Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP lets deal with a couple / few things items from weeks END, specifically housing and PPI related (as we know, innards of PPI will impact PCE … more below) …

CalculatedRISK: Housing Starts Decreased to 1.331 million Annual Rate in January WolfST: PPI Inflation Spikes in Services and Finished Core Goods, Very Disconcerting ZH: Producer Prices Surged In January As Services Costs Soared ZH: Housing Starts Collapsed In January - Biggest MoM Decline Since COVID Lockdowns

Alrighty then as we move along digesting the days and weeks data fully, the MARKETS seem to have continued along their merry way. And when I say ‘markets’ I’m referring back TO what was noted LAST weekend (bearish WEEKLY visuals of 2s, 10s and 30s …) and with THOSE somewhat longer term contextualized visuals in mind, ONE seems to need further inspection and updating …

30s: looks to ME like a TLINE BREAK, firmly ABOVE 4.32 and worse, we’re now back ABOVE 4.42% — level from October … of 2022 …

… and a weekly TLINE break, with STILL bearish momentum (stochastics) should keep any / all dip buyers PATIENT…

… NOT to switch up topics too much but, at least as far as WEEKLY visuals and MESSAGES go, perhaps who ever it was betting via options, that rates are headed higher (10s up to 4.55% — noted HERE by Bloomberg’s best — Ed Bolingbroke) maybe not such a lunatic fringe guy / gal after all??

… Ok I’ll move on AND right TO the reason many / most are here … some UPDATED WEEKLY NARRATIVES … some of THE VIEWS you might be able to use.

THIS WEEKEND, a couple / few things which stood out to ME …

… with 10y at 4.25% and 30y at 4.4%. While the market is more reasonably priced, we believe the risks are still skewed towards higher yields …

Barclays w/Jan PCE preview

We estimate that core PCE accelerated 0.4% m/m (2.8% y/y) in January, led almost entirely by core services inflation, consistent with the strong CPI and PPI data for the month. Our Q4/Q4 core PCE estimate has now increased to 2.5% for 2024 (+0.1pp) and is unchanged at 2.3% for 2025…

… We maintain our call for the FOMC to initiate the first 25bp rate cut in June of this year…

…While the reports are troubling, we argue that it is likely premature to abandon expectations of continued gradual disinflation, or to judge consumer spending to be faltering …

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

While January activity data came in on the weak side, we are raising our 2024 growth forecast by 0.3pp to 2.1%, which is now well above the consensus forecast of 1.6%. The change is driven by the more resilient labour market, which is likely to mean a shallower slowdown in consumption than we previously expected. With labour market tightness continuing to ease, however, we still expect the Fed to hit its 2% inflation target before the middle of the year, paving the way for rate cuts in June.

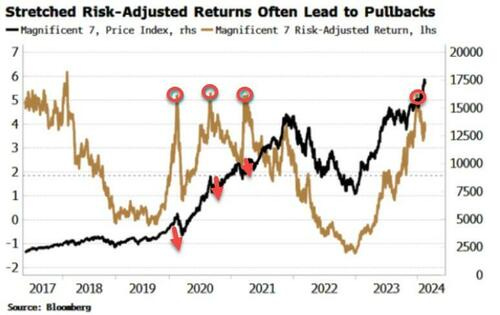

Bloomberg(via ZH): Magnificent 7's Blistering Risk-Adjusted Return Is A Warning

… Previous extreme risk-adjusted returns for the Magnificent 7 have occurred at price reversals.

Interestingly, today the risk-adjusted return is high, but not at historical extremes.

This suggests that, from this perspective, a notable pullback might not be imminent, yet one could be in the offing if the adjusted return keeps rising.

Risk-adjusted returns are often nothing more than a deep tide concealing the dignity of swimmers who have been remiss in donning their trunks.

They are boosted by falling volatility, but repressed vol typically explodes higher at some point. High risk-adjusted returns thus suddenly become very low ones.

They are thus a warning sign rather than a green light.

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned (both 10yr and 30yr SPEC SHORTS COVERING … not covered but buying of dip? more shorts out there, though … )

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,