weekly observations (7/17); bullish seasonals and a lesson from history, "Inflating Away the Debt: The Debt-Inflation Channel of German Hyperinflation" (via FRBNY...)

Good morning / afternoon / evening (please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

LAST weekend I began with a question (#Got5s?) … The belly WAS oversold and remains quite topical as we exit the week just past. SOME of the brightest bulbs and sharpest tools in the shed are asserting we may have just witnessed THE inflection point.

We’ve now reached THAT point of the programming when the yield curve will start bullishly steepening. This is what THEY — the best in the business (and don’t forget — as if anyone might let you — II voting is now open again) suggesting of that trade of the year — cyclical resteepening — and the time is NOW …

BMOs Macro Horizons latest episode is “Better Lagged Than Never” (Google link but I’m sure it exists everywhere) and just one example of how I began MY weekend…

My boring existence aside and without further delay, on TO some weekly NARRATIVES where I’d note a few which caught MY EYES,

BAML: US 2Y yield may be forming a double top BCA: Top Trades for H2, 2023 #3: Buy Long-Maturity Treasuries BMO: Summer of Bonds BNP: … US rates to bull steepen through H2 2023 … Citi: Is another bond sell-off coming? GMOs: SLOW BURN MINSKY MOMENTS (and what to do about them) JPM: Have you missed the market rally? MS: Buy Any Dip in Bonds

Most of these you’ll note are more bond friendly (ie BULLISH) than not. The standout IS Citi and so, an excerpt which caught my eye from the weekly note

… There is, however, one major risk to the bullish picture for Treasuries - the beginnings of a bubble formation in tech stocks, driven in large part by the AI frenzy. As our GAA team has written recently (see Global Asset Allocation - Between the soft [survey data] and a hard place: No sign of a downturn in resilient US economy), a bubble in tech stocks can have a duration of as much as ten months or more. The recent bubble in crypto for example took 12 months from Oct 2020 to peak in Nov 2021, before bursting. With the tech stocks frenzy starting in March or May (the determination is subjective), i.e. only two to four months ago, there is plenty of time for the bubble to inflate further, also going by experience from the dot-com bubble period. Back then, the bubble period was Nov-1998 to Apr-2001, i.e. about 30 months for a full round trip in the NDX, 16 months to the top, followed by 13 months to the bottom after the bubble peaked in March 2000. In that period, bond yields rose, as investors shrugged off the safety of Treasuries for the allure of higher returns in internet stocks and tech stocks broadly (see Figure 10). We think there is a strong likelihood of a similar dynamic happening again, especially as momentum strategies chase tech stocks higher. Eventually, the bubble would of course burst, and the ensuing collateral damage will bring bond yields lower – we just don’t know the timing of that yet. Meanwhile, in the quiet summer months, the bubble can grow.

That’s interesting … it is ALSO followed by note on BULLISH summer seasonality. That excerpt concludes,

… Focusing on years when the Fed was hiking, rallies tend to be larger in the second half of July. For the 10y sector, our data shows that a rally in the first half of July was followed by rally in the second half of the month 75% of the time. Based on history, we are likely to be entering a bullish period for 10y rates over the next two weeks.

SO in other words, even bond bears cannot be too terribly bearish?

Meanwhile, still waiting for Lacy Hunt / HIMCO Q2 be like,

First up with all the bullishness of RATES in mind I thought a look at POSITIONS worth a moment …

Hedgopia: CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

NET SHORTS DOWN TO 3m low … NOTED.

Moving on to reason for all this position jockeying presumably idea Fed may be DONE because, you know, DISINFLATION, right? This is precisely why this next note caught my eye,

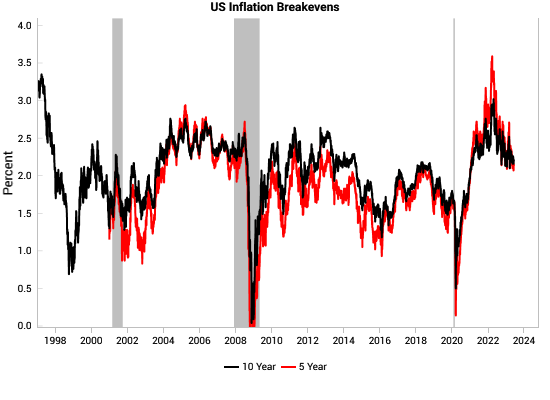

We like allocating towards TIPS at prevailing real yields. Given our structural Age of Scarcity thesis, we suspect a regime shift in the coming years where inflation realizes more than breakevens.

… The TIPS market has only existed since 1997 during a disinflationary era. We are skeptical about extrapolating previous TIPS experiences into the future. The era of financial repression and fiscal and monetary policy coordination suggests inflation risks are biased to the upside when 5 year inflation breakevens are back down to 2.15% and 10 year inflation breakevens are back to 2.20%.

… We acknowledge that TIPS are prone to trading liquidity issues in times of stress, e.g. in March 2020 and through 2008. In the context of our broader asset allocation positioning (link) we rely on nominal Treasuries for upside as a recession scare gets priced in, and would look to sell and deploy excess cash into capital-scarce risk assets. We would look to hold onto TIPS through a downturn (and ride through trading liquidity issues) into the next cycle where inflation settles at a high level.

Perhaps a note worth noodling over and at same time, a bit of a focus on NOMINALS via Bloomberg,

ZH: Bonds Might Look Appealing, But Only For Now Authored by Simon White, Bloomberg macro strategist,

US bonds are rallying with core inflation that shows clear signs of decelerating. That is likely to continue in the medium term, but the longer-term picture is one of rising yields in the context of historically elevated inflation.

After touching a high of 4.09% in recent days, the 10-year yield is lower by over 20 bps, at around 3.82%. The trigger was Wednesday’s core CPI, which came in lower than expected. That trend should continue over the next three-six months.

Inflation leading indicators continue to point downwards, showing headline inflation should keep falling for now. Fixing swaps also anticipate a continued steady drop in headline over the next six-nine months.

Core’s fall is now being driven by the shelter component - accounting for a significant ~43% of the core basket - and that should also keep declining as rental vacancy rates rise.

Now that it is clear core as well as headline inflation’s downwards momentum is rising, the Federal Reserve can afford to take its foot off the brake, as falling inflation naturally tightens real rates (a July hike looks baked in, but it’s probably only necessary now so as not to upset forward-rate pricing).

This is a global phenomenon. Expectations are central banks will become less hawkish, leading to the Advanced Global Financial Tightness Indicator rising, i.e. financial conditions are becoming less tight – and this points to lower US 10-year yields.

But this should be viewed as a trade, not an investment. Inflation is likely to re-accelerate again.

The US

labor market is structurally very tight, higher profit margins are becoming entrenched and, sooner more likely than later, easing in China will break through.

The bulk of disinflation seen thus far has been driven by China. But we are nearing the limits of what the nation can tolerate in terms of tepid growth and rising unemployment. The turn in China would mean a re-acceleration in global inflation as soon as year-end.

Term premium has been remarkably subdued in this cycle despite near double-digit price growth. But a volte-face in inflation right at the moment most think it’s been pacified would likely lead to a structural rise in longer-term yields as holders demand extra compensation. You don’t want to get caught on the wrong side of that.

ONLY FOR NOW … as in next couple / few SEASONALLY GOOD weeks?

One last LINK from the intertubes which hit inboxes on Thursday … When the FRBNY and folks down on Liberty Street think like this, out loud, I am guessing we should be paying attention … in the case there are any subliminal messages as to how fiscal and monetary policy are working in concert …?

… Wrapping Up By exploiting a newly digitized firm-level database, our research provides empirical evidence supporting the relevance of the debt-inflation channel in the transmission of unexpected inflation to the real economy. What are the broader implications of these findings? Can the debt-inflation channel be operative during times of moderate inflation?

The relevance of the debt-inflation channel depends on the structure of debt contracts. In cases where debt contracts are nominal, long-term, and denominated in domestic currency, the debt-inflation channel may be relevant even during more moderate bouts of inflation. The debt-inflation channel may also operate through households, especially in a context of fixed-rate, long-term mortgage debt, as suggested in existing academic work such as Doepke and Schneider (2006). At the same time, for firms with floating-rate or foreign-currency debt, inflation may have neutral or even negative effects on heavily leveraged firms.

Other factors can also counteract the expansionary effects of the debt-inflation channel. One example is if monetary policy responds to rising inflation by increasing interest rates and tightening financial conditions. Another potentially important offsetting effect comes from the losers of the debt-inflation channel: creditors. An increase in inflation can erode bank equity and contribute to credit contraction that offsets the expansionary effect from reducing borrower debt burdens.

Hmmm … Okie dokie.

AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

AND … in case you may have any questions in your mind at all, some clarification,

Before hitting SEND just a NOTE — first I’d like to express a degree ]of gratitude for all readers (casual and those interactive, pledging support) past, present and future.

I’ll be posting much lighter in the days just ahead as some changes here in big picture LIFE stuff occurring. We’re celebrating BIG birthdays, traveling some AND visiting ‘Thing 1’ soon after he spreads his wings and goes WEST to begin his post university life and career.

So much to be grateful for and your patience over the next couple / few weeks is included!

AND … THAT is all for now. Enjoy whatever is left of YOUR weekend …

I've just returned from 2 wks in the woods and mtns myself go have yourself some fun while it's summer!