with the Greens.

“What more do you want than what we have proposed to you?” Merz asked, prompting jeers from the party.

“The headlines are providing some comfort that the Greens are on board with the proposals,” said Evelyne Gomez-Liechti, a strategist at Mizuho International Plc, adding that markets had been pricing some chance of the agreement not passing through.

As Goldman Sachs Alberto Bacis notes, the narrative prevailing over the last 10 days is the following:

Germany has pivoted towards a fiscal expansionary stance > they have plenty of room > defense and infrastructure spending will generate a massive growth turnaround for Germany and rest of the block, bringing the following externalities:

1/ ECB must remain restrictive

2/ Inflation will fly

3/ Sky is the limit for investments

… By days END, US shares monster BID and so, a sticksave from being worst week since 2020 (ie C19 pandemic) …

ZH: Stocks Shrug Off Sentiment Slump As Century-Old Signal Flashes Red

…Despite plenty of intraweek vol, Treasury yields ended dramatically unchanged...

Source: Bloomberg

A notable decoupling this week between bonds and stocks...

Source: Bloomberg

… AND … enough.

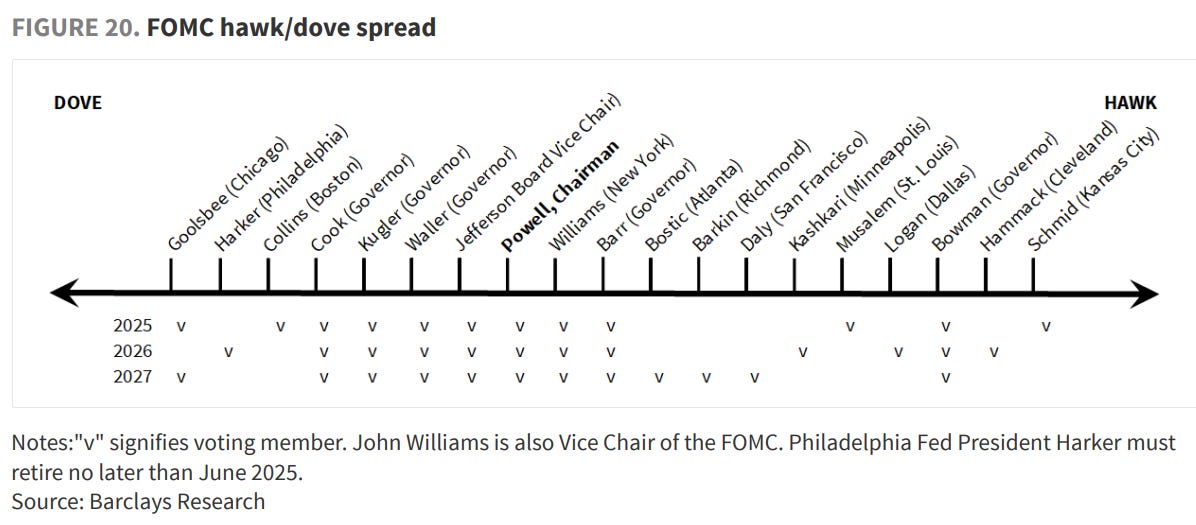

I’ll move on TO some of Global Walls WEEKLY narratives — SOME of THE VIEWS you might be able to use. A few things which stood out to ME this weekend from the inbox … mostly FOMC pre caps with a few ideas / positions / visuals sprinkled in …

A British shop on the FOMC (with a visual that caught MY attention) …

We expect the FOMC to keep policy rates unchanged at 4.25-4.50%, amid rising uncertainty, tariffs and inflation expectations. We think the SEP will show upward revisions in inflation and unemployment projections and lower growth. We expect the dot plot to show one 25bp cut this year and two in 2026.

… Same shop on RATES (from Thurs) as they remain LONG into Fri, weekend and presumably, the FOMC ….

In the US, policy uncertainty remains elevated, hurting consumer and business sentiment and the economic outlook. We remain long 5y USTs. In Europe, EUR rates remain torn between near-term tariff risks and medium-term fiscal optimism. In Japan, yields rose sharply with Monday's soft 5y auction.

…We continue to recommend being long 5y USTs (entry: 4.10%, current 4.02%) as the market implied medium-term path of the real policy rate is too high both in absolute terms as well as relative to market's own expectation of inflation returning to the 2% target in a couple of years ( Figure 3 and Figure 4).

… and same shop on US economy in the all-important week ahead …

As the US administration seems determined to impose high tariffs and 'detox' the domestic economy, US growth is set to slow sharply with global spillovers. Any effect from higher European investment will take time but could be significant. Next week, the Fed, BoE and BoJ will likely wait and see.

…US Outlook Rock | Fed | Hard Place

Trump and his administration have expressed more tolerance for adverse economic fallout from tariffs than we had thought. We adjust assumptions accordingly, incorporating softer trajectories of activity and a bigger inflation upsurge, with the Fed weighing a profound policy dilemma.

February inflation data sent mixed signals, with core CPI inflation (0.23% m/m) retreating even as PPI details point to another elevated core PCE print (+0.36% m/m). Although these swings reflect volatile components, tariffs pose an intensifying threat to the Fed's inflation mandate, with Michigan 5-10y inflation expectations visiting levels not reached since the early 1990s.

We have adjusted our outlook to allow for higher tariffs, with our placeholders assuming a 15% trade-weighted tariff that is 5pp higher than our prior assumption. With tariffs undermining purchasing power by boosting import prices, policy-related uncertainty instilling precaution on spending, and balance sheets less supportive, we now expect even slower growth this year.

With a shutdown averted, attention turns to the FOMC next week. We expect another hold, consistent with recent signals. With updated SEPs likely showing slower growth and a more significant price effect from tariffs, we expect the median dot to show just one cut this year and two next. Powell will likely talk tough on inflation, citing uncertainty as a reason to remain on hold.

…We adjust our baseline in the direction of downside risks … We expect these higher tariffs to weigh on GDP growth over the next few quarters, for a variety of reasons. Supply chains of many US manufacturers are closely integrated with its close trade partners, including Canada and Mexico, which threatens to boost production costs and disrupt production significantly. They will also drive up prices of goods, undermining household purchasing power. Beyond this, evidence is mounting that policy-related uncertainty is contributing to a more precautionary spending environment from businesses and consumers, including fallout on equity markets in recent weeks. Taking account of these influences, we have lowered our GDP growth projection in 2025 0.8pp, to 0.7% Q4/Q4, and boosted our end-year unemployment rate projection 0.4pp, to 4.2%. We retain our outlook that GDP growth will remain at 1.5% q/q saar throughout 2026, with the labor market tightening over the course of the year amid labor supply constraints.

The higher tariffs also feed through to faster core PCE inflation this year, boosting our projection in 2025 0.4pp, to 3.2% Q4/Q4. With tariff-related prices no longer spilling into 2026, as in our prior baseline, we trim our 2026 projection 0.1pp, to 2.2% Q4/Q4. Our core CPI trajectory has been adjusted by similar magnitudes, to 3.6% Q4/Q4 in 2025 (+0.3pp) and 2.5% Q4/Q4 in 2026 (-0.1pp).

Best in SHOW (now $hort FF futures (FFN5) as mkts ‘fully priced’ for 25bp rate cut in June (so, a FADE) and remains LONG BONDS (at 460) …

In the week ahead, the FOMC will leave policy rates unchanged and provide an updated look at its operating framework for the balance of the normalization cycle …

… While not our base case, the tail risk of just one cut being indicated is a conceivable outcome from our perspective, even as such a move would be decidedly at odds with current market pricing. Conversely, there is a compelling case to be made for a median dot that reflects 75 bp of rate cuts this year, particularly given the recent plunge in business and consumer sentiment, softening in consumption, tightening in financial conditions as a result of the selloff in equities, and prospects for a trade-war-driven downturn in GDP growth. That said, with the unemployment rate at 4.1% and core-PCE estimates tracking at an elevated monthly pace of +0.34%, our base case is for the median dot to remain unchanged, indicating 50 bp of rate cuts by year-end. After all, the Fed's preferred measure of inflation is currently expected to make its largest monthly gain since March 2024, and that's without fully accounting for tariff driven goods inflation …

Here is yet another shop with TWO, count ‘em, TWO, NOT ONE FOMC precaps for the week ahead … First from the econ team …

We expect the FOMC to hold rates steady at next week’s meeting, keeping the fed funds range at 4.25%-4.50%.

The FOMC’s economic projections should begin to reflect prospects for higher, tariff-fueled inflation and softer US economic growth.

We see policy remaining on hold through year end and rate cuts restarting in Q1 2026.

… and next from the RATES FOLKS …

14 Mar 2025 BNP: The December FOMC Clue | US Rates Insights

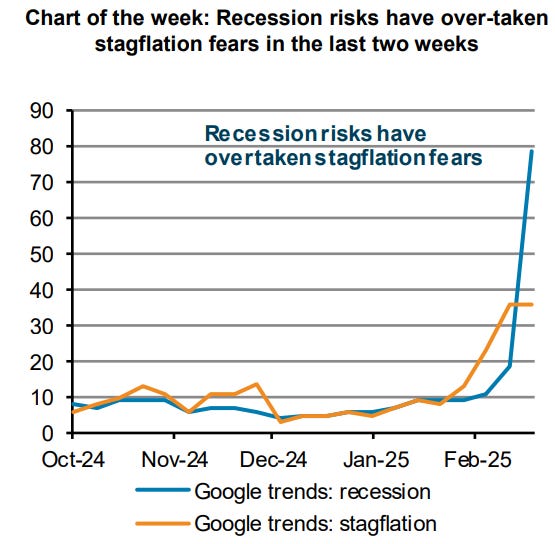

KEY MESSAGES Treasuries and TIPS: Recession risks have overtaken stagflation risks, leaving markets confused between steepening and flattening. We think the March FOMC meeting – like the December FOMC meeting – might not share the market’s view that growth risks are dominating inflation risks and instead bring back focus on heightened inflation fears. Recent UMich data and PCE tracking have added to inflation risks. We maintain 2s10s flatteners and long 10y TIPS into the March FOMC and will re-assess after the meeting…

…What’s new: Stagflation vs. recession, wait for Fed Treasury yields are nearly unchanged over the week, with an interesting mix of higher real yields and lower breakevens – a price action that doesn’t fit in either stagflation or recession mold. The curve steepened and flattened mildly, reflecting confusion about the macro narrative…

…Investors behind the steepener are confident that the Fed will err on the side of alleviating growth concerns even though data has been mixed. We are not so sure…

… The recession pricing dynamic has occupied the most mind-share recently, with weakness in risky assets adding to the theme. No surprise then that recession searches on Google have leap-frogged for “stagflation” – inducing some steepening (see Figure 1). However, we disagree with the market’s focus on growth risks at the expense of rising inflation risks.

This next note from a Brit and former Bear Stearns economist …

The Fed meets next week in the wake of inflation data that argue for caution and amid rising recession fears. In the attached Weekly we discuss why, despite the moderation in core CPI inflation reported this week, we remain cautious about the inflation outlook and also why recession is not our base case for 2025. We also preview next week's FOMC meeting.

… This all suggests that we should be cautious in judging inflation trends to be improving particularly since i) the impact of the Fed’s 100 basis points of rate cuts in the last four months of 2024 has likely not yet passed through and ii) there is the looming impact of tariffs on the price measures. The share of small firms in this week’s NFIB survey that were raising prices jumped 10 points in February with the report noting that “tariffs are being broadly applied and retaliated against, changing the prices of imports and exports.”

In the 39-year history of the NFIB survey, there was a larger monthly gain on only one occasion: September 2020…

…The FOMC Needs to Think Hard About the Monetary Dilemma Posed by Tariffs… …There is no doubt that policy is better positioned now than it was in early 2022, but Powell might be well advised to read former Fed Vice Chair Alan Blinder’s June 1995 speech The Strategy of Monetary Policy in which he outlined the ‘stitch in time’ approach to monetary policy. Blinder said “have to base your thinking on some kind of a monetary theory, even though that theory might be wrong” because “the other strategy—the Bunker Hill strategy—is sure to lead you into error.” In this case, a stitch in time could be to signal no cuts in 2025. This is an unlikely step, but Powell needs to outline this as a possible outcome for policy this year.

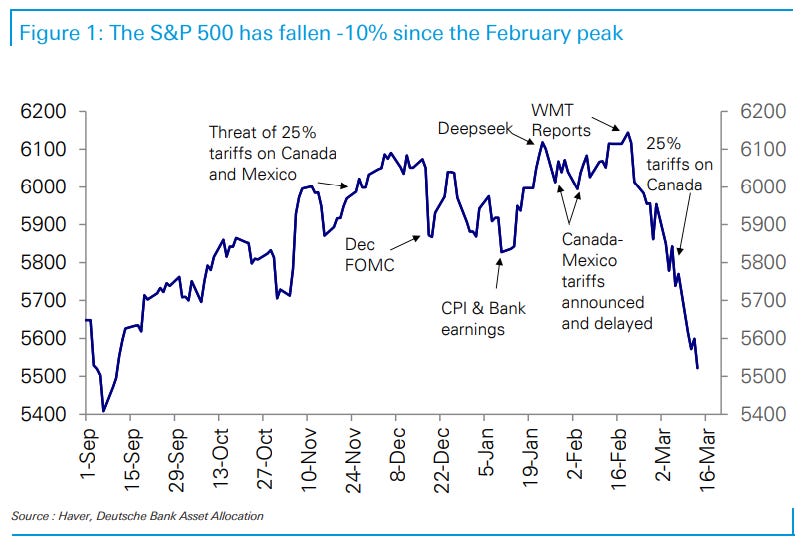

As you know I value POSITIONS data especially when combined with visuals and this next note from a small German shop contains both and even though it’s relating TO equities, given the week just past — equities in correction, then bounce, all impacting move in rates (ie 60/40 still NOT DEAD yet …), well …

14 March 2025 DB: Investor Positioning and Flows - Sliding Further

What stood out this week: Equity positioning continued to turn more underweight (z score -0.36, 26th percentile); with trade policy uncertainty likely to continue, at least until April 2nd, we expect positioning to continue to unwind and a move to the bottom of its band which is where it fell to in the last trade war would take the S&P 500 down to 5250 (Taking Stock of The Selloff); positioning is now below average across most sectors; US equity funds (-$2.8bn) saw outflows this week, especially notable because the second week of March typically sees large inflows; Europe ($5bn) continued its recent strong run with the strongest inflows in 8 years; across bonds, flows rotated into government bonds ($6.4bn) and away from HY (-$2.2bn) and IG (-$0.3bn).

… NOTED. For somewhat more — a different perspective and stratEgerist but same shop …

We see the selloff in US equities as having further to go. Equity positioning has been cut sharply, but only from near max overweight to slightly underweight levels. With trade policy uncertainty likely to continue to weigh, at least until April 2, we expect positioning to continue to unwind. A move to the bottom of the positioning band which is where it went to in the last trade war, would take the S&P 500 down to 5250.

The fundamentals have been weakening. Both consumer and corporate confidence have fallen sharply. Capex intentions have been slashed and the decline in CEO confidence is likely to arrest the budding recovery in manufacturing that had begun. Consensus GDP growth forecasts for Q1 have not been cut yet and downgrades likely to come. Earnings estimates for Q1 have been downgraded somewhat more than is typical, but in our reading do not yet factor in any slowing in macro growth, and we look for downgrades to continue…

…Too early to throw in the towel on our year-end target. If the slide in approval ratings prompts a credible plan to resolve tariff uncertainty, it will allow the business cycle to continue. Equities can bounce back sharply in such a scenario, catching back up to their longer-run uptrend channel, as they did after the Phase 1 deal in 2019, so while the risks have grown, for now we maintain our year-end S&P 500 target of 7000.

… Same shop from Germany weighing in with their FOMC precap …

14 March 2025 DB: March FOMC preview: Patience is a virtue amidst cross currents

We expect the Fed to hold rates steady for the second straight meeting and, given heightened uncertainty, provide limited guidance about the policy path ahead. The statement is likely to announce a pause in QT beginning in April, and we expect forward guidance indicating that QT is expected to resume once the debt ceiling is resolved and the liability composition of the balance sheet normalizes. We see risks that a slowing is announced rather than a pause.

The updated Summary of Economic Projections is likely to show a median expectation of two rate cuts this year, unchanged from December. However, we expect some upward drift in individual dots with risks the median shows only one reduction in 2025. Motivating this slightly hawkish signal will be economic projections that show higher inflation, somewhat weaker growth, and an unchanged forecast for the unemployment rate this year. Finally, we expect the long-run dot to continue drifting slowly higher.

The overall tone of the meeting and Chair Powell's press conference should mirror his comments from last Friday's US Monetary Policy Forum – although some indicators signal downside risks to growth, the Committee is not in a hurry to adjust rates. This week's inflation data, which point to another strong core PCE print, reinforces this message of patience for the time being (see "Feb CPI recap: Core PCE might not benefit from CPI's downdraft").

Our long-standing view for the Fed expects the policy rate to remain on hold this year. But as we noted recently (see “Tariff they neighbor” and "How should the Fed respond to an economy in "transition"?"), we see mounting downside risks to the economy that could require the Fed to reduce rates in 2025. Like the Fed, we hope to get a better sense of the details around policies before deciding whether an adjustment is needed. However, the data and financial markets might not allow us (or the Fed) to be so patient.

… and finally, some more economically centric FLATION related visuals …

…Details within the CPI and PPI point to 0.30-0.34% core PCE print for Februar

Progress on core PCE seems to have stalled

Everyone’s got an FOMC opinion and here’s another precap …

14 March 2025 ING Federal Reserve preview: No imminent pressure, but downside growth risks point to 2H rate cuts

After 100bp of interest rate cuts in late 2024, Chair Powell suggests that the Fed aren’t in a hurry to ease policy further and a no change outcome is widely expected on 19 March. But President Trump’s spending cuts and trade protectionist policies are hurting growth prospects and will likely force the central bank’s hand in the second half of 2025

This next shop and group of stratEgerists is always got great content and as long as I’m blessed to receive in the ‘inbox’, I will read / learn and share … Here they are asking a very important question which I’ve attempted to ‘play along at home’ and tackle in the short-term with visuals of yields and momentum, etc …

March 14, 2025 MS: How to Know You're at the Lows in US Treasury Yields | US Rates Strategy

We think US Treasury yields have further to fall as long as tariffs, related threats, and fiscal austerity continue. We don't yet see signs of an overextension like we saw when yields were rising around the year-end turn. A hawkish dot-plot would only extend the bull market in Treasuries.

Key takeaways

No "Trump put", no "Fed put", no service. As this reality bites harder, willingness to take risk declines, growth expectations suffer, and Treasuries benefit.

SOFR swaption markets suggest the decline in US rates could extend further, as market-implied probabilities of sustained lower rates remain well behaved.

In contrast, earlier this year, SOFR swaption markets flagged an overextension during the rise in US rates that lasted through mid-January, or a bear trap.

Stay positioned for lower yields via the 2s5s30s 50:50 butterfly, short 10y TIPS breakevens, long 2y TIPS, long May fed funds futures, and M5/Z6 flatteners.

A "not in a hurry" Fed and/or a hawkish FOMC dot-plot in the coming week risk sending investor growth expectations and Treasury yields even lower.

…United States | No signs of panic buying in options We use options markets to help determine if yields have reached their lows

… More sophisticated technical indicators – like those derived from swaption-implied rate distribution probability data – also suggest that buying of options on lower rates remains well within the bounds of normal, i.e., not frenetic…

… In Exhibit 4 , we show the in-sample residual from the regression in Exhibit 3 . The residual represents the amount of the market-implied probability of the 5-year SOFR rate trading below 4.00% in three months the level of the 5-year SOFR rate cannot explain

… Today, the regression residual in Exhibit 4 remains near the middle of a +/-4pp range – suggesting more balanced investor sentiment using the past two years of options market trading. Until investor sentiment becomes overly bullish in the options market, we think yields could keep falling…

…Based on our economists' view of the Fed's messaging, investor interpretation should coalesce around the idea that the strike on the "Fed put" remains far out-of-the-money.

As a result, we continue to suggest investors stay positioned for lower yields, with a heightened focus on the carry profile of the expression. In our case, we see the 2s5s30s 50:50 butterfly – either in USTs or in SOFR swaps – as a positive-carry way to position for lower yields.

14 Mar 2025 NatWEST US: March FOMC meeting preview

The FOMC announcement is on Wednesday, March 19. The policy statement will be released at 2:00pm (EST), along with the projections materials (including a new dot plot and the SEP), and then Chairman Powell’s press conference at 2:30pm.

The main takeaways we expect include:

No change in interest rates (target funds range 4.25%-4.50%)

Limited changes to policy statement, dot plot and SEP economic projections

Powell to emphasize “wait-and-see” approach and uncertain outlook

We don’t expect any major fireworks from Wednesday’s FOMC meeting. The Fed is universally expected to hold its benchmark policy rate steady in the 4.25%-4.50% range. We think the Fed is likely to continue to signal a “wait and see” approach to near-term policy before deciding whether renewed rate cuts at a later date will be required….

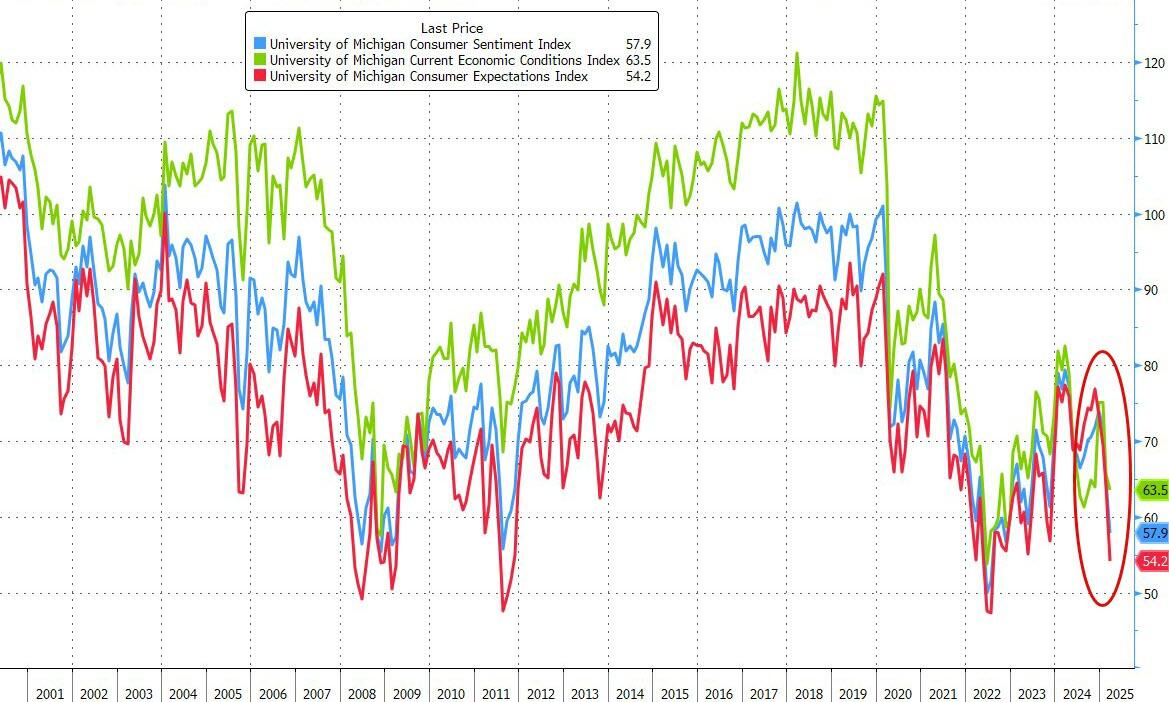

…The University of Michigan survey of consumers showed a surge in inflation expectations in February and March (3.9% a 32-year high). Unlike these consumer inflation expectations, market-based measures of inflation expectations have shown little net change recently. Chair Powell will likely sound hawkish on this fact, and emphasize that the Fed is carefully watching and will NOT allow expectations to drift up further.

This next note is an economic week ahead and I’ll bring forward the FOMC precap excerpt …

14 March 2025 UBS: US Economics Weekly | Uncertainty reigns and rains

…The Week Ahead: FOMC, the dots and data Our expectations for next week's FOMC meeting are recapped starting on page 2 in the Economic Comment this week. Next week, February retail sales should post an increase given the improvement in auto and light truck sales and our expectations for a consensus-like increase in sales at the control group of stores. Import prices will round out our core PCE tracking for February, which post-CPI and PPI currently sits at +0.34%. We'll receive a run of housing data including starts and permits. The first regional manufacturing surveys for March could also offer more signal for how firms are taking in trade policy uncertainty. On Friday, the January regional employment data could shed some light on the impact of the devastating California wildfires on employment. We also could have more proposed tariffs, or not…

Interrupting all of the FOMC precap for a quick sentiment review by the covered wagon folks …

March 14, 2025 Wells Fargo: Price Expectations Soar as Sentiment Sinks 48% of Respondents Spontaneously Mention Tariffs

Summary Consumer sentiment has not been this low since the high-inflation days of 2022. Unlike that era, however, consumers now see rising prices as more than passing phase. In a sign of this entrenched expectation, long-term inflation expectation rose to its highest since 1993.

The S&P 500 rebounded nicely today in the morning after falling into correction territory yesterday (chart). Was yesterday the bottom? It might have been based on sentiment indicators. On a fundamental basis, President Donald Trump (a.k.a., Tariff Man) didn't tweet about tariffs today after doubling down on Thursday. "I'm not going to bend at all," Trump said when asked about his tariff plans during an Oval Office meeting with NATO Secretary General Mark Rutte. Any day without a Trump tariff comment is a good day for the market. Also, today we learned that in an unsigned letter addressed to the US trade representative, Tesla said while it "supports" fair trade it was concerned US exporters were "exposed to disproportionate impacts" if other countries retaliated to tariffs.

The market is also rallying on relief that there won't be a government shutdown. Democratic Minority Leader Senator Chuck Schumer announced Thursday evening that he will support a Republican short-term funding bill that will effectively help avoid a government shutdown at the end of the day. This morning, Schumer explained that a government shutdown would give Trump and Musk's DOGE more power to lay off or fire more government workers and shutter federal agencies.

We will be more inclined to call a bottom when we see the stock market move higher on a day or days when Trump blusters about tariffs again. We know that on April 2 there will be lots of reciprocal tariffs imposed on many more nations by the administration, undoubtedly eliciting lots of comments from Tariff Man…

John Maynard Keynes is credited with saying, “When the facts change, I change my mind. What do you do, sir?” However, there is no definitive evidence that he actually said or wrote it.

Wall Street’s forecasting community (including us) is scrambling both to assess February’s weaker-than-expected batch of economic indicators for January and to reassess the likely near-term negative impact of Trump 2.0. The Citigroup Economic Surprise Index surprised most forecasters during the second half of last year with positive readings (Fig. 1 below). It has surprised them with slightly negative readings since February 20. We continue to bet on the resilience of the economy. However, we acknowledge that it is being severely stress-tested now by Trump 2.0’s tariff turmoil and shotgun approach to paring the federal workforce.

Figure 1

Perhaps the biggest surprise is that President Donald Trump wasn’t bluffing or even just exaggerating when he often said during his presidential campaign rallies that he loves tariffs. The widespread assumption was that his constant threat to raise tariffs was mostly a negotiating tool to force America’s major trading partners to lower their tariffs. However, he also often said that he viewed tariffs as a great way to raise revenues and to force US-based companies to move operations back to the United States.

President Trump talked about tariffs at the Inauguration Day parade held in the Capital One Arena in Washington, D.C. He said, “I always say tariffs are the most beautiful words to me in the dictionary.” He added that “God, religion, and love are actually the first three in that order, and then it’s tariffs.” That sounded like Trump’s typical bluster, positioning him to make deals to reduce other countries’ tariffs. But, apparently, he meant it: The man loves tariffs. He has even called himself “tariff man.”

On March 7, Commerce Secretary Howard Lutnick said, “We’re going to make the External Revenue Service replace the Internal Revenue Service.” In other words, revenues from tariffs will replace revenues from taxes on individuals and corporations. That’s simply dangerous and delusional nonsense. It certainly isn’t passing the sanity test in the US stock market…

… Strategy II: Time To Blink? Given all the above, it isn’t surprising that many forecasters are turning more cautious on the economic outlook. Some are lowering their outlook for GDP and their year-end forecasts for the S&P 500.

We respect the economists and strategists at Goldman Sachs. That’s because they have often agreed with our outlook for the economy and financial markets. They are data dependent, as we are. However, it seems to us that they tend to tweak their forecasts faster and more often in response to new data than we do because we tend to stick to our base-case scenarios longer. So their forecasts occasionally reflect the latest data points sooner than we do. We, on the other hand, tend to question data that don’t support our outlook. More often than not, this approach has worked for us, as subsequent data and/or revisions in the previous data often proved to support our narrative after all. In other words, Goldman’s view tends to determine the consensus outlook. We tend to stray occasionally…

… On the other hand, under the circumstances discussed above, we are lowering our forward P/E forecasts for the end of 2025 and 2026 to a range of 18-20, down from 18-22 (Fig. 12).

That lowers our best-case S&P 500 targets for the end of this year from 7000 to 6400 and for the end of next year from 8000 to 7200 (Fig. 13).

The worst-case scenarios using the same forward earnings and the same 18 forward P/E assumptions would be 5800 and 6500 for this year and next year….

… to continue reading, he directs one / all HERE (to his post on LinkedIN)

… Moving along TO a few other curated links from the intertubes, which I HOPE you’ll find useful …

First up, another instance where narratives FOLLOW ‘price’ …

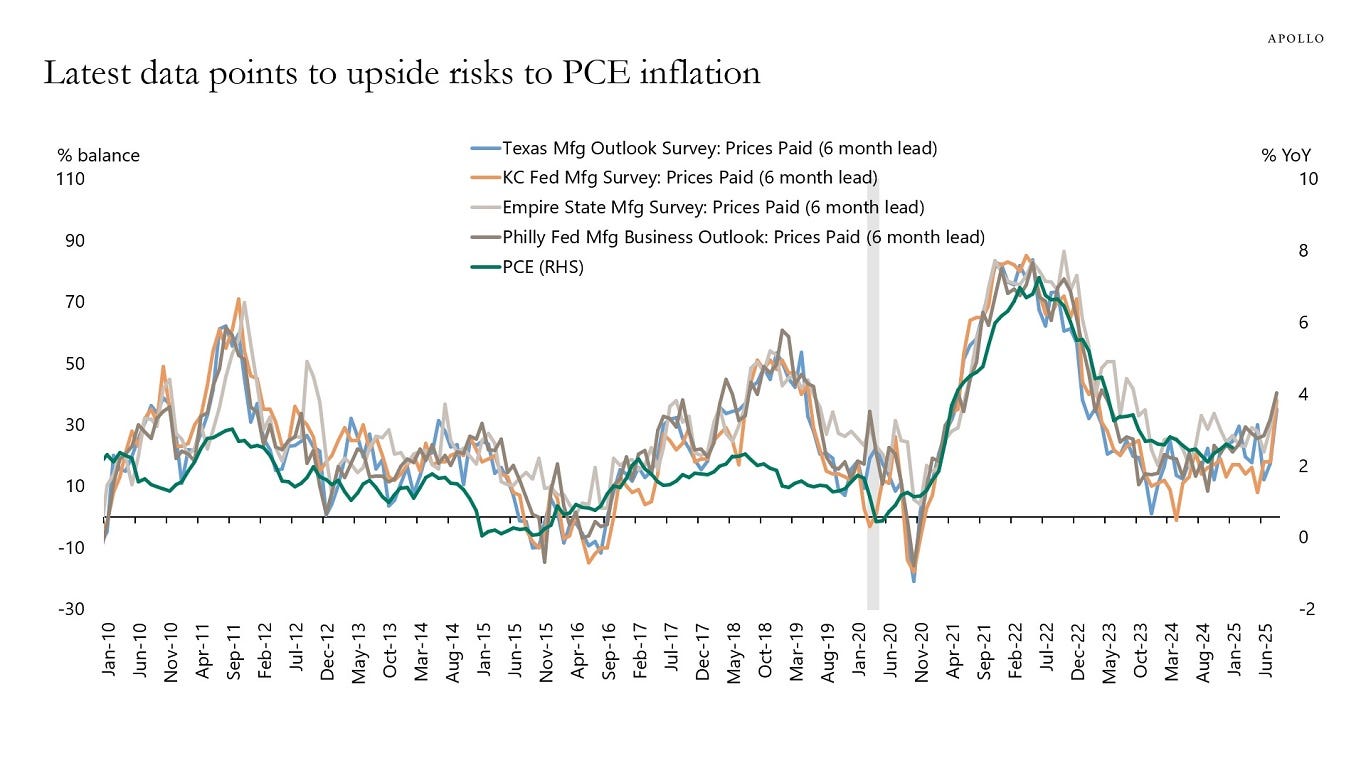

March 15, 2025 Apollo: Hard Data Starting to Weaken

Surveys of firms show that companies have in recent weeks started to pull back capex plans, and consumers are getting more worried about their jobs, see the first two charts below. At the same time, leading indicators point to higher inflation ahead, see the third chart.

Furthermore, airlines this week reported a slowdown in bookings, and the latest credit card data points to broad-based weakness across all categories except online sales.

The bottom line is that the soft data points to weakness coming in the hard data.In addition, this past week was the survey week for the March employment report, and with uncertainty elevated, the downside risks to March nonfarm payrolls—when it is released on Friday, April 4—are significant.

Our updated chart book with daily and weekly indicators for the US economy is available here.

Here’s a LONG READ (at least thats how the source describes it) and is from an economist at MS …

March 14, 2025, 10:17 am EDT Barrons: This Economist Sees Slowing Growth and Multiple Rate Cuts Ahead Ellen Zentner, chief economic strategist at Morgan Stanley Wealth Management, expects economic growth to slow due to tariffs and reduced immigration.

…What do you expect for interest-rate policy this year? We could see a Fed that is willing to make another rate adjustment as early as its May meeting. But the data would have to show an obvious, material weakening for the Fed to start to deliver more cuts.

Are multiple cuts in your forecast for the year? The Fed can deliver a couple of cuts. They can start as early as May. But again, the data, especially on the labor market, have to be markedly weaker over just a couple of prints. And then, it may be a one-off adjustment if, indeed, tariffs still haven’t gone into place.

If tariffs are coming through, if DOGE continues to ratchet tighter on federal employment, if households decide pent-up demand has been met and curb demand, and if GDP is closer to 1% than 2%, then the Fed will need to adjust rates. I would not be surprised if the Fed has to cut two to three times this year. I don’t think they need to adjust rates a tremendous amount. Barring a recession, I would be surprised if they cut rates below 3.5%….

This next link is a story that was out end of the week and, well …

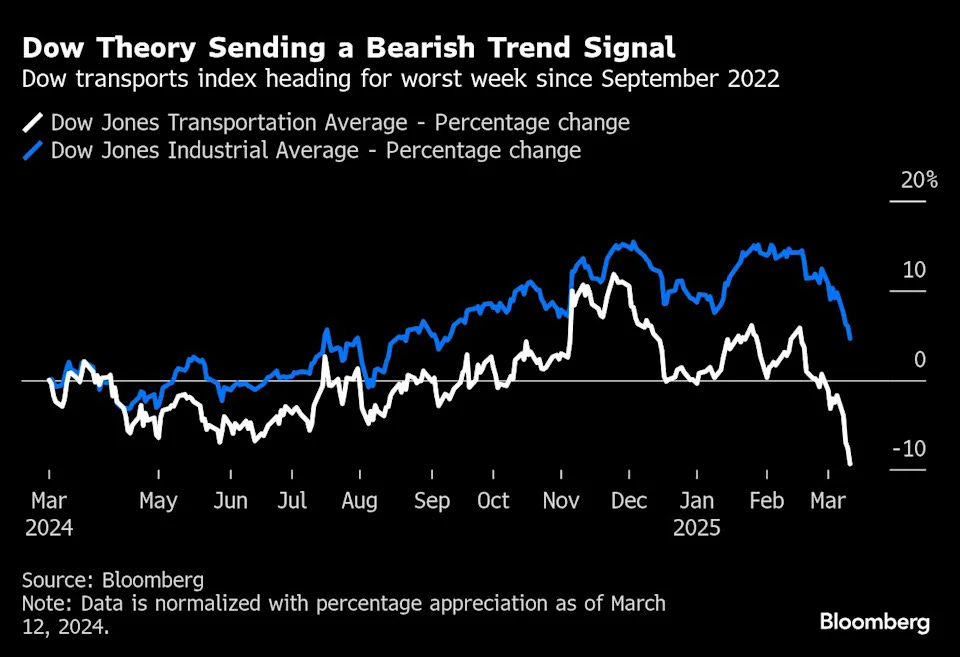

Fri, March 14, 2025 at 5:30 AM EDT Bloomberg: A Market Indicator From Early 1900s Is Blaring an Alarm for Stocks

(Bloomberg) — A century-old indicator that has helped predict the direction of the US stock market is signaling more pain ahead for battered investors.

Known as the Dow Theory, it holds that moves in the Dow Jones Industrial Average (^DJI) must be confirmed by transport stocks, and vice versa, to be sustained. As of Thursday’s close, the 20-member Dow Jones Transportation Average — a barometer of consumer and industrial demand — has slumped 19% from its November peak, teetering near so-called bear-market territory…

…“To make matters worse, its Dow Theory cousin — the Dow Jones Industrial Average — has also rolled over and violated the pullback lows from January, checking the box for a sell signal as the averages confirm the primary trend of the market is no longer higher,” he said.

Next up, gotta give credit TO credit SPREADS and per the rando visual from TWITTER …

at conradseric

Will credit SPREAD give credit to the trendline resistance?

…Propagating Price Pressure Plotting by Danielle DiMartino Booth

“Please allow me to introduce myself I’m a man of wealth and taste I’ve been around for a long, long year Stole many a man’s soul and faith”

—Sympathy for the Devil, by The Rolling Stones

Whoever controls the narrative… Such was the unoriginal thinking that drove a professor of law at the University of Ingolstadt, Bavaria, to hatch a secret society he called the Orden der Illuminati. In Adam Weishaupt’s mind, to be among the “Illuminated Ones” raised one above the muck of the monarch’s and especially the church’s brainwashing. And so it began in 1784, in a nearby forest. There, bathed in torchlight, five men crafted the rules of admission with the proviso that all candidates be of the highest societal standing, men of “wealth and taste,” to quote Mick and Keith in what many, myself included, agree is one of the best songs of all time. And like the iconic lyrics, seen to glamorize the darkest of figures, the Illuminati were castigated as atheists and anarchists….

… ut what of the truth about inflation? Last year, the founders of Truflation granted QI access to their full history of real-time daily inflation prints harvested using blockchain technology to collect and analyze 18 million data points from more than 60 data providers. The output was a .97 correlation with the headline US consumer price index (CPI). Per Truflation, on a time continuum, their metric tells you with near-perfect accuracy where the CPI will be 45 days hence. There was thus no irony in TJM Institutional Services’ Mark Gomez sharing first thing this morning that Truflation had printed at 1.32%, down from 2.70% when Federal Reserve policymakers last convened on January 31.

Zoom into the more recent history of Truflation and you can see that as recently as mid-December, the year-over-year (YoY) rate was as high as 3.11% on December 14. Understanding the drivers of both the upward and subsequent downward pressures to land at today’s 1.32% YoY is key to appreciating the simplicity of what’s played out in the CPI with a lag…

…Before leaving the subject of revisions behind, most in the media were quick to disregard (or didn’t take the time) to properly dissect what hit the wires alongside the “hot, hot, hot!” inflation data for January. Bloomberg’s Anna Wong, who has become a friend and is a refreshingly unbiased media economist, did do the legwork. Her takeaways are both cogent and materially alter the narrative:

Every February, the Bureau of Labor Statistics (BLS) re-estimates seasonal factors to include data from the previous year—this year, the re-estimation covers 2017–2024. This didn’t change non-seasonally adjusted values but changed the contour of seasonally adjusted CPI and core CPI.

The revisions strengthened the disinflation narrative for the second half of 2024. Both the three- and six-month annualized rates of core CPI for December 2024 were revised down to 3.1%, from 3.3% and 3.2% respectively.

Details of the report help us understand why the print was so strong, and none of them convinces us core CPI is in the midst of reheating. One obvious factor is residual seasonality—the idea that BLS’s seasonal factors haven’t properly accounted for typical January price gains.

As Wong rightly predicted, the surge in 2025’s first month was nearly fully reversed in February. At the headline level, CPI tumbled to 0.216% to the third decimal, less than half January’s 0.467% and an appreciable decline from December’s 0.365%. Meanwhile, the core rose 0.227%, exactly half of January’s 0.446% and lower than December’s 0.210%. Finally, the so-called supercore services gauge, on which the inflationistas have been fixated since Fed Chair Jerome Powell conjured the construct out of thin air last year, sank to 0.22% in February from the blistering 0.76% spike the prior month. As Wong noted, “It’s clear the disinflationary effect from softening services outweighed the uptick in goods inflation.” Bloomberg Economics’ proprietary nowcast for CPI pegs March CPI to come in at 2.5% YoY…

…Note that the same inflation expectations hysteria the media is hyping was evident in the University of Michigan’s (UMich) one-year and five-10-year expectations. And yet, we’ve seen scant follow-through in what the New York Fed has tracked via its Survey of Consumer Expectations. Convergence better describes what’s taken place in the last year. At work are two very fundamental influences on households. Per the NY Fed this past Monday, mean unemployment expectations “jumped 5.4 percentage points to 39.4%, its highest reading since September 2023. The share of households expecting a worse financial situation in one year from now rose to 27.4%, the highest level since November 2023.”

AND finally …

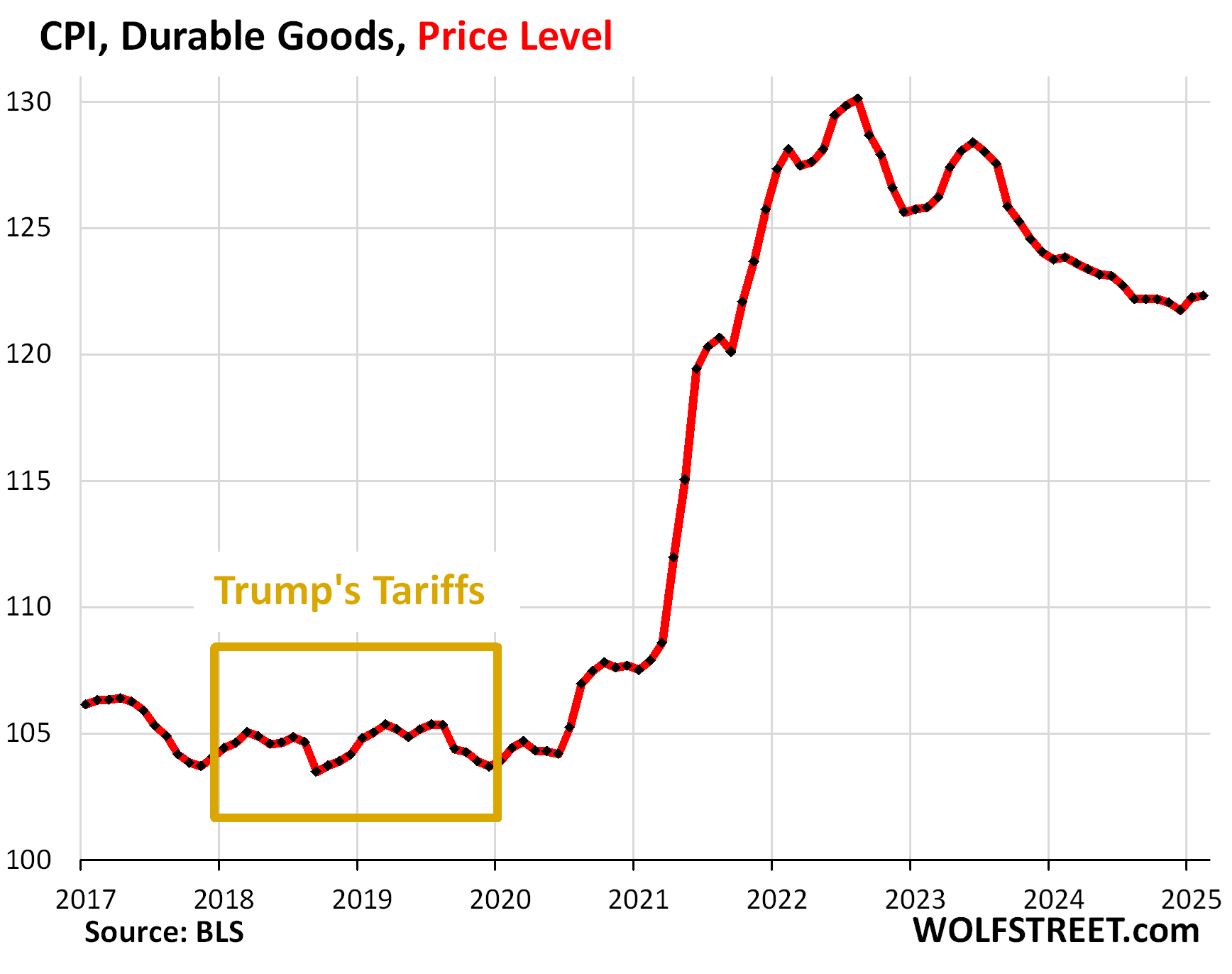

Mar 14, 2025 WolfST: Will Economic Detox Lead to a Recession? Maybe Not. But a Long Deep Stock Market Rout Will (See Dotcom Bust)

“We’re focused on the real economy,” Bessent said. “Ouch,” stocks said. Where did the Trump put go?

… Consumer durable goods would be hit the most by tariffs. This is the CPI for durable goods, shown as price level. There was no visible impact from tariffs in 2018 and 2019:

Even if a portion of the tariffs will get passed on to consumers, given that the economy is now in an inflationary environment, that portion, as Bessent said, will be a one-time bump…

…But even if a stock market rout comes along that is deep enough and long enough to trigger a recession, that short-term price may well be worth paying for the long-term risk-reduction that comes with sorting out the US fiscal mess and for the enormous long-term benefits of increasing manufacturing in the US.

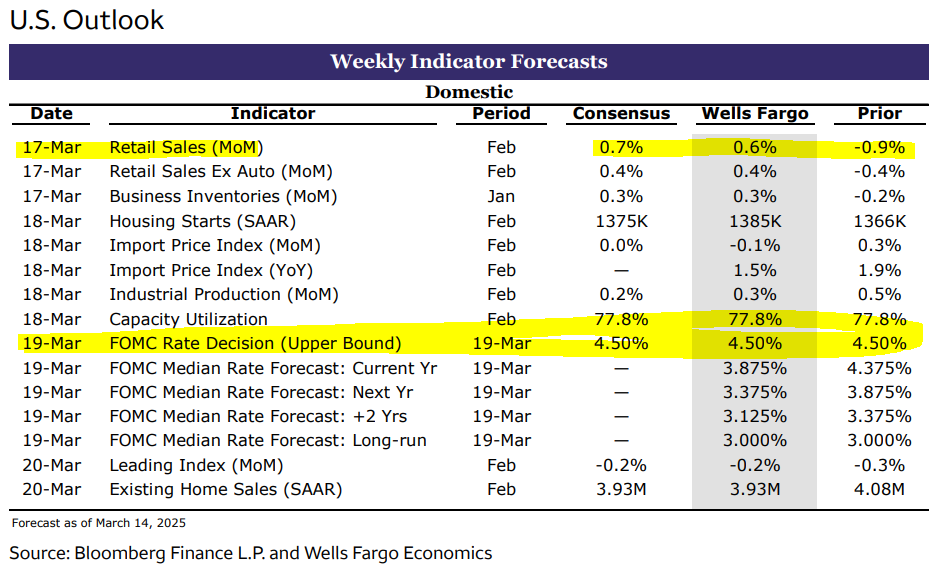

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

THAT is all for now. Will scour the inbox tomorrow at some point and send any / all relevant updates / links either ahead of futures open OR NOT (at which point, think Monday morning) … For now, nothing happens in markets without consequence … which of THESEare you …

{kind=link}

{kind=link}

{kind=link}