Good morning … Rates are aggressively UNCHANGED this morning on heels of what has been an historic start to the year (best since 2001). Along with FOMC MINS (more below), Ka$hkari (voter now) wrote in a blog post on,

“it will be appropriate to continue to raise rates at least at the next few meetings until we are confident inflation has peaked… Once we see the full effects of the tightened policy, we can then assess whether we need to go higher or simply remain at that peak level for longer.”

And now for something completely different. A few links / updates from ZH. A daily recap including FOMC mins (and pricing)

ZH: Fed Admits Recession Is "Plausible", Pushes Back Against "Unwarranted" Easing Expectations

On DATA

ZH: ISM Manufacturing Contracts For 2nd Month, Prices Paid & New Orders Plunge

Complimented by some GOOD (?) news,

ZH: Job Openings Come In Much Hotter Than Expected Despite Continued Deterioration In Hiring

Never mind … here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly lower with the curve flattening beyond the 3yr point as markets further digest yesterday's FOMC Minutes amid heavy EGB issuance today (Portugal, France and Ireland). DXY is little changed while front WTI futures are higher (+2.2%) for a change. Asian stocks were mostly higher, EU and UK share markets are mixed and little changed while ES futures are a touch (+0.1%) higher here at 6:50am. Our overnight US rates flows saw Treasuries trade 'heavy' during Asian hours with flows skewed toward better selling of intermediates by fast$ names amid light news flow. Overnight Treasury volume was ~105% of average overall with relatively elevated turnover seen in 5yrs (145%).

… and for some MORE of the news you can use » IGMs Press Picks for today (5 JAN) to help weed thru the noise (some of which can be found over here at Finviz).

Now with some of the news you can use in mind lets turn TO Global Wall St narrative creation machine and a couple things which caught MY eyes … First a few comments on the Fed’s minutes

BMO

As Hawkish As Expected... TSY off the highs … "Participants noted that, because monetary policy worked importantly through financial markets, an unwarranted easing in financial conditions, especially if driven by a misperception by the public of the Committee's reaction function, would complicate the Committee's effort to restore price stability." If anything, this puts a higher terminal rate on the radar -- at least on the margin…

Paul Donovan / UBS highlighting,

Another failure of the Fed? The minutes of the Federal Reserve struck a hawkish tone, with lots of protestations about rates staying high until inflation convincingly declined. There are two reasons the Fed may fail to convince markets. First, since the June 2022 policy errors, there is little reason for investors to trust what the Fed says it will do with policy. Second, investors see reasons why inflation will convincingly decline. Profit-driven inflation is less sticky than wage-driven inflation, as the record breaking durable goods price disinflation has shown….

Barclays

Worries about misperception The December minutes reveal FOMC concerns about labor market tightness, its impact on core services inflation, and some frustration with the easing in financial conditions, which might be related to misperceptions of its reaction function.

MS

Not Tight Enough Financial conditions are too easy, reflecting a misperception among investors of the Fed's reaction function. Policymakers want to err on the side of being too restrictive. As long as financial conditions are misaligned with the Fed's goals, expect additional tightening…

… Between what appeared to be a quite hawkish overall outcome from the December FOMC,as well as the minutes that clarified and reinforced that message, our FCI has marginally retraced tighter - on net tightening about 21bp in fed funds equivalent (Exhibit 1). Ultimately, thee asingin FCI since November is "unwarranted" and complicates the "Committee's effort to restore price stability".

Goldilocks

December FOMC Minutes Stress Data Dependence in Determining the Size of Upcoming Hikes BOTTOM LINE: The December FOMC minutes noted that the committee would “continue to make decisions meeting by meeting,” leaving the FOMC’s options open for the size of rate hikes at coming meetings. We continue to expect the FOMC to slow the hiking pace to 25bp at the February meeting. "No” participants anticipated that it would be appropriate to reduce the funds rate this year. Participants welcomed the recent softening in inflation but stressed that “substantially more evidence” was required. Participants remarked that “activity appeared likely to expand in 2023 at a pace well below its trend growth rate” and that risks to the growth outlook are weighted to the downside.

And in other NOT FOMC MINS news (was there any?), a large German operation attempts to put the curve inversion into some perspective

Money market inversion in perspective At the time of writing, peak pricing has declined around 9-10bps in recent days – we had noted in this FICOTD that the peak in policy rates was short lived, and the market continues to expect an unwind to start in the first half of 2024. Today's FICOTD puts the inversion in the context of peak pricing over a longer period. Here we proxy peak pricing as the peak in first four futures contracts, basis adjusted post GFC. The inversion of the money market curve has occurred sooner than in previous cycles, though as noted in this FICOTD, market pricing has not been a good predictor of realised outcomes, nor has this cycle been similar to previous ones. The latest PMI dataset raises questions around whether the worst is behind us, and if so what that implies in terms of terminal rates and/or how long they might remain at restrictive levels – the latter is also very likely to reflect a drag from the US, which is pricing a substantial degree of easing over 2024.

ING on JOBS report coming tomorrow,

US jobs numbers could soon start to turn Today’s data offers further further evidence that labour demand remains strong despite clear signs of a weakening economy. Labour data is a lagging indicator though and with CEO confidence at the lowest point since the Global Financial Crisis, we expect a more defensive stance of American companies to result in much weaker jobs numbers later in 2023

Somewhat MORE on JOBS — and CLAIMS from Joe Lasagna via John Authers,

… Why else might investors be confident that the Fed has it wrong, and that inflation will soon subside? One interesting point of view comes from Joe Lavorgna, now chief US economist for SMBC Nikko, who points out that although claims for jobless insurance are very low, the most reliable recession indicator historically has been the percentage rise in claims from their cyclical low. And claims are rising. This is Lavorgna’s comment:

Today’s claims are well below where they were prior to the last five (non-pandemic) recessions. However, our work has found that the percentage rise in claims from their cyclical low is more important than the level of claims in foreshadowing a downswing in the labor market. On balance, recessions have begun whenever claims have risen 23% from their cyclical low. We are past that threshold.

Somewhat MORE on TRIMMED MEAN (noted HERE) and ‘UIG’ (underlying inflation gauge)

A stabilizing but still unfriendly trend The latest November PCE price data showed further deceleration and tentative signs that inflationary pressures are abating, though inflation remains at a very elevated level. Updating our suite of statistical models, we find that our underlying inflation measures were steady, hovering above 3.5%. Our monthly mean estimate stayed flat at 3.7% and the median estimate edged up only 4bps to 3.5%. Both measures remain at historically high levels since our gauge began in the early 1990s. These elevated readings of underlying inflation reinforce Fed officials’ messages that there is still a long way to go to be confident inflation is on a path back to 2%.

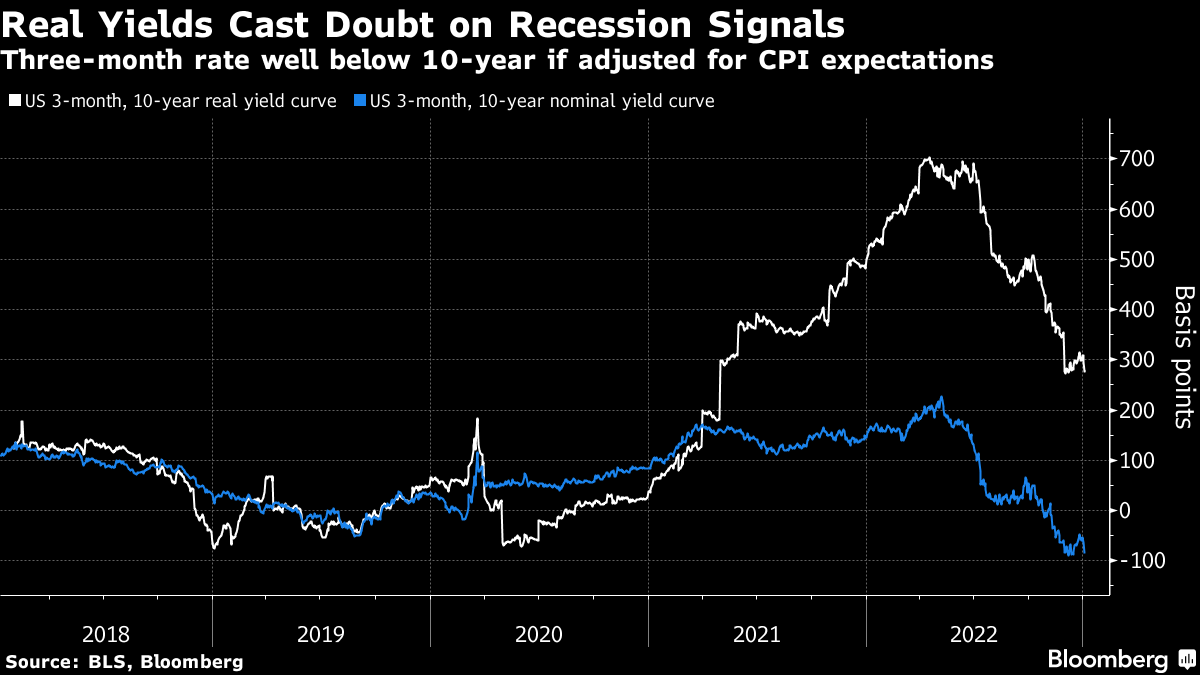

Finally, a couple visuals of 3mo10yr for some context. First from Paul Winghart (HERE)

The spread on the U.S. Treasury 3mo/10yr curve fell back again today and continues its very sharp retrenchment deeper into inverted territory.

Most investors and economists are girding for a US recession, and steep yield-curve inversions have been a key driver of that theme. There are other reasons, too — the scope of the Federal Reserve’s tightening, the fact that inflation rarely slows from elevated levels without a recession, and forecasts for severe slowdowns in Europe and China.

Still, Campbell Harvey, the economist who pioneered the link between inversions and slowdowns, reckons this time maybe we won’t get a US contraction despite the deepest inversion since 2001 in his favored measure — the gap between 10-year and three-month yields. Part of his reasoning is that his model was linked to inflation-adjusted yields, and market expectations for a rapid slowdown in CPI growth boost the odds of avoiding recession. Indeed a gauge of the curve that adjusts yields based on breakeven rates (with the three-month rate derived by cross-referencing current CPI with the one-year breakeven) would seem to show no recession signal at all as that gauge is in the positive. The question then becomes how reliable the market’s forecasts are for annual US CPI to plummet from 7.1% in November to 1.82% a year from now, and whether such a collapse in inflation can happen without a recession.

Campbell Harvey and his much ballyhooed indicator of gloom aside … as football seasons finale coming into focus it is nearly time to focus ON …

What inspired the inclusion of the logorrheic rap? Surely the first and last Top-40 hit that mentions "a bottle of kaopectate." Seems fitting I suppose, since it was the stated intention by the "baby of the bunch" to wiggle my behind, but, then resorting to using "TNT" on the same behind is at cross-purposes with the Kaopectate. Wriggles is soooo confused now.... On the other hand if the "stinky chicken" rap is meant to represent the seething wriggling mass of narratives writhing about in an attempt to make sense of the times back then, just as they are writhing today, then, perhaps I get it, as in, art imitates life while history raps-on but doesn't quite repeat itself and all that stuff. Janus, like so much from the pre-paternal-mono-sky-god days is a 'mother' lode of psychological wisdom, was the first(?) to explicitly recognize our tendency to gravitate towards binary decision points in 'krisis' to such an extent we no longer see beyond the self imposed either-or. Well, that's how I spin it, but either way, size-your-bets to perverse your capital, don't take song lyrics to literally, and you'll still be around to play come the next new year.

What inspired the inclusion of the logorrheic rap? Surely the first and last Top-40 hit that mentions "a bottle of kaopectate." Seems fitting I suppose, since it was the stated intention by the "baby of the bunch" to wiggle my behind, but, then resorting to using "TNT" on the same behind is at cross-purposes with the Kaopectate. Wriggles is soooo confused now.... On the other hand if the "stinky chicken" rap is meant to represent the seething wriggling mass of narratives writhing about in an attempt to make sense of the times back then, just as they are writhing today, then, perhaps I get it, as in, art imitates life while history raps-on but doesn't quite repeat itself and all that stuff. Janus, like so much from the pre-paternal-mono-sky-god days is a 'mother' lode of psychological wisdom, was the first(?) to explicitly recognize our tendency to gravitate towards binary decision points in 'krisis' to such an extent we no longer see beyond the self imposed either-or. Well, that's how I spin it, but either way, size-your-bets to perverse your capital, don't take song lyrics to literally, and you'll still be around to play come the next new year.