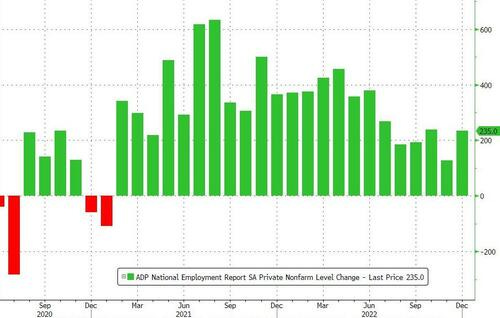

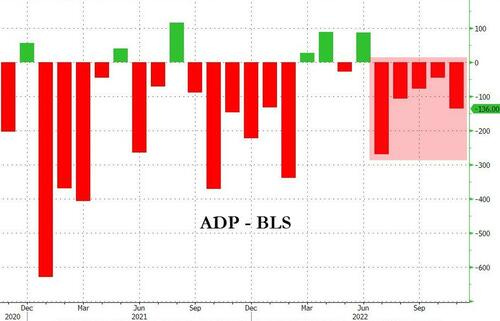

… Finally, we note that ADP has under-forecast (fewer jobs added) the BLS numbers for 5 straight months...

For somewhat more cerebral approach

BMO: ADP +235k, Claims 204k, TSY Weaker, Curve Inversion Extends ADP printed at +235k Dec vs. +150k consensus … As for the wage data, job stayers saw a 7.3% annualized pay increase, while job changers received an average 15.2% increase in compensation … Initial jobless claims in the week ended December 31 came in at 204k vs. 225k forecast and the prior read was revised slightly to 223k from 225k. Continuing claims in the week ended Dec 24 were 1694k compared to the 1728k consensus and prior was revised to 1718k from 1710k. Overall, a series of data consistent with front-end weakness and a deeper curve inversion…

Oh never mind … here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mixed with the curve extending flatter around little-changed intermediates after a ghostly quiet, pre-NFP session overnight. DXY is higher (see attachments) at +0.4% while front WTI futures are little changed. Asian stocks were modestly higher on balance, EU and UK share markets are little changed while ES futures are UNCHD here at 6:45am. Our overnight US rates flows saw a quiet, curve flattening session with some real$ buying in the long-end noted during Asian hours. Overnight Treasury volume was a bit below average with 7's (144%) seeing the highest relative average turnover overnight.

… Our next two attachments focus on curves that markets and the Fed monitor for recession warning signals. The first shows the Tsy 3mo-10y curve with recession shading added. While notably flat, experience would suggest that the recession alarms only ring when this curve rebounds back to flat or above and we're certainly not seeing that yet. A similar story with the Fed's preferred curve, the 3mo Bill versus 18mo forward 3mo rate curve which is shown next. Here's the San Fran Fed suggesting late last year that a recession countdown may be 'on the clock' based on the unemployment rate at least FRBSF These two curves might concur

… and for some MORE of the news you can use » IGMs Press Picks for today (6 JAN) to help weed thru the noise (some of which can be found over here at Finviz).

From NEWS to some VIEWS and narratives from the Global Wall St inbox. Here’s one may be of interest in light of jobs data (past and future) from a large German bank

Quits and the Curve Our UST rate forecast for this year has 2s10s steepening to 50bp, driven by recession in H2 and Fed rate cuts starting in December. However, given still-elevated levels of inflation and inflation risk, we’re looking for further rebalancing in the labor market before recommending steepeners.

Evidence on the relationship between the private sector quits rate and wage growth supports focus on quits as a key indicator of labor market slack. The quits rate is also strongly associated with the contemporaneous level of 2s10s, controlling for other variables meant to capture the curve’s recessionary signal. Based on pre-Covid dynamics, the current quits rate of 3.0% is consistent with 2s10s at -35 to -50bp, moderately above recent levels. Quits at 2.5% would be consistent with our forecast of 2s10s at 50bp later this year, suggesting this level of quits as an implicit target for our forecast.

Timing of what some may consider to be THE trade of 2023 — steepener of one variety or another — makes this one note of particular interest …

From the braintrust that helps define the ‘official fed’ narrative, from the bowels of Liberty Street where a NY Fed study finds inflation remains too high BUT some indicators signaling improvement … make if IT (The Layers of Inflation Persistence) whatever you want and NOTE the conclusion,

… To conclude, however, while recent developments are in the right direction, the MCT is still way above its pre-pandemic level and consequently well above a level consistent with price stability.

Are we clear here, yet? Stocks down. bonds down incorporating ADP, Claims, FOMC and Fedspeakers yest sorta makes me think markets are slowly coming ‘round?

…In the meantime, these signs of strength in the labour market data led investors to price in a more aggressive path of rate hikes from the Fed yesterday. For instance, the chances they’ll continue hiking by 50bps at the next meeting in February now stand at 44.2% according to futures, which is up from 32% the previous day. And looking further out, the terminal rate priced in for June hit a 6-week high of 5.03% (cycle high 5.146% - Nov 3rd), with the year-end rate for December also up +13.6 bps to 4.67%.

Those views on the future policy path were given added support by the latest speakers from the FOMC. For instance, Kansas City Fed President George said that the Fed should keep rates above 5% into 2024, and Atlanta Fed President Bostic said that inflation was still “way too high”. St. Louis Fed President Bullard last night spoke a little more dovishly when he said that “the policy rate is not yet in a zone that may be considered sufficiently restrictive, but it is getting closer.” In a presentation, Bullard cited the recent FOMC dot plot showing the median projection of 5.1% as being adequately restrictive…

Now as far as what the Fed seems to be saying vs what markets are pricing, well, I cannot say it better than THIS REPORT from a large French bank

We initiate a May 2023 versus December 2023 1m OIS curve steepener, as markets continue to ‘fight the Fed’ on H2 2023 rate cuts and this is ultimately a losing battle, in our view.

Since mid-June 2022, markets have priced about 40bp of rate cuts on average for H2 2023, despite clear and repeated pushback from the Fed.

We think markets are too optimistic that the Fed has induced a disinflation trend even though core services inflation remains extremely high. This, coupled with a resilient labor market, means there is still potential for an unwelcome wage-price spiral.

While we forecast a US recession in H2 2023, we do not anticipate an easing cycle until 2024….

They go on to detail some trade ideas // expressions to help you NOT fight the fed. They like things like 1m OIS steepeners, receiving May OIS vs Dec and I’ve gotta be honest with you, once we start introducing concepts of swaps and receiving … well, they’ve sorta lost ME but then again, I’m now just a casual spectator …

For the more pedestrian view and keeping theme of NOT fighting the fed in mind, Bloomberg

… “Don’t Fight the Fed!” is supposed to be a Wall Street mantra, but these days it is definitely more honored in the breach than otherwise. Rates traders remain insistent the Federal Reserve will be cutting interest rates by year’s end. They are ignoring a slew of policymakers as they reiterate that the plan is to hike further into restrictive territory and then hold rates there until inflation has been fully tamed.

That leaves bonds and stocks vulnerable to rapid reversals, with US December payrolls due Friday looming even larger than normal as a result. Upside surprises would bolster Fed hawks who are already way more aggressive than the market expect. Even results in line with expectations could be enough to spur fresh hawkish commentary, given that persistent bets for the Fed to lower its rate in the second half of 2023 are already helping to make financial conditions the loosest they’ve been since September.

There maybe some within the Fed attempting to … well, fight the fed and at one point yesterday, the BULLard presentation hit and mkts reacted,

I’ve made it this far without any mention of NFP narratives and so …

Donovan / UBS: A tale of two employment reports Today, a group of people with English literature degrees will gush about data that people with economics degrees know to be wrong—it is US employment report Friday. Data shows there is no net job creation, or booming job creation. Job offers are high, but real wages are low. Markets obsess about average hourly earnings, which are not wages (the number of low skilled workers employed impacts the data—incidentally, members of Congress are being paid for this week).

There clearly has been a structural shift in global labor markets. While job offer numbers are high relative to unemployment, they are not especially high relative to hirings. Job offers are being filled. This suggests ongoing churn in the labor market, with people moving companies more than normal…

Here’s another take from Ed BOND VIGILANTE Yardeni (who’s got both journalistic as well as econ degrees,

Strong Labor Market Frustrates Fed On August 27, 2020, Fed Chair Jerome Powell's speech at Jackson Hole explained why on that same day the Fed issued a revised Statement on Longer-Run Goals and Monetary Policy Strategy. The statement and Powell's remarks stressed that monetary policy would focus on reviving the labor market after it was weakened by the pandemic. Powell said: "With regard to the employment side of our mandate, our revised statement emphasizes that maximum employment is a broad-based and inclusive goal. This change reflects our appreciation for the benefits of a strong labor market, particularly for many in low- and moderate-income communities."…

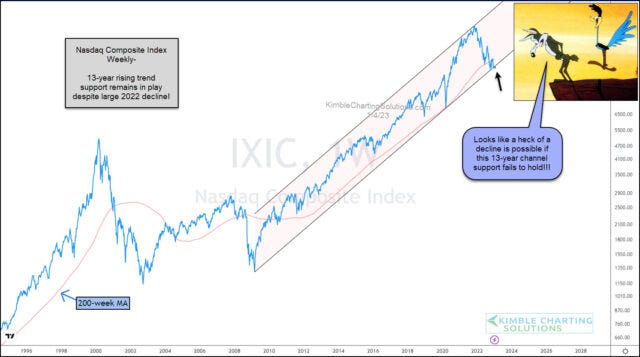

From the ivory towers back down to earth and searching out some sort of truth in price (at least thats a technical analysts creed), so a couple technically inclined charts and links … FIRST from Kimble on high tech (as we know there’s a relationship with longer end of the curve),

… For the past year and a half, I have looked to developed market yields outside the US for insight into the direction of domestic interest rates. It has proven invaluable on multiple occasions.

The rationale (based on rising rates worldwide) works both ways. It follows that developed market yields should confirm one another as long as the rising rate remains intact. And when they don’t, it raises an eyebrow or two.

Here’s a daily chart of the US 10-year yield highlighting the divergence:

Sure, the underlying trend moves up and to the right. I’m not arguing that it isn’t.

Just consider, perhaps, US rates have it right? And developed yields worldwide head lower from here.

I’d have to witness a breakdown in the US 10-year below 3.40% before taking that stance from an intermediate time frame.

If it does, our recent bond setups likely fire buy signals again, and long-duration assets such as communication and tech stocks will probably enjoy a reprieve from selling pressure…

So, in other words, WHEN 10yy hit 3.40 (they are currently NORTH of 3.70 — see visual just above), this is when allstars will be ‘buyin it’ and “taking that stance from an intermediate time frame.”

FYI, from my former front row seat in that market, it’s precisely THEN where the pros will likely be unloading their book TO retail, saying thank you very much, and looking for a way to preserve those gains or leverage them into a different market / space and add some more zeros to their 2023 bonus…just sayin’.

Have been thinking more about your references to the 'narrative-makers' now that I've picked through a tiny sampling of the FI sell-side content you used to post via the google-drive links. Rather than use this as platform to wax-stupid about my ill-conceived understanding(s), principally (at the moment at least) about the FI marketing machine and the complete(?) distortion that has been wrought upon Capital Markets (from their purpose(s) as immaculately conceived in textbooks) via forces beyond our willingness to shape and control, that are nowhere near to being licked into shape, I'll just post a couple of recent links that help me to keep the daily volatility grind in perspective while serving as a useful reminder not to forget what I already learned watching over my equities.

I suppose buried in there is one of the key reasons the sell-side opinion maker fraternity are constantly trading places as they strive to create and propagate narratives. The 'power' and 'money' to be harvested once you've implanted a narrative that catches on is probably irresistible for many. I know many will say "Doh!", and they are correct to point out that this is hardly an earth shattering observation in speed-of-light Influencer driven Krill & Whale Capitalism, but still, the sheer scale of it is so vast and shifting it will tax the brightest and long-living student foolish enough to attempt to understand the whole organism. I suppose most of us confronted with such complexity wisely(?) only attempt to tackle a bit-player or two and humbly accept we are no less someone else's Krill, and then hope we make it to Retirement before getting Whaled ourselves. So, it is understandable in a twisted way how attractive it must be to calf off (capture) your own school of Krill, feed them on a narrative as long as possible, and then use second and third order anticipatory game-theory thinking ("strategic sophistication") to harvest them now that you have insight into how most of the school will zig and zag for a time or two ahead.

Apparently Krill never tire of getting bubbles blown up their.... The metaphor suggests the importance of the SEC for resource management and mitigating the dangers of over-fishing leading to ecosystem collapse I suppose.

Of course, I could be utterly wrong and would be better off working on my belly-button lint collection.

Have been thinking more about your references to the 'narrative-makers' now that I've picked through a tiny sampling of the FI sell-side content you used to post via the google-drive links. Rather than use this as platform to wax-stupid about my ill-conceived understanding(s), principally (at the moment at least) about the FI marketing machine and the complete(?) distortion that has been wrought upon Capital Markets (from their purpose(s) as immaculately conceived in textbooks) via forces beyond our willingness to shape and control, that are nowhere near to being licked into shape, I'll just post a couple of recent links that help me to keep the daily volatility grind in perspective while serving as a useful reminder not to forget what I already learned watching over my equities.

https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr1044.pdf

The plain English synopsis and link source:

https://www.bloomberg.com/opinion/articles/2023-01-04/the-fed-may-have-discovered-the-secret-to-successful-trading

I suppose buried in there is one of the key reasons the sell-side opinion maker fraternity are constantly trading places as they strive to create and propagate narratives. The 'power' and 'money' to be harvested once you've implanted a narrative that catches on is probably irresistible for many. I know many will say "Doh!", and they are correct to point out that this is hardly an earth shattering observation in speed-of-light Influencer driven Krill & Whale Capitalism, but still, the sheer scale of it is so vast and shifting it will tax the brightest and long-living student foolish enough to attempt to understand the whole organism. I suppose most of us confronted with such complexity wisely(?) only attempt to tackle a bit-player or two and humbly accept we are no less someone else's Krill, and then hope we make it to Retirement before getting Whaled ourselves. So, it is understandable in a twisted way how attractive it must be to calf off (capture) your own school of Krill, feed them on a narrative as long as possible, and then use second and third order anticipatory game-theory thinking ("strategic sophistication") to harvest them now that you have insight into how most of the school will zig and zag for a time or two ahead.

https://en.wikipedia.org/wiki/Bubble-net_feeding

Apparently Krill never tire of getting bubbles blown up their.... The metaphor suggests the importance of the SEC for resource management and mitigating the dangers of over-fishing leading to ecosystem collapse I suppose.

Of course, I could be utterly wrong and would be better off working on my belly-button lint collection.