while WE slept: USTs xtend gains (flattening) on light volumes; here we go again (GME); a nuanced lean LONG, "... via equi-notional 2s/5s flatteners..." (JPM)

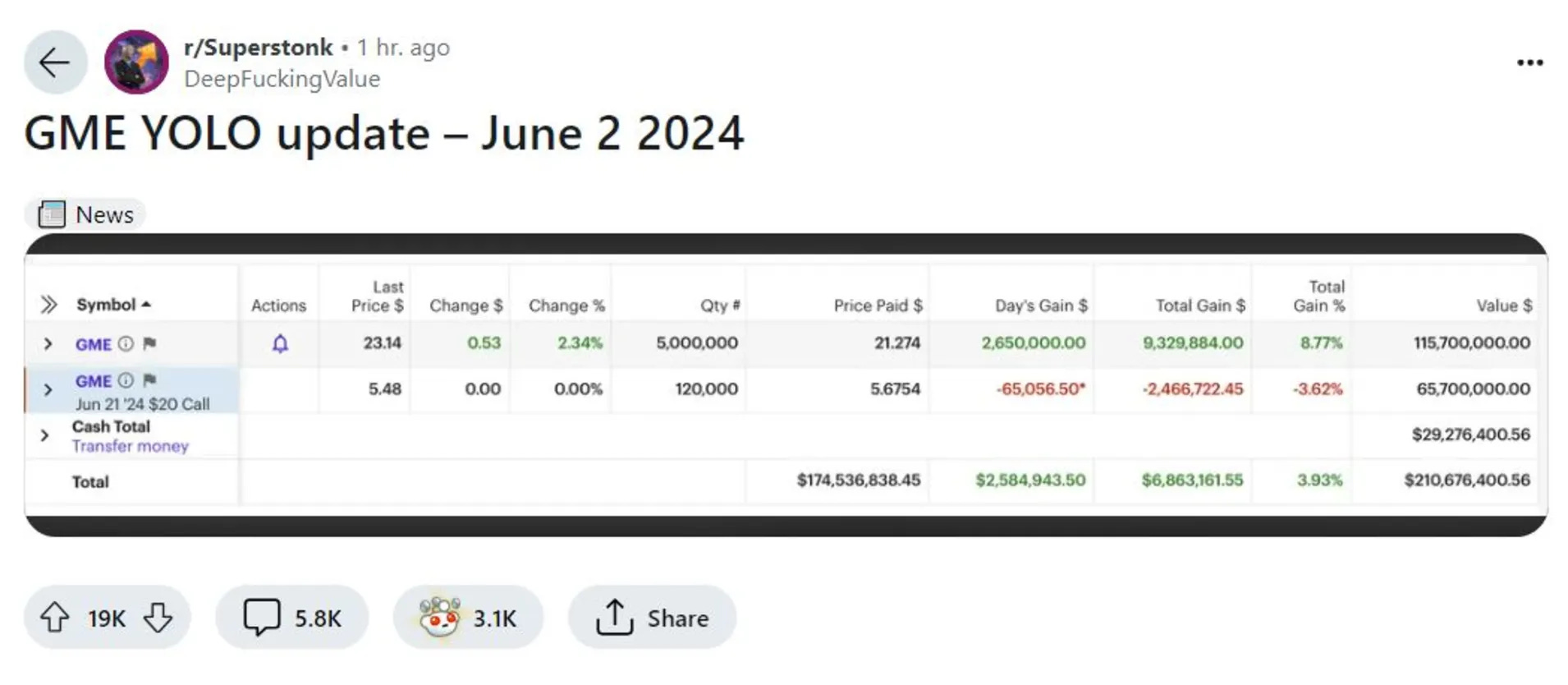

CNBC: GameStop shares surge 70% after ‘Roaring Kitty’ trader posts account showing $116 million position

… The post was not independently verified by CNBC. Notably, he didn’t post on the infamous WallStreetBets chatroom where he posted all of his trade updates at the height of the GameStop mania over three years ago, although the username is the same one used.

Around the same time Sunday night, Gill posted a cryptic picture of a reverse card in the game “Uno” on X.

in addition to 2yy weekly and 10yy daily visuals (and a couple / few other things) noted over the weekend (HERE) and in light of months end now in the rear - view mirror …

5yy Monthly where the 2024 UPTREND appears to be intact BUT at risk AND (overSOLD) momentum appears to be waning

… something for mostly everyone, especially those on Team Rate CUT. For more on how the data / inputs all settled out on the month behind, be sure to check out DBs latest Monthly Performance Review just below.

In the meanwhile, here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are extending gains from Friday amid modest flattening pressure on long-end buying in Europe. The French downgrade by S&P last week has seen limited impact on spreads in Europe, though EURUSD is modestly weaker in early trading. Instead, USDMXN has shot 3% higher on ~7x the usual trading volumes post-election. Crude Oil is unch’d after OPEC extending production cuts into 2025, Citi analysts turning neutral (0-3m target lowered to $82). EU nat gas / electricity prices are much higher this morning however, after an unplanned outage in Norway. APAC equities were buoyant overnight (KOSPI +1.7%, NKY +1.1%), and so are US (NQs +0.5%) and EU bourses (DAX +0.9%). UST volumes are running ~75% the 30d ave.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: Equities firmer, DXY is incrementally firmer and Crude is choppy after OPEC+; US ISM Manufacturing due … USTs are firmer as Friday's PCE momentum remains in the driving seat into the ISM Manufacturing PMI. Within this, the Prices Paid metric will draw scrutiny following the jump to 60.9 (prev. 55.8) which took it into strong expansion territory.

We don't expect the ECB’s well-telegraphed rate cut to have a large market impact, although at the margin risks skew to a more dovish reception.

We initiated a short EURCHF trade idea, as we see room for a more hawkish Swiss National Bank … USTs continue Friday’s post-PCE advance ahead of US ISM Manufacturing …

In South Africa, ongoing election uncertainty means it’s too soon to turn bullish on local assets.

… So, this week’s payroll print will be key. However, it’s unlikely that we are heading towards a marked deterioration in the US labour market. Instead, we project continued rebalancing in line with a downward trajectory in job vacancy rates. We estimate payrolls growth will have decelerated to 200k in May from the 246k average pace of job creation so far this year (see US May jobs preview: Rebalancing, not deterioration, dated 29 May). We think the sharp drop in the pace of job creation between March and April likely overestimated the degree of weakening, at least partially due to the early timing of the Easter holiday this year, which could have pushed some hiring forward.

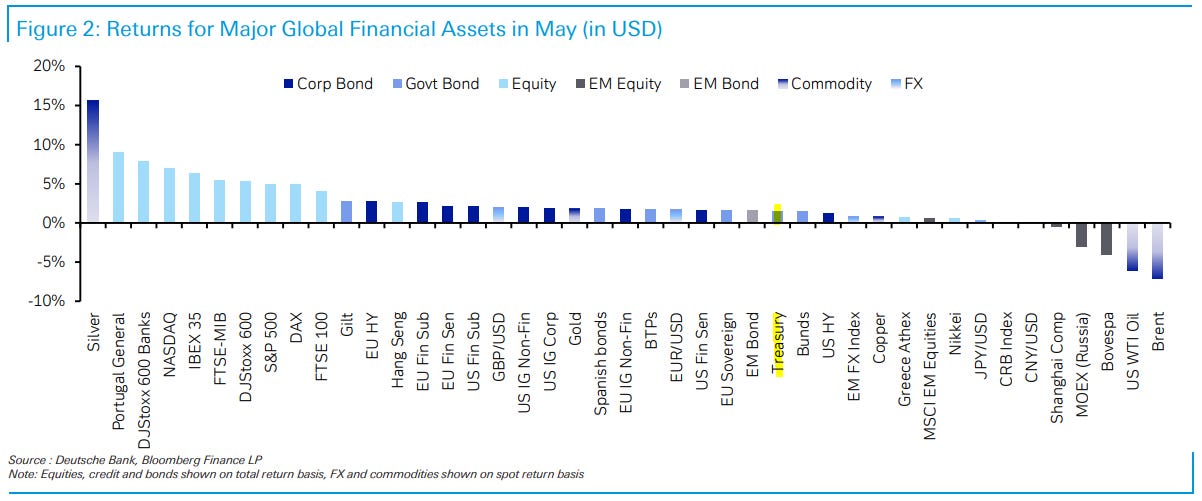

… Which assets saw the biggest gains in May? … US Treasuries: Although they lost ground towards the end of the month, US Treasuries were still up +1.5% on a total return basis. They were supported by Chair Powell’s comments that it was “unlikely” the next move would be a hike.

As we approach the half-way mark for 2024, the global economic outlook is looking increasingly positive. In the US a soft landing is a strong consensus with the economy proving impressively resilient against the rapid rate hikes of 2022-23. Growth is looking more positive in Europe too, with external demand helping to end the stagnation of the last couple of years. Over in Asia, China’s growth has surprised on the upside in Q1, whilst Japan’s growth should stay above potential.

There are plenty of obstacles to navigate. The global economy is still experiencing the lagged effects of tighter monetary policy. QT is continuing. Inflation has come down, but both headline and core inflation are still above target in several major economies, including the US and the Euro Area. The rest of 2024 will also see an unusually large number of elections, with the US election the main focus, providing the potential for major implications for the global trading system and our forecasts. Moreover, those elections come against the backdrop of several geopolitical hotspots, including in the Middle East and Ukraine. Indeed, given the surprises of recent years, it’s hard to imagine there won’t be at least some economic shock over the next couple of years. So a positive outlook for now but with uncertainties ahead.

Some highlights:

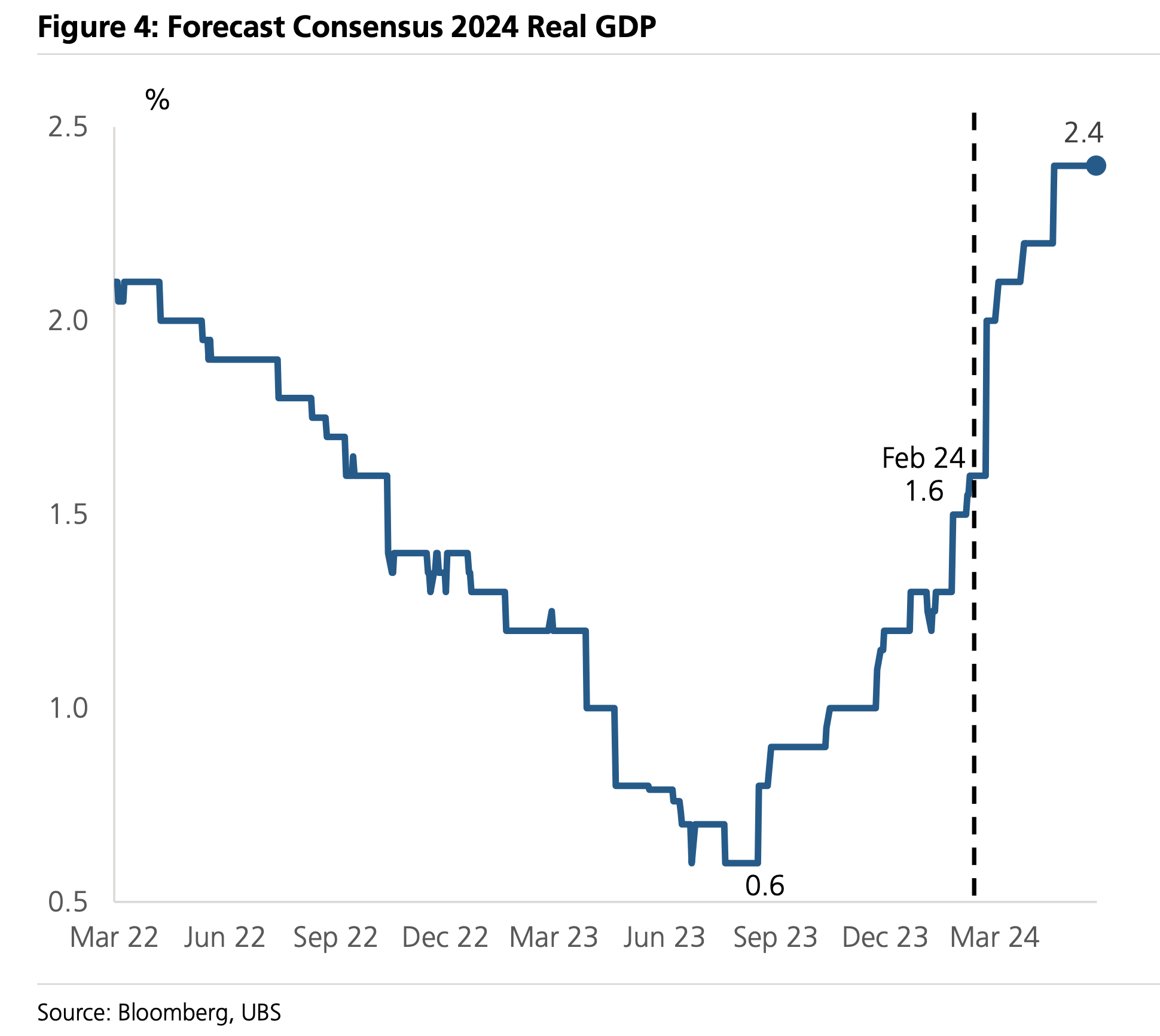

After a big lift in January, our US economists’ growth forecasts remain at the higher end of consensus for the next two years (2.4% in 2024, 2.2% in 2025) but with the election a risk to the base case.

Our economists are upgrading euro area 2024 growth by half a percent to 0.9% but this is more cyclical than structural with 2025 forecasts remaining unchanged at 1.5%.

In China our economists upgraded 2024 growth to 5.2% in April, supported by ongoing export growth and accelerating fiscal spending. Beyond that, growth will likely slow to 4.5% in 2025 with the housing market facing downward price pressures from an excess supply of homes.

In Japan our economists are more hawkish on rates, believing that the BoJ will hike to 1% by Q1 2026.

India remains a beacon of growth with a minimum of 6-6.5% real GDP growth and 10-11% nominal growth over the next several years.

In Rates, our strategists believe term premia is too low globally, thanks in part to a structural shift in fiscal policy that’s likely to endure.

We are neutral duration in the US and EUR. Our forecast sees slightly higher 10y rates by year end with 10y UST at 4.6% and 10Y Bund at 2.7%.

Relative to current market pricing, the most salient feature of our forecast is the view that term premia are too low globally …

In FX, the bullish view on the dollar and FX carry is maintained with the conditions needed for a stronger Yen yet to materialise.

In equities, the YE 2024 S&P 500 forecast is at 5,500 but with a tactical preference for Europe.

Credit spreads are expected to grind tighter over the summer with the hefty HY maturity wall the medium-term risk.

… Treasuries Add tactical bullish exposure via equi-notional 2s/5s flatteners

Over the near term, further moderation in job openings and a slower pace of job gains could further support a decline in yields, and even with the rally the last few days, valuations remain somewhat attractive

In a tactical, range-trading environment, it’s tough to hold outright long duration positions, given their negative carry profile. We find more value in equi-notional flatteners, which offer low-beta bullish duration exposure with better carry profiles...

...synthetic 2y3y exposure constructed from 2s/5s flatteners offer the best value, given the combination of a relatively flat carry profile and still high exposure to changes in front-end yields: we recommend adding equi-notional 2s/5s flatteners

The 20-year sector has outperformed significantly, given a tailwind of cheap valuations, strong carry and positive supply technicals. However, the potential for further gains seems limited without a continued decline in volatility. The sector’s increasing sensitivity to implied volatility underscores its recent performance but also indicates caution for maintaining longs in 20s

We recommend unwinding 100:95 weighted 4% Feb-2028s/ 4% Feb-2030s steepeners

Treasury FRN DMs have narrowed 11bp YTD, supported by a reduction in Fed easing expectations and narrower GC/OIS spreads. Looking ahead, we think these supports are likely to reverse and prevent FRN DMs from narrowing much further …

… Overall, though yields have declined from their local highs earlier this week, we think valuations remain somewhat attractive …

… Technical Analysis

… Tens converge on the 4.475% 50-day moving average as the market bounces in a springtime range cheaper than key levels in the 4.30s. Look to the 4.75% area to continue to mark key support and a rally to eventually extend from that area through the cluster of moving averages in the summer months.

EM remains heavily influenced by core rates and so the tone of this week's ECB meeting accompanying the expected cut will be important. However, there are also strong idiosyncratic stories in EM which we cover in our recently published detailed mid-year outlook, with core trades below.

… For a reminder of our core views, our US team continues to see US CPI coming down in a way that gives the Fed the confidence to cut in each of the final three FOMC meetings of the year, with our rates strategists expecting this to bring 10-year UST yields to 4.1% by end-2024. There remains market scepticism about this call, but this should fade as we move through the summer…

Federal Reserve President Kashkari has advocated a significant tightening of central bank policy, by raising real interest rates (keeping nominal rates stable as inflation slows). The pain of this would likely hit lower income groups disproportionately. Kashkari’s wants to keep inflation expectations anchored—yet inflation expectations are properly observed through consumers’ actions (certainly not through surveys). Moderating wage growth suggests well-anchored expectations…

Wells Fargo: June Flashlight for the FOMC Blackout Period

Summary

The FOMC remained on hold for the sixth consecutive policy meeting on May 1 as elevated inflation and strong job growth earlier this year led policymakers to conclude that policy easing at that time would not be appropriate.

Data released since the last meeting indicate that the threat of price re-acceleration due to strong economic activity has diminished somewhat. However, we share the universal expectation that the FOMC will keep its target range for the federal funds rate unchanged at 5.25%-5.50% at the conclusion of its policy meeting on June 12.

We expect to see a nod in the post-meeting statement to the recent mix of activity and price data suggesting a lower risk of price re-acceleration, but we think the Committee will continue to characterize inflation as “elevated.”

The FOMC will publish its quarterly update to the Summary of Economic Projections (SEP). The last dot plot, which was released in March, showed the median Committee member anticipated 75 bps of easing by year-end 2024. We look for the median projection in the updated dot plot to signal 50 bps of easing by the end of the year. However, we would not be surprised if the median dot shifted up to only 25 bps of anticipated rate cuts in 2024. The May employment report to be released on June 7 may be the deciding factor.

We will also be keeping a close eye on the Committee's "longer-run" fed funds rate projections. The median longer-run dot was essentially unchanged at 2.5% between June 2019 and December 2023. The median ticked up ever so slightly to 2.56% in the March SEP, and our best guess is that the median longer-run dot is headed modestly higher in the June SEP, probably to a value between 2.625% and 2.75%.

We do not look for any major changes to the macroeconomic forecasts in the SEP. The Committee's projections for real GDP growth do not seem likely to change materially.The median forecast for the unemployment rate at year-end 2024 may increase by a tenth or two, and median projections of PCE and core PCE inflation rates for this year seem likely to increase by about 0.2 ppt each in our view.

… And from Global Wall Street inbox TO the WWW,

Apollo: Four Years After Covid: Downtown Recovery Remains Weak

Data from downtowns shows that cellphone activity in San Francisco is at 57% of pre-pandemic levels, see chart below. Las Vegas is at 97%, and Miami is at 82% of 2019 levels. The slow recovery of downtowns combined with rates higher for longer has important implications for retail, restaurants, and offices.

Sam Ro from TKer: Bull markets are usually longer and stronger than this

… UBS raises its target for the S&P 500 On Tuesday, UBS’s Jonathan Golub raised his year-end target for the S&P 500 to 5,600 from 5,400. This is his third revision from his initial target.

“On February 20, we upgraded our market target to 5,400 citing robust economics,” Golub said. “Since then, consensus 2024 GDP forecasts have increased from 1.6% to 2.4%. At the same time, recession/tail risks have declined on a number of key metrics including economist surveys and the Chicago Fed's Financial Conditions Index. These trends also support further market upside.”

Roaring Kitty, I wish he'd go away....all he does is lead the Lemmings to the Ledge