Following up an earlier post and thought experiment whereby those who think they can see the future, really cannot (Yogi Berra economics HERE), I stumbled upon this one from 20th December 2021 from the Federal Reserve Bank of St. Louis.

During 2021, the U.S. economy rebounded strongly, but the rise in inflation surprised many.

Headline and core inflation rates for the personal consumption expenditures price index will likely end 2021 at their highest in 30 years or more.

The U.S. is expected to post strong GDP growth in 2022. If higher inflation persists and erodes household purchasing power further, that could put growth at risk.

Those in the public sector put their economic forecasting pants on the same way those in the private sector and, in my view, have NO better chance of predicting the future than anyone else. WHY we then trade / invest / position portfolios around longer-term DOTS PLOTS is beyond me …

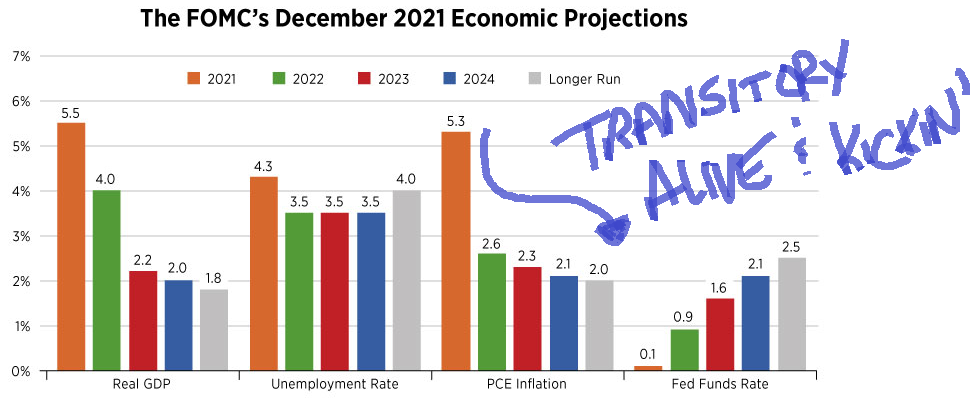

… Most FOMC participants continue to project that 2021 will be the highwater mark for inflation going forward. (See the figure below.) Further improvements in supply chains that enable an increased supply of durable goods, such as new vehicles; vaccines and other therapeutics that spur more workers to rejoin the labor force; and the waning effects of the large monetary and fiscal economic policies implemented in 2020-21—which could slow the demand for goods and services—are some of the key factors that forecasters point to in helping to drive inflation lower over the medium term.

… Strong demand for labor is likely to lower the unemployment rate to around 3% to 3.5% by the end of 2022 and generate continued strong growth in employee compensation. The latter will help mitigate the reduction in purchasing power from higher prices of goods and services. But if the reduction in household purchasing power from higher inflation persists, consumers will either need to reduce real spending or draw down their savings. Either development could pose a threat to consumer spending, and thus real GDP growth.

Not sure what to say other than HOPE for Team Transitorian is NOT DEAD. YET?