Truce continues, Pilgrimage HOMES hopefully nearly completed, Black Friday spending has morphed into cyber Monday and BOTH are celebrated (which is odd for an economy requiring rate CUTS as many bet / forecast next year) and the day is FILLED with Treasury DEALS … buy one 2yr at auction early this morning and THEN you have the pleasure of bidding on a 5yr auction later on in the afternoon.

Lucky YOU.

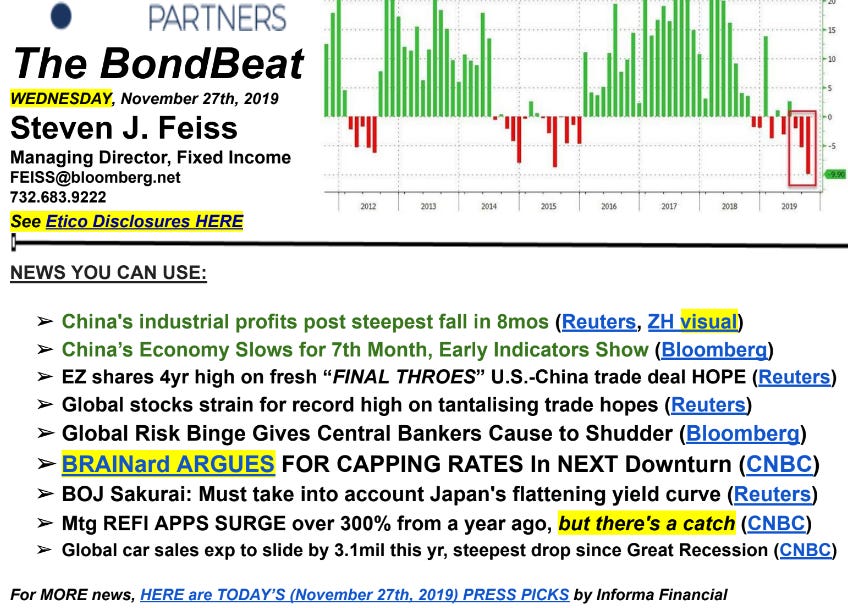

I’ve posted some levels / visuals of 2s and 5s HERE where you’ll also note several more 2024 outlooks from Global Wall … Today’ all are talking of DBs 5100 S&P call (link below) and I’ve little to add other than to say I missed wishing one and all a happy US YCC anniversary … Yesterday was 4th anniversary of BRAINard speech in which SHE argued for capping rates in the NEXT downturn which I noted THEN in my daily

AND that was THEN (happy anniversary of that which has YET to occur) and this is now where, the TOP story from this mornings press picks (below)

WSJ: Black Friday Spending Was Strong. How People Pay for Gifts Is Upending Retailers.

Consumers are shifting away from store credit cards as brand loyalty wanes and interest rates rise

… The cards, which typically can only be used at a particular chain, have been a lucrative source of revenue for retailers as merchandise sales have slowed. But the stream is drying up as Americans carry fewer cards and increasingly finance purchases with buy now, pay later providers. Interest rates surpassing 30% on some retailers’ credit cards aren’t helping, according to analysts.

ALSO in today’s WSJ and worth noting,

WSJ: Investors See Interest-Rate Cuts Coming Soon, Recession or Not

Recent data has fueled bets that cuts could come under a variety of circumstances

… Interest-rate futures indicated last week a roughly 60% chance the Fed will lower rates by a quarter-of-a-percentage point by its May 2024 policy meeting, up from 29% at the end of October, according to CME Group data. The same data has pointed to four cuts by the end of the year.

Rate expectations

Source: Tradeweb Note: Shows expected path of federal-funds rate as of Nov. 22, based on interest-rate swaps.

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… NY Open - Tranquil It's a mixed start to the week - high-beta FX are the biggest beneficiaries overnight, with the DXY index modestly under pressure. Overnight, Chinese stocks underperformed as last week's property rally unwound, though indices recovered most losses at the close. Gold prices shot higher, triggered by stops, while oil prices continue to slide. In FI, the bunds rally helped USTs reverse early losses, the former is watching budget headlines today. ECB's Lagarde also features at 09:00 EST.

Double supply today with 2y, 5y auctions may see USTs pressure later today. Otherwise, New Home Sales prints at 10:00 EST. Citi Economics are below consensus forecasts, though demand should remain strong. ILS awaits an interest rate decision. Polish PM Morawiecki will announce an interim cabinet and has two weeks to gain vote of confidence. Brazil watches tax collection data.

… and for some MORE of the news you can use » The Morning Hark - 27 Nov 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

Apollo: Credit Conditions Tightening for Consumers (NOT what you wanna see heading in TO holiday shopping season …)

The New York Fed’s latest household survey shows that a record-high share of consumers are saying that it is much harder to obtain credit, see chart below.

This is what the textbook would have predicted. When the Fed raises interest rates, it becomes more difficult for consumers to borrow.

The View: The Year Ahead is done, long live the year ahead We are bullish duration in both the US and EA – next week’s inflation data should confirm the disinflationary trend, while the German fiscal discussion serves as a useful reminder that fiscal risks in the EA are skewed towards policy that is too tight….

Rates: Bond fairy tails US: 5Y should continue outperforming the wings until Fed cuts are closer. We are cautiously optimistic on improved UST demand in ’24…

Positioning, Valuation and Risk premium are signalling that in the near-term the bar is rising for further USD depreciation. We have taken profit on our USDCNH vs. CNY basis convergence trade.

Our central case is for OPEC production cuts to be extended into Q1 24. However, OPEC cohesion falling apart would initially reduce Brent prices to USD 65-70/bbl (unless OPEC floods the market), in our view. At USD70/bbl there will be a significant demand response.

Fiscal giveaways in the UK tilt the balance of risks for the next general election to Spring 2024. We see scope for the FX vol premium attached to a May election next year to rise.

… From 2033 to 2024, and this morning we've just published our 2024 World Outlook entitled "The Race Against Time...". See it here. Over the last 2-3 years we’ve had a fairly consistent macro narrative, viewing this as a classic policy-led boom-bust cycle that would culminate in a US recession towards the end of 2023. We think our narrative still holds even if the exact timing is more uncertain. Monetary policy famously operates with lags which are highly uncertain in their timing and impact. A US recession before this point would have been early historically relative to the start of the hiking cycle. The race against time narrative refers to the fact that funding has dried up or tightened considerably over the last couple of years for various parts of economies as rates have risen. Can lending standards loosen, and can yields fall, quickly enough to avoid a funding accident that could see contagion? Non-linearity risk that can turn a mild downturn into a deeper recession remains high.

We expect global growth at 2.4% in 2024 (from 3.2% in 2023), with 2.5% generally seen as the upper bound of being deemed to be in a global recession. Even this pace of global growth relies heavily on the EM world with India (+6.0%) and China (+4.7%) big contributors. The lag of policy will help trigger a mild US recession in H1 2024 with 175bps of Fed cuts and 0.6% GDP expected in 2024. The Euro Area is on course for nearly two years of stagnation by mid-2024 when the recovery slowly starts (2024 GDP of 0.2%). The ECB will likely cut 100bps from June to YE 2024. Germany’s 2024 growth has been downgraded around half a percent to -0.2% in the week of this publication due to the Constitutional Court hearing. We also have all our 2024 asset class forecasts updated in the doc.

While our economic forecasts for the DM world suggest a sober outlook at best, the next 12 months could see more evidence that AI will revolutionise productivity growth later this decade. So the medium-term future looks more promising than it has done for some time. So try to remember that as the world flirts with recession in 2024.

DB: World Outlook - 2024 Outlook: The Race Against Time...

Over the last 2-3 years we’ve had a fairly consistent macro narrative, viewing this as a classic policy-led boom-bust cycle that would culminate in a US recession towards the end of 2023. It’s true that the recent resilience of the US economy has tested this view, but we think our narrative of the last few years holds. We only saw what is likely to be the last Fed hike in the cycle in July (ECB in September), likely closing out the most aggressive tightening of policy in several decades, and made more so when you include the QT still continuing in the background. Monetary policy famously operates with lags which are highly uncertain in their timing and impact. A US recession before this point would have been historically early measured against the start of the hiking cycle.

The race against time narrative refers to the fact that funding has dried up or tightened considerably over the last couple of years for various parts of economies as rates have risen. Lending standards generally remain very tight and yields are close to multi-year highs. After 10-15 years of negative or zero rates and substantial QE, these ultra loose conditions were expected to hold for many years. This led to some over exuberance that will be exposed if lending standards remain tight. So can they loosen, and can yields fall, quickly enough to avoid a funding accident that could see contagion? CRE, US regional banks, private markets, HY corporates and the weakest consumers, amongst others, will nervously wait on this. Non-linearity risk, that can turn a mild downturn into a deeper recession, remains high.

We expect global growth at 2.4% in 2024 (from 3.2% in 2023), with 2.5% generally seen as the upper bound of being deemed to be in a global recession. Even this pace of global growth relies heavily on the EM world with India (+6.0%) and China (+4.7%) leading the way, even if the latter will require more government support to reach this level.

DM growth will be very low with no G7 country seeing growth above 0.8% (Canada) in 2024. The US will be at 0.6%.

The lag of policy will help trigger a mild US recession in H1 2024 with the upside risks being a continuation of the inflation/labour market progress made in 2023, with the downside being the non-linearity risk mentioned above. We think there will be 175bps of Fed cuts in 2024.

The Euro Area is on course for nearly two years of stagnation by mid-2024 when the recovery slowly starts (2024 GDP of 0.2%). The ECB will likely cut 100bps from June to YE 2024. Germany’s 2024 growth has been downgraded around half a percent to -0.2% in the week of this publication due to the Constitutional Court hearing.

While DB’s 10yr YE 2024 Bund target is broadly unchanged at 2.6%, with 10yr UST yields likely to “only” fall around 40bps to 4.05%, 2yr yields are expected to fall substantially, by around 105bps and 180bps respectively.

Geopolitics and the US election will be two big ongoing themes for 2024. For the former, the peace dividend era is fraying at the edges and the latter could be the main macro story in H2. Casting a wider net, over half the world’s population vote in elections this coming year, one of the highest figures on record. So this will inject a bit more event risk after a light year for elections across the globe in 2023.

While our economic forecasts for the DM world suggest a sober outlook at best, the next 12 months could see more evidence that AI will revolutionise productivity growth later this decade. So the medium-term future looks more promising than it has done for some time. So try to remember that as the world flirts with recession in 2024.

… United States Summary: The US economy proved to very resilient in 2023. Accordingly, we have become more optimistic on the US outlook over the past year. That said, there have been signs the labor market is more clearly slowing and that consumers are softening as long anticipated headwinds hit. Our forecast of a mild recession in H1 2024 is therefore little changed since our last update in October. An even softer landing, in which inflation is tamed without the unemployment rate rising much from current levels, remains a notable upside risk to our view.

… As inflation has fallen and the labor market softened, focus has shifted to rate cuts. We continue to expect the first rate cut of 50bps to occur in June 2024 as core PCE inflation moves clearly below 3% and the unemployment rate reaches 4.5%. On our forecast, the Fed cuts rates by 175bps in total next year, bringing the fed funds rate to 3.6%, and a further 50bps in early 2025. At that point, the fed funds rate would be broadly consistent with our view of the nominal neutral rate (3-3.5%), which is above the Fed’s median long-run dot. Cuts on our forecast occur later than policy rules would suggest, consistent with our view that the Fed is intent to not repeat the mistakes of the 1970s of easing too early and too aggressively.

… Rates: Priced for perfection We expect 10Y UST to decline to 4.05% and 10Y Bund to remain broadly unchanged around 2.6% at the end of 2024. The most salient feature of our forecast is a significant steepening with 2Y UST declining to 3.15% and 2Y Bund declining to 1.97%. As markets are already pricing a soft landing and term premia remain too low, the risk reward for steepeners is attractive, notwithstanding the current uncertainty about the timing of an easing cycle. On the other hand, the BoJ is significantly behind the curve in tightening policy. The more the easing cycle in the US is delayed, the more likely it is that the BoJ will have to hike interest rates substantially more than currently priced in…

… Equities: Solid fundamentals, poor perceptions … Setting 2024 year-end S&P 500 target 5100. Our base case for EPS remains $250, but it incorporates a mild short recession whose timing has been rolled forward. Allowing for some continued roll forward, we set a target of 5100 for year-end 2024; in our upside scenario, EPS of $271 should see the multiple expand some, so S&P 500 at 5500. We note that the S&P 500 has been in a clear trend up channel since the GFC. After falling below last year, the rally in the first half this year took it back up to the bottom and it has been muddling along at the lower end since. A continued muddle through along the bottom implies 5300 by end 2024, while a move to the middle to 6000. By comparison, our base case target of 5100 and even the upside scenario of 5500 look conservative…

… Early signals suggest record online sales over the US Black Friday consumer festival. Caution is needed —while the US lags some other developed economies in online retail, the trend to virtual shopping is increasing and this data may cannibalize in-person sales. “Buy now, pay later”, the most traditional form of credit, seems to have been favored …

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Bond Market’s Dramatic Recovery Is Seen as Opening Act for Broader Revival

Recent yield slide erases 2023 losses for US Treasury index

Cooldown in inflation, jobs gives Fed incentive to pivot

… “I don’t think the Fed is going to be fast to pivot” but that will be “the direction of travel,” said Ashish Shah, chief investment officer of public investing at Goldman Sachs Asset Management. “That’s because you are seeing inflation coming down as well as a deceleration of growth.” Next year “is going to be the year of bonds, with them performing well. You’ll also see a steepening of the yield curve because there is a lot of borrowing that is going to take place.”

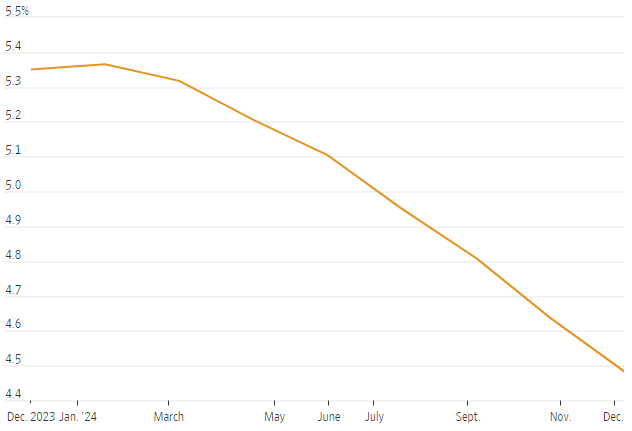

Benchmark 10-year Treasury yields have fallen just over half a percentage point after hitting a 16-year high of 5.02% on Oct. 23, to hover at about 4.47% as of Friday afternoon in New York. Two-year yields traded at 4.95% versus a high this cycle of 5.26% reached last month…

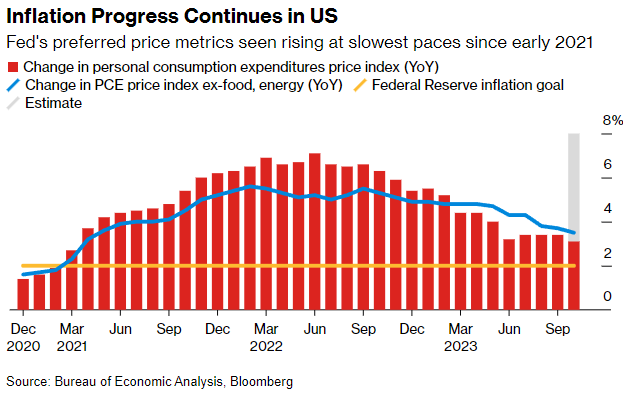

Bloomberg: Inflation Gauges at 2021 Lows May Support End to Hikes: Eco Week

Fed’s preferred measure and euro-zone index due Thursday

OECD will release global forecasts, and Lagarde will testify

… The Federal Reserve’s preferred measures will be published on Thursday, with the personal consumption expenditures price index seen rising 3.1% in October from a year ago. The core measure, which excludes food and fuel and is considered a better gauge of underlying inflation, is expected to have climbed 3.5%.

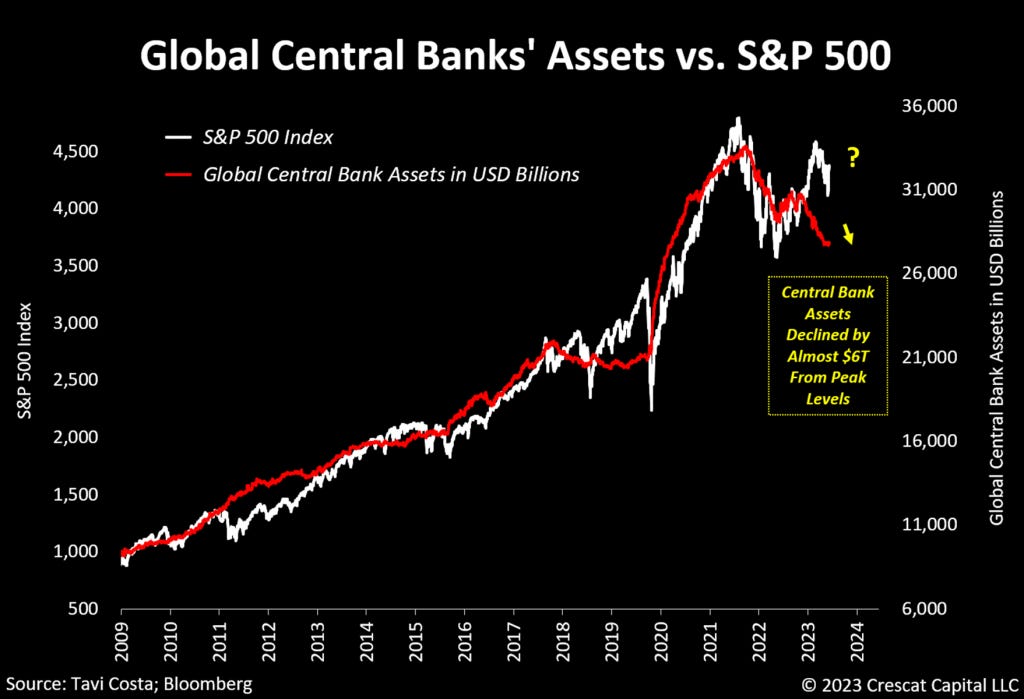

Crescat Capital: A PROFUSION OF RECESSION INDICATORS (like ‘em or not, some funTERtaining charts … like this oldy but goodie on liquidity drainage)

… A Major Liquidity Withdrawal

Global central banks’ assets have already declined by almost $6 trillion from peak levels. To be clear, that does not include any mark-to-market losses from the recent collapse in prices of sovereign bonds worldwide. Undeniably, this is a major liquidity withdrawal from financial markets. More interestingly, the chart below shows the historical correlation between the aggregate size of central banks’ balance sheets and the performance of US equity markets. We have recently noticed an important divergence in these two metrics, which in our strong views indicates that the overall equity market has significant downside potential from their current prices.

Despite the prevalent belief that the recent stock rally signifies the start of a new bull market, we align ourselves with a historical perspective that quantitative tightening is significantly draining liquidity from the system, and the economy is still on track for a hard landing.

It is worth noting that although technology stocks, particularly mega-cap companies, have carried most of the market gains so far this year, the year-to-date performance of eight out of eleven sectors is currently negative.

AND me after hitting send, watching AMZN cart all day like

Fascinating Read !!!

Agree that the 10 yr might only fall to 4.05%

I have trouble with the thought that Powell will go 50 in June....I'd probably think 25, more likely

for Mr. Careful....

Gov. L. Brainerd.....More like Ms. Brainless......

Like the Black Friday post at the end of the article......Accurate..... LOL!!!!