HEREis a link thru to what some of the best and brightest minds on The Street are saying and thinking. The Fed is NOT having an emergency meeting Monday but rather a well-advertised DISCOUNT RATE meeting. Listen to Ian & Co of BMO for more in his weekly, Don’t Jimmy Me, Jimmy.

Meanwhile, the sellsideis attempting to guess how many hikes in 2022 and I think they’d have better luck guessing the number of jelly beans in a jar.

A large Canadian bank closed 2s3s steepener and has entered 2s5s tactical steepener and the shop who’s often leaned on 2s5s as the BIBLE have a few choice words (and charts),

… Our Financial Bible (2’s 5’s curve) suggests we are heading into the twilight zone

The chart now appears to be heading towards the “Twilight zone”

You’ll FINDany number of HIGHER RATE CALLS along with hike / QT guesses and if thats your thing, well, enjoy.

The past weeks CPI and BULLard commentary combined for a wild rollercoasters and a 30bps candle, and the moves have been detailed by many far more qualified and able than I. Bloomberg’s Tracy Alloway with a nifty lookin’ chart,

… The bond market used to be a lot more lively before 2009,when the Federal Reserve began expanding its quantitative easing program. Things got even sleepier after it unveiled more emergency measures in March of 2020, during the worst of the Covid-19 pandemic.

After the great financial crisis, central banks basically anchored short-term rates at zero to create an era of relative quiet in fixed income. And while it’s always hard to call major turning points in the market, it feels like Thursday’s abrupt volatility could mark the start of something new …

30bps candle with some context … for even MORE context, ZH with DB charts,

Nothing without consequence, Jimmy … So as we’re clear … MY current (uneducated and not nearly as important as anyone elses) GUESS as to how many hikes from the Fed in 2022 is now going to be 11 (as noted Friday morning HERE), which, IF CORRECT, would put ‘terminal’ FF level at approx 2.75% (11x25bps). AND as a bonus, I believe that would put me currently in the lead?

Clearly I’m joking BUT my PERSONAL view remains that if even REMOTELY correct or, in some FRACTIONAL way, this amount of taper/tightening is forced upon markets in efforts to break back of the CURRENT ‘flation, the yield curve will CONTINUE to flatten — INVERTING already in some cases (7s10s) — and so, yes, I’ll say it, we’re gong to be talking of it as a sign a recession is coming.

(Barclays) Forecast Update - We expect 10y yields to end the year at 1.9% (versus our previous target of 1.75%), which is roughly 25bp below forwards. Our forecast incorporates the view that the expectations component in 10y yields is likely to remain low to reflect subdued nominal neutral rates and the term premium somewhat negative to reflect Fed’s credibility and the role of USTs as a safe asset … …In light of downside surprises on the fiscal front and the tightening of financial conditions so far, we believe investors are being too optimistic about growth prospects later this year and next; a recalibration should cap long-term rates …

An example from Goldilocks of what 100bps may do,

JEFF’s

Assessing The "Damage" Of 7+ Hikes … Our own inclination is that the post-pandemic economy will be less rate sensitive compared to the last decade. The cash-rich households and businesses have plenty of spending capacity and are thus not as reliant on credit growth as they have been in the past. Debt service ratios are also extremely low, i.e. there's a lot of space to absorb higher interest rates before credit quality comes into question. Inflation is helping as well, by boosting both household income and corporate revenues, and thus reducing the burden of paying off "old" debt. For all these reasons, we expect this to be a sustained tightening cycle which ends with a higher terminal rate than the last one.

And more. Much, much more. Consider it something to get you from here / now up until pre-game coverage which starts in just a couple/few hours.

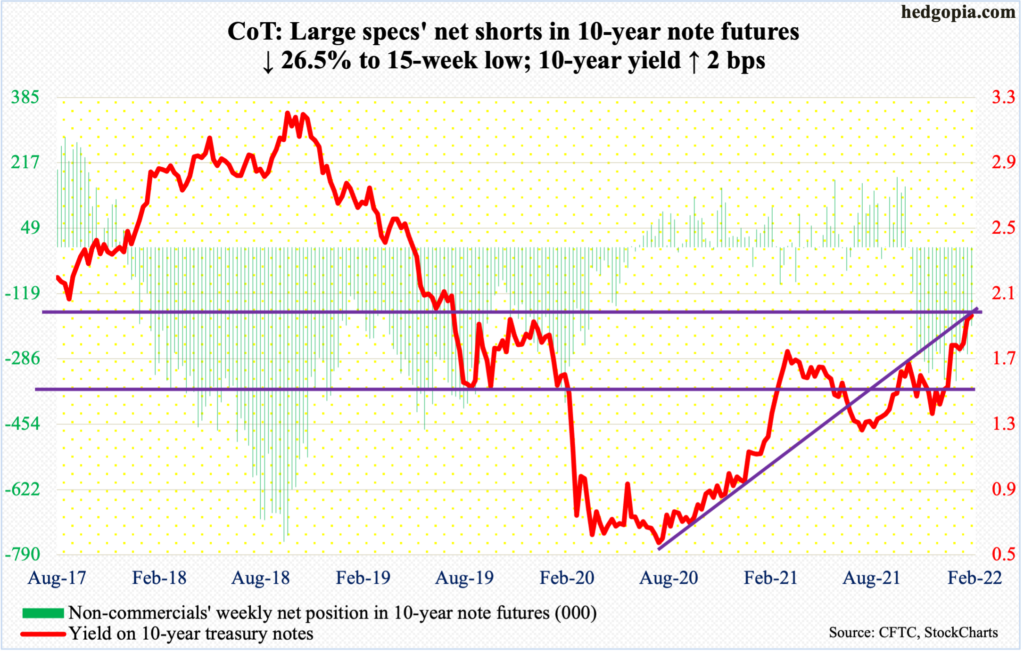

In as far as POSITIONS — pre CPI and BULLard — goes, a couple of useful links,

InvestMacro: COT Bonds Speculators drop 10-Year Treasury bearish bets to 15-week low

In life there are few if any things without consequence. The current administrations posture towards fossil fuels having a great deal of added upwards pressure on gas at the pump which is impacting us all. That Hunter is one of, if not THE most protected people on the planet, may also be impacting (clouding) judgements and commitments being made on ALL our behalf. Rather than diver deeper into politics of it all, well, I’ll quit while I’m behind and let the Sunday talk shows have at it. Or not.

Enjoy the rest of the weekend and the game(s) … bracing for a bit more snow tomorrow after enjoying some warmer weather and celebrating Thing 3s (far right) birthday earlier today at a local ‘escape room’ (was either that or the hatchet throwing place — maybe next time!) …

I can confirm ALL the signage are about as accurate a description of a bunch of 7th graders as there ever was. But nobody got hurt and lots of laughs had by all!

{kind=link}

{kind=link}