Good morning … #GotBONDS? Want some? Yesterday was one of those where if you gave me the data ahead of time, I’d likely have mucked up the ‘trade’. That said, lets jump in …

30yy DAILY: watching an area (noted) up nearer 4.75% (just north of 50dMA)…

… momentum has been a good indicator here and kept us on the right side of this current tick HIGHER from approx 4.40% … It’s not yet suggesting any yield top but certainly worked off overBOUGHT’ness … I’d be looking to put some hay in the barn into any further pre-auction concession (aka dipORtunity) … i’m not FORCED though … just a thought…

… far more in as far as technicals and levels (from those forced to be bullish) below. Seems to ME that here and now, we’re forced to shift (some of) our attention from tariffs TO a government shut down …

Bloomberg: Stock Futures Decline as Growth Worries Persist

… on the positive side of ‘things’, a slowdown (tariff or shutdown induced) will bring with it … well … less demand for things …

Bloomberg: Trade War Erodes Oil Demand as OPEC+ Boosts Supply, IEA Says

CPI set the table for the 10yr auction (I know, it’s cute that I’m referencing funDUHmental data and supply / demand things at a time like this) …

ZH: Core Consumer Price Inflation Slowest In 4 Years As Energy & Airfare Costs Tumble

CalculatedRISK: BLS: CPI Increased 0.2% in February; Core CPI increased 0.2% CalculatedRISK: YoY Measures of Inflation: Services, Goods and Shelter

More below from all those who would certainly have predicted a lower than expected point of data to be followed by HIGHER (been down so long they look up?) RATES (not to be confused with being ‘forced’ by mkts into bullish view as momentum remained pointing towards HIGHER yields) … and from there we went TO the afternoon supply dance …

ZH: Solid 10Y Auction Enjoys First Stop-Through Of 2025

…Overall, a solid if hardly spectacular stopping through auction, which is probably good news for a day when many were worried that a hot CPI print could lead to sharply higher yields and a far uglier auction.

… with 10s out the way, we’ve now cleared path for this afternoons 30yr auction and before you are ‘forced’ to be bullish, well, measure twice and cut once? Keep your friends close, your stops closer? DipORtunity at hand?

Oh, forget it … again, much more below from YESTERDAYS NOTE from the very best techAmentalists in the biz … Yesterday, though, in a nutshell …

ZH: Bond Yields, Big-Tech, Bullion, & Black Gold Bounce As Stagflation Fears Ease

… here is a snapshot OF USTs as of 705a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWKUS Market Open: US equity futures are mixed & USD steady ahead of US PPI & geopolitical updates … Bunds are modestly lower awaiting the Bundestag debate while USTs look to PPI and shutdown developments … USTs are flat, after spending the early portion of the morning a little firmer following a strong 10yr auction, which garnered strong demand with a stop-through of 0.5bps. Back to today, US paper has held a downward bias, in tandem with pressure seen in Bunds. Focus today will be on the US PPI, where some components will feed into the US PCE metric. Sentiment has also taken a slight hit following updates out of Washington; US Senate Democratic Leader Schumer said Senate Republicans do not have the votes to approve the House-passed government spending bill without amendments. On the supply front, a 30yr auction is due.

Yield Hunting Daily Note | March 12, 2025 | CPI Day, JEQ Into ASGI + Tender!, KIO/VBF Notes. Buffer Ideas.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

First up, everything CPI-related …

ABN AMRO: US inflation more than meets the eye, but tariffs less so

The US economy saw two significant developments today. The next step in Trump’s trade war came into force, with the US imposing 25% tariffs on all steel and aluminium imports. Many of its major trading partners, including the EU, announced retaliation. This afternoon, we got a CPI inflation release that surprised to the downside, with 0.2% m/m gains of both headline and core inflation, while consensus expected 0.3% m/m. The tariffs are bad news, but perhaps not as bad as the headline suggest, while the inflation reading is good news, but perhaps not as good as the headline figure suggests…

BAML: February CPI inflation: it’s the details that matter

A softer than expected print for the top line numbers February headline and core CPI inflation printed below consensus and our expectations. Both came in at 0.2% m/m resulting in the y/y rates falling by 2-tenths to 2.8% y/y for headline CPI and 3.1% for core. That said, the details were less favorable for the Fed’s preferred inflation measure—PCE inflation, which led markets to reduce the likelihood of Fed cuts in the near-term and reinforcing our view that the Fed will remain on hold.

Softer services helped by a large drop in airfares…

Potential tariff effects.. more to come? …

PCE read-through suggests stalling progress …

Initial PCE read-through keeps the Fed on hold The PCE inflation read-through is unwelcome news for the Fed as it provides more evidence that inflation is moving sideways. It also supports our view that the Fed is likely to stay on hold this year unless activity data shows a material weakening. Even if the data weakens, the Fed will have to balance that against upside risks to inflation from tariffs and a potential deanchoring of inflation expectations. The bottom line is that no change in policy rates remains the most likely outcome in our view.

Core CPI slowed 22bp to 0.23% m/m SA (3.1% y/y), largely aided by a deceleration in core services inflation. Headline inflation also benefited from a lower impulse from energy and food prices, which rose just 0.22% m/m (2.8% y/y). However, the core PCE translation is higher, at 0.33% m/m (2.7% y/y)…

…Overall, we view the February CPI data favorably. The slowing in rents and OER CPI was more than we had expected, but the direction of travel seems to be consistent with our baseline outlook of a slowing toward their pre-pandemic run rate (0.25-0.30% m/m) by mid-2025. In addition, the nice payback registered across a slew of core services categories after the January surge confirms that the uptick in the prior month was indeed a one-off, likely an annual price-reset, and not indicative of persistent inflation. We think it is too early to parse the data for tariff effects, although some of the categories that we expect to be affected by China tariffs (household furnishing, apparel and "other goods") did see price increases.

Core CPI inflation decelerated 22bp, to 0.23% m/m (3.1% y/y), in February, almost entirely reversing the 24bp uptick in January, helped by core services prices. We revise our 2025 core inflation forecast higher to 3.6% y/y (+0.3pp), after baking in more tariffs in our baseline.

While subtle, we thought the February CPI report reflected some early signs of tariff pass-through.

Weakness in several typically volatile services categories pulled the overall print below expectations. Still, given signs of falling consumer confidence, these discretionary spending categories will be worth monitoring.

Inversely to January, we think PCE inflation may print relatively stronger than CPI for February – we pencil in a preliminary 0.32% m/m core forecast. PPI on 13 March will be key in determining our final PCE forecast.

BMO: Core-CPI +0.227%, Supercore +0.215%, TSY Dismiss as old info

…The most interesting aspect of the release isn't the data itself, which was bond-friendly, but rather the market's lack of follow-through. While there was an initial kneejerk bid to the headlines, the buying interest quickly faded as investors refocused on the potential reflationary implications from the trade war. This is the first time in the cycle in which such a benign inflation print has been completely discounted in favor of other risks…

Brean Economics Commentary: CPI rose by less than expected in February

Key Takeaways: This CPI report was better than expected from the Fed’s perspective as the 12-month core inflation rate dipped to 3.1% in February, which was the lowest reading on this metric since April 2021. The core index increased 0.2% in the month but this is a reading from the pre-tariff economy. Headline CPI inflation also dipped more than expected being helped out not only by lower than expected core prices but also by unchanged prices for food at home even as egg prices rose a further 10.4% in February (and are up 58.8% over the last 12 months). Core commodity prices on a year-over-year basis were down 0.1% in price, which was the same as January, but this is an area most likely to boosted by tariffs. With the three- and six-month core inflation rates both at 3.6%, we expect Fed officials to stay away from mentioning higher frequency rates and focus on the improvement in the 12-month inflation rate and we think they will be happy to take the good news for now. Were it not for tariffs, this report would be a promising one in terms of showing renewed progress on disinflation…

DB Feb CPI recap: Core PCE might not benefit from CPI's downdraft

Both headline (+0.22% vs. 0.47% in January) and core (vs +0.23% vs. +0.45%) CPI came in slightly softer than our expectations. The year-over-year rate for headline and core fell two-tenths, the former to 2.8% and the latter to 3.1%. Shorter-term trends in core improved, with the three-month annualized change falling two-tenths to 3.6%, while the six-month annualized rate fell a tenth to 3.6%.

In terms of the breakdown, gains in core goods remained on the firmer side with (seasonally adjusted) strength in used cars and trucks as well as positive payback in apparel after last month’s weak print. On the services side, a 4% decline in airfares masked some strength in other service components.

While the CPI reading was slightly softer than expected, the readthrough into core PCE is somewhat less benign. A pickup in food away inflation will feed through into core PCE while the weakness in CPI airfares will not. As such, the details in tomorrow’s PPI will be heavily scrutinized.

With respect to the near-term outlook, the biggest risk remains tariff policy. The textbook response to prices level effects is to “look through” it, though discerning in real time how much of any price increases are a function of tariffs and how much are organic price pressures will be difficult, especially with some evidence that inflation expectations may not be reliably anchored.

At the same time, uncertainty around economic policy may prove paralyzing for consumers and businesses, which presents downside risks to a labor market that has held in so far because of low firing rates. While our baseline view for the Fed, which we adopted shortly after the election last November, continues to see the policy rate on hold this year in response to resilient growth and sticky inflation, there are compelling arguments to the both the hawkish and the dovish side (see “How should the Fed respond to an economy in ‘transition’?”).

First Trust: The Consumer Price Index (CPI) Rose 0.2% in February

The Consumer Price Index (CPI) rose 0.2% in February, below the consensus +0.3%. The CPI is up 2.8% from a year ago.

Energy and food prices both increased 0.2% in February. The “core” CPI, which excludes food and energy, increased 0.2% in February, below the consensus expected +0.3%. Core prices are up 3.1% versus a year ago.

Real average hourly earnings – the cash earnings of all workers, adjusted for inflation – rose 0.1% in February and are up 1.2% in the past year. Real average weekly earnings are up 0.7% in the past year.

Implications … a subset category of prices that Fed Chair Jerome Powell said back in November 2022, “may be the most important category for understanding the future evolution of core inflation” – known as the “Supercore” (which excludes food, energy, other goods, and housing rents) – has been running hotter than headline and core inflation, up 3.8% in the past year. The good news is this measure rose 0.2% in February. Still, no matter which way you cut it, inflation continues running above the Fed’s 2.0% target. While this month’s inflation report is an improvement, one month of data does not make a trend. We expect the Fed to remain on hold until inflation renews its long and winding march toward 2.0%, or the economy slows substantially.

ING US inflationcools, but tariffs threaten higher prints in coming months

Good news on inflation, but the fact it was overwhelming caused by falling airfares has muted the market reaction. Tariff fears are already seeing companies nudging prices higher and risk higher inflation readings over the summer…

RBC: February's modest rise in core CPI helps Fed's optionality

The Bottom Line:

Core CPI moderated in February, in-line with our expectations and proving that seasonal spikes were a January effect this year. February data indicated that inflation expectations in consumer surveys were overblown. But this divergence highlights a key yellow flag emerging in the US economy – a divergence between “soft” sentiment data and hard data.

The pace of core services halved relative to a month ago and a sizable decline in airfares contributed to this. We are watching demand for travel as a leading indicator of higher-income households paring back spending. Hotel prices also moderated this month suggesting travel demand is fading.

Additionally, we have witnessed a spike in year-over-year used car prices in contrast to the continued declines in prices for new cars. We are watching closely to see if the recent retracement on the stock market results in a pullback from high-income consumers.

Still, this morning’s data adds to our conviction that the Fed will keep rates on hold at next week’s meeting as the y/y pace of core inflation remained elevated at 3.1% and the unemployment rate remained low at 4.1%. But a moderation in inflationary pressures alongside a softer trajectory for employment data (thanks to DOGE layoffs and education hiring freezes) shifts the balance of risks, providing a potential cutting bias if the labor market continues to weaken.

…We expect next month’s March release to show more slowing in both headline and core CPI. Currently we project the headline CPI to decline (-0.04% seasonally adjusted; +23bp NSA) and the core CPI to increase around 20bp (seasonally adjusted).

12-month headline CPI inflation is projected to slip to 2.4% next month and core CPI inflation is projected to edge down to 2.9%. Both headline and core CPI inflation are projected to see see little further slowing over the remainder of 2025, with even a slight pickup in May through July…

Summary The Consumer Price Index came in slightly softer than expected, with both the headline and core indices advancing 0.2% in February. Slower growth in food and energy costs, as well as an easing in core goods and services inflation, helped overall price growth cool. The outturn is a welcome development after January's unexpectedly strong print.

Stepping back from the month-to-month noise, inflation has essentially moved sideways since early 2024. New and potential tariffs are poised to stoke goods inflation in the coming months, which is unlikely to be offset by further slowing in shelter and other services inflation.

With today's data in hand, we expect the core PCE deflator to increase around 0.35% in February, which would keep the Fed's preferred inflation measure running closer to 3% than its 2% goal. This presents a challenging situation for the FOMC, but we expect the Committee to respond with a gradual pace of monetary policy easing later this year amid slower growth and a somewhat softer labor market.

…. moving on to all other things from the Global Wall inbox …

The US decision to proceed with a planned 25% tariff on all imports of steel and aluminium triggered an immediate retaliation by the EU, targeted at politically sensitive US exports. Though the tariffs cover all US imports, this is the first that brings the EU directly into the fray. There are two key things to note about these tariffs.

Next up a few words on how markets love of uncertainty impacting one shops FOMC call (ie UPDATE!! added another rate cut TO f’cast — now thinking 2 vs just one, so, still some room to be ‘marked to market’) …

We lower our GDP growth and raise our inflation projections for 2025 due to higher tariffs and a surge in trade policy uncertainty. The softer labor market causes us to add another rate cut, despite higher inflation. We now think the FOMC will cut rates 25bp twice this year, in June and September.

… We now expect the FOMC to lower rates 25bp twice this year, in June and in September. We added another rate cut to our previous baseline that assumed one rate cut in June. For 2026, we expect three 25bp rate cuts, in March, June and September.

Recent de-rating fastest since 2022 amid growth concerns; Big Tech cheapest in almost 2Y and SPX ex-Tech at fair value; valuations look reasonable as we await clarity on US policy chaos; still like Healthcare here, and Big Tech long term; SPX breaking below 20x signals more trouble ahead.

…Worst de-rating since 2022 as recession concerns return... Looking to 2/19/25 as the local peak for SPX, we compared current multiple compression against peak-to-trough declines of at least 5% since the 2022 bear market, finding that the current P/E washout is the fastest and most severe of the last 3 years.

We point out that positioning was not overly extended this time, whereas prior (near-)corrections were preceded by record SPX futures positioning among LOs, extended systematic equity longs and downside asymmetry in CTA flows (see our Aug '23, Apr '24 and Jul '24 positioning analyses). We think this frames the current pullback as less of a technical unwind and more of a fundamental reassessment of the growth outlook amid a significant increase in economic and policy uncertainty. Note that both equity and credit risk premiums have inflected higher over the last few weeks while Treasury term premium (which had been rising since September as safe haven demand evaporated) has declined.

Lookin’ back in effort to learn from history and help then choose a path forward …

March 12, 2025 BMO Close: Looking Back to Look Forward

Treasuries sold off on Wednesday despite a surprisingly benign core-CPI gain of 0.2% (0.227%), a tenth of a percent less than economists expected. As the post-CPI bid quickly faded and the inevitable process of ‘explanations chasing price action’ got underway, the most frequently cited exposition was that the sourcing data wouldn’t feed through to a softer move in core-PCE. Particularly given the formulaic differences between the two series, and the risk that core goods put more upward pressure on the Fed’s preferred measure of inflation than it did the core-CPI series. Beyond the core-PCE argument, the cheapening was also credited to positioning, supply implications, and an unwind of safe-haven flows as equity futures bounced ahead of the cash open. Despite the credibility of these explanations, it certainly isn’t wasted on us that for the first time in the cycle, such a benign inflation print has been completely discounted in favor of other risks. If anything, the price action speaks to the market’s preoccupation with the forward risks associated with the Trump Administration’s agenda, as investors deemphasize February’s data as old information. After all, there was no concrete evidence of tariffs within the details of February’s CPI report…

…Despite the sharp increase in volatility over the last several weeks and entrenchment of uncertainty among investors in US rates, end-user demand has remained solid in the primary market for Treasuries. Today’s 10-year auction stopped 0.4 bp below where the WI yield was trading at the bidding deadline, and non-dealers took a fairly typical share of the issue at 86.9%. 10-year notes have since been comfortable trading on both sides of the auction stop (4.310%), as the choppy price action that’s come to define the price action in US rates persists. While the 4.25% interim anchor remains intact for the time being, yields have been approaching the local range top of 4.342%. As a result, we’ll be watchful of a potential breakout higher in yields as the balance of the week unfolds. Note that if the 4.342% level is breached, there is little in the way of support in the path toward the 100-day moving average of 4.412%. Conversely, if yields drop back below 4.25%, the 200-day moving average comes into play at 4.235%. Below that level is the 2025 low yield close of 4.155%, before the YTD low mark of 4.104%.

A note that glitters …

12/03/2025 BNP Gold: Prices flying in the face of chaos

Gold forecast upgrade on elevated economic uncertainty: We raise our average 2025 forecast by 8%, and expect gold prices to push above USD3,100/oz during Q2 2025.

Trump tariff chaos and geopolitical shifts support gold prices: The Trump administration issuing a slew of tariff threats and the realigning of international relationships have added a new layer of macroeconomic and geopolitical uncertainty, providing a significant boost to gold.

Tariffs fears have dramatically tightened physical gold market: Physical tightness due to the surge in demand for moving gold into the US ahead of tariffs, a pick-up in central bank buying and an acceleration in physically-backed ETF gold demand have been key YTD gold price supportive factors, and we expect this to continue through 2025.

Chinese investors and PBoC still favouring gold: The return of PBoC gold buying in November 2024 after a six-month hiatus has, in our view, bolstered Chinese retail investor interest, and this is likely to support Chinese gold imports in 2025 at levels above the recent five-year average.

Gold’s relationship with US real rates, USD and equities increasingly unstable: Gold’s current unstable relationship with other asset classes is undermining fair-value-based gold price modeling. We see the general instability as positive for gold prices due to higher safe-haven demand.

Next up is a techAmental look at rates (with a dose of healthy skepticism in as far as the recent bid goes) … I’ll focus on today’s ($22bb 30yr) BOND auction …

Mar 12, 2025, 0:57 CitiFX US rates: Lower yields, but watch for momentum upticks

A break of key technical levels in US yields last week means that we now see lower yields again in the medium term. Short term, however, support could hold, and we wait for a further break to 'confirm' the downtrend. That said, we now note that weekly slow stochastics is showing signs of converging, just as we touch 'oversold' territory. We closely watch this as a cross higher from 'oversold' territory has been an indicator of a turn higher in yields…

…US 30y yields We did not see a weekly close below support at 4.46%-4.49% (200d MA, 55w MA). Instead, we have posted an outside day candlestick suggesting we could see a tick higher in yields in the short term. We see resistance first at 4.63% (March high) followed by 4.74% (55d MA).

Longer term, we continue to look for a weekly close below the 200d MA and 55w MA supports to suggest a move lower in yields.

Here is an overview (with a few words on CPI as it does NOT read through to PCE) …

Miss in US CPI, but not as soft translation to PCE; USTs sell off as risk sentiment recovers; BoC cuts rates, but signals cautious path ahead; balanced remarks from ECB's Lagarde; ZAR weakens after Budget announcement; oil prices rise; DXY at 103.58 (-0.2%); US 10y at 4.312% (+3.3bp)

US CPI comes in softer than expected, with core and headline slowing to 0.2% m/m; the decline was led by a significant declaration in core services, with particular weakness in components that do not feed into PCE.

The post-CPI knee-jerk rally in USTs quickly reverses as market participants digest the translation to PCE and as US equities recover (S&P 500: +0.5%); USTs sell off and STIR reprices higher as the data do not push back on Chair Powell's stance that the Fed is "not in a hurry" to ease…

AND same shop w/a few words / thoughts and updated FISCAL narrative — food for thought…

March 12, 2025 10:13 AM GMT MS: US Public Policy, US Economics & Global Macro Strategy: The Fiscal Factor

Congress and the White House are eyeing tax cuts, spending cuts, and other policies that could alter the US fiscal trajectory. Upon considering political plausibility, we think policy choices on balance will result in deficit projections largely in line with current policy, though risks are skewed toward less deficit expansion implied by current policy. Hence, for 2026, we think fiscal policy is unlikely to boost growth and will be supportive of the US rates market.

Tax cuts are coming, but their fiscal impact requires context. We continue to argue that the most likely outcome for tax legislation is one where current policy is extended and any incremental tax cuts will largely be offset by pay-fors. This is a function of Republicans' thin Congressional majority limiting ambitions and requiring that tax provisions enjoy near-unanimous support in the caucus. On balance, this would leave tax revenue estimates for 2026 in roughly the same place as current policy (though revenue would be lower than if tax cuts were allowed to expire at the end of 2025).

We're skeptical that meaningful spending cuts and sustained new revenue sources will be realized for 2026, though risks are skewed in that direction:

The recent budget resolution created room for considerable spending cuts, but we don't think the votes will ultimately be there to execute themto a meaningful amount.

It's possible the Department of Government Efficiency (DOGE) will uncover spending cuts that Congressional Republicans would be amenable to execute on, but so far those numbers have been modest and the politics of underwriting them are unclear.

If current tariffs are sustained and potential future tariffs are levied, they may be considered a substantial mitigant to tax extensions and cuts, but the tariffs that ultimately stick are likely to be fewer than what's currently been proposed, and, if we're wrong, tariff revenues are still likely to fall short of estimates as demand for the affected products wanes.

At a macro level, we highlight two key takeaways for investors:

We don't expect fiscal policy to be a positive factor in the US economic outlook this year and next.

Growth risks and market pricing of less restrictive Fed policy should drive UST yields lower, along with fading deficit concerns relative to previous expectations. A larger fiscal drag or a smaller fiscal impulse than expected implies even lower UST yields.

…US Rates Strategy: Not the Deficit You Were Looking For

Key Takeaways

We expect lower growth expectations and a more dovish repricing of Fed policy to be the primary drivers of the move lower in UST yields.

Potentially helping this trend, near-term risks around Treasury's perceived borrowing needs are skewed to the downside. If spending cuts manifest, then less coupon issuance, less term premium, and lower long-end UST yields may follow.

…As downside surprises in growth data now receive more investor attention, we expect this will lead to a repricing lower of the trough fed funds rate (see Exhibit 4). As shown in Exhibit 5, this positive correlation illustrates that as goes the market pricing of trough fed funds, so goes the pricing of Treasury yields further out the curve…

… in other words, bad (economy)is good (for bonds). Same firm then offers an FOMC precap …

March 13, 2025 MS: March FOMC Preview: Still Not in a Hurry

The Fed should stay on hold in March; when and how it moves next is dependent on policy outcomes that remain unknown. Hence, Powell is likely to repeat they are not in a hurry to act. Our strategists stay long 5s on the UST 2s5s30s butterfly and neutral on mortgages.

Key expectations

The Fed stays on hold and communicates a heavy dose of patience. Chair Powell is likely to sound cautiously optimistic on the economy, but point to a cloudy outlook since policy uncertainty is high.

Incoming data signals a moderation in growth and some resumption of disinflation. However, the data in hand matters less than the data that is to come.

We look for an unchanged policy rate path: 3.9% this year and 3.4% next. We think FOMC perceptions of risks to GDP growth will shift meaningfully to the downside.

Our rates strategists suggest investors stay positioned for lower yields via the UST 2s5s30s butterfly and remain positioned for a 25bp rate cut at the May FOMC meeting.

Our FX strategists continue to recommend short USD positions against EUR, JPY, and GBP.

On agency MBS, our strategists remain neutral on basis and prefer less negatively convex mortgage expressions.

…Based on our economists' view of the Fed's messaging, investor interpretation should coalesce around the idea that the strike on the "Fed put" remains far out-of-the-money. As a result, we continue to suggest investors stay positioned for lower yields.

Trade idea: Maintain long 5y US Treasury notes on the 2s5s30s 50:50 UST butterfly at -0.23% with a target of -0.36% and a stop of -0.16%….

Few and far between — a few words ahead of PPI …

13 Mar 2025 UBS: Cutting confidence more than spending

…Much global economic uncertainty originates with US trade policies and government cuts. However, the government cuts have mainly reduced job security and efficiency to date—government spending rose 7% y/y in February. The risk is that sentiment or “animal spirits” is being damaged without any fiscal savings.

US February producer price inflation is due after a slightly lower consumer price inflation release. As with consumer prices it is too soon for trade taxes to show up in the data. Tax increases hit prices once stocks have been depleted, which takes some time.

Producer prices better reflect corporate pricing power than do consumer prices. Pricing power is also important in determining how much of a trade tax is passed along the supply chain (ultimately to consumers). Because of the political sensitivity it may be worth looking at food prices in today’s data. Egg prices are an internet meme, but did rise 186.4% y/y at the producer level last month.

Ahead of NEXT WEEKS fomc meeting without Fedspeak, whatever are we to do …

March 12, 2025 Wells Fargo: March Flashlight for the FOMC Blackout Period

Summary

A moderation in economic activity since the FOMC last met in January is unlikely to shift the Committee out of wait-and-see mode at its upcoming meeting on March 19. We look for the Committee to maintain its target for the fed funds rate at its current range of 4.25%-4.50%.

Concerns over the growth outlook have intensified in recent weeks amid the swirl of policy uncertainty related to U.S. trade and federal spending. Yet the labor market's cooling has continued to be gradual on trend, while inflation remains frustratingly high. With Chair Powell reiterating ahead of the blackout period that the FOMC does "not need to be in a hurry" to adjust policy, we expect the FOMC will continue to await greater clarity on how policy changes affect its employment and inflation mandates.

We expect the post-meeting statement to make a nod to the recent moderation in growth and labor market conditions, but to otherwise be little changed. The Committee likely will state that risks to its employment and inflation goals are "roughly in balance." That said, we would not be surprised for Chair Powell to make a dovish comment or two at the press conference that reveal a slight easing bias by acknowledging that the downside risks to the labor market have increased somewhat.

The updated Summary of Economic Projections likely will show the median participant continues to expect 50 bps of easing this year. With markets currently pricing in 73 bps of cuts by the end of the year, a shift to one cut could further tighten financial conditions. Yet, as inflation remains roughly 50 bps above target and officials are cognizant of keeping inflation expectations anchored, three or more cuts might be too much for the Committee's hawks. If the median dot for 2025 does change, we think it is more likely to signal 75 bps of easing rather than only 25 bps of rate cuts.

Elsewhere in the SEP, we expect to see a modest downgrade to GDP growth for 2025, with the median estimate dipping a touch below 2.0%. At 4.3%, the median estimate for the unemployment rate at year-end still looks about right, although an increase to 4.4% would not surprise us. Estimates for inflation are likely to edge up further; we look for the median estimate for core PCE inflation at the end of the year to rise from 2.5% to 2.7%.

The March meeting likely will include a discussion about whether a shift in balance sheet policy is warranted. This marks the next step toward an eventual end to runoff. We do not expect any changes to balance sheet runoff until the May 7 meeting when we expect the Committee to announce the end of quantitative tightening.

Finally, a few words on the (fiscal/monetary) PUT bein’ kaPUT …

Vertigo is a sensation of spinning or whirling such that the person or their surroundings appear to be moving. The stock market didn't do much today, but everything else seemed to be spinning. The epicenter of all this vertigo continues to be the White House. More and more economists are increasing their odds of a recession. We raised ours to 35% a week ago. JP Morgan's economists raised their odds to 40% today.

We didn't raise our recession odds today, but we did lower our S&P 500 targets for the end of 2025 and 2026 to 6400 and 7200 from 7000 and 8000. We aren't cutting our earnings outlook yet, but recession fears caused by Trump Turmoil 2.0 are already causing the forward P/E and forward P/S of the S&P 500 to tumble, led by the valuation multiples of the Magnificent-7 (chart).

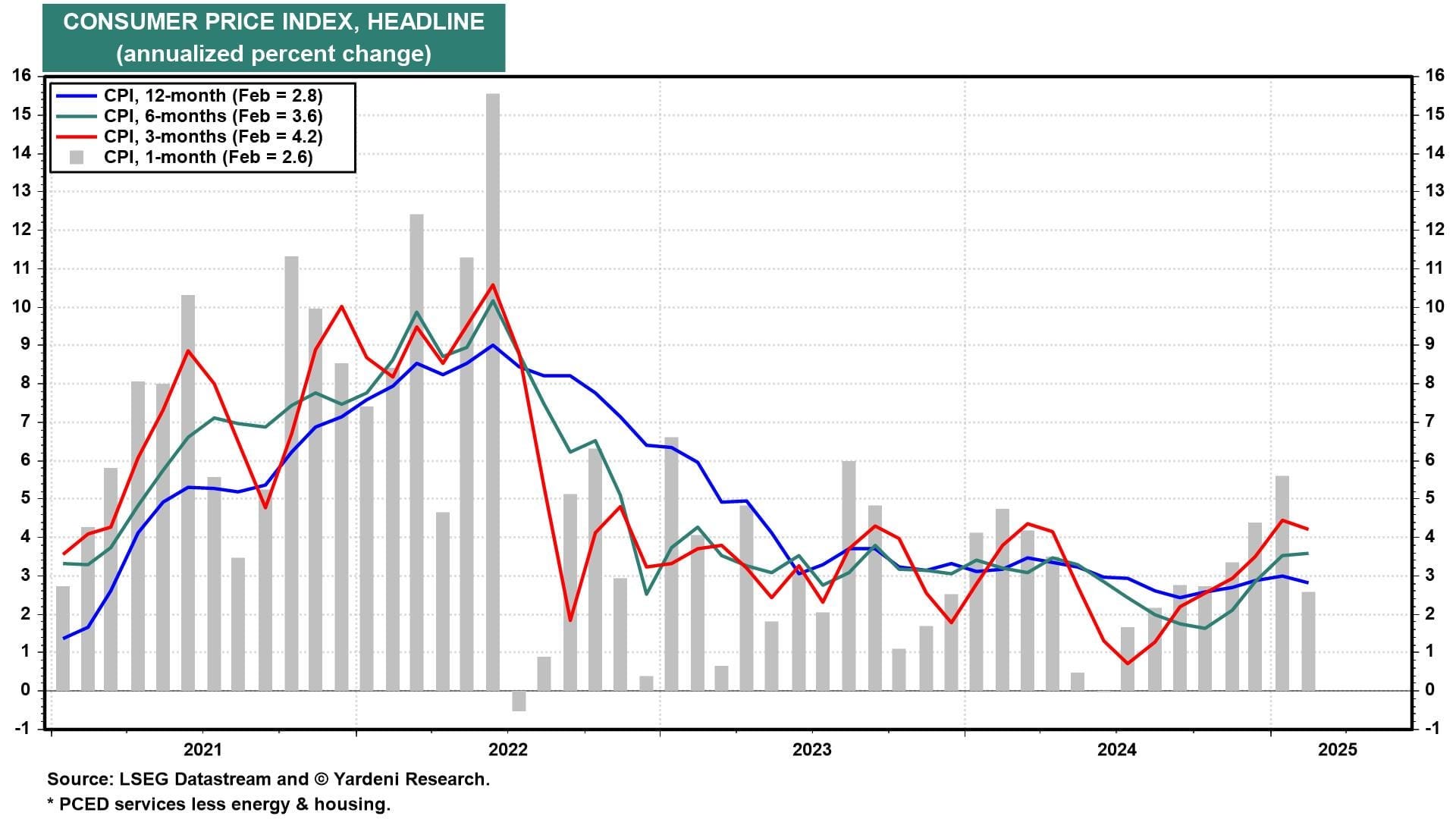

The stock market started the day with a nice boost from a cooler-than-expected CPI inflation rate (chart). The one-month annualized rate was 2.6%, the lowest since August 2024.

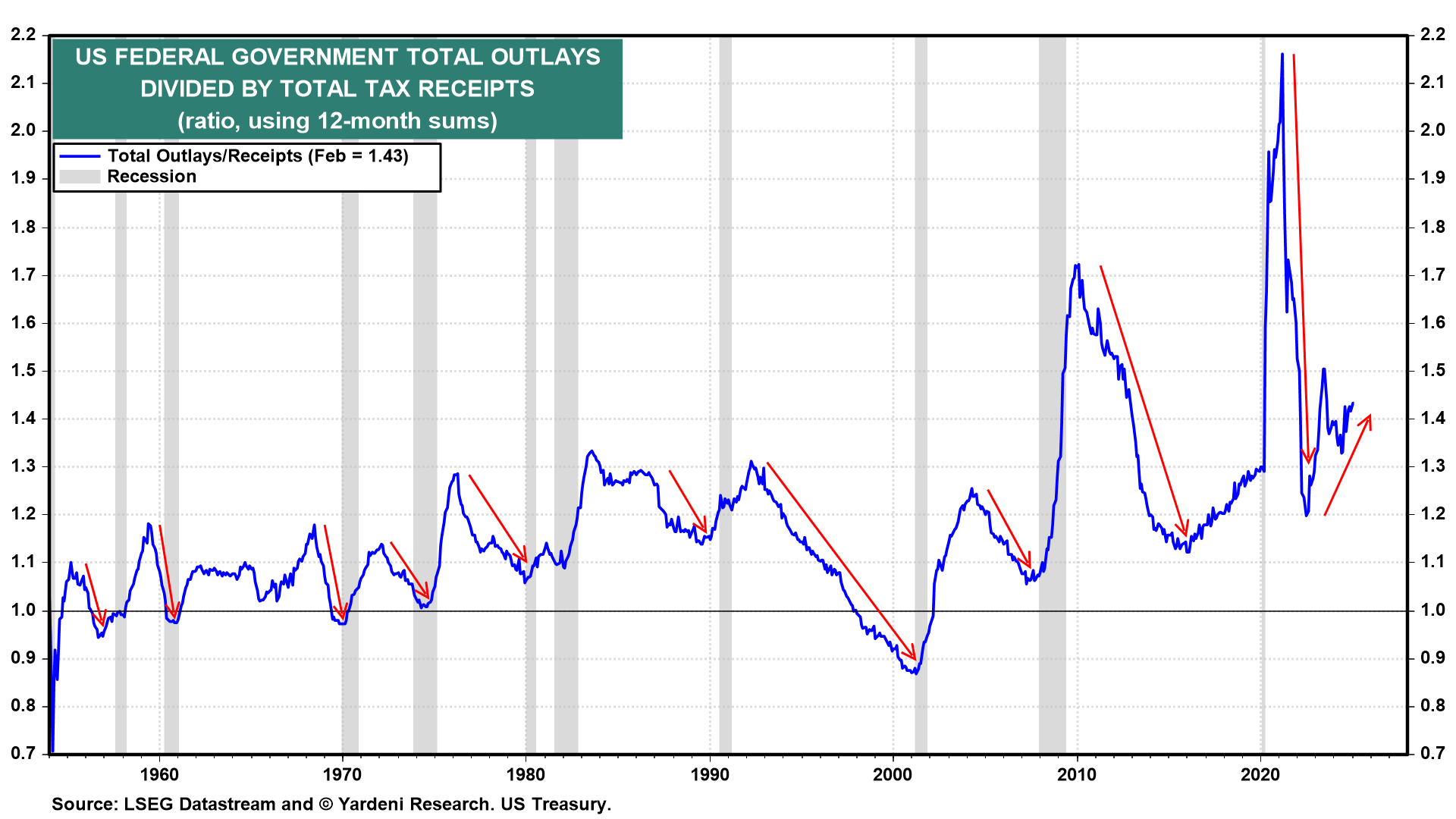

Then stock investors were reminded by the latest tariff tiffs that tariffs may soon boost inflation. Furthermore, the bond yield mostly rose all day, unnerving stock investors. That's because the Treasury reported that the US budget deficit for the first five months of fiscal 2025 hit a record $1.147 trillion. It is very disconcerting to see outlays continue to rise faster than revenues, which shouldn't be happening when the economy is expanding (chart).

In addition, a government shutdown seems increasingly likely by the end of this week. What a mess!

Meanwhile, a “Go Global” strategy (as measured by the MSCI All Country World Ex US index) continues to outperform “Stay Home” (the MSCI US) (chart). Global investors are clearly signaling that they are finding cheaper stocks overseas with happier earnings stories, particularly in China and Europe than in the United States, currently. That could change if the trade war started by President Trump worsens. No wonder gold continues to be one of the best performing assets right now.

The Bull-Bear Ratio compiled by Investors Intelligence fell to 1.3 during the past week. From a contrarian perspective, that's a buy signal. The only problem is that the President continues to give investors vertigo. Speaking outside the White House on Tuesday, where he was testing out his brand new Tesla car with Elon Musk, Trump called the stock market "a fake economy." That's after he said on Sunday, "you can’t really watch the stock market."

The Trump Put is kaput.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Truly amazing this fella offering this level of resource for all on the intertube …

March 13, 2025 Apollo: This Is a Wait-and-See Economy

What characterizes a wait-and-see economy is that consumers and firms are more cautious about spending decisions. Consumers are more reluctant to plan vacations, to buy cars, and to buy new washers and dryers. Similarly, firms are more reluctant to hire and more reluctant to do capex.

The wait-and-see economy is no longer just for companies directly involved in trade with Canada and Mexico. Uncertainty for small businesses is near all-time high levels. This is a problem because small businesses are the foundation of the economy, accounting for more than 80% of total US employment, see the first chart below.

Markets are not yet pricing in the coming slowdown in the hard data. The spread between CCC and single-B has only widened modestly and is still significantly tighter than where it was during the summer of 2022—when the economy was doing just fine—see the second chart. In a slowdown scenario, investors would start to migrate to higher-quality names.

The bottom line is that a wait-and-see economy eventually leads to a slowdown in the hard data. And markets should prepare for that scenario.

A negatively nelly VIEW from The Terminal …

March 13, 2025 at 5:01 AM UTC Bloomberg: Enjoy the good inflation news while you can Uncertainty over tariffs will still leave the Fed reluctant to cut rates.

… The more sophisticated statistical versions of underlying inflation produced by different teams of Fed economists confirm this picture. The trimmed mean (excluding the biggest outliers in either direction and taking the average of the rest) and the median CPI, produced by the Cleveland Fed, are falling slowly but remain above the 3% upper bound of the Fed’s target. The inflation of goods and services with sticky prices (which take a while to change and in practice only go upward), as measured by the Atlanta Fed, is also falling, but very slowly. It’s still at a level that’s too high for comfort. They’re all above their highs for the years leading up to the pandemic:

Another reason why the market didn’t hold on to the enthusiasm generated by the initial numbers: Much had to do with a fall in air fares, which are highly volatile…

… At any rate, in the short term, the market is working on the assumption that inflation is trending up again. One-year inflation breakevens derived from bond prices suggest inflation will touch 4% over the next 12 months, and average 3% over the next 24. If those numbers prove accurate, it would be very difficult for the central bank to cut rates further:

Another from the terminal via yahoo…

Bloomberg: Stagflation Trade Emerges as Rare Winner in US Stock Market Rout

Reuters with some eye candy …

Reuters: The big Trump-driven market slumps, bumps and jumps in charts

One last link on CPI …

WolfST: Beneath the Skin of CPI Inflation: Pace Slows from Spike Last Month, but 6-Month CPI Accelerates Further, Worst Increase since September 2023 Natural gas and electricity pushed up energy costs in February, despite drop in gasoline prices. Used vehicle prices continued to surge.

… “Core services” CPI. Core services CPI, which are all services less energy services, and accounts for about two-thirds of the overall CPI, rose by 0.25% in February from January (3.1% annualized, a sharp deceleration from the spike in the prior month (+6.4% annualized), which had been the worst increase in 11 months (blue line in the chart below).

The 6-month core services CPI rose by 4.1% annualized, a deceleration from January (+4.4%), which had the worst since June (red).

What we noted a month ago was that some services raise their prices annually in January, which can help produce the spikes of the services CPI in January. But we did not see those kinds of January price spikes before the pandemic:

https://youtu.be/T0ntNYbkuyY?si=4tfMcqt2zOMoGRFo

Gundlach Macro Outlook: “Not in My Neighborhood”