Bloomberg: Quality lapses threaten trust in Boeing, bond bulls double down on Treasuries, and US lawmakers strike a deal to reduce the risk of government shutdowns. Here’s what people are talking about…

… <bond>Traders betting on a 2024 bond rally are unfazed by the recent pullback, seeing it as a chance to seize on elevated yields before the Federal Reserve starts driving down interest rates. The dynamic was on display Friday, when bond prices dipped after the Labor Department reported that job growth unexpectedly accelerated last month. But the selloff was curtailed because buyers swooped in as 10-year Treasury yields neared 4.1%, the highest since mid-December…

With the full writeup below on how 10s are ABOVE the proverbial ‘buy zone’, I thought I’d begin the day / week with a look at 2yy …

… Couple / few things to note — momentum has corrected sharply from overBOUGHT to more middle of the road (not yet overSOLD / cheap). I’d also nte quite a gap from where we are here/now up TO more solid support (in / around 4.60%).

Clearly whatever the Fed does / says next will be more instructional here and Logan over the weekend was offering whatever you think you wanted to hear …

And speaking of something for everyone, I’ve heard and read some about MULTIPLE job holders and the spin here was that because they are UP, it is reflecting a GOOD jobs market … let that settle in a moment and read this, from DATATREK for example …

… Third and lastly: Multiple jobholders as a percent of the workforce hit a post-Pandemic high of 5.3 percent, a statistic which got a lot of press so let’s put it into a longer-term historical context. The following chart shows the data back to 1994:

As we have highlighted in the graph, the percent of multiple jobholders has been in secular decline over the last 30 years (6 percent to around 5 pct). Recessions (2001, 2008 – 2009) cause it to decline, and the next cycle shows lower levels. The Pandemic Recession was especially notable, with the multiple jobholder percentage sinking to just 4.0 percent. It has now rebounded back to its pre-Pandemic high of 5.3 percent.

Comment: In order for a worker to hold more than one job, demand for that person’s labor must be strong enough to get them that second position. December’s reading is therefore yet another sign that the US labor market remains in good shape. Also, there’s nothing in the longer-run historical data to suggest that current conditions are abnormal or unhealthy. The 1990s were a good period for many Americans, for example, and a record number of workers carried more than one job for much of the decade. Conversely, the recovery from the Great Recession was long and slow, with lower percentages of multiple job holders.

Takeaway: There was little in Friday’s Jobs Report to support the idea that the Fed will be cutting rates in Q1. On the plus side, the data paints an upbeat picture about the state of the US consumer. That, we suspect, will be the story of 2024: rates will be higher than markets want, but economic growth will be the offsetting positive. To our thinking, that is a reasonable backdrop for another good year for stocks…

… Consider, if you will, the last person for example, you met or know or perhaps are related to WHO holds a 2nd job. A gig. Side hustle. Whatever you wish to call it. Do they do it because the job market is so good OR because the situation REQUIRES it?

… here is a snapshot OF (aggressively UNCH) USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly cheaper amid slow-motion spread-widening, Japan closed overnight and a light economic event calendar seen today. After opening lower in London, there were a few pockets of demand sourced in futures, some 5-10y buying from RM, while fast$ pressed 5s30s steepeners and bought spreads (Logan comments above, 5y SFR spreads +1.6bps). Gilts and Bunds are sharply underperforming USTs on a budding supply calendar (bond sales possible across Italy, Ireland, Belgium), while US IG expectations range from 25-35bn. Equity futures are close to home, SPX futures -1pt here at 7:15am, DAX +0.1%, DXY +0.1%, and commodities on the backfoot (WTI -3%, HG -0.3%, TZT -8%, BCOM -1.3%).

… and for some MORE of the news you can use » The Morning Hark - 14 Aug 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

I’d note one from IGM which caught MY eyes,

WSJ: Wall Street Doubles Down on Bonds - The consensus is that interest rates have peaked for this economic cycle, making further investments in Treasurys and highly rated corporate bonds a good bet, analysts managers say.

Moving from some of the news to some of THE VIEWS you might be able to use … In addition TO what was compiled (HERE) and sent over the weekend (HERE), some other items that Global Wall St is sayin’ …

Apollo: The Impact of the Fed Pivot on Consumers (a view … an educated guess)

Data covering the period after the Fed pivot shows that US consumers significantly changed their expectations to interest rates after the December FOMC meeting. Specifically, the share of consumers expecting interest rates to go down jumped to levels last seen during the pandemic and during the financial crisis in 2008, see chart below. With almost 30% of households expecting interest rates to go down, it would make sense if consumers now start borrowing and spending at a faster pace.

BARCAP PBoC Watching: Weaker data to trigger rate cuts (just one CB of many, see BBG writeup below…)

We expect weaker growth momentum and persistent deflation to prompt a 10bp policy rate cut as soon as January. Exchange rate is less a constraint, and the Q4 PBoC MPC meeting vowed to stimulate prices. A likely DPP election win in Taiwan implies heightened tension, but we see limited risk of a more serious turn.

Goldilocks: 2024 Political Outlook: Uncertainty at the Start and End of the Year (deal or no deal, still plenty uncertainty to go ‘round…)

…The next several weeks will be the most critical for the presidential nomination. With former President Trump in an already-dominant position ahead of the first contests in Iowa (Jan. 15) and New Hampshire (Jan. 23), strong performances in those races (e.g., more than 50% of the vote share) could settle the question in the eyes of financial markets. If not, uncertainty might persist until the S. Carolina primary (Feb. 24) or, at latest, Super Tuesday (March 5).

A government shutdown is a clear risk starting Jan. 20, but most funding—including for economic data releases—extends through Feb. 2. A shutdown starting Jan. 20 would likely create pressure to resolve the issue before the more important Feb. 2 deadline. We estimate a two-week shutdown from Jan. 20 would only hit Q1 growth by 8bps.

The fate of Ukraine funding is also likely to become clear in the next few weeks….

Tax relief for 2024 is also on the table, but the odds of enactment before the election are fairly low, in our view….

US-China relations are unlikely to improve ahead of the presidential election…

MS Weekly Warm-up: Macro Outcomes Still Critical for Investment Strategy

After a year that proved surprising to many, 2024 starts with a consensus view that's almost a mirror image from a year ago. We discuss 3 potential macro scenarios. The probability distribution across these outcomes is balanced, but each has different investment implications.

… Scenario 1: Soft Landing... In some respects, this is the backdrop we were in during 2023—a late cycle market environment influenced by policy shifts as well as secular growth themes; employment trends remained solid, but there was (and still is up to this point) little evidence of a meaningful cyclical reacceleration. What works in this scenario? First off, stock-specific risk likely remains high in this outcome (i.e., a stock picker's environment). We'd expect our defensive growth + late cycle cyclicals barbell to continue to outperform. Lower volatility growth stocks also are likely to outperform. More specifically, from a factor standpoint, we'd expect large cap quality to perform well with a particular focus on earnings stability and operational efficiency.

Scenario 2: Soft Landing With An Acceleration in Nominal Growth... The recent dovish shift by the Fed has led to a significant rally in bonds and stocks over the past few months. This loosening of financial conditions could stir animal spirits for individuals and companies, driving accelerated spending/capex and hiring. The recent fall in interest rates may also spur pent-up demand for housing, autos and other durable goods, which have been under pressure from higher rates. This set up could ultimately lead to another rise in rates, but that can still be risk on if growth is improving (equity returns are strong when ISMs and rates are rising together). This outcome is a bull case but it has gained probability share post the December FOMC meeting, in our view. What works in this scenario?This is likely a constructive outcome for risk assets broadly though we'd expect different leadership from what we saw last year. We see small caps, cyclicals and economically-sensitive industries leading in this environment as the rally broadens out in a durable manner. Further, we'd expect value to outperform growth and lower quality to outperform higher quality. Longer duration assets may underperform in relative terms as rate cuts are taken out of the market.

Scenario 3: Hard Landing… Our economists put the odds of a hard landing at 30% over the next 12 months, which is largely in line with buyside expectations from our dialogue. This outcome is aligned with our bear case as discussed in our 2024 outlook. What works in this scenario?From a sector standpoint, traditional defensives would likely outperform in this backdrop—Healthcare, Utilities, and Consumer Staples. From a broader factor perspective, we'd expect high quality to outperform low quality from an earnings and balance sheet standpoint. We'd also expect large caps to outperform small caps and growth to outperform value….

MSs The Weekly Worldview: New Year, Same View (meet the new year same as the old … soft landing for the WIN!)

The jobs data reaffirm our view on the soft landing for the US

The first key US data release for the New Year was the nonfarm payrolls report for December. We read the data as supporting our long-held soft-landing view, that the US is slowing, but not falling into recession. A few aspects of the labor market are worth revisiting to reiterate our view. In terms of market implications, our baseline is that the Fed cuts rates in June, whereas the market-implied timing is as soon as the March meeting. With the slowing in the economy and the substantial degree of disinflation that we have seen so far, the risks to the forecast are likely skewed to an earlier rather than later start to rate cuts, but we are still comfortable with our baseline view.

First, monthly nonfarm payroll gains have been declining for the past couple of years. The strong 220k average over the past six months stepped down to a soft, but not especially weak, average of 165k per month over the past three months. Friday’s upside surprise of 216k shows that there will be noise in the data even though the trend is down.

Part of our thesis for a soft landing relies on businesses reducing demand to hire new workers over time, but not laying off large numbers of workers…

UBS: Reducing shutdown risk (reduced but not eliminated as this deal appears to be same which ran McCarthy out of town…?)

In the US, the official leaders of Congress have agreed to a spending limit. This reduces the risk of a government shutdown although no legislation has been passed and details still need to be agreed. The spending limit has been denounced by the hard right Freedom Caucus, which presents a challenge for House Speaker Johnson. When another Republican leaves the House on 21 January, the Republicans will hold 219 seats to the Democrats’ 213.

Last Friday’s US employment report offered something for everyone in the data although the subsequent political spin offered few surprises. Inevitably, preconceived ideas of the direction of Federal Reserve policy remain intact. We hear from the Fed’s Bostic today, and it will be interesting to see if the coordinated resistance to Fed Chair Powell’s comments continues.

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Bond Traders Seize on 4% Yields, Confident Fed Rate Cuts Coming (seems like BBG trying to drum up buyers for duration supply this week … and counter TO some of what was found HERE over weekend where, for example, one of the best in show — BMO — not YET buyin’)

Investors piled in after strong jobs data caused yield jump

Market faces next test with inflation data, 10-year auction

Traders betting on a 2024 bond rally are unfazed by the recent pullback, seeing it as a chance to seize on elevated yields before the Federal Reserve starts driving down interest rates.

The dynamic was on display Friday, when bond prices dipped after the Labor Department reported that job growth unexpectedly accelerated last month. But the selloff was curtailed because buyers swooped in as 10-year Treasury yields neared 4.1%, the highest since mid-December.

The rebound — even in the face of data showing continued strength in the economy — highlighted the stark shift in sentiment over the past two months, with investors increasingly confident that the bond market is firmly recovering from its worst downturn in decades. Despite the recent backup, yields are still well below October’s peaks as traders wager that the Fed may start easing monetary policy as soon as March.

“Anything between 4% and 4.2% is a buy” for the 10-year, said Priya Misra, portfolio manager at JPMorgan Asset Management, noting that the yield was at the upper end of that range ahead of the last Fed meeting. “For 4.2% to break, we have to bring hikes back in or take out overall cuts.”

The rally that gripped the bond market during the last two months of 2023 put an end to what had been the worst losses in decades, driving Treasuries to a gain for the year and bolstering conviction that yields won’t retest the previous peaks. While investors are mindful that yields may drift higher if incoming data alters expectations about the Fed’s likely path, some big investment firms have been looking at recent drops as good times to buy….

Bloomberg: Fed Pivot Will Dominate Year of Rate Cuts in Turn of Global Cycle (kinda stating of the obvious but … thats why you pay so much for a Terminal … interesting in the deflection from a US CENTRIC debate, no?)

Quarterly outlook on what to expect from monetary policy

About-turn follows most aggressive tightening in decades

The coming 12 months are shaping up as the year of the interest-rate cut.

After racing ahead with the most aggressive tightening campaign in decades during 2022 and 2023, central banks around the world are poised to begin easing monetary policy as inflation continues to retreat.

The shift is captured by Bloomberg Economics, whose aggregate gauge of rates across the world shows a decline of 128 basis points over the year, mostly led by emerging economies.

Among such central banks, those in Brazil, the Czech Republic and others have already started that process.

The US Federal Reserve will lead the pivot for richer countries after its policy makers signaled 75 basis points of cuts for the year, marking an abrupt shift from previous warnings that rates could still go higher through much of 2024.

Others, such as the European Central Bank, are more reticent to signal cuts, but Bloomberg Economics expects the first easing there is likely to materialize in June. Markets are betting the Bank of England will cut that month too.

Japan will remain the standout among its peers, with Governor Kazuo Ueda expected to tighten policy at last, by ending the world’s last negative rate…

Bloomberg: Let's not overdo it on the markets overshoot (Authers’ OpED — he’s got a point here …)

Overshooting. It’s What Markets Do Stock prices fell, so did bond prices, and a miserable time has been had by all. That is the story of 2024 so far. As two of the worst years for US stock market history, 2008 and 2022, both started with a really bad first week of January, that’s already unleashed concerns that another horror year lies ahead.

That’s overdoing it. The sample size for bad early Januaries leading to really bad years is two. There’s nothing to build an argument on. However, it does, as one of my friends keeps putting it, make sense to respect the price action. Investors want to retreat a little from some of their recent bullish bets, and it’s best to accept that.

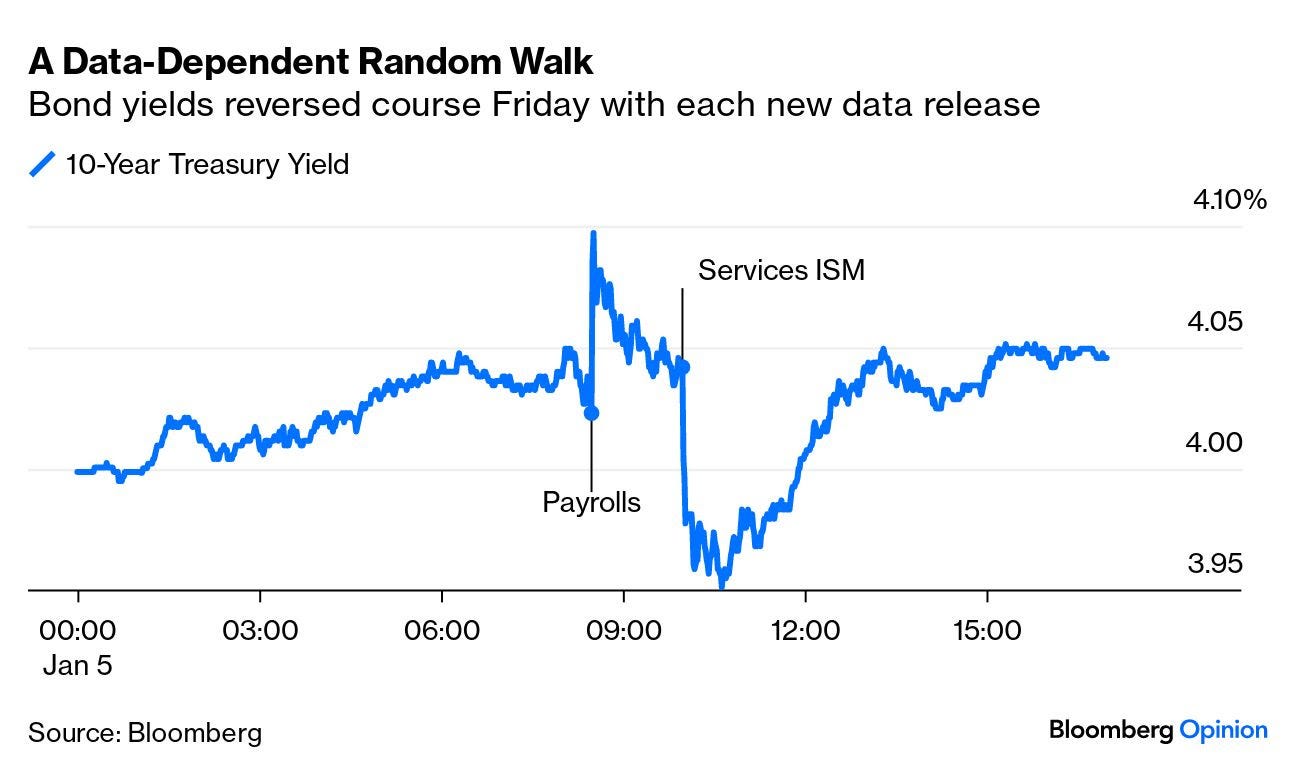

Why the turbulence? Friday witnessed a classic rollercoaster on the US Treasury market. First the raft of unemployment data came out at 8:30 a.m. on the East Coast, followed 90 minutes later by the Institute of Supply Management survey of the services sector. This chart of the 10-year yield shows that these two data downloads had very different receptions:

The employment numbers portrayed a much stronger economy than had been thought, while the services data was surprisingly weak. You can read plenty more analysis here. But to be clear, both were bona fide surprises in different directions…

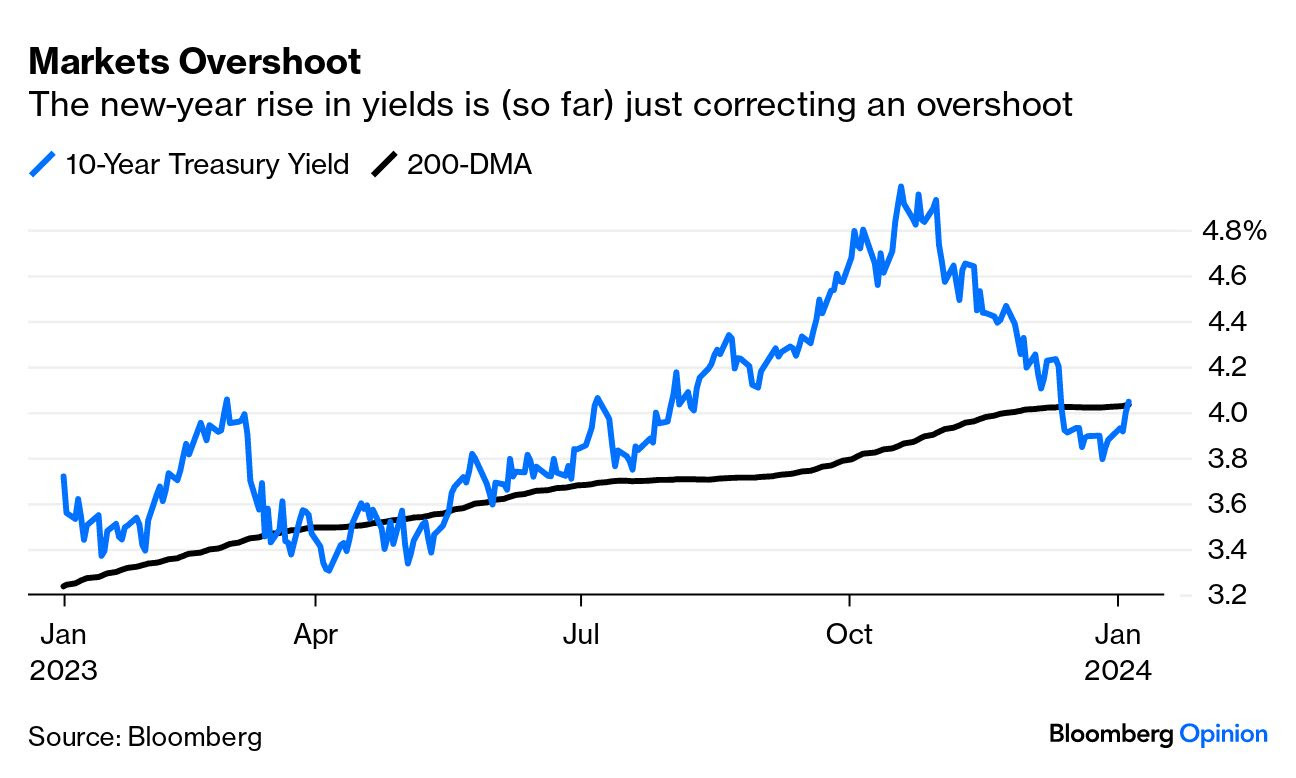

… So, the direction of markets made sense, even if the data — taken conjointly — did not. By Friday’s close, the 10-year yield was back up above 4%, and had roughly returned to its level before the employment data came out. Looked at in wider perspective, it had also come to rest almost exactly on itslong-term trend, as measured by the 200-day moving average:

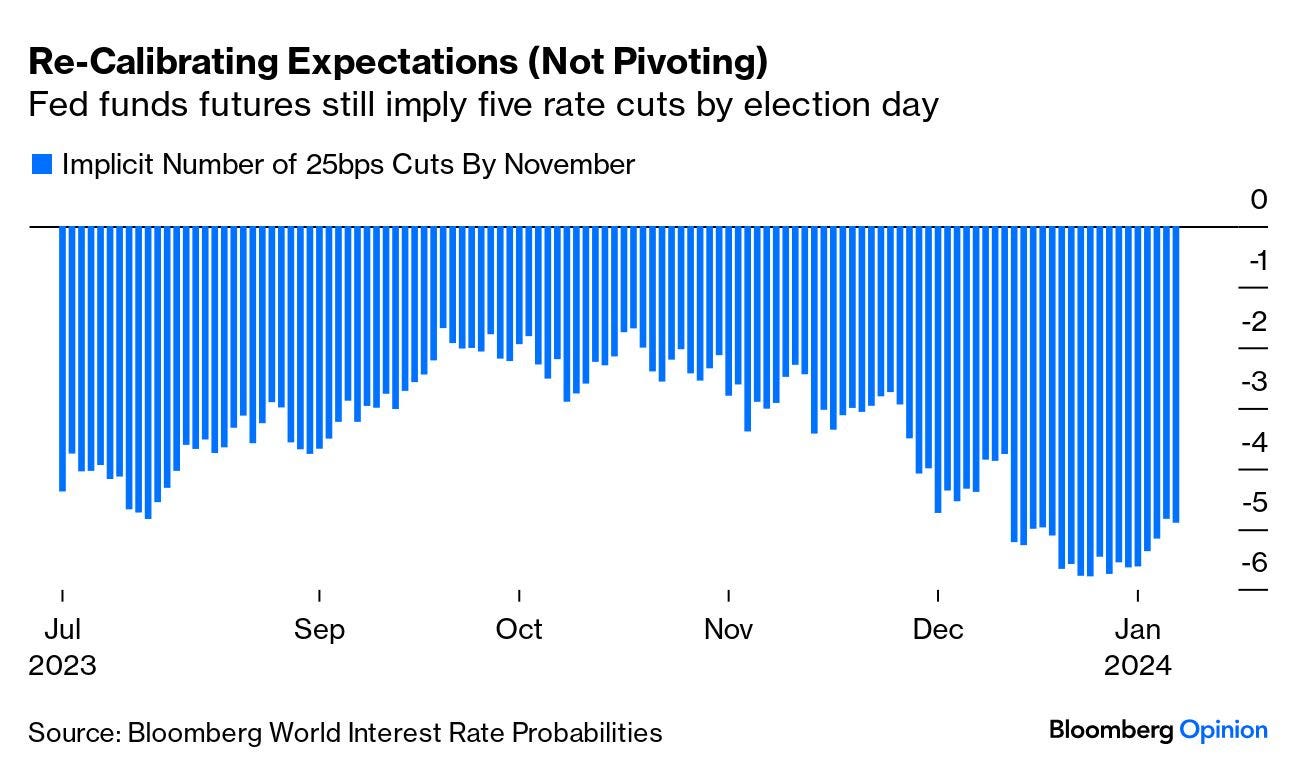

That implies that the first week’s price action should be interpreted as an acknowledgement that expectations of massive rate cuts starting within weeks had been overdone. But not that there’s any need for a reversal. Using the Bloomberg World Interest Rate Probabilities function, this is how the number of implicit 25 basis-point cuts by the US election on Nov. 5 has moved since the Fed’s last rate hike in July:

The market is still braced for five cuts by November, which is a lot. Politics might help to explain this, as the Fed will want to start easing soon to avoid the impression that it’s manipulating the run-up to help President Joe Biden’s reelection chances. But it remains hard to see how the central bank could possibly justify cuts on the scale now expected unless the economy plainly slides into a recession (or some major financial incident increases the odds on one).

-Heard on the ski lift in early 2000s parents could get 3 lessons w/boots poles ski rentals for $99, now it's $224, but HEY that's a WAY low flation' rate than M2 in the same timeframe!

-Appreciate the words & thoughts yesterday, it's the blowhards who seem to reap the BIG rewards these days (Words are wind?!?)

-As a Gov employee in my adulthood, we generally don't take a 2nd job, we just do more OT (chronic understaffing is permanent Gov feature, cause Great Jobs you know). However, the Tenor of that OT has changed since the 90s. Decades ago if you wanted to save for a car or trip you did more OT, you didn't necessarily charge it. Now, OT for most people is a matter of survival. Period.

-Heard on the ski lift in early 2000s parents could get 3 lessons w/boots poles ski rentals for $99, now it's $224, but HEY that's a WAY low flation' rate than M2 in the same timeframe!

-Appreciate the words & thoughts yesterday, it's the blowhards who seem to reap the BIG rewards these days (Words are wind?!?)

-As a Gov employee in my adulthood, we generally don't take a 2nd job, we just do more OT (chronic understaffing is permanent Gov feature, cause Great Jobs you know). However, the Tenor of that OT has changed since the 90s. Decades ago if you wanted to save for a car or trip you did more OT, you didn't necessarily charge it. Now, OT for most people is a matter of survival. Period.

Excellent information !!!!

Thanks......