I thought this bit of research from UBS (29 Dec) was a great accompaniment TO the charts Goldilocks offered earlier, especially as it relates TO the idea that as monetary policy is to be tightened in 2022 AND it’s ALSO widely expected to see FISCAL SUPPORT TO DECLINE.

UBS, then, on MACRO VOL being here (to stay),

The pandemic injected substantial volatility into the economic data. Now reaching 2022, we are almost two years away from the onset of the pandemic. After those two years, historically high macroeconomic volatility remains. As 2021 ends, wondering how long that lasts, expect years rather than months.

It is not just the virus waves. Government spending we expect to decline nearly 20% this fiscal year, the most rapid pace since the end of World War II (see Figure 2). Some price levels are resetting sharply higher. When price levels stop going up, the growth rate (inflation) collapses to zero. U.S. monetary policymakers' asset purchase program will decelerate from an annual pace of $3 trillion (15% of GDP) to zero and perhaps negative in the space of two years. Two major superpowers stare at strategic rivalry while other global actors jockey for attention with disruption. The world's most influential central bank, the Federal Reserve, turns toward rate hikes and normalization with a new, untested framework for the conduct of monetary policy. How often does that happen?

Interesting report and visuals of their very own. Ahead of NFP, one that caught these old bond-eyes was the one pertaining TO NFP VOL, as it drills home the point that,

…Yes, the data is volatile too.

Figure 2 shows the 12-month rolling standard deviation of the monthly change in nonfarm payroll employment. To make the comparison fair the most acute monthly changes surrounding the onset of the pandemic were omitted. Over the 12 months ending in November, volatility has lingered at levels not seen since before 1990.

Continuing to read thru this note, strikes ME like listening to a modern day Yogi Berra whereby 'It's tough to make predictions, especially about the future.' UBS reiterates,

… In other words, whether acceleration or deceleration, payroll employment or inflation, the data volatility remains elevated even as we lap the onset of the virus with a second year. Things may settle down if the virus goes dormant, but the world will be very different from The Great Moderation for other reasons too ...

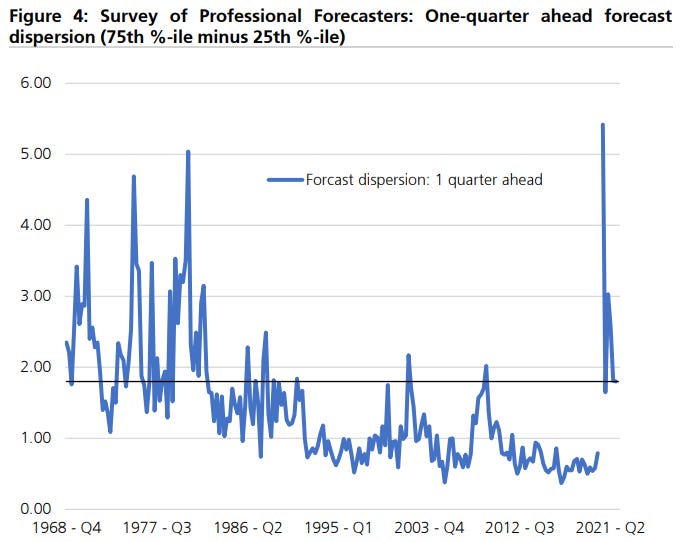

How difficult is it for the forecasting community? VERY. Specifically, as a card carrying member, UBS

… Looking at professional forecasters, it has become harder to know where we are. The forecast dispersion 1 quarter ahead, 2 quarters ahead, and so on all sat at GFC likebreadth in the 2021Q4 Philly Fed survey, well above the readings outside any recessionary period since 1991. One quarter ahead breadth is shown in Figure 4, with the acute quarters of 2020 omitted. The last value shows 2020Q4, and those survey submissions were actually submitted in October and November. That's disagreement over growth right in front of us, essentially underway, and with all the new advance data available. The volatility in the data flow means we can not see as clearly what is already happening …

SO, in other words, no matter what it is they say they think and however convinced THEY are (of … ahem … HIGHER RATES, for another example), they’ve not REALLY got a good handle on it. SEE FORECAST DISPERSION …

YET the paychecks they command for this dart-throwing exercise continue clear and this crowd of economic cognoscenti and sell side popular kids, continues to out-earn those waiters, waitresses, bar(ista’s) staff and others in leisure and hospitality, ALL from the comfort of their own homes (as opposed to, you know, those out at sea stuck on boats …).

Imagine that…The only other next best gig on the planet IS of weathermen/women. It is said that economists exist to make weatherman look good…