Optimism on Main Street continues to grow with the improved economic outlook following the election. Small business owners feel more certain and hopeful about the economic agenda of the new administration. Expectations for economic growth, lower inflation, and positive business conditions have increased in anticipation of pro-business policies and legislation in the new year. -NFIB Chief Economist Bill Dunkelberg

AND some more ‘GOOD’ news overnight spurring a bit of further risk ON …

The global bond selloff and tariff policies of the incoming Trump administration have again been the key market themes over the last 24 hours. Yields reached new highs yesterday, with 10yr Treasury yields up another +2.0bps to 4.78%, their highest since October 2023, while here in the UK 30yr yields again reached post-1998 highs. The market focus shifted towards trade yesterday evening, with a Bloomberg report suggesting that Trump’s economic team were discussing a “gradual approach” to tariff increases. This is driving a risk-on mood overnight even if you could read the story as being hawkish (see below). Before the story broke, US equities had already managed to shrug off the pressure from rates as the S&P 500 closed +0.16% higher, reversing a near -1% initial decline that saw the index trade below its pre-election day levels intra-day … -DBs Early Morning Reid, 14 January 2025

… AND with that bit of ‘good’ news in mind …

Bloomberg: Trump Team Studies Gradual Tariff Hikes Under Emergency Powers\

Plan would boost import duties 2%-5% a month on trade partners

Supporters include Trump advisers Bessent, Haslett and Miran

Members of President-elect Donald Trump’s incoming economic team are discussing slowly ramping up tariffs month by month, a gradual approach aimed at boosting negotiating leverage while helping avoid a spike in inflation, according to people familiar with the matter.

One idea involves a schedule of graduated tariffs increasing by about 2% to 5% a month, and would rely on executive authorities under the International Emergency Economic Powers Act, the people said…

I’ll quit while I’m behind and suggest the new admin will continue to enjoy ‘honeymoon’ phase and small businesses will continue to rejoice until they have less reason to do so.

I’m no longer part of a small business and so I’ll leave well enough alone and move along … here is a snapshot OF USTs as of 652a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK: US Market Open: Crude under pressure as a Gaza ceasefire nears & stocks grind higher on “gradual” Trump tariff reports … Fixed Income is off best levels ahead of US PPI … USTs were initially firmer, but now reside around the unchanged mark. The primary overnight update was reports that President-elect Trump’s team is discussing a gradual tariff approach that could be done on a month-by-month basis, a Bloomberg report which helped to lift the risk tone and provide yields with some respite. As it stands, USTs find themselves at the lower-end of a 107-11 to 107-18+ band with yields softened across the curve and the belly leading thus far, as such there is no overt flattening/steepening bias in play. US PPI and Fed speak from Williams and Schmid due.

Opening Bell Daily: Trump Trade slowdown … The Trump Trade is evaporating from the stock market … The S&P 500 hovers close to where it traded just before election day.

Our NLP analysis suggests FOMC members' views on the monetary policy outlook diverged more than in November, though the committee did seem to be on the same page in preferring gradual easing. Inflation agreement remains elevated despite a pullback, with agreement on upside risks.

Our analysis of the December FOMC meeting minutes using NLP techniques1 suggests diminished consensus among committee members regarding the outlook for monetary policy and inflation relative to November, albeit inflation agreement remains elevated. On the contrary, the indicators showed increased agreement on the labor market and economic outlook (Figure 1).

Best in show offering recap and state of ‘things’ in global bond markets …

Treasuries were under pressure again on Monday, although the market managed to gain slightly off of the overnight lows. There are two primary preoccupations among investors at the moment – first, how did US inflation perform during December and second, what will Trump do on the tariff front during his first few weeks in the White House? Resolution to the former will come far sooner than the latter. By Wednesday morning, the market will have the coreCPI figures for December and Treasuries will adjust accordingly. In light of the magnitude of the inflationary angst at the moment, we’ll argue that the US rates market is trading as if investors are very wary of an upside surprise. To be fair, while the consensus is for a +0.2% monthly gain in core-CPI, the average estimate is +0.24% – which leaves open the real possibility of an above-consensus, low-0.3% print. Ultimately, the combination of CPI, PPI, and Import Prices will afford the market a solid estimate of core-PCE by the weekend; although the bulk of the market’s response will be to the core-CPI move.

As for Trump’s initial actions, there is growing concern that the incoming Administration will attempt to declare an economic state of emergency, which would allow the President great latitude in imposing tariffs on the key trading partners of the US. In the event that Trump takes this approach, we would expect a more dramatic change in the tariff structure and a sharper response in financial markets. At a minimum, this would translate into higher Treasury yields and, presumably, further weakness in the equity market – both as a function of higher rates as well as an escalation of overall economic uncertainty…

…it is still too soon to buy the Treasury market – even as 10-year yields pushed up to 4.802%. We’re increasingly open to 10s testing 5.0%, even if we ultimately expect it will be a level that represents a buying opportunity as the performance of the real economy unfolds in the year ahead. It’s difficult to envision that the goldilocks narrative can continue indefinitely. In fact, the stickier inflation remains, and the more that inflationary angst prevents the Fed from normalizing policy, the greater the probability that the Committee’s flexibility translates into greater economic damage. Alas, that argument could have been more convincingly made at 5.50% fed funds.

Germany weighing in identifying who’s who in the DOTS <GO>, cuz you really need to know … hey, something to read as you play along with #FOMC101

ING: Rates Spark: It's not just US rates exploring new highs

While rates on Monday stabilised, this cannot hide the fact that markets have reassessed their Fed expectations quite noticeably. In fact, the stabilisation was only after touching new post payrolls bond yield highs. Markets are likely to maintain their bearish untertone until data signals otherwise. ECB members are trying to head off spillovers, but likely to little effect as EUR rates have also risen for homemade reasons …

A note summarizing all things thematic at this moment in time …

MS: California wildfires: Inflation up, payrolls & retail sales softer

Current wildfires are expected to be among the most destructive in history. They will likely hit the next data prints. Past episodes suggest a boost to core goods prices, slower employment gains, and perhaps softer retail sales.

Key takeaways

Expect core CPI m/m inflation push of 4bp to 9bp post-wildfires, driven by car prices.

Projected 20k to 40k drag on CA payrolls in January.

Retail headline and control likely down versus trend initially, but historical data are noisy.

Core inflation accelerates, mostly core goods

Pouring some cooler water on the ‘good’ news overnight, noted above …

Markets have reacted to media reports suggesting that the next US administration will impose trade taxes on US consumers gradually, month by month. Remember past media reports on tariff policy have subsequently been denied over social media. This is a boiling frog approach—the price level effect is the same, but consumers may not notice so much. The risk is that repeated tariff increases would encourage repeated profit-led inflation episodes by providing a convenient cover story.

US December producer price inflation is due. This will be worth watching as tariffs develop because trade taxes will increase input costs for US companies. If tariffs succeed in reducing imports, the loss of competition to US firms may also increase pricing power.

The US NFIB small business survey is due. This soared in November, but that likely reflects the partisanship of the survey rather than representing an actionable economic change…

Same shop with an economic chartbook (I love pictures) of the long game …

In 2025 we expect oscillations around a decelerating expansion. The economy did not slow as much as we expected in 2024, but growth has cooled, and the labor market has slowed on the back of that.

YTD real GDP has expanded 2.6% annualized, compared to 3.2% for the same period of 2023. Nonfarm payroll employment averaged gains of 165K for the six months ending in December, down from the over 200K pace of 2023.

We expect the incoming administration policy changes impact 2026 more than 2025. Also note that Chair Powell has warned FOMC reaction to tariffs is more complicated than assumed.

We expect inflation resumes progress lower in 2025, and combined with labor market risks motivates 2025 rate cuts. Last spring, the market priced just one 25 bp cut in 2024, but the FOMC delivered 100.

…Inflation: a bumpy path lower Headline PCE inflation went from over 7% back down essentially to the FOMC's 2% target. However, core inflation remains notably above 2%. Tariffs we expect to lead to a moderate pickup in 2026. The magnitude matters for rates.

… The 10-year Treasury yield around 4.75% is about 40 basis points above the Fed Funds Rate. Historically, back to 1970, this spread in periods outside recessions, averaged 126 basis points, suggesting room for further upward movement in long-term rates if the economy remains strong. A rise to levels approaching 5-5.5% on the 10-year yield would not be inconsistent with a normalizing term structure.

The Fed Funds Futures market, after correcting for the hedging demand of these Futures that I often discuss, at best is now pricing in just one cut in 2025. The market has largely now discounted the Fed being on pause for most of 2025.

Equity markets continue to grapple with higher discount rates, which compress valuations. The S&P 500, trading at 23x forward earnings, reflects overly optimistic growth assumptions. Consensus earnings growth of 16% for 2025 is likely too high; an 8–9% increase is more realistic. Consequently, the market could see a correction as valuations adjust to higher rates and moderated growth expectations …

… And from the Global Wall Street inbox TO the WWW … a few curated links from the internet …

I’ll begin with this visual from X …

at alphatrends

The measured move for bonds $TLT suggests a continuation down towards 82.63 and it would be best to see a slight undercut of the Oct 2023 low of 8242 before a reversal

Trend remains lower = guilty until proven innocent

A VIEW from Bloomberg … seems there remains a definitive and palpable desire out there to see a failure …

Bloomberg: Inflation could derail Trump 2.0 before it starts The battle of expectations continues. Republicans believe inflation will fall to 0.1%, while Democrats foresee 4%.

Here We Go Again We ought to have been able to forget about inflation by now. It was trending down, the Federal Reserve was cutting rates, and attention could move on to averting a recession and sustaining employment. But startlingly strong US employment, a global surge in bond yields, and a big rally for the dollar all ensure that the last consumer price inflation numbers for 2024, published Wednesday, will command attention. If the consensus of the economists interviewed by Bloomberg has it right, then the December number will mean yet more frustration, with core CPI (excluding food and fuel) remaining unchanged at 3.3%, too high to permit more rate cuts:

A significant rise would really set the cat among the pigeons. Worse, inflation expectations can be self-fulfilling. If consumers or companies expect prices to rise, they will buy more now — which pushes up inflation. The market’s clearest inflation forecast comes from the gap between inflation-linked and fixed-income yields. The point at which they break even is the implicit expected level of inflation. On that basis, the 10-year breakeven’s recent rise is generating disquiet. It’s within its range for the last two years, but only just:

Meanwhile, the University of Michigan’s regular consumer survey found that expectations for inflation in five years are now higher than they ever were during the spike in price rises of 2022. With the exception of one month in early 2008, when the oil price was surging and about to crash, its current 3.3% is the highest in any month since 1996:

…Rising inflation now could ruin the Trump 2.0 agenda before it starts. Thus, the risks of conflict with the Fed appear to be growing. SMBC Nikko’s Joe Lavorgna, an economic adviser in the first Trump administration, put it this way:

The Fed cut rates by a larger than expected 50 basis points last September when the job market appeared to be faltering. But then the jobs data rebounded and inflation surprised to the upside, and the Fed kept cutting interest rates by 25bpsin November and December. The last cut was especially perplexing since it was accompanied by upward revisions to both their growth and inflation forecasts. If inflation remains sticky, monetary policymakers will be responsible.

That may well be true — but the message of the last four years is that incumbent politicians pay the greatest price for higher inflation.

SanFran FED — Daly — reflecting on Bernanke …

FRBSF Ben Bernanke: Solving a Crisis, Changing the Fed

Ben Bernanke’s contributions to economic thinking have been vast, from his extensive study of the Great Depression to groundbreaking research on the interplay of finance and the macroeconomy and the usefulness of unconventional monetary policy tools. His research helped guide his tenure as Federal Reserve Chair and his role in putting the U.S. economy on a path to the longest expansion in its history. Through that role, he also built a better and more transparent Fed for the future. The following remarks are adapted from a presentation by the Federal Reserve Bank of San Francisco president, who joined Christina Romer (University of California-Berkeley), Mark Gertler (New York University), Emi Nakamura (University of California-Berkeley), and Peter Rousseau (Vanderbilt University) to discuss Bernanke’s legacy at the American Economic Association Annual Meeting in San Francisco on January 5.

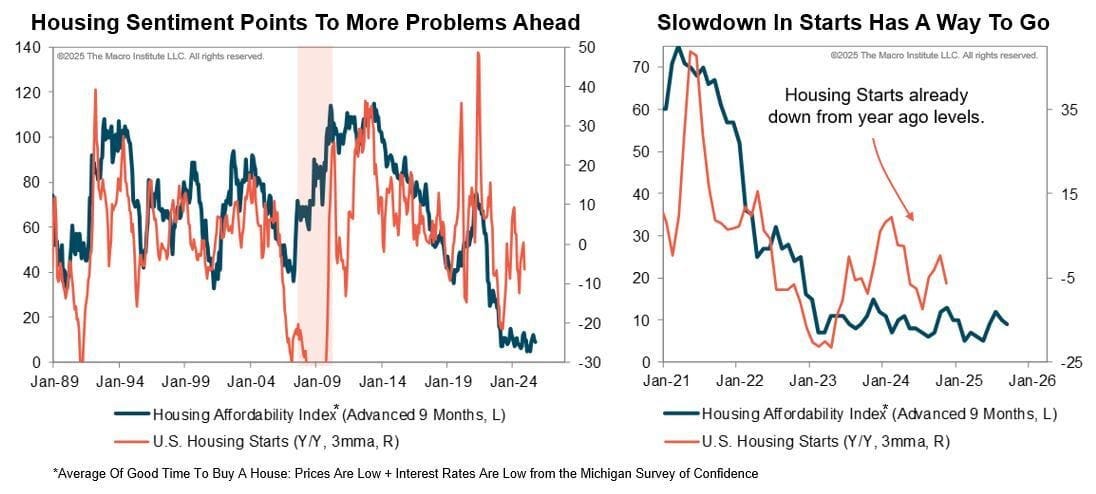

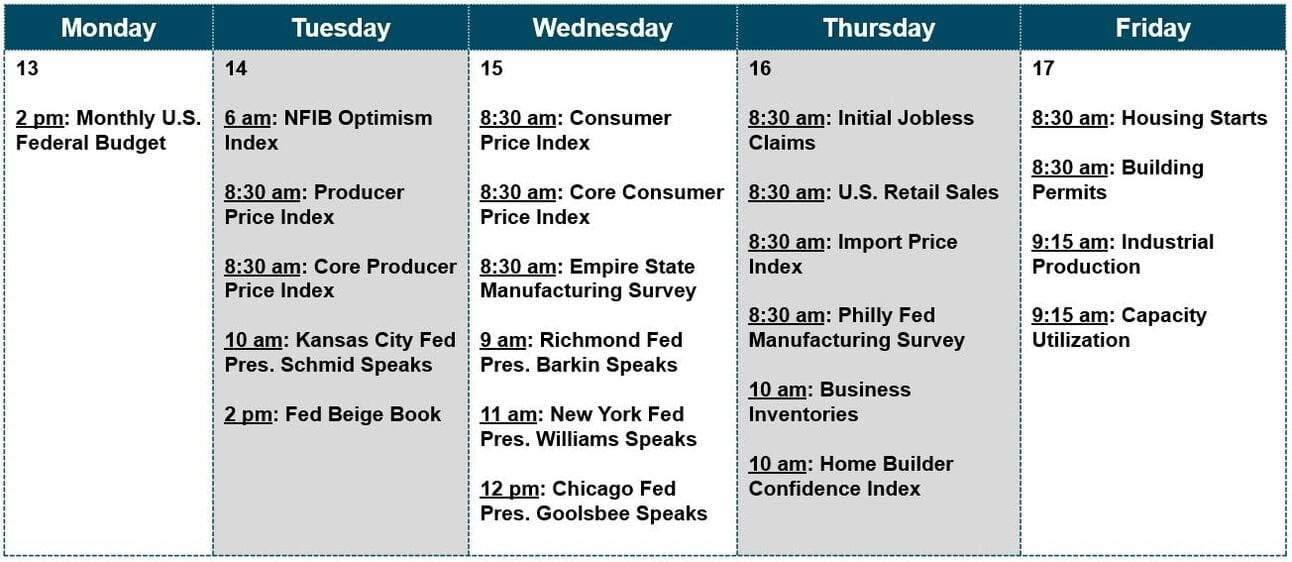

There is so much happening on the data calendar this week that it was difficult to figure out what to highlight. On the inflation front, we get PPI on Tuesday and CPI on Wednesday, and we also have the first regional PMI releases for January with both the Empire Fed Index and the Philly Fed on Wednesday. Those are both important data sets, but we think that housing is the star of the week. Although it’s a small part of GDP, housing provides key insights into household sentiment. The NAHB survey will be released on Thursday and will likely come in lower considering the significant rise in mortgage rates in the last month. On Friday, we’ll see both Housing Starts and Building Permits. The latter typically correlates strongly with the NAHB so don't expect anything surprising. Meanwhile, Starts tend to follow trends in Housing Sentiment and that is sitting near all-time lows as of Friday's Michigan Survey. A lot to digest this week!