… i’m reminded that NONE of us will look back on these two points of data as having any other impact other than MAYBE, just maybe, some (lunatic)fringe demand for the 3yr auction … which came and went as with a bit of a thud as a dud …

ZH: First Bond Auction Of 2025 Tails As Foreign Buyers Slide

… the grandaddy of economic data rays of light is to be Friday’s NFP and a slowing (for better and / or worse) is widely anticipated. IF it slows enough, I suppose it will reinvigorate rate cut pricing. What it may / may NOT do as far as stonks are concerned, well, I wouldn’t even venture a guess any more. Even when I used to try and offer that guess (NFP weak / hot = some reflex in risk = some other equally and opposite reaction in FI), I used to say that if you had given me the data points I’d prolly muck up the trade.

I don’t feel any more confident as 2025 gets underway so I’ll skip TO a look at 10s ahead of this afternoons $39bb auction …

10yy DAILY: the level in / around 4.63/4% is presenting itself …

… and doing so as bonds appear overSOLD (momentum, stochastics bottom panel) and while stopping short of saying ‘buy buy buy’, certainly reason for a pause …?

… said another way, 10s vs 4.64 much like The Black Knight …

… and for more on this, see below thoughts / note / link to CitiFX …

… for somewhat MORE eye candy from one with A Terminal, ahead of this afternoons auction …

NEWSQUAWK: US futures gain modestly, USTs contained into data & supply … USTs are contained into data, EGBs lift slightly on HICP, Gilts lag … USTs are flat, in a narrow 108-13+ to 108-20 band. Complex awaits US data incl. JOLTS and ISM Services alongside Fed’s Barkin (expected to reiterate remarks from 3rd Jan.) before 10yr supply. Last night’s 3yr auction was soft overall and weighed on USTs into settlement.

US corporate bankruptcies have hit their highest level since the aftermath of the global financial crisis, rising 8% Y/Y to 686 companies in 2024, as elevated interest rates and weakened consumer demand punish struggling groups. (FT)

Finviz (for everything else I might have overlooked …)

Opening Bell Daily: Nvidia's building its own future … Nvidia is building the future in its own image — and Wall Street loves it … The stock hit a record high as its CEO delivered a bullish keynote revealing new Blackwell chips.

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

First up, a(nother)NFP pre-cap …

BARCAP: December employment preview: Never a cloudy day

We expect the December employment report to show a 150k job gain, returning to a more normal pace after prior monthly distortions. We expect the unemployment rate to be unchanged, to rounding, at 4.2% and hourly earnings to decelerate to +0.3% m/m (4.0% y/y).

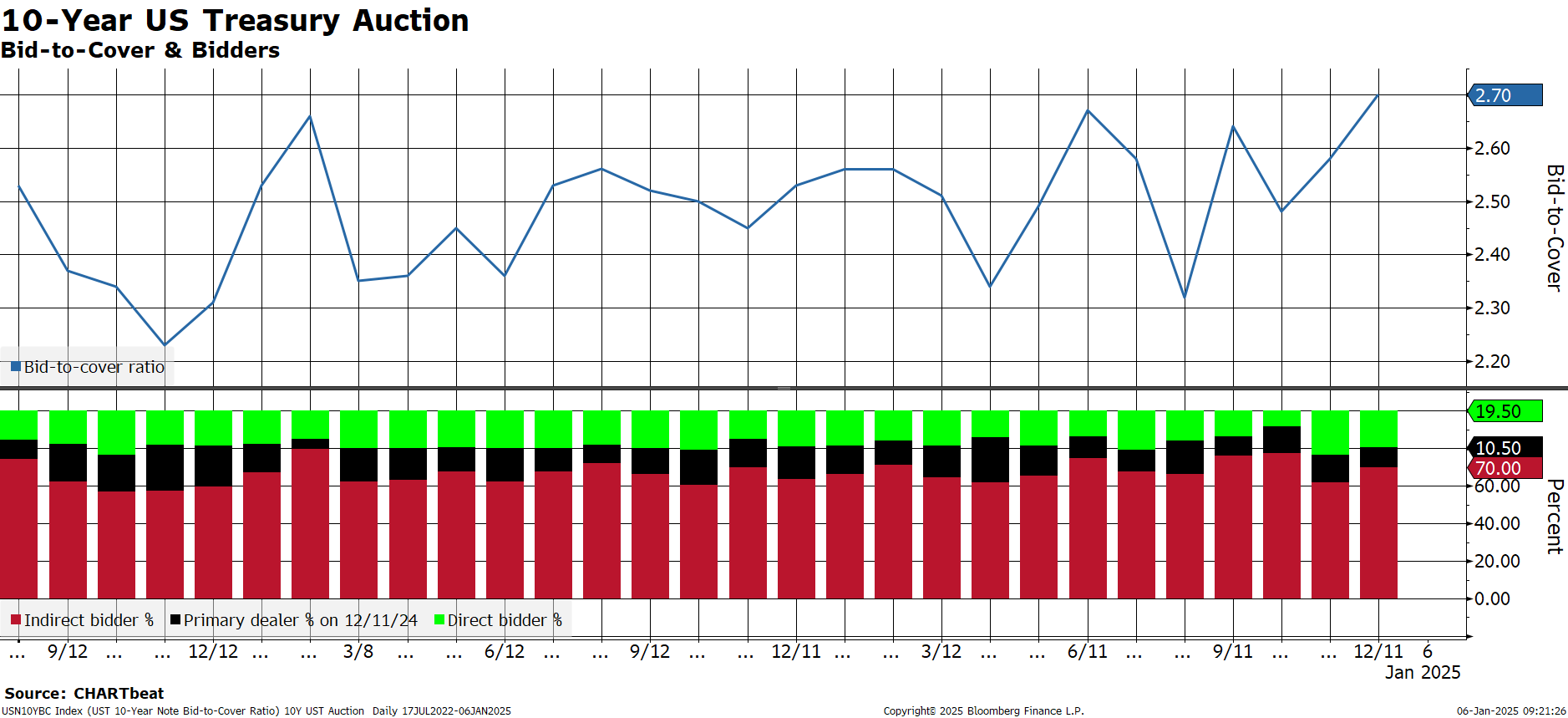

… ahead of this afternoon’s 10yr auction, best in the biz — BMO — closing thoughts excerpt caught MY eyes …

… In the wake of the data, the $39 bn 10-year auction will offer a litmus test of the demand for the benchmark following the sharp selloff over the last four weeks. Recall that last month’s 10-year auction cleared at 4.235%. This was 1.6 bp below the WI yield and non-dealers took an elevated share of the issue at 89.5%. The current outright cheapness of the 10-year sector should, all else being equal, be constructive for the takedown. In addition, when considering the recent breakout in 2s/10s to fresh, multi-year steeps, there is an enhanced relative value case for the 10-year sector compared to shorter-dated coupons. That said, even with 10-year yields convincingly back above 4.50%, the combination of deficit/issuance concerns and the uncertainty associated with Trump’s initial policy actions could lead investors to require a bit of a concession.

… with 10yr auction today once again in mind, charts from THE pre-eminent techAmentalists out there worth a look …

CITIFX TECHS: 3 charts to start the year: US 10y yields, DXY, CAD

US 10y yields have re-tested the 4.64% level. IF we break above, it would suggest higher yields, but with resistance relatively nearby at 4.74%, the move higher could be quite limited.

…US 10y yields: Testing resistance We continue to knock against resistance at 4.64% (May 29 high) after breaking above the 4.50% level in December, while breaking above the down trend seen since Dec 2023. These had all suggested higher yields, which is also what we had flagged in our prior piece.

The key question here is whether we could continue to see higher yields from here. While weekly slow stochastics is ticking higher, we are not yet convinced we could see a big move higher yet. We would need to see a weekly close above 4.64% to make a stronger case for this, however. And even if we do see a close higher, we think it would just be another ~10bps move before we find resistance again at 4.74% (2024 high).

On the other hand, support remains likely at 4.50% (psychological level, November high)

… and being early days still of the new year and, as promised, Global Wall re-energized and overflowing with output … here’s a German shop with a ‘trade update’, a 2025 outlook (where 2s TO end 4.20, 10s, 4.40 and bonds 4.85 … still interested?) and monthly chart package on the Fed …

We briefly reassess our key macro trades for the new year, starting with our bearish US duration view. We maintain our short 10Y SOFR for now but remain open to changing our view if there is any evidence that the more normative policy outcome discussed in our 2025 outlook becomes more likely. Given the recent repricing, we have moved our indicative stop higher to 4.00% and, more modestly, our indicative target up to 4.30%.

… from a positioning perspective, the FT summary of sell-side year-end outlooks, as well as Bloomberg’s compilation of sell-side 10Y forecasts, suggests that being long US duration is likely to be a consensus trade.

Macro Portfolio Update We maintain our bearish US duration trade for now but remain open to changing our view if there is any evidence that the more normative policy outcome discussed above becomes more likely. Given the recent repricing, we have moved our indicative stop higher to 4.00% and, more modestly, our indicative target up to 4.30%.

This chartbook is a compilation and update of key charts from our report "US Rates 2025 Outlook: Policy in Motion", originally published on 13-Dec-2024. Click here to open the report.

…Our fed funds forecast sits above current market pricing through H1 2026, then slightly below thereafter

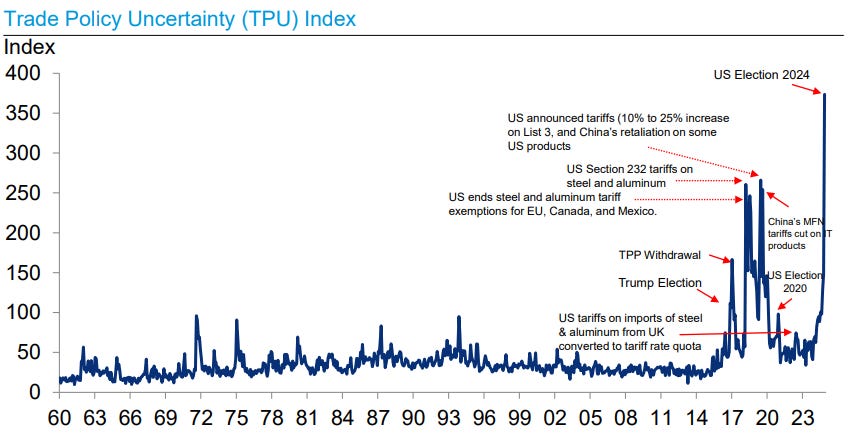

DB: US Economic Chartbook - Monthly charts: Hotter inflation leaves Fed cool on cuts

…Growth outlook: Terrific at first, tariff-ic later on…

… Easier financial conditions provide a tailwind to nearterm private demand growth

…Trade policy uncertainty has spiked higher

… on ‘pared back’ tariff report and an FX angle …

ING: The pared back US tariff report that never was

The dollar has sold off and then bounced back today on a Washington Post report that the new Trump administration may be more selective in its use of tariffs than first thought. Trump has since refuted the report, stating that its facts were wrong. As our traders say: welcome to the age of Trump 2.0

… here’s couple short notes from Switzerland ‘bout Barr resignation …

The resignation of Federal Reserve Vice-Chair Bar highlights the guardrails in protecting central bank independence. While Barr’s resignation from the supervision role might be politically inspired, Barr has not resigned as Fed governor. All seven gubernatorial positions are filled, and a vice-chair of the board of governors needs to be a member of the board of governors. The next term to end is Governor Kugler’s in 2026.

Bond and currency markets exhibited volatility yesterday on speculation about US trade taxes. The Washington Post suggested a universal tariff would only apply to certain imports. US President-elect Trump then denied the story. An unpredictable management style may create opportunities in negotiation, but market volatility also creates economic costs…

In a press release this morning, the Federal Reserve Board (FRB) announced that Michael Barr will step down from his position as Vice Chair for Supervision, effective February 28, 2025. The release also said that Barr will remain a member of the Board of Governors, implying that he will continue to serve as a Governor. Barr's term as a Governor ends January 31, 2032…

…The question of a replacement Vice Chair becomes interesting. There are currently seven members of the Board of Governors, including Barr, who according to the release intends to remain one of those seven Governors. As we detail in our deep dive, the Federal Reserve Act is clear that there are seven members of the Board of Governors: "The Board of Governors of the Federal Reserve System (hereinafter referred to as the "Board") shall be composed of seven members," also calling them "appointive members" and that the Chair and Vice Chair are to be "of the persons thus appointed." In other words, the Chair and Vice Chair are also Governors, and there is already the full allotment of seven. That means that a choice of an existing Governor could be a potential option to fill the Vice Chair role, perhaps Governor Bowman, whose portfolio at the Federal Reserve has included community banking, among other industry-related issues. She delivered a speechlast May on bank regulation…

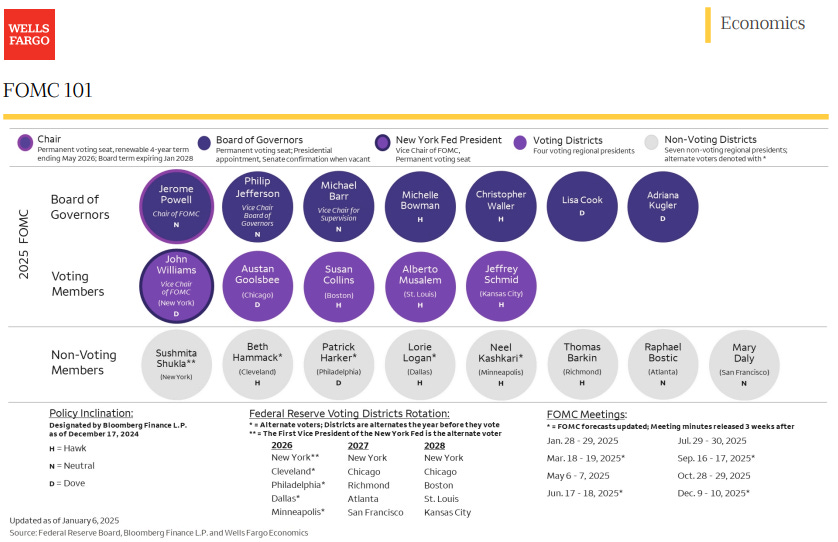

… this next note has been printed and added to my desk calendar so that when I see Fedspeak I can flip right to it and see IF whomever is saying whatever, has a seat at the adult or the kid table …

The New Year brings a new Federal Open Market Committee. For a quick reference guide, see our updated FOMC 101 tool below.

… some updated STOCKS FOR THE LONG RUN thoughts … if HEs offering cautious words, should we all start to worry …

WisdomTree: A Cautious Take on the New Year’s Market

…Valuation levels also warrant scrutiny. The S&P 500’s forward P/E ratio near 23.5x earnings is not cheap, especially as bond yields rise. If we had another 20% gain in stocks in 2025, this would harken back to the gains in 1997, 1998, and the 1999 tech bubble that caused a painful bear market starting in 2000. History reminds us that markets can sustain high valuations temporarily, but risks grow as they deviate further from earnings fundamentals. Analysts currently expect around 17-18% earnings growth in 2025. In 2023 and 2024, two very strong years for the market, we had under 10% earnings growth each year. I wonder what can drive us to these lofty expectations for earnings and that leaves us vulnerable to disappointment.

Bonds remain under pressure, driven by a strong economy, fiscal concerns, and the specter of rising deficits. Long-term Treasury yields, currently around 4.6%, may climb further, potentially reaching the high end of a 4.5-5.5% range. This forecast reflects historical norms where long bonds trade with a premium of 100-150 basis points over Fed Funds in non-recessionary conditions. Such yield dynamics heighten competition for equities, especially those relying on high growth expectations. Dividend-paying stocks, however, retain appeal as their yields remain competitive relative to inflation adjusted bonds while offering dividend growth potential that TIPs do not…

…I could see a market correction in the broad market and a bear market in the Nasdaq if our long-waited market rotation occurs, but the catalyst for this rotation has yet to arrive.

… And from the Global Wall Street inbox TO the WWW … a few curated links …

What better place to start than at THE top … one of the TOP institutional research guys having democratized research is a MUST READ … here are a couple …

The Fed has cut interest rates 100 basis points since September, and over the same period, 10-year interest rates are up 100 basis points. This is highly unusual, see charts below. Is it fiscal worries? Is it less demand from abroad? Or maybe Fed cuts were not justified? The market is telling us something, and it is very important for investors to have a view on why long rates are going up when the Fed is cutting.

Apollo: Price-to-Book Ratio for the S&P 500 at All-Time Highs

The price-to-book ratio for the S&P 500 is at record-high levels, see chart below. This is another piece of evidence that stocks are expensive at the moment.

… from what seems to be yet another ‘hit job’ on the NOT YET president, DJT, Authers OpED has section on the health of the US consumer …

Bloomberg: Markets better get used to Trump's manic Mondays

…Exceptional Consumers Nothing explains resurging US exceptionalism better than the resilience of its consumers. A year ago, a recession forecast made sense. While there have been scares, notably the triggering of the Sahm Rule — named for Bloomberg Opinion colleague Claudia Sahm — the economy still hums along, thanks in large part to the US consumer’s continuing appetite. If the optimism on Wall Street is anything to go by, exceptionalism can keep going, but that will require prolonged consumer resilience.

Ascertaining consumer health is an intense data-driven exercise with many moving parts, some of which we’ll see in action this week. Friday’s nonfarm payrolls will offer a snapshot of the labor market. The median estimate of economists surveyed by Bloomberg is a rise of 160,000 jobs, significantly down from November’s 227,000. Although recent forecasts haven’t necessarily been spot on, the deviation from the actual prints is narrowing, which suggests that the pandemic is no longer distorting predictions:

The Job Openings and Labor Turnover Survey (JOLTS), another vital data point, should be out within hours of receiving this newsletter. Data collection problems appear to threaten the reliability of this metric. Bloomberg Economics notes the survey has low response rates, which have correlated with volatility and large revisions, as shown in this chart:

Still, the economists highlight a labor market trend that shouldn’t be dismissed. The labor market is now back to almost perfect balance, with one vacancy for each unemployed worker:

After job openings declined swiftly in September and partially recovered in October, private-sector data suggest they increased in November by approximately 120,000 to 7.86 million. Despite the increase in openings, the increase in unemployment that month would bring the ratio of vacancies to unemployed workers down to 1.075 from 1.109 in October — a further loosening of the labor market that policymakers will view unfavorably.

Wall Street’s US optimism isn’t new, but the US consumer looks to be in good shape. A healthy consumer probably means good business for consumer discretionary stocks, which have indeed surged since the election — although much of that is driven by Tesla Inc. and Elon Musk’s perceived strength:

Staples were range-bound for the better part of last year, but outperformed cyclicals until Fed cuts and the election changed things in the last quarter. On balance, they’re unlikely to outperform again for a while. Torsten Slokof Apollo Global Management Inc. sees no immediate deterioration in consumers’ health. He reasons that incomes, stocks and home prices are high, debt levels and interest-rate sensitivityare low, and banks are more willing to lend to households. As he shows, consensus estimates polled by Bloomberg suggest that the Street is with him, with 2025 household spending predictions hiked several times since the election:

An analysis of consumer-spending data via the Bloomberg Second Measure suggests an uptick in some categories of discretionary-services spending — such as air transportation and accommodation — compared to a year ago.This aligns with the latest Bloomberg household consumption survey. If this week’s employment data are in line with forecasts, the story will continue to look good — and any negative surprises would be important. For now, the consumer is in a better place, and that props up US exceptionalism.

… and a stocks vs bonds hot take …

at mark_ungewitter

Intermarket study: SPX has nearly exhausted the amount of time it's been able to rally against falling TLT. A new SPX up-leg seems unlikely without the support of bond prices.

sandbox: Cash Rules Everything Around Me (Or Does It?)

…While cash in absolute terms has grown, households have shifted even more aggressively into equities, effectively underscoring the appetite for risk assets remains event stronger.

As a result, cash allocations are at/below long-term average levels while stock allocations are at all-time highs.

Inertia is the tendency for an object to resist any change in motion. What will be the catalyst to jumpstart Cash On The Sidelines?

Some of the most uncertain times – Fed rate hikes, persistent inflation spikes, disappointing earnings – are important market inflection points.

In hindsight, these events are opportune times to reallocate cash in portfolios and align them to their objectives.

Yet, with no meaningful market event currently disrupting the status quo, cash balances remain robust. AND sticky.