Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP, THIS LINK through to SOME of what Global Wall St is sayin / sellin’. WHY it is that this stuff is of some perceived value, more than say, YOUR view, escapes me. Narratives for the year ahead have been re-written several times already and like weathermen, these folks always seem to be sportin’ the nicest suits with the fattest pin stripes and fanciest of shoes …

Ok, RANT aside, read what THEY are sayin / sellin ‘ and thinking and I’ll detail some of MY favs in a minute but for now … lets deal with a couple / few things items from weeks END beginning with what, if any messages can be gleaned from WEEKLY charts …

2s: momentum leans BEARISHLY, watch WEEKLY closes vs ~4.50%

10s: same, bearish WEEKLY momo, watching in / around 4.25% next up 4.40%?

30s: once again SAME bearish WEEKLY, watch close next week in / around 4.423%

AND in as far as some of the ‘news’ (snarky and / or otherwise SPUN) shaping shifting this (price of money) narrative … well, clearly NOT BAD or worse (CPI) = GOOD (CPI)

Bloomberg: US CPI Revisions Confirm Inflation Progress at End of Last Year CalculatedRISK: Updated Seasonal Factors for CPI CNBC: Inflation in December was even lower than first reported, the government says RTRS: Mixed US consumer price revisions leave slowing inflation trend intact ZH: BLS Releases Revised CPI Data: Here's What's In It

… Ok I’ll move on AND right TO the reason many / most are here … some UPDATED WEEKLY NARRATIVES… some of THE VIEWS you might be able to use.

BAML rates weekly, “Ranger danger” (offering some words of caution…ie bearish)

… We now see risks to the recent 10y range shifting higher with strong US data. Clients have appeared willing to “buy the dip” but continued strong data may test their conviction. This is especially true given duration longs have built slightly in our FX & Rates Sentiment Survey (see Self Confident). The survey also shows clients see long rates as both their highest conviction and most crowded trade. We see near-term upside risk to recent rate ranges and would encourage client to be patient in adding duration on any rate break out. We won’t be as constructive on duration until 10y pushes closer to 4.5%.

… TECHNICALS … So goes January and so goes US 10Y yield?

When 10Y yield is up in January it tended to be 70% of the time in Q1. If 10Y > 4.20% then double bottom and higher Q1.

BMO weekly, “Revised and Forgotten” (stopped OUTTA 5s/30s steepener, enter 2/30s flattener)

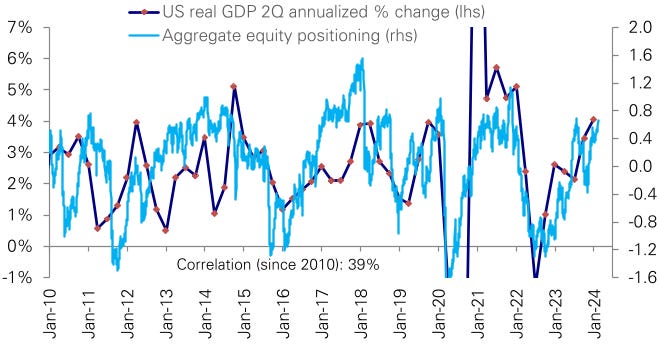

DB - in addition to updated softening of the ‘soft landing’ narrative, you’ll note interesting chartbook with FOMC ‘scorecard’ as well as another comment / VISUAL of equity positioning …

The climb in positioning has been in line with the sharp acceleration in macro growth

JEFF: Updated Economic Outlook: Growth, Everlasting? Unlikely (we’re getting updated updates now seemingly every day of the week … i know, i know, when the facts change i … never mind…NEVER ceases to amaze me this stuff is ‘paywalled’ suggesting highly sought after and worth something when you and I could likely produce similar results with the eTrade monkey throwing darts …)

… Since we sent out our 2024 outlook on December 1, 2023, the economic data have continued to tell us an unexpectedly strong story. We had thought that consumer spending was going to decelerate sharply during the holiday season after consumers overextended themselves over the summer. However, the "pullback", if you could even call it that, was limited to the month of October!..

…We struggle to reconcile the idea of strong economic growth with the rate cuts that are priced into the market. We think that there will be room to cut rates by June, but only if growth slows. If growth continues, however, rate cuts would generate excess risk of a reacceleration in inflation…

MS Global Macro, “Enter the Dragon” (staying LONG ‘duration’ affirming tight stop)

… Long duration with tight stops: We remain cognizant of the risks to our long duration call, but think that Treasuries offer a good risk reward at these levels. With merely ~4 cuts priced through December, we think the market has ample scope to reverse this recent rise, and also make new lows in yields. In line with our "buy the dip" mantra, we continue to suggest long 5y notes, with stop out at 4.24% …

SocGEN FI Weekly, “Buy the dips” (speaking of 10s and Bunds)

… Buy the dip if 10yT rises to 4.25% and add to steepener if UST 2s10s flattens to -40bp.

There you have it. A SAMPLE of what you’ll find. Something for BULLS (stay long, buy dips) and for the bears (be patience — it IS a virtue, you know) … AND more. MUCH, much more…

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

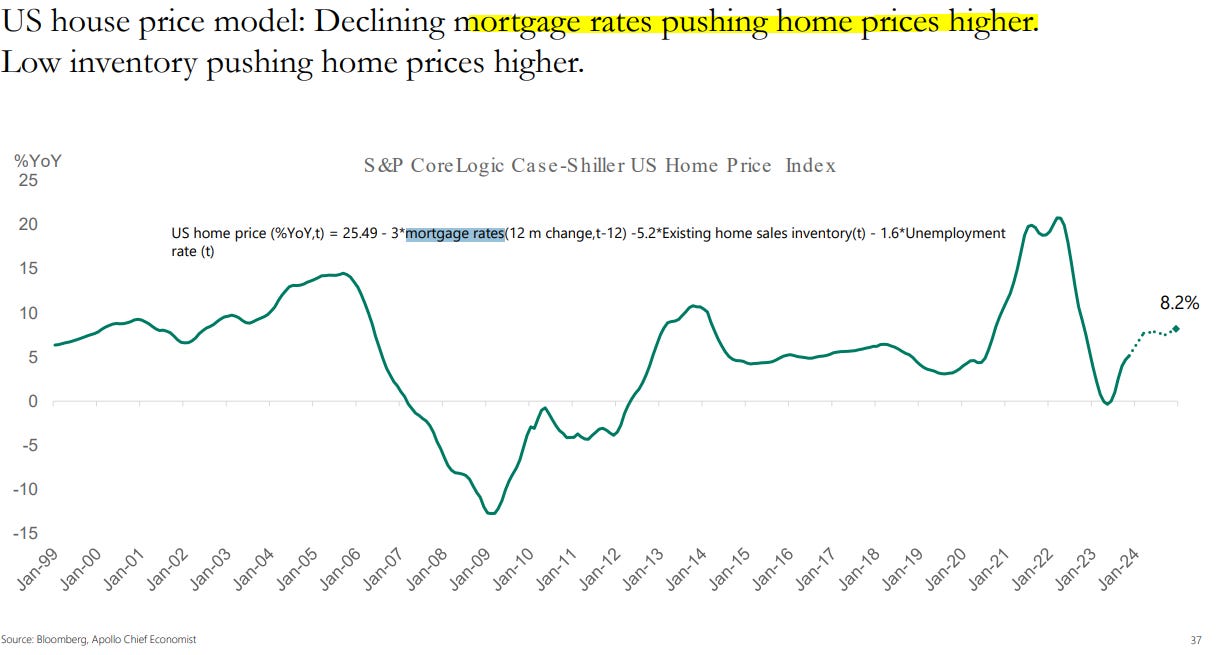

Apollo: US Housing Outlook (check me if i’m wrong here but higher prices on top of already HIGH prices will make houses … LESS affordable than they are already?)

A housing recovery has started, driven by low supply and pent-up demand boosted by FALLING MORTAGE RATES

Our latest outlook for the housing market is available here, key charts below.

AllStarCharts: Rates: Higher for Longer It Is! (wait, i thought these clowns liked bonds … i mean FIRST OF ALL bond traders don’t give a rats a$$ OR even know TNX is a thing. Cuz … it isn’t … bond traders trade futures or wait, here’s a crazy idea, actual cash bonds…Further more … you gotta remind people you follow interest rates cuz nobody but WSJ is?? to say nothing of the awesome idea to BUY last week? WTaF … at least in that post to BUY these clowns … er um allstars … referred to futures…whatever … i’m not perfect EITHER but I admit it and do NOT pose as an allstar anything … ask anyone)

… Whenever a fellow parent asks what I do, I tell them I comment on interest rates.

I’m not involved in the semiconductor industry or the AI revolution. I don’t rob community banks (a personal favorite, despite mixed reactions). And I certainly do not analyze fixed-income, forex, and commodity markets (that’s a show-stopper).

The only thing people want to know these days – whether they’re navigating Wall St. or Main St. – is where rates are headed.

But no one seems to be listening to the one person who has a direct impact on the direction of US Treasury yields…

Of course, I’m talking about Fed Chair Jerome Powell.

For most of last year, his mantra regarding rates was “higher for longer.”

Yet the bond market was pricing in at least five rate cuts in 2024…

… I’m convinced no one is paying attention to Powell except Nick Timiraos.

Honestly, I don’t use these probability tables as a guide to where rates are headed. Instead, I view these tables as positioning and sentiment indicators.

When it comes to gauging the direction of interest rates, I simply follow the charts and the underlying trend:

The uptrend remains intact. And I have to err in that direction.

Bloomberg(yest): Hedge-Fund Short Sellers Revel in Hidden Cash Perk Like 2007 (as yet another example of how each and every one of you out there in markets tryin’ to earn a living, make some scratch … are ALL created equally but … as we know, SOME are created MOAR equally than others … and this subsidy brought to you BY the letters, “F”, “O”, “M”, and “C”)

Short rebates are offering traders a boon in cash-is-king era

TIFF and Cambridge Associates are bullish on industry outlook

…It’s the tidy income the masters of the universe are enjoying just on their cash proceeds after shorting stocks, all thanks to the highest federal funds rate since 2007.

When the fast-money set bets against a company, it sells borrowed shares, resulting in a pile of cash that is held as collateral with their prime broker. That cash earns interest, known as a short rebate.

Cambridge Associates, an industry consultant, has cited this benefit as one reason to be bullish on hedge funds this year — alongside all the rich stock-picking opportunities fueled by the Federal Reserve’s disruptive policy-tightening campaign. TIFF Investment Management, Morgan Stanley Investment Management and Evanston Capital, which allocate money to a range of investment vehicles including hedge funds, have said the same.

In a good year, short rebates are just a small fraction of hedge-fund returns, of course. Yet the effectively free money is offering traders a boon just as the great monetary squeeze separates the strong from the weak across Corporate America — spurring an uptick in short interest from historic lows.

With Jerome Powell & Co. pushing back against market bets on fast rate cuts this year, these mundane lending dynamics are getting more attention as the cash-is-king era powers on — and raising big questions about the hefty fees charged by some funds.

“For the first time in 15 years, the wind’s at their back on the short book,” said Joe Marenda, head of hedge fund research at Cambridge Associates. “The other aspect simply is that with higher rates, one would expect weaker companies to underperform.” …

… “Maverick’s average net short rebate of 4.5% is the highest it has been since 2000,” wrote Lee Ainslie, a so-called Tiger Cub who founded the hedge fund. “To put that figure in perspective, our net short rebate was actually negative in eleven of the last fourteen years! Our short alpha is certainly enhanced by replacing a mild headwind with a strong tailwind.”

To be clear, returns derived from an elevated short rebate can be at least partly offset by higher borrowing costs on the long side when leverage is employed. Interest income is no substitute for smart investment decisions, and the actual track record of the rate-hike cycle so far is mixed…

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Happy New Year to any / all that celebrate and from our collective good friends over at Hedgeye …

THAT is all for now from THIS guy who ALSO can and has been described as

… likely present himself to a jury, as he did during our interview of him, as a sympathetic, well-meaning, elderly man with a poor memory…

-U.S. Department of Justice, Special Counsel's Office p10 of THE PDF (here)

From ONE well-meaning elderly man with a poor memory (but withOUT the ‘nuke football’ to y’all … GO Niners! Enjoy whatever is left of YOUR weekend … including the big game!!

Will read soon.

Wanted to post this:

https://youtu.be/7RtsCIgOWv8?si=8717GXm_-xh95-4C

Avalanche of Job Losses, FED Driving Economy into Recession – Danielle DiMartino Booth

What the Main Stream Media isn't telling us........

That was FUN :)