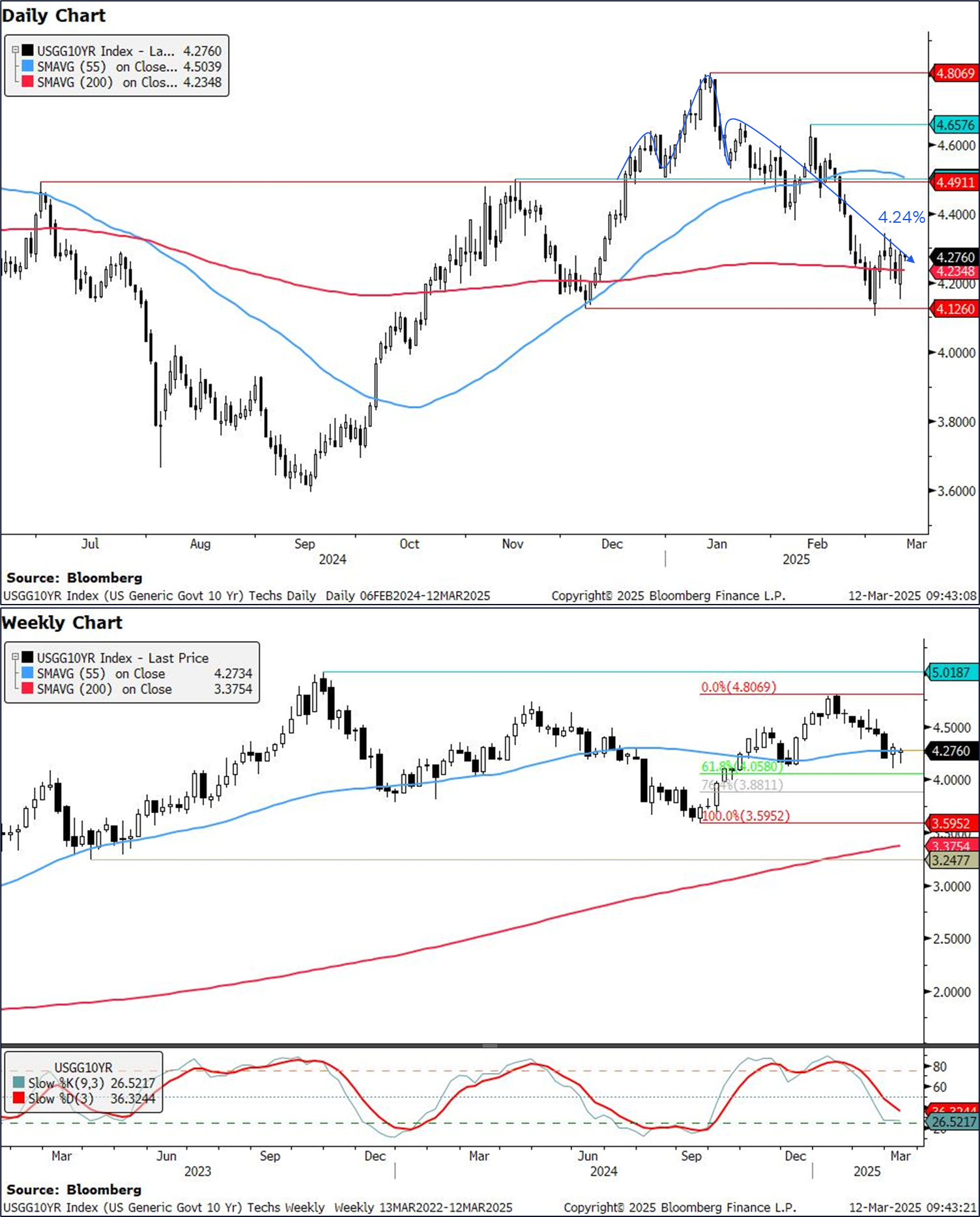

10yy: 50dMA (4.50%) support and 4.13% (recent lows) resistance …

… momentum appears to be pointing towards HIGHER yields but note 50dMA clearly turned lower and in recent past we can see and know that momentum can / will change with either a move in rates OR simply the passing of time (picture Kamala talkin’ bond techs … no, don’t do that … sorry) …

… a much healthier look from those with A Terminal AND some of the best techAmentalists in the biz just below.

In as far as how 3yr auction came and went …

Mar 11, 2025 ZH: 3Y Auction Tails Despite Crashing Stocks

…Overall, this was a subpar auction and while not terrible one would expect a far stronger showing at a time when everyone is - reportedly - piling into Bills and the short-end of the curve as protection from the ongoing collapse in risk. Which then begs the question: what is everyone doing with all that excess cash they just got from nuking their deep underwater momentum stonks...

… and with 10s ahead, am NOT suggesting we drive the car looking in rear-view mirror but understanding some of what drove price action yesterday, helping arrive us at this point, well, I find therapeutic …

Mar 11, 2025 ZH: Goldilocks JOLT Shows Unexpected Increase In Jobs Openings, Hires And Quits

… So how to make sense of this sudden collapse in the labor market? Well, it's possible that after "shocking" the market last month when we saw the biggest drop in job openings in over a year, Trump got the tap on the shoulder that the US market should probably not collapse under his watch, even if he can (still) blame Biden, and so he sent a memo to the BLS to make sure that the numbers aren't in freefall, but dropping more gradually. Then again, with markets now focused almost exclusively on the global trade wars which they are convinced (at least for now) will be far more negative for the US than anyone else, no amount of pig lipstick on hard data will offset the fact that the global trade war has become the Elephant Bear in the china shop, and until there is some clarity on that front expect most if not all rallies to be sold.

AND …

Mar 11, 2025 WolfST: Labor Market Dynamics Tighten Further. Job Openings, Quits, Hires Rise, Layoffs & Discharges Drop, Back Fed’s Wait-and-See - The low point was in September. The Fed faces a scenario of re-accelerating inflation amid a retightening labor market.

… The figure Powell cites a lot: The number of job openings per unemployed person ticked up to 1.13 job openings for each person who was unemployed and looking for a job during the reference period (7.74 million openings for 6.85 million unemployed).

The ratio is the highest since May. The low point had been in September, when the Fed got spooked. It shows a relatively tight labor market compared.

A reprieve, for now and I’ll move right along … here is a snapshot OF USTs as of 710a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries traded with a firm tone in early Asia, bouncing on light demand from real money accounts. Buying from in 10s was cited by the desk, countered by selling in intermediates from systematic accounts, mainly in 5s (2s5s10s +0.5bps). The EU commission launch of countermeasures on US imports was seemingly well absorbed, with S&P futures +0.7% here at 7am, the DAX +1.8%, DXY +0.2% and WTI +1%. Continued position-squaring is expected into CPI, with 10y supply at 1pm.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

Reuters Trading Day: Another sea of red as tariff fears trump ceasefire hopes

… Commodity Futures Trading Commission figures show that open interest, the broadest measure of investors' exposure to U.S. bond futures, is sliding at a historic pace. In some cases, such as two-year contracts, the fall is the sharpest on record. In the week through March 4, open interest in two-year futures fell by a record 396,525 contracts, or nearly $80 billion. That's around 10% of investors' total exposure, and it means overall open interest is down 17% from its peak around the U.S. presidential election in November.

…Why does this matter? As a paper by Federal Reserve staffers Andrew Meldrum and Oleg Sokolinskiy found last month, cash market depth "significantly affects liquidity fragility in all maturity sectors" of the Treasury market. In other words, the slump in open interest could mean that one of the world's most important markets has become easier to disrupt…

Job openings rose to 7.74mn in January, in line with the average in Q4 24. The overall separation rate rose, reflecting higher quits, while the layoff rate declined, indicating firms' willingness to retain workers, prior to the latest trade-related decrease in household and business confidence.

…All Hitchhiker, No Guide. Literally …

March 11, 2025 BMO: Close: All Hitchhiker, No Guide.

… Underperformance of duration as a supply accommodation represents a page directly from ‘The Hitchhiker’s Guide to the Treasury Market’ – not a real book, yet. Self-publish or perish? We digress. There is certainly a path for a breakout steeper from current levels in the event of a downside surprise in the February core-CPI data. However, in the event of an as-expected (or higher) inflation print, as the supply is absorbed, the steepening pressure should pause – albeit only momentarily as the new duration finds sponsorship. As the market has recently become sensitive to, the translation of core-CPI, core-PPI, and Import Prices into the Fed’s favored inflation measure in core-PCE is the operative information to be extracted from the ‘early’ look at the February inflation series. Said differently, investors might ultimately be less willing to allow CPI to set the tone for the next couple of weeks in US rates…

Next up is a techAmental look at rates (with a dose of healthy skepticism in as far as the recent bid goes) … I’ll focus on today’s auction (10s) and likely to circle back with today’s thoughts on BONDS ahead of tomorrows auction there …

Mar 12, 2025, 0:57 CitiFX US rates: Lower yields, but watch for momentum upticks

A break of key technical levels in US yields last week means that we now see lower yields again in the medium term. Short term, however, support could hold, and we wait for a further break to 'confirm' the downtrend. That said, we now note that weekly slow stochastics is showing signs of converging, just as we touch 'oversold' territory. We closely watch this as a cross higher from 'oversold' territory has been an indicator of a turn higher in yields…

…US 10y yield We have dramatically broken below 4.24% (200d MA, head and shoulders indicated target). On a weekly basis, we have also closed below the 55w MA at 4.27%. Given this, as well as other technical building blocks, we are now again forced to turn bullish on US 10s (i.e. lower yields).

These are the indicators:

Monthly evening star formation

Weekly slow stochastics ticking lower

Weekly close below 55w MA

Now, all eyes are on the 4.13% (December 2024 low). A weekly close below that would set a 'lower low' and add to the building blocks towards lower yields.

Short term, we see resistance at 4.10% (200d MA). Longer term, we see a possibility for a move much lower towards 4.0% (psychological support), and 3.36%-3.60% (200w MA, 2024 low) in the longer term.

World order of global TRADE and the potential reshaping of things …

11 March 2025 DB: Four forces that could shape the new global trade order

The global trade order is being reshaped in dramatic ways. Taking a step back from the ongoing news flow, we look at the longer-term forces that are likely to shape global trade going forward, focusing on the four key economic blocs:

1. US energy independence is enabling a return to its protectionist roots and the US' historical approach to industrialization.

2. China is likely to remain trade-focused to secure resources, export markets for its goods, and greater global influence, even if domestic consumption becomes a bigger priority over time.

3. Trade still lies at the heart of the European project; intra-EU trade could benefit from renewed consolidation and spending, while FTAs and openness to investment could help externally.

4. The Global South will likely continue to look to trade for development; the risk of disruption to global value chains bears watching, as does Chinese export reorientation and outward investment.

US trade policy is introducing some of the biggest shocks the global trading system has seen over the past 80 years. But how global trade evolves will be a function of how different economic blocs respond and react to each other. The interwar years in the first half of the 20th century featured a period of significant decline in global trade driven by protectionism, recessions and tit-for-tat retaliation. The trade decline lasted around three decades before a new free-trade consensus emerged, shaped by US leadership. Whether trade endures a painful decline, or is able to reorient along new corridors remains to be seen. While there are signs of US disengagement, we also see incentives and potential for the three other blocs of China, Europe and the Global South to remain engaged.

Tariffs ON, off, on, and so it goes … what matters? Where are RATES headin’ …

Some weeks back we identified some key drivers for lower Treasury yields. This update brings in tariffs as a latest influencer. They are forcing yields further lower, with likely more to come. But tariffs are a double-edged sword. And there are perception risks to take into account too. This thing could easily swing in the other direction in due course …

…Still tactically bullish on Treasuries as a call But let’s not confuse the overall message. Right now, the knee-jerk should be bullish for Treasuries. We've also identified a floor, and how that floor could in fact shift lower.

But you can see how this could also flip the other way, Timing on the latter bit is not easy.

Practical to stick with Treasuries as a safe haven, at least for as long as that tag is applicable…

What happens in Japan, stays in Japan? Maybe. Maybe not …

March 11, 2025 08:52 AM GMT MS: Japan Macro, Equity Strategy, Economics, and Financials "Understanding Investors in Japan" Reboot: Big Changes in Investment Behavior Under Way

Japanese investors hold ~US$48 trillion in financial assets, and major changes in their investment activity could have meaningful impacts on asset class performance. Following the recent dramatic changes in Japan's economic situation, we are revisiting the work in our 2019 report.

Key takeaways

Investors in Japan including households have US$48 trillion in financial assets, with the highest international investment position among G10 countries.

With Japan's shift to an inflationary regime, we assess changes in investment behavior across investors by category and impacts across asset classes.

Households have taken steps to protect their assets against inflation, while depositary institutions' focus has shifted from securities investment to lending.

We estimate that the impact of household investment in Japanese stocks via the new Nippon Individual Savings Account (NISA) is at least JPY 6.3 trillion.

Structural inflows from households support our constructive view on risky assets; we don’t see institutions as active buyers of JGBs despite higher yields.

Oh Canada, how they would so LOVE for us — ‘Merica — to fall flat …

March 11, 2025 RBC: ‘Yellow flags’: The cracks forming in the U.S. economy that we’re watching

…One sector, in particular, that continues to see anemic activity is the housing market. Affordability measures are near record highs, meaning home ownership will remain out of reach for many young households. What’s worse is the primary mechanism to lower mortgage rates (i.e., the Fed lowering interest rates) is unlikely to improve affordability, because of the well-documented lock-in effect wherein existing homeowners have little incentive to leave favourable mortgage rates.

… US February consumer price inflation will not reflect the direct consequence of trade taxes—it is too soon. Hints of second-round effects may be in evidence. Some companies may have anticipated tariffs in their normal price-setting process. The media attention on tariffs and inflation (at least among Democrat-leaning media) may give retailers cover for some profit-led inflation.

Absent tariff effects, the forces of supply and demand suggest broadly stable US inflation. Egg prices will no doubt be a social media meme, but neither Federal Reserve Chair Powell nor Trump are chicken farmers, and cannot affect a relative price shock…

… same shop, different group, with a look at JOLTS …

Job openings rise to 7.74 million in January Job openings rose 232K to 7.74 million in January, a little better than consensus (7.60 million), leaving the series very close to the average for the 12 months of 2024 (7.78 million). We expectthat the general direction of travel for job openings is a bumpy path downward, as it has been since early 2022 — but emphasis on the word "bumpy." The rise in January left the level down 728K from 12 months prior…

…Alongside today's release, the BLS revised the JOLTS estimates to incorporate the impact of the recent benchmarking of the CES data and updated seasonal adjustment factors. Unadjusted and seasonally adjusted data from January 2020 on were subject to revision. In the five-year period open to revision, job openings were revised down by 72K per month, on average. The hiring contour in March 2023 through March 2024 was a little softer than previously estimated, down 147K per month in that 12-month period, on average.

They say small biz finances and employs most of ‘Merica …

March 11, 2025 Wells Fargo: Small Business Optimism Takes Another Step Lower Higher Prices and Labor Troubles Weigh on Small Firms in February

Summary Uncertainty Surges Higher Amid New Tariffs Small business sentiment appears to be moderating amid higher economic uncertainty. The NFIB Small Business Optimism Index fell for the second consecutive month in February to 100.7 as the uncertainty index rose to its second highest level on record. Although economic perceptions remain much more constructive than in recent years, the recent flurry of tariff activity appears to have dented economic expectations and put upward pressure on small business prices. The net share of small firms raising their selling prices leapt 10 points in February to 32%, its highest level since May 2023. Price plans increased three points in kind. Meanwhile, the labor market reemerged as the top concern facing small firms, causing hiring plans to dip three points in February

… this same shop commenting on job openings …

March 11, 2025 Wells Fargo: Job Openings Stabilize in January, but Likely Short-Lived

Summary The first Job Opening and Labor Turnover Survey for 2025 showed the labor market maintained solid momentum heading into the year. Job openings rose slightly to 7.7 million, and the ratio of jobs-per-unemployed worker ticked modestly higher to 1.13. Layoffs and discharges remained historically depressed at just 1.0% of total employment, and the recent sideways trends in the hiring rate and quits rate are welcome compared to the downward slides that punctuated most of last year.

Yet while today's JOLTS report offers further evidence that the jobs market started the year in decent shape, headwinds have emerged more recently. The low rate of hiring leaves the jobs market in a vulnerable position to a renewed deceleration in labor demand.

… finally, from Dr. Bond Vigilante, THE question of the moment …

Mar 11, 2025 Yardeni: Will Trump Tariff Turmoil Dim The Economy's Lights?

The stock market was whipsawed today by geopolitical developments. Stocks fell this morning when President Donald Trump announced a 50% tariff on Canadian steel and aluminum. They then recovered after Ukraine agreed to a US-proposed ceasefire deal (pending Russia's acceptance). Incremental progress on a tariff-avoiding deal between the US and Canada late in the day provided an additional boost. But stock prices still closed down a bit for the day.

Investors are worrying about the adverse macroeconomic consequences of all this geopolitical turmoil. The uncertainty associated with rapid-fire tariff announcements from the White House could weigh on the economy. The NFIB survey of small business owners includes an uncertainty index, which rose to a new record high of 110 during October (chart). After the November 5 elections, it fell down to 86 in December and then rebounded to 104 in February.

Uncertainty typically increases in advance of a presidential election then decreases once the new president's policy goals are clearer. If uncertainty lingers, then consumers may pull back on spending and companies might be reluctant to invest, ultimately hurting the jobs market…

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

First up, an NFIB recap …

March 12, 2025 Apollo: Small Business Uncertainty Near Record-High Levels

The February NFIB survey of small businesses shows that business uncertainty is near the highest levels since the survey started in the 1970s, see chart below.

NEXT, a couple from The Terminal where this first note is on POSITIONS and from EBB — one of, if not THE very best in the biz…

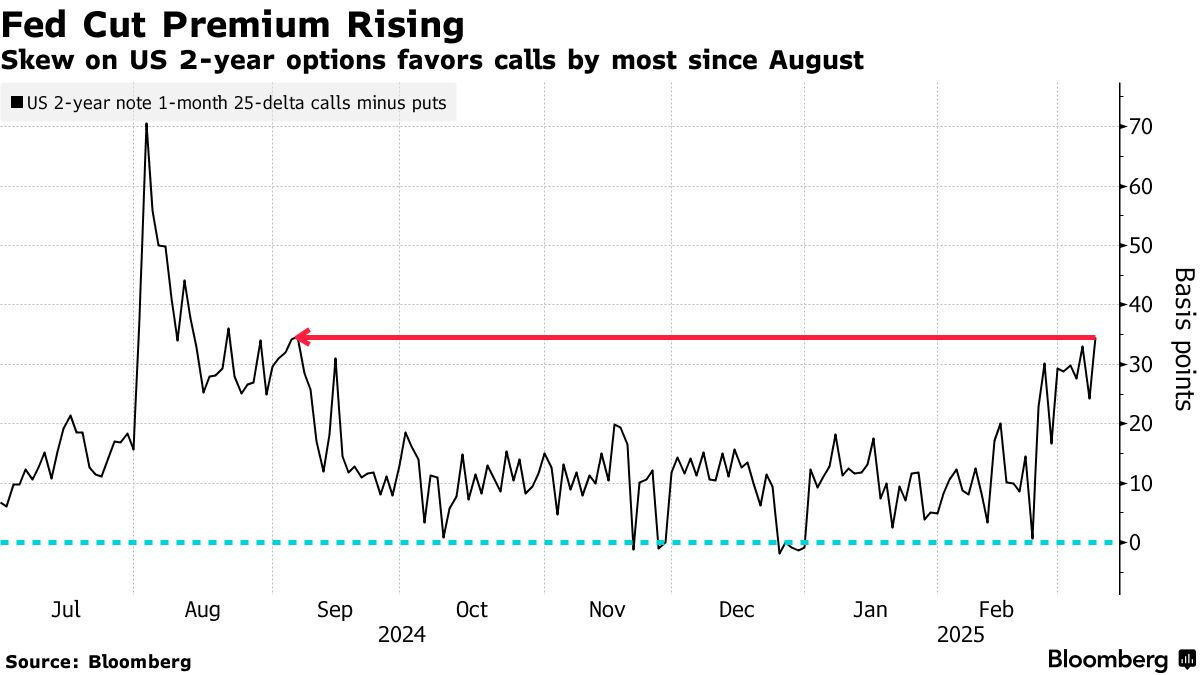

March 11, 2025 at 8:30 PM UTC Bloomberg: Traders Ramp Up Bets on Fed Rate Cuts as Recession Angst Builds

… Options traders are anticipating the risk will ramp up pressure on the Fed to boost the economy by cutting rates in the coming months. This has led to growing demand for call options on two-year Treasury notes, which will pay off if the Fed gets more aggressive on rates. The premium on these bullish bets has risen to the highest since last September, when slowing job growth was feeding fears of a slowdown during the final months of Joe Biden’s presidency…

… AND here’s an OpED …

March 12, 2025 at 5:00 AM UTC Bloomberg: Why Trump cares less about market pain this time Theories abound, but the big question is whether the Trump Put is really dead or just on life support.

Yesterday was as much about confidence as anything so on that sort of note …

Employee confidence dropped in February to a new record low as a chill comes over employee sentiment, according to the latest data from the Glassdoor Employee Confidence Index. The share of employees reporting a positive 6-month business outlook fell to 44.4% in February 2025, the lowest level on record since our data begins in 2016. Rising economic uncertainty is tamping down employee sentiment and also stretching employees thin as workers are asked to do more with less amid tight budgets and pressure from leaders.

Economic anxiety and, in particular, concerns about job security, layoffs and its impacts on the workforce left behind are weighing on employees…