Good morning … Ahead of today’s JPOW testimony (see latest Monetary Policy Report noted HERE) and ahead of today’s $58bb 3yr auction …

3yy: 4.42% appears to be very familiar level dating back to LAST August and here we are with overBOUGHT momentum (stochastics, bottom panel) and in the middle ‘ish of triangulating RANGE …

… what is it YOU see … I’m not sure JPOW will be hawkish enough to cause concession BUT, if so, it may not be worst thing he could do …

… and, ahead of JPOW, at least part of the reason we’re NOT having as much ‘concession’ as one might have hoped / thought on heels of MIXED NFP is courtesy of … well … the FRBNY …

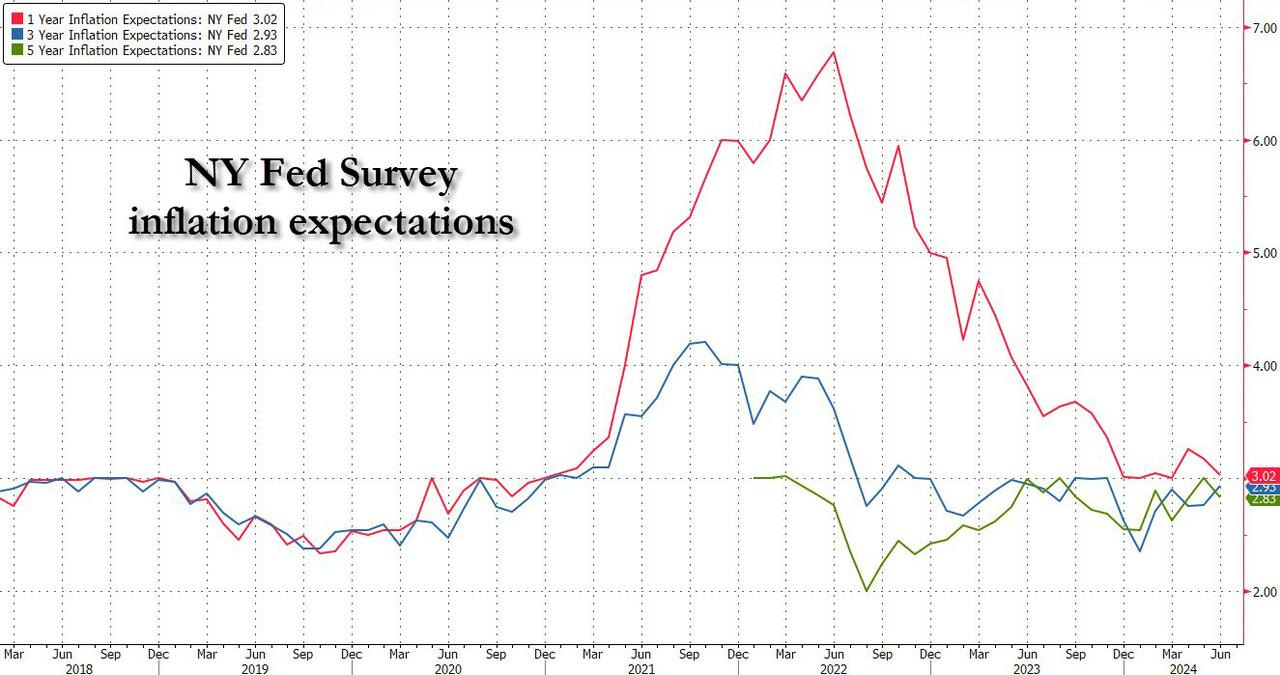

ZH: Short-Term Inflation Expectations Slide In NY Fed Survey Despite Earnings Growth Optimism (HERE is the source)

Inflation expectations at the one-year horizon dropped for the second month in a row, sliding to 3.02% in June from the previous month’s 3.17%, and from a 2024 high of 3.26% in April, according to the New York Fed’s survey of consumer expectations. At the same time, 3 year inflation expectations rose modestly to 2.93% (up from 2.76%) and the highest since Nov 23. Finally, the median five-year ahead inflation expectations also dropped to 2.83% after hitting a one-year high of 3.00% in May.

… and then there was this little bit ‘bout credit …

ZH: Credit Card Debt Unexpectedly Surges As Card APR Hits New All-Time HIgh

… and so we should all, theoretically, be on Team Rate CUT hoping for the Fed to lower the price … of money. Problem is the REASON they are likely to do so (July? see below) is because they FEAR something more ominous brewing in the economy.

At least that’s how its supposed to be and was the case in cycles past. We’ll leave well enough alone for now, anxiously awaiting JPOWs words of wisdom and the comical sound bite seaking commentary from Senate banking committee today, House finance folks tomorrow.

… here is a snapshot OF USTs as of 611a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: US equity futures firmer, DXY flat & Crude subdued ahead of Fed Chair Powell's testimony … Bonds are lower, with focus today on Fed Chair Powell and US 3yr supply … USTs are softer by only a handful of ticks as markets await Fed Chair Powell's testimony. Treasuries are currently sitting in a narrow 110-13 to 110-18 band, with support residing at 110-10, 110-04 and 109-17+.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BARCAP FOMC Minutes NLP Analysis: Weakened consensus on monetary policy

Participants' agreement about the outlook for monetary policy and the labor market diminished again in the June meeting. Even though views converged on economic trends and inflation agreement was unchanged, disagreement about monetary policy was similar to that seen amid the 2019 rate cuts.

… USD rates: Fed to cut cautiously with limited depth … Overall, we expect the Fed to lower rates by 25bp in December with 100bp of cuts next year and more reductions to follow in 2026. So while the curve should ultimately steepen with 2y yields falling as rate cuts are realized, we think they are unlikely to outperform forwards considering the Fed’s likely cautious pace.

DB: Softening labor trend supports view Fed is sufficiently restrictive (wake me up when September … nevermind …)

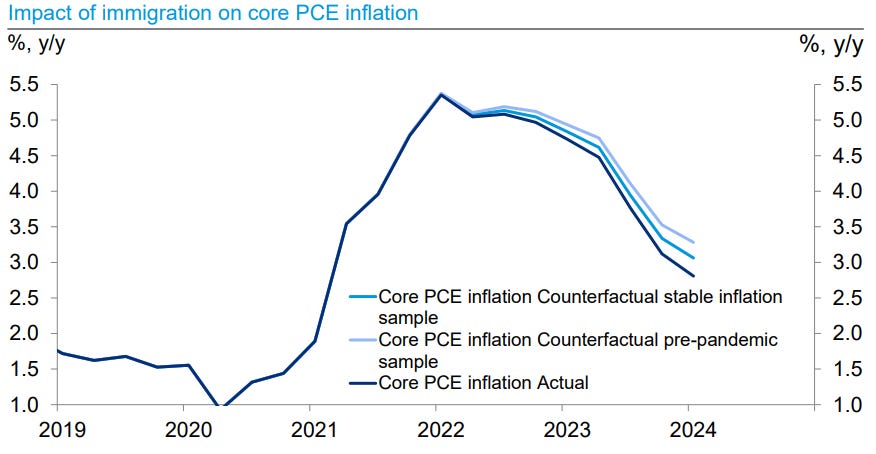

DB Monthly charts: Will inflation go quietly into the night and vanish without a fight? (hmmm interesting 1st chart i’ve spy’d)

…Uptick in immigration in recent years likely reduced inflation 25-50bps…

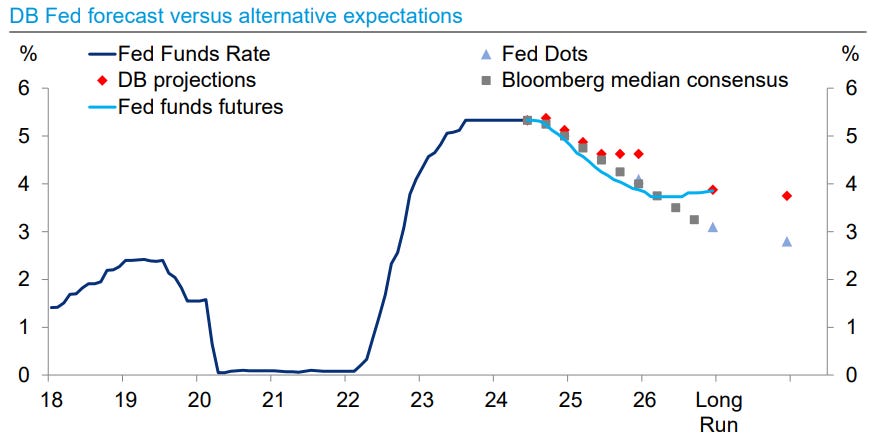

…DB Fed expectations: First cut in Dec, nominal neutral rate ~3.75%; risk of September rate cut…

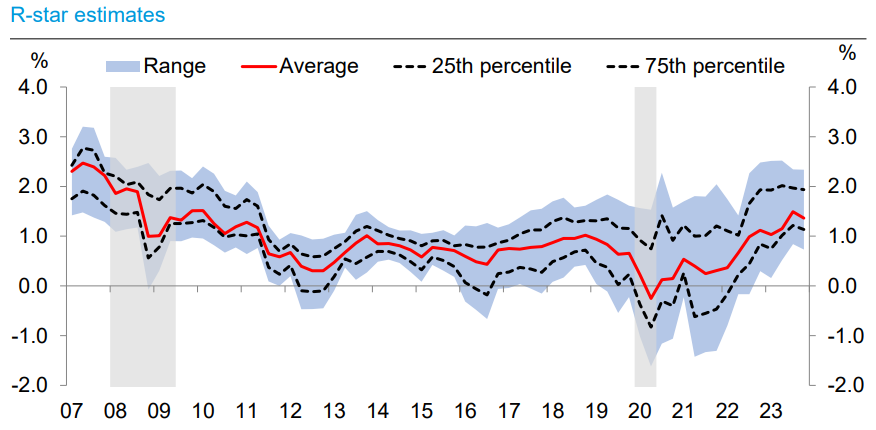

…Real monetary policy stance is reaching elevated levels from a historical perspective..

…The neutral level of the policy rate is highly uncertain but has likely risen meaningfully

DB Mapping Markets: The remarkable consistency of Q3 performance (a very LIMITED look back at Q3s — since Pandemic — but worth a look)

… What does it mean for 2024? So far at least, this pattern of a strong July has held in 2024. The S&P 500 has risen to new records, and is already up +2.06% since the start of July. Global bonds have also done well, with yields on 10yr Treasuries down around -10bps already this month…

Home prices are at record highs while pending home sales are at record lows. For-sale inventory continues to increase and might finally be contributing to a deceleration in home price appreciation. We still believe HPA finishes 2024 at +2% YoY, but slowing demand data is worth watching.

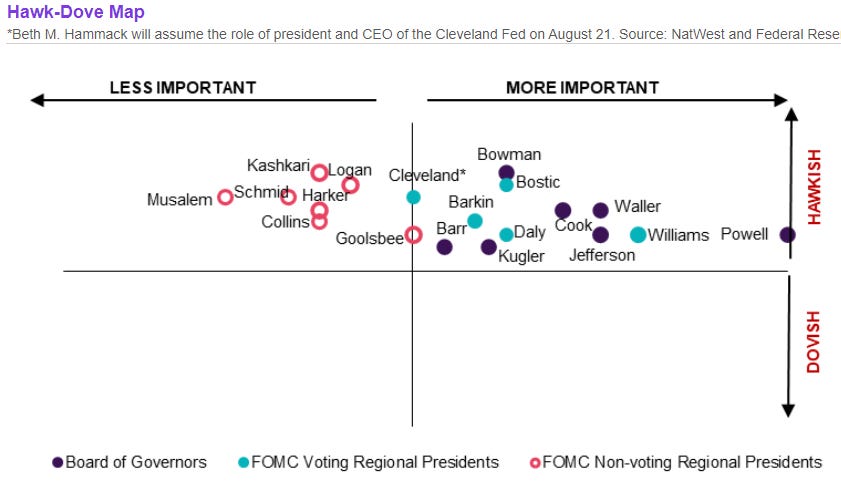

NatWEST: US: The Fed Watcher (can i get a hawk-dove map, please? is it ME or is everyone IMPORTANT and hawkish?)

Federal Reserve Chair Powell is testifying to the Senate Banking Committee today. The issue is whether Powell (who is not an economist) will be able to answer any perceptive questions that might be asked. If US inflation is lower than in Europe, why is the Fed not cutting rates? Why emphasize data dependency when data is unreliable and policy works with a lag?

The Powell Fed has become more politically sensitive—Powell has tended to focus more on issues politicians care about and less on what an independent central banker should worry about. The best to hope for today is probably recognition of some of the recent data weakness, and retaining the option of a September rate cut…

Summary Consumer price inflation likely firmed in June relative to May but remained on a downward trajectory through the month-to-month noise. We estimate headline CPI rose 0.1% in June, with a decline in gasoline prices helping keep the overall increase in prices tame. The core index also looks to have rebounded slightly. We expect core CPI to register a “high” 0.2% gain (0.24% before rounding) after posting the smallest monthly gain in three years in May (0.16%). While a bounce back in core services ex-housing is likely to propel the pickup, favorable seasonal factors and broadly easing price pressures should mitigate the extent of June's rebound.

Overall, we expect June's CPI report be consistent with inflation slowing on trend. A 0.24% increase in June would be a noticeable step down from the 0.35% average monthly pace registered in the first quarter. If realized, the three-month annualized rate of core CPI would slow to 2.8% from 4.5% in March and 3.3% in December. While additional improvement on the inflation front is likely to remain slow-going when compared to the rapid reduction registered over 2022 and 2023, we continue to expect inflation to grind lower in the months ahead as input cost pressures ease and more tepid consumer demand makes it harder to raise prices.

… And from Global Wall Street inbox TO the WWW,

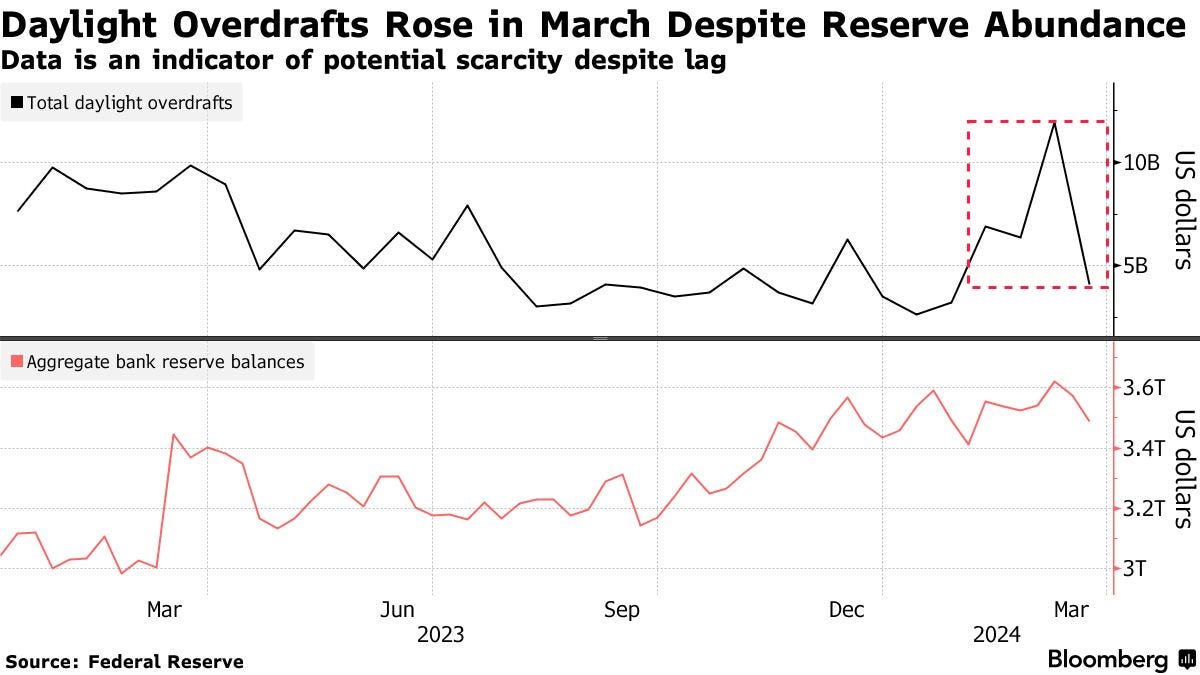

Bloomberg: Key Scarcity Indicator Flashes Warning Sign for Funding Market

Fed daylight overdraft data shows trends akin to 2019 behavior

Numbers are a ‘useful gauge’ despite time lag, Wrightson says

… The level of daylight overdrafts — when a bank withdraws more money than it has in its account at the Fed — spiked earlier this year, according to the latest data released by the central bank. That’s a signal of concern to some on Wall Street as it reflects a similar, though less-extreme, pattern to when instability hit US funding markets in September 2019.

“The level of daylight overdrafts at the Fed was an important early warning sign of potential liquidity strains in the run-up to the September 2019 repo squeeze,” Wrightson ICAP economist Lou Crandall wrote in a note. “In light of that history, we were slightly disconcerted” by recently issued data for the first quarter…

Bloomberg: Morgan Stanley’s Wilson Says a 10% Stock Market Correction Is ‘Highly Likely

US election in November and rate outlook among mounting risks

Pullback may offer opportunities, valuations ‘unexciting’ now

Bloomberg: Macron leaves France and markets in an unholy mess (Authers’ OpED and card carrying Team Rate CUT member it would appear)

… Recent economic data show that the effects of monetary policy remain potent, though there’s been a frustratingly long lag. On Wednesday, the so-called core CPI, which excludes food and energy costs and is regarded as a good measure over the forms of inflation that can be impacted by monetary policy, should add wind to the Fed’s sails toward looser monetary policy. It’s expected to have shown a rise of only 0.2% in June for a second consecutive month. That would mark the smallest back-to-back gains since August:

If the forecasts are accurate, then the pickup in inflation over the turn of the year will begin to look more like a blip, and make it far easier to predict the timing and magnitude of cuts for 2024. For now, the Bloomberg World Interest Rate Probabilities function — which projects the implicit market predictions for the fed funds rates using futures prices — is pricing in two cuts of 25 basis points each, with the first in November. This compares with the median prediction by Fed governors of a single cut on the central bank’s dot plot. For most analysts, one or two cuts could be a base scenario. While making it three by easing in July may seem overly optimistic, Academy Securities’ Peter Tchir believes that the data not only support it, but would take the spotlight off the Fed in the heat of the election campaign:

The data could easily justify a July cut, and from a political standpoint, it makes sense, but there does seem to be a risk that after getting “transitory” quite wrong, they are going to be overly cautious on cutting.

The most recent data show unemployment at its highest level since late 2021. As Points of Return laid out yesterday, it’s uncomfortably close to triggering indicators that a recession is inevitable. It reinforces growing evidence that the job market is normalizing, and reducing inflationary pressure. Add the drop in the New York Fed’s measure of consumer inflation expectations for June, an important metric for the FOMC, and there’s plenty of evidence that the Fed can begin to relax. Generally, when the expected inflation rate is lower than the unemployment rate, it’s a sign that monetary policy doesn’t need to stay too tight:

Powell acknowledges that recent data is heading in the right direction, but adds that such progress must be consistent. The bigger test is determining how much more progress the Fed needs to see. Bloomberg Economics argues that soft inflation for June, July, and August should provide the required confidence to start cutting rates by September.

As apparent as cuts may seem, the Fed is in no hurry. The scars of inflation’s re-acceleration just after the startling pivot toward easing last December are still fresh. SMBC Group’s Joseph Lavorgna believes the Fed will err on the side of caution. In his view, the first easing won’t happen until after the November election. Until then, investors parsing every possible piece of information for clues should start with Powell’s testimony.

FirstTRUST: Monday Morning Outlook - How Strong is the Labor Market?

We aren’t naturally cynical about economic data, but there are things that don’t add up about the job market…

… Putting it altogether, we think the job market is poised somewhere between the still strong picture painted by the payroll report and the soft reports on civilian employment. No recession yet, but some early signs of a slowdown.

FRED: Changes in discretionary spending during the pandemic : Data from the Visa spending momentum index

FRED recently added new data for the Visa Spending Momentum Index (SMI), which can offer new insights into US consumer spending behavior during the COVID-19 pandemic.

The FRED graph above shows two SMI data series* available between January 2014 and May 2024:

The red bars represent changes in the momentum of non-discretionary spending categories. Those include medical/health, food, and utilities—among several others.

The blue bars represent changes in the momentum of discretionary spending, which is everything else (except for spending on restaurants and gas).

The position of the bars indicates the direction of change in spending momentum: Bars above the zero line signal consumer spending was above trend, and bars below the zero line signal consumer spending was below trend. The length of the bars indicates how big those upswings and downswings were.

During March and April of 2020, discretionary spending markedly slowed down. It remained very close to its trend value for the next 12 months and surged above trend for almost a whole year afterward. Between March 2022 and the time of this writing, the Visa SMI has signaled either at-trend or below-trend discretionary consumer spending.

The June employment report officially beat consensus when it was released on Friday. However, there were a lot of other important stats from that report. First, revisions to employment in prior months were quite significant ... and to the downside. Second, the share of government jobs as a share of payrolls increased again. Lastly, the uptick in the unemployment rate to 4.1% is perhaps the biggest story. Two more months with a 0.1% uptick in the unemployment rate would trigger the famous "Sahm Rule", which would then argue that a recession is very likely. Time will tell what the future holds, but a trigger of the Sahm Rule would inevitably change the conversation at the Fed and all but guarantee rate cuts this fall.

Employment growth has consistently come in above pre-pandemic estimates of the rate needed for unemployment to stay near its long-run natural rate. Even so, unemployment has held steady, which raises the question of whether the “breakeven” employment growth rate has changed. In the short-run, recent surges in immigration and labor force participation have caused the current breakeven employment growth rate to rise as high as 230,000 jobs per month. However, the long-run breakeven employment growth rate appears unchanged, ranging around 70,000 to 90,000 jobs per month.

… Under the baseline projections, short-run breakeven growth will converge on the long-run breakeven growth rate (gray line) by the end of 2025. However, this return to the longrun trend stretches further out to 2027 for the CBO high immigration scenario.

WisdomTree: Prof. Siegel: Time for a Rate Cut? (Team Rate CUT member — prof Siegel — saying heck to the YEA)

The employment report from last Friday, in my view, was weak. Although the headline number came in slightly above expectations, the composition was troublesome, with more than 110k jobs subtracted from the last two months and private sector jobs lagging. Furthermore, the unemployment rate ticked up to a three-year high of 4.1%. Normally, I don’t make much of this, but there is empirical evidence (first presented a number of years ago by Claudia Sahm, an American economist) that when the three-month moving average of the unemployment rate rises one-half percentage point from its 12-month low, the probability of a recession jumps to over 90%. Last Friday, the moving average did just that—the actual rate has risen 0.7 percentage points from its 3.4% low hit in January 2023…

… The Fed should tee up a rate cut at the July 31 meeting for September, and in fact should contemplate a cut at the next meeting if inflation behaves and the economy continues to slip.

The market is continuing on a bull run and, with the prospects of rate cuts, I believe may continue for a while. But the narrowness of the rally is bothersome. I said at the beginning of the year, that growth is trouncing value, and that trend would continue, probably until we get a rate cut. That prediction has proven right.

… and in a few short hours, the bulls and the bears will come together like …