Good morning … Tariffs + Ukraine + Schumer Shutdown = X, please solve for X … But first, before we attempt high-level math, lets pause a moment and remember …

Published Fri, Mar 14 20089:34 AM EDT CNBC: Bear Stearns Gets Bailout From the Federal Reserve

The Federal Reserve agreed to provide emergency financing to Bear Stearns, after the investment bank said its cash position had deteriorated sharply in the past 24 hours.

The short-term financing from the Fed Bank of New York is being arranged through JPMorgan Chase. Bear said the financing is intended to help shore up confidence in its operations…

…On March 14, 2008, the Federal Reserve Bank of New York ("FRBNY") agreed to provide a $25 billion loan to Bear Stearns collateralized by unencumbered assets from Bear Stearns in order to provide Bear Stearns the liquidity for up to 28 days that the market was refusing to provide. Shortly thereafter, FRBNY had a change of heart and told Bear Stearns that the 28-day loan was unavailable to them.[22] The deal was then changed to where FRBNY would create a company (what would become Maiden Lane LLC) to buy $30 billion worth of Bear Stearns' assets, and Bear Stearns would be purchased by JPMorgan Chase in a stock swap worth $2 a share, or less than 7 percent of Bear Stearns' market value just two days before.[23] This sale price represented a staggering loss as its stock had traded at $172 a share as late as January 2007, and $93 a share as late as February 2008. Eventually, after renegotiating the purchase of Bear Stearns, Maiden Lane LLC was funded by a $29 billion first priority loan from FRBNY and a $1 billion subordinated loan from JPMorgan Chase, without further recourse to JPMorgan Chase.[24] The structure of the transaction, with both loans collateralized by securitized home mortgages[25] and with the JPMorgan Chase loan bearing losses before the FRBNY loan, meant that FRBNY could not seize or otherwise encumber JPMorgan Chase's assets if the underlying collateral became insufficient to repay the FRBNY loan.[25][26] Federal Reserve Chairman Ben Bernanke defended the bailout by stating that a bankruptcy of Bear Stearns would have affected the real economy and could have caused a "chaotic unwinding" of investments across US markets.[23][27]

… AND finally …

FRBNY: Press Release Summary of Terms and Conditions Regarding the JPMorgan Chase Facility March 24, 2008

The Federal Reserve Bank of New York ("New York Fed") has agreed to lend $29 billion in connection with the acquisition of The Bear Stearns Companies Inc. by JPMorgan Chase & Co.

The loan will be against a portfolio of $30 billion in assets of Bear Stearns, based on the value of the portfolio as marked to market by Bear Stearns on March 14, 2008.

JPMorgan Chase has agreed to provide $1 billion in funding in the form of a note that will be subordinated to the Federal Reserve note. The JPMorgan Chase note will be the first to absorb losses, if any, on the liquidation of the portfolio of assets…

Those were days that were some of the best of times (for me personally) and those days then led directly to some of the worst of times (for me personally as well as us all …). We move on and now back to our regularly scheduled programming. The Schumer Shutdown is … no more?

March 13, 2025 at 10:30 PM UTC Bloomberg: Schumer Says He Won’t Block GOP Bill to Avert Shutdown

… “I will vote to keep the government open and not shut it down,” Schumer announced on the Senate floor Thursday, adding that a shutdown “would give Donald Trump and Elon Musk carte blanche.” …

… and so some good news to then dwell on it as ‘bad’ … To illustrate what I mean, a quick look at 5yr yields with a TLINE I’ve etched in and am attempting to note it’s turning incrementally MORE important (and red = bearish) …

5yy DAILY: TLINE ~4.05% on the DAILY …

… momentum (stochastics, bottom panel) continues to point towards higher yields as path of least resistance but again, we know momentum can turn from overBOUGHT to overSOLD simply by the passing of time at a price …

… a TLINE break might be caused by some sort of calming of geopolitical tensions, tame tariff talk or some sort of dead feline sort of bounce in equities … whatever the case may be, a ‘dip-or-tunity’ (bonds vs 4.75%, 5s somewhat north of where they are here / now) may still be working it’s way towards a movie theater near you and I soon.

That said, I’ll quit while I’m behind and attempt to find something more funTERtaining over the weekend (time permitting) and move along TO how things shook out yesterday …

First up, PPI …

ZH: Core Producer Prices Tumbled Most Since COVID Lockdowns In February

… whatever happened to the idea of a concession and building it so they’d come? By days END … all was glittering …

ZH: Gold Spikes To Record High As Tariff-Tumult & Schumer-Shutdown Slam Stocks

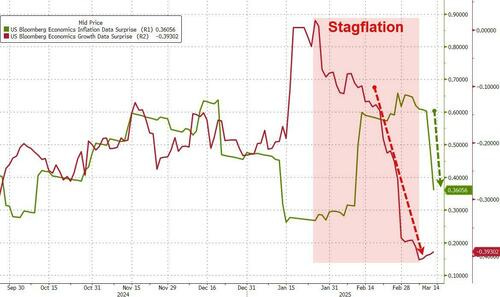

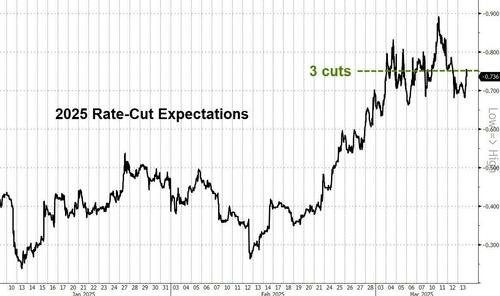

… Low PPI following yesterday's slow CPI combined with strong jobless claims data (all of which eased fears of stagflation), SHOULD have prompted some optimism...

...with market-implied rate expectations maintaining three cuts priced for the year

...so why are equity markets not reacting to the data (or worse, reacting to it negatively)?

As Goldman's Chris Hussey notes, stocks are forward-looking, and the two issues that are concerning investors most right now have not yet taken hold: AI and a tariff-driven growth slowdown.

Concerns about the durability of the AI trade that was set off by revelations from DeepSeek's low cost AI model only surfaced 7 weeks ago -- probably too soon for any company to change its capex plans or reconfigure its AI strategy.

As for tariffs, many of the bigger tariffs that have been announced (25% on Canada and Mexico) have still not gone into effect after they were paused twice. The next date for tariffs: April 2nd…

AND I’ll quit while I’m now far behind and so … here is a snapshot OF USTs as of 705a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWKUS Market Open: Spot Gold makes a fresh record high above USD 3000/oz & sentiment lifts ahead of Trump Executive Orders and UoM … USTs hold a slight downward bias, in-fitting peers; currently sitting in a 110-24 to 110-31 range. Some of the bearish action stems from the positive risk tone, as well as a weaker-than-average 30yr auction on Thursday. Trade updates on Thursday included President Trump noting he will not change his mind on the April 2nd tariffs. As for US Government shutdown developments, things seem to be improving with US Senate Minority Leader Schumer suggesting he will vote to keep the government open and not shut it down. Focus ahead will be on the US UoM survey and then Trump executive orders thereafter.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

FIRST UP, a couple things PPI (and so, PCE)related …

BMO: Headline PPI Unexpectedly Stalls but PCE Components Confirm Core-PCE Uptick

Headline PPI disappointed at 0.0% MoM in February vs. 0.3% MoM expected, but 0.4% MoM prior was revised up to 0.6% MoM. This brought the YoY pace down to 3.2% from an upwardly revised 3.7%. Core-PPI unexpectedly dropped, printing at -0.1% MoM vs. 0.3% MoM surveyed, but 0.3% MoM prior was revised up to 0.5% MoM. Within the details of the release, the PCE components were generally firmer. This reinforces the upside risks for core-PCE in February, and the market's expectations for a solid +0.3% monthly increase; albeit the risk that the figure rounds up to +0.4% remains on the radar…

First Trust: The Producer Price Index (PPI) Was Unchanged in February

The Producer Price Index (PPI) was unchanged in February, coming in below the consensus expected increase of 0.3%. Producer prices are up 3.2% versus a year ago.

Energy prices declined 1.2% in February, while food prices increased 1.7%. Producer prices excluding food and energy fell 0.1% in February but are up 3.4% versus a year ago.

In the past year, prices for goods are up 1.7%, while prices for services have increased 3.9%. Private capital equipment prices declined 0.1% in February but are up 4.3% in the past year.

Prices for intermediate processed goods rose 0.5% in February and are up 0.3% versus a year ago. Prices for intermediate unprocessed goods increased 1.3% in February and are up 10.5% versus a year ago.

Implications … Trade disputes, and specifically companies adapting purchasing plans as they try to make heads and tails of what may come next in this constantly shifting environment, will likely bring increased volatility to the data over the coming months. We will be focusing on the M2 measure of money, which is down from the peak in early 2022, as a guide to how inflation is likely to move as we progress through 2025. In employment news this morning, unemployment claims fell 2,000 last week to 220,000; continuing claims declined 27,000 to 1.870 million. These figures are consistent with continued job growth in March.

Our translation of this week's February CPI and PPI estimates points to a 0.36% m/m (2.8% y/y) rise in core PCE prices and a 0.33% m/m increase (2.5% y/y) for the headline index. Our Q4/Q4 core PCE forecast is unchanged at 3.2% following our forecast upgrade earlier today.

…Our 2025 Q4/Q4 core PCE forecast is unchanged at 3.2%, which is our new baseline forecast for this year. We revised our inflation projections higher earlier today after baking in higher tariffs to our new baseline. In particular, we now expect the US trade-weighted tariff rate to rise to 15% (from 10% previously assumed). This boosted our Q4/Q4 core PCE forecast higher by 40bp, to 3.2% in 2025; and lowered it by 0.1pp, to 2.2% next year. With tariff-related price pressures likely to start materializing in the next two to three months, we think the low-point for the annual rate will be 2.6% y/y in April 2025…

Equity investors holding out hope for a "Trump put" may be disappointed; during Trump's first term, the President's focus seemed to shift to markets only after tax, border security, and trade policy goals were mostly achieved; it's likely that we get a retread of the same this time.

Don't count on a "Trump put" coming to the market's rescue. We've heard plenty of speculation around a Presidential pivot on tariffs as stocks continue to get routed, but a look into Trump's active Twitter/X account during his first trade war suggests any such hopes may be misplaced. Tweets do not equate to policy. Nonetheless, we find it illustrative that mentions of the stock market were relatively quiet throughout the 2018 US tariff campaign against China and several equity selloffs during the same year (except for a pickup just ahead of the US midterm elections) but increased substantially around the back half of 2019. What changed? In our view, mid-2019 was when the Trump administration assessed it had achieved most of what was possible on key policy goals, including taxes and border security – even trade, if we consider the US-China "truce" in principle announced at G20 Osaka. Extrapolating that to today, we're inclined to believe the President and Treasury Secretary Bessent when talking down the "Trump put," and we expect that markets are likely to play second fiddle to primary policy goals until significant progress on the latter is achieved – similar to how it played out before.

…Despite continued evidence of sticky inflation, the prospects for a trade-war-driven economic downturn continue to limit the extent to which yields can backup. 10-year yields reached as high as 4.35% in the wake of Thursday’s data before an escalation of the trade war on Trump’s tariff threats against Europe triggered a risk-off tone that brought the benchmark rate back down to 4.25%…

… Safe-haven demand has played a key role in the anchoring of 10-year yields below 4.30% in recent weeks as forays above that level have repeatedly proven short-lived. With the S&P 500 entering correction territory, the bullish underpinnings associated with the risk-off tone have proven difficult to fade as the safe-haven premium in Treasuries remains elevated for the time being. That said, 10-year yields extended the local range top to 4.35% on Thursday, and we’ll be closely watching that level as initial support as attention begins to turn to next week’s events with the FOMC on Wednesday. If 4.35% is traded through, we’ll look for support at an opening gap from 4.396% to 4.400%. Conversely, initial resistance comes into play at the 200-day moving-average of 2.234% before the recent yield low of 4.10%…

A new production from a rather large German bank and this looks worthy of a point and a click …

13 March 2025 DB: Macro, Markets and Tech - A guide for CFOs and Corporates

We're pleased to share our second Guide for CFOs and Corporates, providing essential insights into macroeconomics, markets and technology. This report offers critical analysis and perspectives to help corporate clients navigate today's complex economic environment.

Key highlights:

Macroeconomic outlook: Global growth projections, central bank policies, key risks, and takeaways from EU defence spending and Germany's historic regime shift; including a table with our latest 2025 DB forecasts on growth, inflation, rates, and other key market metrics.

Market analysis: FX, funding costs, and commodity market risks and management strategies.

Geopolitics: Tariff impacts, global bifurcation, and CEO reaction functions.

AI's impact: Disruptive potential, business model impact, and implementation challenges.

… Same shop with a more macro review and some words on yesterday …

… The market sell-off resumed in earnest yesterday, with the S&P 500 (-1.39%) down to another 6-month low and into technical correction territory, with the index down -10.13% from its peak as recently as February 19. This is the first correction since October 2023, and Bloomberg reported that this was the seventh-fastest correction in data back to 1929, taking just 16 sessions for it to happen. Other asset classes also continued to struggle, with US HY spreads (+22bps) reaching their widest level since August, at 335bps. And as investors poured into perceived safe havens, gold prices (+1.85%) hit a record high of $2,989.

Once again, the main driver was a fresh volley of tariff threats from President Trump, who made several posts criticising the EU yesterday. In terms of the latest, President Trump said that if the EU continued with its 50% tariff on American whisky, then the US would respond with a 200% tariff on EU wines, champagnes and alcoholic products. That immediately caused issues for several European beverage companies, with Pernod Ricard (-3.97%) posting the worst performance in France’s CAC 40 yesterday, and Remy Cointreau (which produces cognac) fell -4.67%. More broadly though, President Trump’s comments reignited fears that the EU could soon face a much more serious trade escalation, particularly with reciprocal tariffs set for April 2. Indeed, earlier in his post on the 200% tariff, he described the EU as “one of the most hostile and abusive taxing and tariffing authorities in the World, which was formed for the sole purpose of taking advantage of the United States”. Bear in mind that President Trump has said he considers VAT to be like a tariff, so that could cause considerable issues for EU member states.

Matters weren’t helped yesterday by the potential threat of a US government shutdown, with funding set to run out at midnight tonight. However, after the US close, the Democratic Senate Minority Leader Chuck Schumer said that he would vote to advance the Republican bill rather than see a shutdown. So that’s helped futures to recover a decent amount of ground this morning, with those on the S&P 500 up +0.76%…

…Moreover, the decline for this week alone now stands at -4.31%, which if realised would be the worst weekly performance since the week of SVB’s collapse two years ago. As in recent days, the Magnificent 7 (-2.49%) led the declines, moving back into bear market territory having shed -20.25% since its December peak. And even though tech led the losses, it was still a broad-based decline, with the equal weighted S&P 500 (-1.00%) struggling as 78% of its constituents lost ground on the day…

And a few words on the global MACRO …

March 13, 2025 MS: Global Macro Commentary: March 13

S&P 500 enters a technical correction; soft PPI with firm PCE translation; USTs gain as risk sentiment deteriorates; BoJ's Ueda sees wages improving; EUR and SEK retrace some recent strength; Indonesia posts budget deficit; DXY at 103.85 (0.2%); US 10y at 4.268% (+4.4bp)

S&P 500 (-1.4%) enters a technical correction as it closes more than 10% below its February peak as policy uncertainty and recession fears continue to weigh on sentiment.

US economic data are mixed; PPI data surprises to the downside, but components that feed into PCE remain firm, while Jobless Claims continue to fall, easing fears around labor market weakness.

Though USTs briefly cheapen as PPI data pushes up PCE estimates, growth concerns, equity losses, and a potential government shutdown dampen risk-sentiment, spurring a rally across the curve (5y: -4bp)…

…USTs briefly cheapened given the firm PCE forecasts and fall in jobless claims, however the risk-environment and decline in US equities quickly sent UST yields back down, and USTs rallied into the NY afternoon. The sizeable rally led to a poor set up for the 30y auction, and accordingly the auction was weak with a 1.1bp tail. The demand was below average with a bid-to-cover ratio of 2.37x (P: 2.33x; 1y Average: 2.43x). The bright spot was demand from direct participants who, similar to the other auctions this week, had an above-average allotment of 23% (P: 19%; 1y Average: 18%). However, this was offset by a sharp fall in allotment to indirect participants to 60% (P: 65%; 1y Average: 67%), which left primary dealers with 17% (P: 16%; 1y Average: 15%).

After the disappointing auction, USTs pared some of their gains, and closed away from session highs. however, the flight-to-quality bids kept UST yields ~3-4bp lower d/d as STIR repriced slightly lower. With growth concerns and tariff uncertainty remaining at the forefront, consumer sentiment data released on Friday will be key in understanding how consumers are viewing recent developments and if inflation expectations continue to rise.

… same shop with a WEEKLY review / preview of economy with especially noteworthy topic …

March 14, 2025 08:00 AM GMT MS: US Economics Weekly: How GDP Trackers Stack Up

GDP trackers have diverged, causing confusion. We think this comes from 1) methodological differences, 2) gold imports that are an extreme outlier from a historical context, and 3) the front-loading of non-gold imports that has yet to firmly show up in inventories or spending.

Key takeaways

We re-introduce our Morgan Stanley US GDP tracker. We are currently tracking 1.4% growth for Q1 (q/q saar).

The Atlanta Fed GDPNow is signalling recession (-2,4%) while the FRBNY Nowcast shows acceleration (2.7%).

GDP trackers differ in methodology and have been thrown off track by gold imports on an unprecedented scale.

Imports ex-gold exhibit front-running effects, but where they have gone (spending or investment) is a mystery.

The recurring risk of a US government shutdown has receded, with some Democrat senators looking to advance legislation. Against the backdrop of damage to “animal spirits” from erratic government policy and taxes, the potential for economic damage from a shutdown would be larger and longer lasting.

The US March Michigan consumer sentiment poll is due. The Michigan data does at least break out political partisanship. Democrats’ pessimism is equivalent to that during the 2008 global financial crisis. Republicans’ optimism is stable. If Republican sentiment starts to waver that might signal economic concerns are penetrating partisan presentation.

US President Trump suggested extremely aggressive tax increases for US consumers of imported alcohol, with a 200% tariff on European products. Tariff calculations have changed over time, but in scale and target this tax is similar to the eighteenth century UK trade taxes. Those taxes led to a massive increase in smuggling. The economic impact of tariffs tends to decay over time—either because supply chains reroute (per China’s response), or in extreme cases because smuggling increases…

… a MONTHLY economic outlook …

March 13, 2025 Wells Fargo: U.S. Economic Outlook: March 2025 Economy Entered 2025 with Momentum but Policy Uncertainty Weighs on the Outlook

Economy Entered 2025 with Momentum, but Policy Uncertainty Weighs on the Outlook

The U.S. economy entered 2025 with a fair amount of momentum. However, GDP growth in the first quarter of the year looks to be soft. Real consumer spending declined in January, although the weakness may be attributable, at least in part, to bad weather.

Furthermore, the surge in imports in January, which mechanically reduce GDP (everything else equal), will also weigh on output growth in Q1. In our view, the surge in imports reflects front-running ahead of potential increases in tariff rates.

Tariff announcements have come and gone in recent weeks. In terms of our forecast, we assume that the 20% tariff on China will remain in place through the end of our forecast period (Q4-2026). We are also assuming a 10% effective tariff on the European Union along with effective tariff rates of 5% on Mexico and Canada as well as on countries in the rest of the world. In each case, we assume that foreign countries will retaliate on the United States with their own equivalent tariffs.

In our view, these assumptions strike a reasonable balance between upside and downside risks. Notably, these assumptions, which are based on the ebb and flow of tariff announcements in recent weeks, are not meaningfully different from the assumptions we have been using over the past few months.

We look for real GDP growth to downshift in the second half of 2025 as tariff hikes lead to a modest uptick in inflation that erodes growth in real income, which weighs on growth in real consumer spending.

We think the FOMC will "look through" the one-off tariff-induced increase in the price level and refrain from tightening monetary policy. Indeed, we have added an additional 25 bps rate cut to our outlook due to the softer labor market conditions we expect by midyear. We look for the FOMC to cut rates by 25 bps at each of its policy meetings in June, September and December.

We readily acknowledge that uncertainty related to tariffs and reductions in federal government employment amid signs of slowing growth raise the probability of an economic downturn this year, but it is not our base-case scenario, because the underlying fundamentals of the U.S. economy generally remain healthy.

Finally, Dr Bond Vigilante (fresh off a week with his downgraded S&P tgt), tacklin’ question we’re all asking …

Mar 13, 2025 Yardeni: Why Cooler Inflation Isn't Lifting Markets

February's inflation data provided conflicting stories. Both the CPI and PPI came in cooler than expected, but neither cheered the stock and bond markets. That's because the components of both gauges that feed into the Fed's preferred PCED inflation rate were actually a bit hotter. In addition, January's PPI increase was revised up from 0.4% to 0.6%. So it's unlikely that the Fed will lower the federal funds rate (FFR) anytime soon even if economic growth slows.

It won't be until March, or perhaps even sometime during Q2, that Trump's tariffs start to boost the inflation data. But in the meantime, goods inflation did decelerate in February. The final demand goods PPI fell back below 2.0% y/y to 1.7% y/y despite egg prices soaring 54%, which accounted for two-thirds of the 0.3% m/m increase…

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

First up, some REALLY great news …

March 13,2025 AAA: Gas Prices Dip as Spring Break Travel Heats Up

WASHINGTON, DC (March 13, 2025) – Despite increased demand, gas prices dipped lower this week, with today’s national average at $3.07 per gallon, about 3 cents lower than a week ago. This drop at the pump comes as many travelers gear up to hit the road for spring break and drivers may be surprised to find gas under $3 in 31 states.

From The Terminal — BTFD …

Fri, March 14, 2025 at 5:57 AM EDT Bloomberg: BofA Says Policy Moves to Keep Stocks Away From Bear Market

(Bloomberg) -- The slump in US stocks is likely to prompt policy intervention from President Donald Trump as well as the Federal Reserve, Bank of America Corp.’s Michael Hartnett said…

… “We say this is a correction, not a bear market in US stocks,” the strategist wrote. “Since equity bear threatens recession, fresh declines in stock prices will provoke flip in trade and monetary policy.” Even so, he reiterated his preference for international equities over the US this year…

AND … an OpED from THE Terminal …

March 14, 2025 at 5:01 AM UTC Bloomberg: Strategists' forecasts need a correction of their own It’s still a long way to the top if you mark to market.

… Kostin makes clear that the big question is whether there will be a recession. If so — and strategists didn’t expect it three months ago — then the stock market is likely to fall further. If not, it’s still a long way to the top, but the chances are that this will turn out to be a buying opportunity:

Historically, the median peak-to-trough decline in S&P 500 earnings during 12 economic downturns since WWII equals 13%. During recessions, the index level typically declines by 24% from its peak. Outside of a recession, history shows that S&P 500 drawdowns are usually good buying opportunities if the economy and earnings continue to grow, which is our base-case scenario.

At this point, Kostin’s adjustment is a mark to market, and makes the assumption that a much more aggressive tariff policy has been priced in. The projected gain for the rest of the year is barely changed from the growth predicted from a higher base on Jan. 1. The likelihood is that other strategists will follow, and that this will dent sentiment further. And the bottom line remains the direction of the economy. It’s not a coincidence that the key for the latest leg of this selloff appears to have been President Donald Trump’s reluctance to predict that a recession would be avoided.

And finally: I really dislike the word “correction,” and particularly the notion that it means a 10% fall from peak to trough. That 10% number is arbitrary. If the market was massively overvalued in the first place, a 10% drawdown won’t correct it. The word implies that the market is now correct, which is a dangerous assumption. To take one measure that admittedly makes this market look particularly expensive, the S&P 500 still trades at a higher multiple of sales than at the top of the dot-com bubble in 2000. That multiple may or may not prove to be justified, but there’s no obvious reason to believe that US stocks are now “correctly” valued:

The market has fallen fast, looks oversold on many measures, and may well be ready to bounce. But we should attach minimal significance to the fact that its fall is now in double figures. It really doesn’t matter.

Finally, a few words from Wolfy on PPI

WolfST: It’s Again the Hefty Up-Revisions that Heat PPI Inflation: Been Happening Month after Month January was up-revised to worst increase since August 2023, PPI inflation doubling in 12 months. February unchanged, waiting for up-revision.