(USTs higher, belly BID - thanks ECB - on less light volumes)while WE slept; recession odds CUT (GS); housing; "End of the Bond Bull? Not so fast…." and gas prices relative to incomes

Good morning … this morning will be last ‘regular’ hit until next week as noted this past weekend. Try not to break anything while I’m gone. Like tomorrow’s 20yr auction,

NOTE: momentum from oversold TO nearly overbought and in a couple short sessions. 20yy are AT 50dMA (4.06%) which COULD become important (will only know IF it holds as RESISTANCE and as always, the benefit of hindsight wins the day). The price action has 20yy within recently redrawn and so, still triangulating range … Granted, he WITH crayon says when trend remains yer friend and knowing this, I’d strongly urge one and all to head TO Terminal or TradingView or whatever and etch in your very own TLINES and things…

In as far as WHY the bid?

BBG: Bonds Rally as ECB Official Signals Rate Reprieve: Markets Wrap BBG: Yellen Sees Disinflation Pressures at Work as Hiring Surge Fades

Well thank you ECB and officials NOT whole-heartedly endorsing further hikes.

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries have been led higher this morning (belly outperforming) by German bonds after ECB GC member Knot said today that ECB tightening beyond next week's meeting is "at most a possibility, but by no means a certainty." (Yahoo). DXY is lower (-0.2%) while front WTI futures are modestly higher (+0.5%). Asian stocks were mixed, EU and UK share markets are little changed while ES futures are also little changed here at 6:55am. Our overnight US rates flows saw belly out-performance emerge in Asian hours with the desk noting some front-end selling from real$ in otherwise quiet conditions. London's AM hours were quiet too with on-balance buying from real$ seen- focused on the 10y point. They also noted evidence of receiving in swaps given the tightening in spreads in recent hours. Overnight Treasury volume was ~95% of average overall with Japan back from holiday today.

… Our first attachment this morning looks at the weekly chart of Treasury 5yr yields after they tested and held support derived by their fall '22 move highs earlier this month. What is also quite clear is that there remains a barrier of demand for US 5yrs near 4.35% and above (no weekly opens or closes above the level this policy cycle). Anyway, medium-term, weekly momentum (which tends to guide for 2-4 month moves) is somewhat 'oversold' and looking ripe for a new bull signal- one that will need a week-end/Friday close for confirmation. So no sign of a sustainable bull turn yet- but the set-up is decent for that if the data plays along.

Next we show the weekly chart of 5yr (TIPs) real yields. We like 5yr reals' potential bull set-up even better after the false bearish breakout early this month. Indeed, if the emerging momentum signal (lower panel, circled) is confirmed on Friday, we'd guess that a return to the recent range lows near 1.00 becomes a legit threat from now into Q4.

… and for some MORE of the news you can use » Finviz « worth a point and click …

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ …

As the narratives churn from day to day, this first note a reasonable acknowledgement,

The probability of a US recession has fallen further as both recent data and ongoing fundamentals point to rapid—and mostly painless—disinflation from here. We don't share the concerns about yield curve inversion as a recession predictor because 1) the term premium is lower than normal, 2) there is a plausible non-recession path to cuts, and 3) we think rates investors, like forecasters, have yet to take the recent signs of a soft landing fully on board.

… Valuation remains a challenge for the risk asset outlook, but the newsflow should remain broadly supportive in the near term. Our US equity strategists expect companies to meet or exceed the low bar set by the consensus forecast that S&P 500 earnings per share will fall 9% year-on-year in Q2, our credit strategists continue to recommend overweight positions in lower-rated bonds given the benign backdrop in defaults and ratings migrations, and our FX strategists predict continued near-term downward pressure on the dollar. On the rates side, our strategists are looking for a widening of US breakevens; although we usually find ourselves on the optimistic side in the inflation debate among economists, rates market pricing of inflation is even lower than we think is justified, probably in part because of greater worries about recession. Lastly, we see room for the oil market rally to extend in the near term, though the upside is probably capped by the increase in OPEC spare capacity on the back of the series of production cuts over the past year.

And with narratives churning, an outlook for the week ahead and a question,

The best news last week was that inflation came in below expectations for June. Consumer prices rose a moderate 0.2% for the month, while producer prices increased only 0.1%.

the month, while producer prices increased only 0.1%. That was good news for both stocks and bonds, because it made it less likely the Federal Reserve would raise rates multiple more times this year, in turn reducing market perceptions about the risk of an eventual recession. Meanwhile, the news boosted the markets’ odds the Fed would be in a more aggressive rate cutting mode in 2024, not necessarily because the economy would be weak but because inflation would be low.

We think the optimism is overdone. The M2 measure of the money supply has dropped in the past year and we think that drop is starting to gain traction, including in the form of lower headline inflation…

… If the M2 measure of money (next reported Tuesday July 25) declines further, then, yes, perhaps better inflation news is ahead, including a continued decline in core inflation, as well. But it’s hard to see a drop in core inflation down to the range of 2.5% or below unaccompanied by some significant economic pain. In the past several decades a drop in core inflation of 1.5 percentage points or more over the course of two years has always been associated with a recession. Now the Fed is projecting that size drop in core inflation in about one year, not two.

If core inflation drops substantially, that also means many businesses will find their pricing power is less than they expected. That should undercut corporate profits and restrain business investment…

… The bottom line is that if the Fed keeps the money supply trending down it will succeed in bringing inflation down. But we remain skeptical it can pull that off while leaving the economic expansion intact.

With inflation in mind one thinking of the Fed and guidance ahead of the upcoming FOMC meeting will either be dismayed or pleased that we’re in the ‘blackout period’. As far as the pre FOMC meeting ‘blackout period’ goes, this next note may be of some use,

Wells Fargo: July Flashlight for the FOMC Blackout Period

The FOMC kept the fed funds rate unchanged in June, but the post-meeting statement said that the Committee would take into account "economic and financial developments" when "determining the extent to which additional policy firming may be appropriate."

In our view, recent "economic and financial developments" will lead the FOMC to raise its target range for the federal funds rate by 25 bps on July 26.

For starters, the employment reports for May and June, which were released since the FOMC last raised rates on May 3, showed that while job growth is slowing, the labor market remains tight and is helping to keep inflation above the Committee's 2% target.

Inflation slowed in June, including the smallest monthly gain in the core CPI since 2021. However, with price growth running well-above target for about two years now, we believe participants will want to be more confident that inflation is on a sustainable downward path before ending the FOMC's tightening cycle.

Furthermore, written and verbal communication by Fed officials since the last FOMC meeting suggest that further tightening likely lies in store. The "dot plot" that was released after the June 14 meeting showed that most members believed that further tightening would be appropriate by the end of this year, and Fed officials have generally sounded hawkish in recent public comments.

The FOMC could conceivably refrain from hiking its target range by 25 bps on July 26, but we do not believe a consensus currently exists among Committee members for another hold next week. A far more likely way to reach consensus, in our view, would be via a 25 bps rate hike with indications in the post-meeting statement that the FOMC is prepared to hike further, if "economic and financial developments" warrant.

We do not expect the FOMC to make any technical tweaks to the interest rate it pays on reserve balances that banks hold at the central bank, nor to its repo and reverse repo rates.

One of many key inputs for the Fed will be the HOUSING market and on that topic, a couple notes.

First up on housing and growth,

Goldilocks: Has Growth Picked Back Up?

■ In early March, we highlighted the risk that economic growth could improve in 2023 because of fading headwinds from monetary and fiscal policy tightening, strong consumer income growth, and a possible bottom in the housing and manufacturing sectors. While the spring bank failures seemed to reduce the odds of this outcome, our review of official and alternative data suggests that this growth rebound may have happened anyway. If so, the strong growth momentum to start the third quarter will help offset the mounting drag from reduced bank lending, which is now apparent in the H.8 data.

■ Official data indicate that domestic demand growth picked up sharply to +3.5% annualized in Q1—and with two months of data in hand—is tracking at +2.6% for Q2. We are also tracking GDP growth at +2.2% annualized in the first half of the year, slightly above potential.

■ High-frequency data from alternative sources is also upbeat. We seasonally adjust weekly credit card spending, housing demand, and industrial freight indicators through early July, finding that consumer spending continues to grow, manufacturing activity is currently bottoming or rebounding, and the large declines in housing activity appear mostly behind us.

■ Fiserv credit card data and the Affinity Solutions spending panel suggest a pickup in consumption growth in June and early July—even before the record Amazon Prime Day

■ In the manufacturing sector, industrial rail volumes, container exports, and steel production have all rebounded by a few percent since the spring. Additionally, our East Asia economists now expect an export rebound in that region, and Korea goods exports have already increased two months in a row despite continued weakness in the Chinese economy.

■ Finally on housing, Redfin pending homes sales and MBA purchase application are edging lower but are no longer plummeting, and residential investment GDP appears to be bottoming out thanks to still-elevated construction backlogs.

Oh, Ok … all is well, past year of hikes have had their impact — NO LAG — and there’s basically nothing but runway, blue sky and rainbows ahead!

For somewhat deeper dive on housing,

MS Insight: Global Economics & Equity Research: Navigating a Different Housing Cycle

Cyclical housing headwinds are significant but approaching a peak globally. Sequencing and sensitivity across economies is the immediate focus, but structural shifts in affordability, supply, and mortgages will have profound implications for the next housing cycle — and its consequences for growth, policy, and markets. We highlight key opportunities and risks.

Peak headwinds approaching for an important asset class... Residential housing is the world's largest asset class, a key channel of monetary policy and an important driver of the economic cycle. After several years of historic volatility, we think an expected peak in policy rates for DM economies through 2H23 marks the start of an important inflection point, with some green shoots already emerging.

...but the structural backdrop has changed significantly: 1) Higher rates and resilient house prices have driven a sharp deterioration in affordability in most markets. 2) Housing is now undersupplied in most economies, and this will worsen near-term as construction slows and population growth reaccelerates. 3) While lengthening duration of mortgages in several economies has lowered policy rate sensitivity, it also reduces turnover because the gap between new and existing mortgage rates are considerable.

Mind the gap — focus on sequencing and sensitivity… Expect the housing recovery to be volume-led but price-constrained…

For equities, we think now is the time to focus on housing opportunities (and risks). Wider dispersion across economies and relative to historical outcomes, increases the importance of picking trends across stocks, sectors and geographies. The unique cycle means it is harder to estimate what is in the price. A housing recovery that is driven by activity more than prices suggests a more favorable outlook for activity-linked sectors (Homebuilders, Developers) over price-exposed (Banks, REITs).

Watching ESG and government policy response: Housing policy focus is increasing, particularly through an ESG lens. Social concerns around affordability are likely to skew government policy toward supply-supporting measures, while an environmental focus could drive higher costs structurally.

With the housing cycle — different or NOT — and the Fed, inflation and THE DOLLAR all top of mind, who better to turn to than none other than recently displaced Zoltan Poszar who’s now got his very own shop. This was discussed on a recent Bloomberg podcast, linked / detailed and describe a bit here

ZH: Zoltan Poszar On The Global Financial System's "Monetary Divorce" From Dollar Hegemony

For the past decade, Zoltan Poszar has arguably been the world's foremost expert in the ugly nuances and arcanery in world money-markets (and more recently, on how the financial and physical markets overlap on the geopolitical chessboard). However, amid all the chaos at Credit Suisse, the erstwhile expert on all things 'pipes' in the global funding markets has decided to go out on his own.

The name of his new firm is Ex Uno Plures, "and I will be providing research to institutional investors and consult institutional investors about the plumbing," Poszar explains at the start of this discussion with Bloomberg's Odd Lots podcast.

The former Credit Suisse man expounds on the concept of "Bretton Woods III" and the changing dynamics in the global economy, explaining that the traditional idea of a unipolar world dominated by the US dollar is shifting, and we are entering an era where multiple currencies will play a significant role. Simply put, he notes, the global financial system is going through a "monetary divorce" from US dollar hegemony and becoming more multi-polar.

"You know, these topics: de-dollarization, the re-monetization of gold, using central bank digital currencies to build out, to knit out a de novo financial system, you know, the petroyuan and the renminbi invoicing of commodities and traded goods going forward."

Zoltan highlights the growing focus in the West on reducing dependence on Chinese supply chains and becoming more self-sufficient in key areas.

On the other hand, in the East, there is a focus on extracting themselves from the Western financial system and de-risking their relationship with the US dollar and Western financial institutions.

"If you go into a world where trade is not dominantly invoiced in dollars... it's no longer a machinery where the dollars are getting created on the margin, the dollars are getting accumulated on the margin. And the question is how do you recycle the earned dollars back into funding and rates market?"

He mentions that there have been developments indicating a move away from the US dollar as the dominant currency, such as the renminbi (Chinese currency) being used for invoicing commodities and the increasing use of central bank digital currencies (CBDCs).

"We are starting to see evidence that more and more commodity trades are being settled in renminbi... you can have a lot of ground that renminbi could gain."

Zoltan suggests that CBDCs could create a new network of correspondent central banks, facilitating direct settlement of international transactions between central banks rather than relying on correspondent banks.

By establishing this state-to-state and central bank-to-central bank network, independent of Western financial centers and the dollar, Zoltan believes it could provide an alternative to the current dollar-based system.

"The underlying issue here is very much one where if you look at this unipolar world... you should be imagining correspondent central banks."

Regarding the role of CBDCs, Zoltan suggests that they can be a part of RMB internationalization. CBDCs can help raise offshore RMB and tap swap lines with the People's Bank of China (PBOC). He highlights the overlap between countries planning or piloting CBDCs and the network of swap lines with the PBOC. Zoltan notes that evidence shows an increasing number of commodity trades being settled in renminbi, and the share of renminbi in trade finance has been growing, indicating a potential gain in the currency's importance in the coming years.

"Gold is definitely something that's coming back as a theme... we are seeing this more and more in the data that especially the countries that are not geopolitically aligned to the US are shunning Treasuries and shunning the dollar and they are buying gold instead."

He also emphasizes the need to rethink the role of central banks as dealers of last resort in the foreign exchange (FX) market, particularly for the global East and South, in the context of CBDCs and the correspondent central bank system.

Zoltan believes that the evolving dynamics of global trade and the emergence of multiple currency options for payment will have significant implications for dollar funding and rates markets. He mentions that if countries have the option to pay for commodities in different currencies such as dollars, renminbi, or gold, it could reshape the FX swap market and the demand for dollars. The accumulation of dollar reserves by countries, such as China, may also be affected if they can use their own currency for commodity imports, reducing the need for large dollar reserves.

"You can pay dollars for oil, but you can also pay renminbi for oil. But if you are a gold miner, you can also pay for oil with gold... You would just choose whichever one is cheaper."

Shifting his focus from global to local, the money-market-mage mentions mentions that the solutions crafted by the Fed to address liquidity problems, such as the Bank Term Funding Program (BTFP), were powerful and surprising. He acknowledges that the BTFP program received mixed responses, with some seeing it as the right move within the framework of Basel III regulations, while others criticized it for potentially undermining the need for interest rate risk management in banks' portfolios. Nevertheless, Zoltan believes that the BTFP is now a part of the system and will likely remain as a standard feature.

He highlights the importance of the BTFP in supporting the Treasury market by preventing banks from liquidating underwater bonds and potentially causing further strain in the market. The program provides a mechanism for banks to access liquidity without disrupting the market and serves as part of the scaffolding of the financial system.

He points out that while blanket deposit insurance may not be implemented, the Federal Deposit Insurance Corporation (FDIC) acts as a buffer between the troubled institution and the Federal Reserve, ensuring that the Fed's lending is secured to its satisfaction.

Zoltan explains that the banking system will likely deal with problems on a case-by-case basis. While there may be challenges in credit portfolios and commercial real estate lending books, as well as potential consolidation across the banking system, there are levers that the Fed can pull to help resolve issues. He notes that interest on reserves provides banks with a steady stream of interest income, which can indirectly help pre-fill their capital base.

Zoltan also mentions the role of larger institutions like JPMorgan and the potential for banks like Wells Fargo, which still have unused balance sheet capacity, to assist in cleaning up issues if needed. He emphasizes that while there may be micro-dislocations and challenges in specific areas, the overall banking system is fine, and the key is to anticipate and position appropriately.

"I think the banking system is fine for now... There will be consolidation across the banking system. But there are many levers that the Fed pull to help clean things up."

Regarding shadow banking, Poszar explains that if his thesis about world trade invoicing in currencies other than the dollar comes true, it could provide balance sheet relief for global systemically important banks (GSIBs). The shift of market making and FX functions to the balance sheets of central banks and the migration from correspondent banks to correspondent central banks would potentially benefit US banks, allowing them to use their balance sheets for other purposes.

"Regarding that shadow banking question... I think over time that's going to provide balance sheet relief to all the GSIBs because FX market making, credit lines exclusively provided in US dollars... that's the bread-and-butter domain of JP Morgan, Bank of America, and Citibank."

He suggests that as the shadow banking system deals with credit and real estate problems, the banking system could become a source of strength, providing both capital and balance sheet capacity.

"It's better to suffer those losses in non-banks than banks because banking crises are very nasty things."

Zoltan concludes by noting that the concept of shadow banking has evolved, and he focuses on the new frontier of traditional financial functions migrating to the balance sheets of central banks, central bank digital currencies (CBDCs), and different currencies. He believes this shift will drive rates and funding markets in the future and intends to focus on mapping and understanding this new shadow banking terrain.

Finally, Poszar highlights the fact that "in the IMF data and in the data of the Gold Council, we see this massive increase in foreign central banks' purchases of gold."

"That gold aspect definitely survives... You basically have gained sovereignty from a monetary perspective... So again, you will not have to run with as much FX reserves...

...I think that gold aspect definitely survives... I think the commodity shortage and this... I think it's definitely there in gold."

* * *

Listen to the full podcast below:

Zoltan reveals his next move — 2:06

The meaning of Ex Uno Plures — 2:31

Is the Bretton Woods III thesis playing out? Plus a new angle on CBDCs— 5:19

Are big macro stories actionable for investors? — 15:26

Changes in structural demand for US Treasuries — 24:13

The role of commodities financing in Bretton Woods III — 27:21

Thoughts on the recent banking drama — 33:36 Strength of the banking system now — 39:51

CBDCs and central banks a the new shadow banks — 44:02

From one brief podcasted interlude to another and this next interlude is for those inner stock jockeys in every bond guy / gal (note commentary on BONDS with regards to the flows…which caught MY attention)

Retail is back, buying stock calls and equity MFs. Upside chase by MFs is in full swing, with continued rotation into Tech at the expense of Financials. But, HFs have turned cautious, with room to add if earnings give credence to soft landing. Systematic US equity exposure in CTAs, Vol Target and Risk Parity remains high.

… Outside of equities, bonds and USD assets remain in favor. Demand for long duration assets from asset managers continued last month as the recent pace of disinflation boosts market confidence that the Fed is near the end of its hiking cycle. We see potential signs of a bottoming out in USD speculative futures as US growth has remained resilient despite macro weakness in RoW, particularly China and Europe. The significantly low USD positioning provides more room for USD strength into 2024 as the US Tech sector asserts its dominance in the AI stack.

… Despite the latest buying spree in equities, flows are still mostly directed to bonds and money market, with long-duration and high quality assets in greater demand. The regional banking crisis was a key catalyst for flows this year, triggering an exodus of cash from bank deposits into money market funds as well as a rotation towards safer assets: away from equities into bonds. The rotation is such that the inflows US equities saw during the 2020-21 bull market have now completely reversed, leaving more room for the equity inflows to continue into year end.

… Bonds still preferred by Retail As the market narrative shifts from inflation to recession, demand for longer duration and higher quality assets has remained strong among retail investors. Retail buyers continue to flock to US Govt bond funds and higher quality investment grade assets. Outflows from High Yield bond funds have continued this year, albeit at a slower pace.

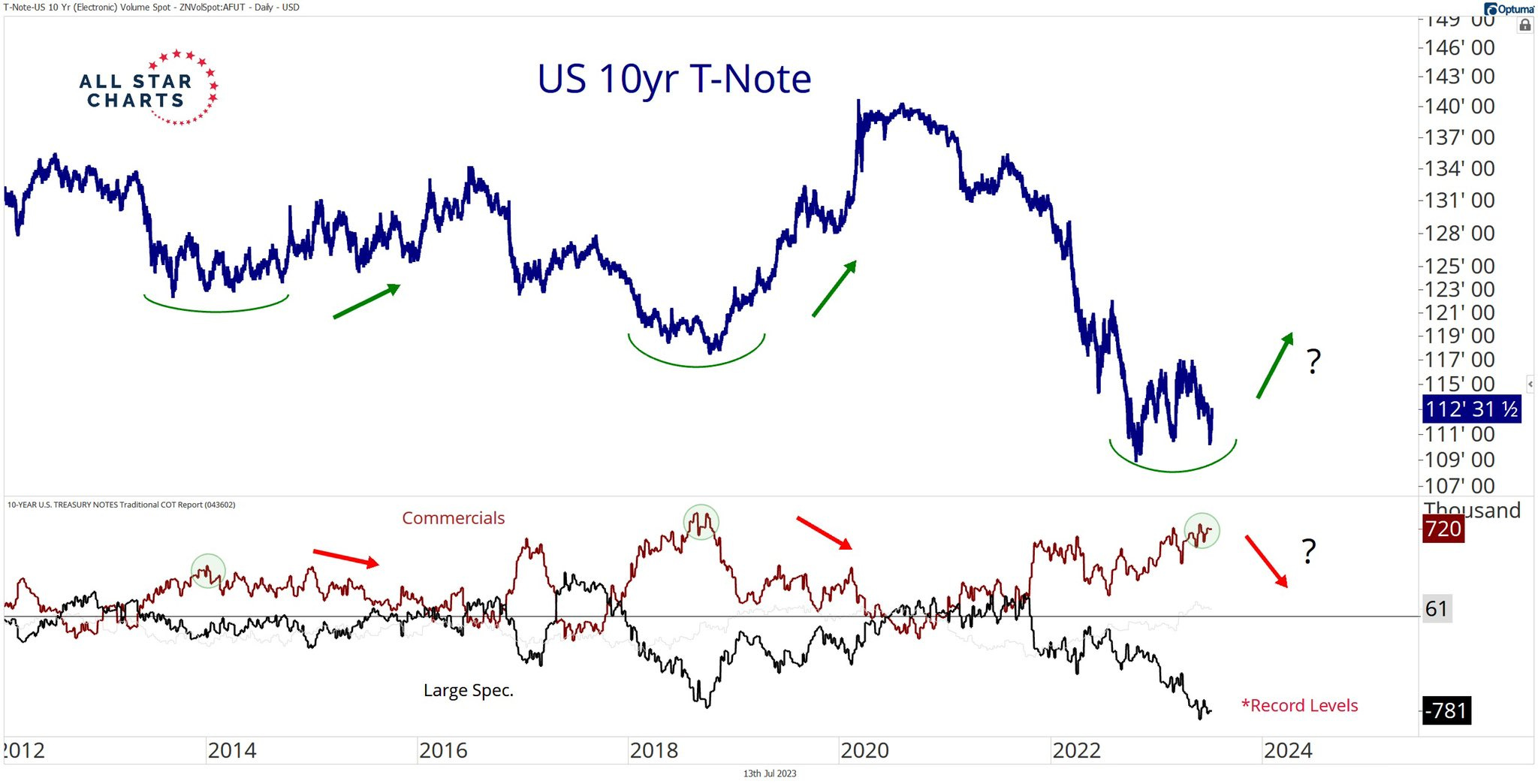

What’s this all add up to? The END of the bond bull market, right? Of course … always and forever one must hate bonds, they do NOT sell and stocks are sexy …

It’s hard for me to have a conversation about the stock market without bringing up what’s happening in bonds.

Think about it like this, the market cap of all US Stocks is somewhere around $40 Trillion. For the bond market it’s over $120 Trillion.

Volatility in bonds tends to trickle down to other asset classes, especially stocks.

US Stocks really got going in the 4th quarter last year, once the US 10-year Note stopped falling in price.

I don’t believe that was a coincidence.

But at this point, Large Speculators have on their most aggressive short position in bonds ever.

So in other words, what is historically the “dumb money”, particularly at turning points, are betting more aggressively than ever that bond prices are going to fall and rates will now continue higher:

This has me wondering.

What if this is NOT the end of the 40-year bond bull market, like the “dumb money” is currently betting?

What happens if it’s the opposite, like it usually is when they act this way?

What if it’s bonds that are about to rise off these lows, and it’s the interest rates that are about to fall apart?

What then?

How are stocks going to react to increased bond volatility?

Why would interest rates fall apart? What would the bond market be pricing in for stocks, that rates would need to come down so much?

That’s what’s on my mind and what I’ll be paying close attention to this week.

Last week some of our upside targets were hit in equities, and we took profits accordingly.

We also started to initiate some short positions…

Bonds being for losers, aside, I’ll end with a note from Fred

FRED: Are real gasoline prices really higher? : Data from 900 gas stations for FRED Blog’s 900th post

The FRED Blog is proud to have reached the milestone of 900 blog posts. As with every centennial, we present a graph that’s related to the number. Although 900 was challenging, FRED always delivers.

Today’s topic is gasoline, and the data set comes from a survey of 900 retailers. The values reflect the average prices of “regular” gasoline, with octane levels of 85 to 88. The FRED graph above offers some not-so-surprising observations: Gas prices fluctuate dramatically, and gas prices have increased substantially since the 1990s, peaking in mid 2022.

Adjusting for consumer price inflation, as we do in our second graph, shows the same variability but reveals something new: After the increase in the early 2000s, the real gas price has not been trending up and the 2022 peak in the first graph is surpassed on several occasions. But, of course, what really matters is how gas prices relate to incomes, which we show in our third graph. There, we see that current gas prices (measured as the number of minutes of work it takes to purchase a gallon of gasoline) are not that much higher than in the 1990s.

This IS good news and perhaps a way of looking at prices at the pump from a lense of affordability, the way in which we often consider housing.

And while the Fed and policy makers in DC may just be thrilled to hear / see things in this light, it is also reflected in other ways.

The Animal Spirits Index (ASI) jumped to 0.28 in June, up from -0.19 in May. The positive outturn broke a 17-month streak of negative values.

All five components of the ASI increased in June.

The ASI's break into positive territory aligns with better-than-expected economic data over the past few months.

… All five components of the ASI increased in June. The S&P 500 gained roughly 270 points during the month and closed out a four-month streak of gains. Stock market volatility also eased in June, evidenced by the VIX Index falling four points. In the bond market, the yield spread on the 10-year and 3-month Treasuries unwound some of its deep inversion, rising to -141 bps in June from -156 bps the prior month.

… The ASI's break into positive territory aligns with better-than-expected economic data over the past few months. As outlined in our latest U.S. Economic Outlook, the U.S. economy has shown incredible resilience to the Federal Reserve's aggressive monetary policy tightening. Interest-rate sensitive sectors, such as housing and construction, have seen activity stabilize, while the labor market is only slowly cooling off. While we have seen stronger-than-expected data, the latest readings on employment and consumer spending suggest momentum is fading. We look for hiring to continue to slow in the coming months alongside softer wage growth. The weaker labor market will pressure consumer spending, and we expect real personal consumption expenditures to contract over the first half of 2024. The pullback is set to weigh on confidence later this year and early next, creating scope for the ASI to return to the red. Stay tuned.

… THAT is all for now (and for several days … Off to the day job, back in about a week!