This morning I am going to lead with an updated look at 30yy WEEKLY (as they will be up for sale Thursday, AFTER CPI data dust has settled)…

… and while the belly (5yy) might not show as decisive a BEARISH BREAK, it is worth noting there is a tough, weekly (so a more medium term) setup further out the yield curve. There IS a way / reason one could say this is GOOD as it could be a reasonable concession for duration (3s, 10s and 30s this week) … I’ll simply note some of the best in the biz are setting up SHORT (here … some WEEKLY NARRATIVES for YOUR review). TIME at a price or a bit more of an upward push to resolve and only TIME will tell how this resolves…

Now, ahead of this evenings futures market open I wanted to reach out and first, say thank you AGAIN for slowing down and finding / sticking around this spot on the intertubes.

It started as a place for ME to vent - a financial markets diary of sorts - having used ‘the pen’ as a career tool long before things like Substack existed.

In my former line of work as an ‘interest rate strategist’ (bond trader’ing / sales) who was once ‘armed and dangerous’ with a Bloomberg Terminal, I’d ‘compete’ for buyside attention like all of Global Wall Street’s evil sellside.

I never claimed to be smarter or more tech saavy but one thing I could always do is out work colleagues in my role. I could also LISTEN.

Much of Global Wall Street is filled with ‘enough ‘bout ME, what do YOU think of ME’ kind of personalities.

Never interested in that and perhaps to my own detriment. Be that as it may, I continue to believe that YOUR (and my former clients) time was most important and untradeable commodity and so I began down the path of waking up earlier than everyone, reading MORE than most and then offering not only MY techAmental view of global MACRO but also a look at what everyone ELSE was saying / thinkin’ / sellin’.

In real time.

Things that ultimately would find their way up to places like ZeroHedge. A source of information (along with a few friends from my past lives) which has taken a prominent role here (sorry, not sorry).

MY view always was and remains that YOUR view — whatever your role may be — is more important than Global Wall Street’s sellside AND mine. Combined.

Happy to offer MY view if asked. I will continue to hint at that here on this ‘stack and it will ALWAYS be based on my now somewhat limited technological capabilities (ie NO Bloomberg Terminal with which to economically workbench and then present data like this Bloomberg TWEET by Anna Wong (chief econ) AT AnnaEconomist (suggesting belief that ISM > nfp and I gotta be honest with you … am NOT 100% there and behind that message … for more SEE YESTERDAYS NOTE, HERE).

Getting down off my Sunday soapbox, and in addition TO what was compiled (HERE) and sent over the weekend (HERE), some other items which Global Wall St is sayin’ …

BNP Sunday Tea with BNPP: Caution on consensus trades (jives with what one of best in biz — BMO — saying and frankly, I’m in full agreement with this sentiment BUT …)

KEY MESSAGES

Going into CPI this week, we believe that markets will react more to a high print than a low one. We see tactical upside risks to US yields.

With the market having entered the year short USD, we like hedging structural short USD exposure at these levels.

As US earnings season kicks off, there are downside risks to earnings expectations. With equity skew at very low levels, we like owning puts to protect the downside.

… Looking ahead, we expect to see a sharper deceleration of the US economy in H1 2024, forecasting growth to contract by Q2. We also expect the Fed to cut to a deeper terminal level than currently priced, and thus continue to like steepeners and short USD positions from a strategic perspective. However, going into this week we think that both positions can be challenged and tactically recommend lightening / hedging exposure.

This is because we see asymmetric market risks around this week’s key data release – CPI on Thursday. More specifically, we think the market will react more to a higher-than-expected number than vice versa. A majority of the increase of cut pricing for this year has occurred because of a reassessment of one side of the Fed’s dual mandate: not only has inflation fallen rapidly in recent months, but also the market expects further material progress through the year (Figure 2).

Therefore, we think a higher-than-expected inflation print (we forecast a core CPI rise of 0.3% m/m versus 0.2% consensus) will challenge the notion that the road to 2% will be a smooth one. And with a 70% chance of a rate cut priced in for March, we see scope for expectations of cuts to be both pushed back and taken out of the curve…

MS: Sunday Start | What's Next in Global Macro: We Three Themes

Welcome to 2024. Just as in 2023, we present three key secular themes we believe will have profound impacts on markets for many years. A culture of collaborative, cross-asset, cross-discipline analysis has long been core to our mission. We believe this is necessary to master the complex, secular themes that make the difference to being ahead of or behind the curve in rapidly changing markets. You seem to agree, with our thematic research among our most read work last year. To that end, in what’s become an annual exercise, we gathered analysts from around the globe to assess our current thematic focus, identify prospective new themes, and establish a plan to deliver in-depth, collaborative insights for our focus themes in 2024.

We retain two of our prior three themes (AI tech diffusion and decarbonization) while adding a new one…longevity. Why not three entirely new themes? Because these trends tend to endure for and evolve over multiple years. Hence, ongoing research in these areas is important for keeping our asset class views and forecasts appropriately anchored. To that end, here are our insights in brief on the importance of and our approach to these three themes:

Longevity: There are ramifications across myriad sectors for years to come from the life-affecting and extending effects of innovation across the pharma space, be it the advent of GLP-1s, smart chemo, or the potential implications of AI for drug development. There are both micro and macro impacts to assess from effects on demographics, consumer habits, the healthcare system, government finances, and how we plan our futures financially…

… and from the intertubes …

Apollo: 2024 Outlook for Private Markets (I’ll move Slok updates from ‘paywalled’ Global Wall St inbox to here as any / everyone interested can / should sign up for updates …)

Fed cuts and lower costs of capital could boost private markets in 2024. Our latest chart book is available here.

Bloomberg: JPMorgan Strategists See Treasuries’ Rally Resuming After ‘Rest’ (this, after having gotten OUT of 30yr LONG just before NFP … they see move UP then down and so, in other words, have cake and eat cake, too … no matter WHAT happens they will have ability to say THEY TOLD US SO … typical sellside!)

JPM’s Hunter, Kolanovic see 10-year yield moving up, then down

Goldman’s Korapaty says benchmark yield likely to be around 4%

… “Bigger picture, we expect the rally to develop further after a period of consolidation relieves the current overbought conditions,” the strategists said. “Look for 10-year note weakness in the early weeks of the year to find solid support at 4.25 to 4.30%,” an area where they expect “material buying pressure.”

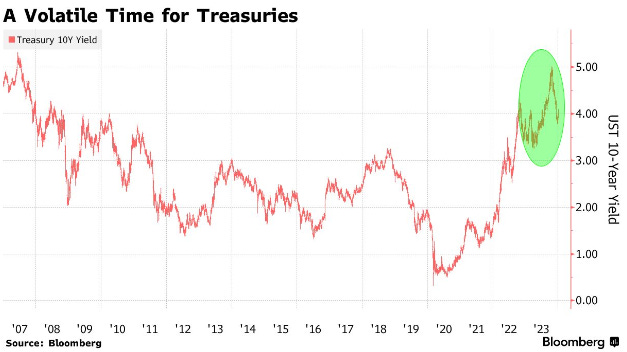

… The 10-year yield ranged between 3.25% to 5.02% during 2023, with levels above 5% - albeit barely - seen for the first time since 2007. The ICE BofA MOVE Index, which measures volatility in Treasury options, hit its highest levels since the global financial crisis 16 years earlier.

Meanwhile, a Goldman Sachs team led by chief interest rate strategist Praveen Korapaty said in a note Friday that they see the 10-year yield hovering around 4%. That’s amid a growth rebound this quarter, further progress on lowering inflation, and anticipation of another round of increases in Treasury auction sizes…

MacroVisor: The Weekend Edition # 117 - Weakest Start since 2008

Sam Ro from TKer: The stock market will often fall on its way up (reading thru this I cannot help but think FED will need more DEMAND DESTRUCTION evidence before putting paid TO current rate cut pricing … just a thought …)

Finally, as I hit SEND and prepare to watch some football — Week 18 is by and large meaningless while tonights game (Dolphins v Bills) is going to be a good one — I will reiterate a couple things.

First, my gratitude for your time and I HOPE this continues to evolve in such a way it proves worthy (for all of us) and SECOND, I’d like to mention that this all is nothing without feedback. Good AND bad, do not ever hesitate to reach out.

It is with that in mind, I’d like to end by highlighting another Substack I’ve come across recently and after dialoguing, would suggest you head over and have a look for your self.

It is tailored to JUNK debt and while I never traded that, I can say that debt is at the root of all that is <evil / good> choose one and watching where high yield goes might help those like ME with an interest in global MACRO, as HY and equities are often times one and the same … For somewhat more see Apollo and for NOW, I’d suggest you have a look at,

For those new to the newsletter, I write about complex situations that I personally find interesting. Typically, these involve credit/credit-like instruments (e.g., preferred equity, trusts, post-reorg equity, etc.). Consider these write-ups as real-time diligence journals summarizing complex situations that often require a credit investors’ perspective. Importantly, I tend to avoid names/situations that are already well-covered, even within distressed debt, because you can already find a plethora of information on these situations from the likes of sell-side, independent credit research, or even Twitter. Rather, this newsletter aims to systematically review companies that lack even basic coverage, in the hope that this might create mispricing opportunities. By definition, many of these situations are illiquid, not actionable in size, and/or have very wide bid/ask spreads. Almost always, these are low-quality businesses (i.e., #shitcos) which means they are NOT long-term investments but trades that must be monetized …

Check it out and let me know what you think. Finally, how I envision YOU clicking up / reading this note …

(substitute AD for POST) and … THAT is all for now. Enjoy whatever is left of YOUR weekend …

{kind=link}

Agree with much of the commentary....

Rates backing up for the Bond auctions, then lower, as the economy decelerates...

I for one, really like your choice topics and format of your newsletter.

I always learn a lot, every time I read it.....

Certainly an interesting time in the FI markets...

Please continue your FINE WORK !!!