Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

I won’t lead with an ‘attempt to be brief’ and what follows is a collection of thoughts, links and notes as I watched the data print yesterday and markets do the best they could to incorporate said data into some sort of price action.

MY take away summed up by the word REVISIONS.

YES the headline NFP print was strong but, as the pattern has been, back months revised lower AND as this is happening, the URATE inching higher, getting folks all hot and bothered about … The SAHM RULE. More on THAT in just a bit.

I’ll lead with a look at front-end yields which are to be a raging BUY in what many continue hoping to produce THE trade of the year (2nd year running, best I reckon) — a Fed rate cut induced bullish STEEPENER. I’ll offer a couple looks at 2s and will focus more on this weeks upcoming supply (3s, 10s and 30s) next Tuesday when the liquidity provisioning process gets underway.

2yy DAILY: momentum becoming overBOUGHT as we near bottom of 20bps RANGE … Fed CUTS then this will, in hindsight, have been THE level to BUY BUY BUY …

2yy WEEKLY: momentum nearing overBOUGHT as medium term range triangulates … again, Fed CUTS will lead us all to WISH we could see 4.75% yields again to BUY BUY BUY …

And so it goes … technically closer to levels I’d be standing aside (booking profits if they were to be had and awaiting the next input — JPOW delivering Mon Pol Report (see below) and CPI — for more ‘forward guidance)…

First UP lets deal with a couple / few things items from Friday and the NFP …

NO SAHMRULE recession (YET but close?) for you BUT …

BBGs at M_McDonough (on 3m NET change and so, TREND)

3M Net Change in Non-Farm Payrolls from ECAN<GO>: The trend is clear:

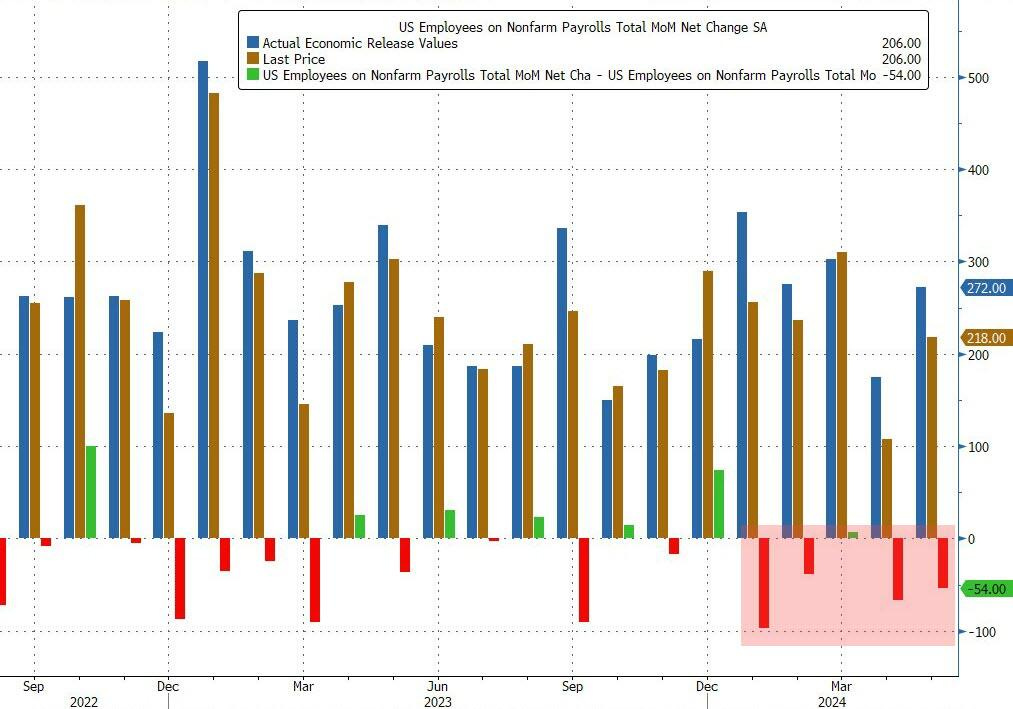

ZH: Payrolls Rise 206K After Huge Downward Revisions As Unemployment Rate Jumps To Three Year High

… Not bad, especially with Goldman expecting 140K. Of course, a quick glance reveals where the "beat" came from: both previous months were revised sharply lower:

May jobs revised from 272K, to 218K

April jobs revised from 165K to 108K

With these revisions, employment in April and May combined is 111,000 lower than previously reported. So yes, it is easy to "beat" when you have a pool of 111K jobs that never existed to push into this month. And course, next month when the June data is revised lower, the 206K beat will be revised to a sub 190K miss but by then it will be too late. And as shown in the chart below, 4 of the past 5 months have seen payrolls revised lower.

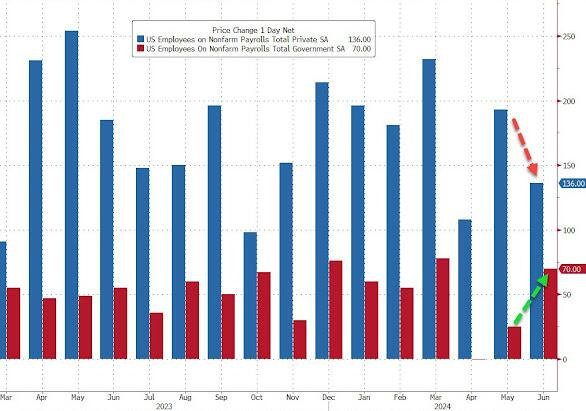

Not only that but the composition of jobs was once again dismal and followed the same gimmick the BLS used for its "strong" JOLTS report this week: private sector workers came in at 136K, well below the 160K expected and down from a downward revised 193K (was 229K). The gap was filled by - what else- deep stater and other government workers, as government payrolls jumped from 25K to 70K!

Even Steve Liesman admitted that it's all government jobs…

… And here is Seema Shah, chief global strategist at Principal Asset Management:“The equity market may be a little conflicted how to respond to today’s jobs report. On one hand, the downward revisions to prior months and the rise in the unemployment rate raises the odds of a September Fed rate cut – bond markets are certainly celebrating this. But those same figures cannot help but prompt a twinge of concern about the direction of the US economy. The broad host of economic data all point to a softening – today’s report adds to that picture.”

However, the bigger take home message here besides the timing of the next Fed cut which will come - just a matter of when - is that the Biden BLS is now clearly expecting to dump the mother of all disastrous job report realities on the Trump admin, which will come in just in time to have to revise the actual number of jobs lower by several million.

… From NFP to the Federal Reserves Monetary Policy Report out to inbox about 1115a (time stamp is 11am) and is ahead of (what used to be called the)Humphrey Hawkins testimony …

The Federal Reserve Act requires the Federal Reserve Board to submit written reports to Congress containing discussions of "the conduct of monetary policy and economic developments and prospects for the future." This report—called the Monetary Policy Report—is submitted semiannually to the Senate Committee on Banking, Housing, and Urban Affairs and to the House Committee on Financial Services, along with testimony from the Federal Reserve Board Chair.

… and with all of this in mind — trying NOT to infer too much from price action where we all know, the ‘A’ team has been ‘behind the hedges’ and / or down the shore since WEDNESDAY mid morning — by days end, the dust settling produced …

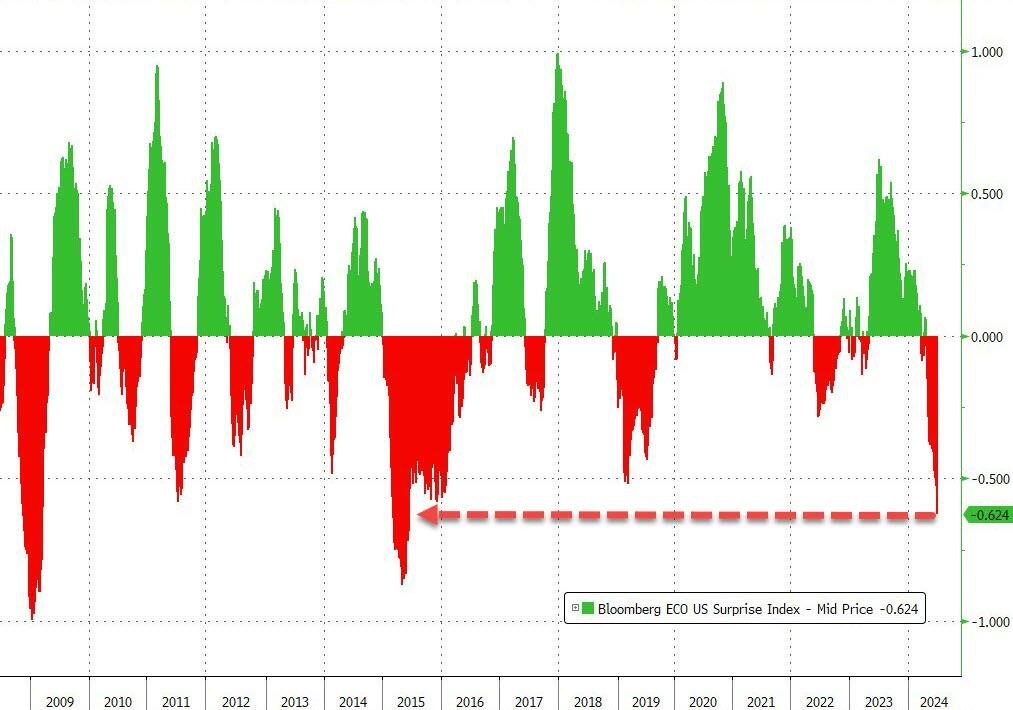

A wild (holiday-shortened and illiquid) week of dismal macro data and dramatic market divergences.

It was 100% - a bad news week...'hard landing' much?

… ..which means 'good news' for rate-cut expectations (which dovishly soared)...

… Ok I’ll move on AND TO some of what Global Wall had to say how they are sellin’ some of these NARRATIVES … here are some of THE VIEWS you might be able to use (and I’ve brought some forward from before July 4th interruption given MY view they are important / funTERtaining reads now in light of NFP details)

While headline payrolls increased 206k, private payroll growth slowed to 136k, and payroll income gains remained solid. The unemployment rate ticked up to 4.1% amid a rise in the labor force. We think labor market conditions are moderating in line with the Fed's baseline, keeping our September cut call intact.

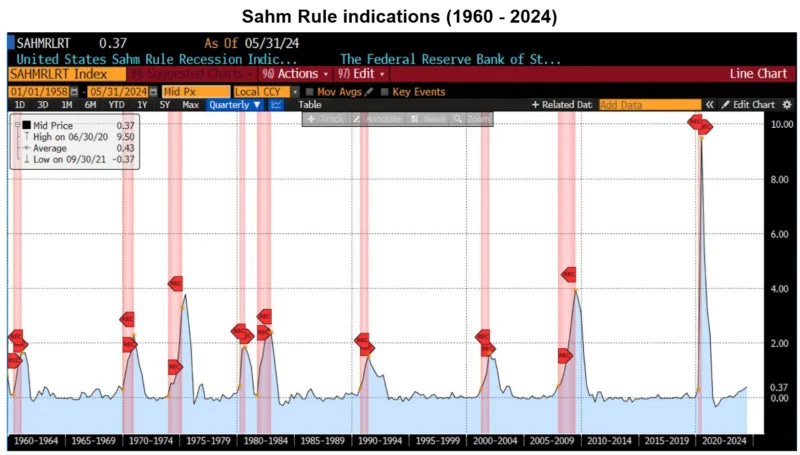

… The 3mma of the unemployment rate rose to 4.0% in June, about 0.1pp short of what would trigger the Sahm rule recession indicator (Figure 2). However, the current episode does not resemble prior instances, when it had accurately signaled that a recession is underway. In particular, those instances typically showed rapid increases in the unemployment rate, which tends to be boosted by a drop in the job finding rate and increases in the separation rate. Such nonlinear dynamics are not evident in the current episode, with the 3mma gradually ascending toward the threshold in a way that is uncharacteristic of prior downturns.

BARCAP: Taking profits on short 10y USTs (out July 2 w/10s about 10bps cheaper than yest close so another job well done)

BMO: Unemployment Rate Highest since Nov. 2021; net -111k revisions.

… Moreover, the Unemployment Rate unexpectedly increased by 0.1 pp to reach 4.1% -- this is 0.7 pp off the cycle low and surely triggering concerns that the Sahm rule will hold this year. That said, the increase in the Labor Force Participation rate of 0.1 pp to 62.6% suggests it was a constructive increase in the UNR -- if there were such a thing … Overall, it was a softer read on the labor market, albeit not dramatically weaker.

BMO Weekly: Back to the New Norm (stopped OUTTA 2s10s flattener for small loss)

BNP US June jobs report: Still within Fed’s comfort zone, but risks rise (…and as risks rise, so too does the hair on the neck of Team Rate CUT)

KEY MESSAGES

Sizable downward revisions to past US payrolls and the third consecutive increase in the unemployment rate to 4.1% at least partly offset positive news from another solid increase in payrolls.

The household survey still does not show any major pick-up in new layoffs and the increase in the unemployment rate remains within the range that Chair Powell has said was within the Federal Reserve’s comfort zone (4%+0.2pp).

The latest increase in unemployment has not triggered the Sahm rule, however, another 0.1pp rise in the next report would do the work.

… Interest rate strategy: The June nonfarm payroll report appears to support some of the signs of rebalancing and cooling evident in other labor market data such as ISM employment sub-indices and jobless claims. With a disinflationary trend seemingly back in place, focus on the activity side of the economy may be more acute relative to inflation. Markets have nearly fully priced in two 2024 25bp rate cuts and we believe that the hurdle is high to price in more than 50bp absent a materially weaker economy. Incremental evidence of continued softening, however, is likely to be reflected in increased rate cut pricing for 2025. We favored SFRZ4Z5 flatteners going into the June NFP and continue to hold the position (see US rates: Front-end asymmetry returns into payrolls, dated 28 June).

While we continue to forecast December as the month for the first rate cut, curve steepeners would be on more solid footing should the Fed cut earlier.Our historical analysis suggests that 2s10s tends to begin secular steepening within three months of the first rate cut, but remain more rangebound when cuts are further out. Therefore, we favor remaining tactical in 2s10s steepeners or in positive carry, limited downside range-bound expressions. We view 5s30s steepeners a bit more favorably as we would expect the 5y to perform well in an environment where more cuts are priced into 2025 while deficit concerns are back in focus for the long end of the curve.

We expect US core CPI to rise by 0.2% m/m for the second straight month in June, providing further evidence that prices are returning to a disinflationary trend following a stronger-than-expected Q1.

Risks seem modestly tilted to the upside (we see a 50% chance of a 0.2% print, versus 30% of 0.3% and 20% of 0.1%) with particular uncertainty around auto insurance.

We think core PCE inflation remains on track to print in line with the Fed’s June FOMC median forecast of 2.8% q4/q4, even after May’s weaker-than-expected data. Another downside surprise in June would likely push our tracking lower and put a September rate cut in play.

DB: June jobs report: Cooling labor market heats up prospects for September cut

Although job gains remained sturdy in June – headline payrolls expanded 206k – the overall labor report leaned weaker. Total payrolls over the prior two months were revised lower by 111k and private payrolls expanded by only 136k. The unemployment rate continued its slow and steady march higher, rising to 4.1%. Although the unemployment rate is now 0.7 percentage points above the low set in January and April 2023, this rise did not trigger the Sahm rule which uses three-month moving averages to capture the trend in unemployment rather than month-to-month fluctuations.

Partially offsetting some of this weakness was the fact that the unemployment rate barely rounded higher (it was 4.05% unrounded). Its rise also reflected a one-tenth increase in labor force participation, with the prime-age (25-54 age group) participation rate hitting 83.7%, its highest since 2001. Further encouraging details can be found in stable income gains from the payroll proxy (5.1% year-over-year), the rise in the diffusion index of job gains to its highest reading since January, and a decline in those unemployed because they lost their job, with permanent job losers falling to the lowest since January. Notably, the largest contributing factor to higher unemployment was a pickup in new entrants to the labor force, which hit its highest level since 2017.

For the Fed, the softer elements of this report do not rise to the “unexpected weakening” Chair Powell has highlighted as triggering rate cuts. That said, the June jobs report adds to evidence from other recent growth indicators that the Fed is likely sufficiently restrictive. These data therefore boost prospects for a September rate cut, though that outcome requires continued evidence of moderating inflation over the coming months. As a reminder, our base case is that the Fed cuts rates just once this year in December, but a September reduction is clearly on the table (see “(Pushed) Back to December”).

… Revisions to nonfarm payrolls have been broadly negative

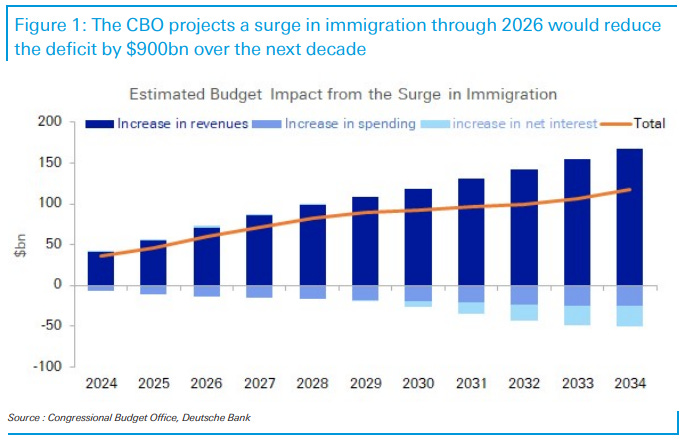

DB: Trump's immigration policy agenda and interest rates (hmmm interesting one here)

… According to CBO estimates, the immigration surge would reduce the federal deficit by $900bn over the next decade. The main source of deficit reduction comes from higher individual income and payroll taxes, with increased economic activity also boosting tax revenues from other sources.

The CBO also argues for higher interest rates over the next decade due to immigration, driven by increases in the labor force and productivity growth, as well as greater demand for residential investment. Further into the future, the impact of an improved debt-to-GDP ratio becomes more dominant, leading to lower interest rates than otherwise. This suggests that a policy shift to significantly limit immigration could lower medium-term rates while raising long-term rates through increased term premium…

Our measure of aggregate equity positioning moved largely sideways this week at elevated levels (z score 0.80, 93rd percentile) as discretionary investor positioning declined modestly (z score 0.90, 93rd percentile) but that for systematic strategies rose to the highest since Feb 2020 (z score 0.84, 88th percentile). Across our measures of absolute sector positioning, that for MCG & Tech continued to ascend and is close to the top of its historical band. Fund inflows were strong across asset classes this week. Inflows to equity funds ($10.9bn) picked up on the back of solid inflows to the US ($7.0bn). Across sectors, Tech ($1.8bn) and Financials ($0.8bn) got notable inflows. Inflows to bond funds ($19.0bn) spiked to the highest in over 3 years and were broad based across categories. Money Market funds ($51.9bn) also received strong inflows.

Equity positioning went sideways this week and remains elevated

Payrolls gains of 206k with 111k in downward revisions the past 2 months show a slowing labor market. More weakness in the household survey pushed the unemployment rate higher. Earnings are moderating. The labor market is coming into better balance and we expect three cuts this year starting in Sep.

MS US Retail Sales Tracker: Under Pressure (Team Rate CUT!!)

We forecast control retail sales fell 0.3%M in June. Softer payrolls, goods deflation, and decline in auto sales, likely impacted by the cyber attack, will weigh on sales. Headline to decline by a greater 0.5%M. Data in line with our forecasts lower the 2Q24 real PCE tracking 30bp to 1.4%.

MS US Economics: CPI Preview: More Disinflation Evidence (picture is NOT that compelling as title but…)

We see core CPI inflation at 0.27%M in June (0.2%M cons, 3.5%Y). Data in line with our expectation points to June core PCE at 0.23%M up from 0.08%M in May, but still the second lowest print of the year. We expect headline CPI at 0.13%M due to negative energy inflation (3.2%Y, NSA Index: 314.823).

…Bottom line: June brought another robust payroll gain in the U.S. but according to the meeting minutes, FOMC participants have begun to question if job gains in the establishment survey have been overstated with the separately calculated unemployment rate continuing to rise. Jobless claims have been broadly edging higher in recent weeks and survey data has also pointed to rising uneasiness with employment situation among consumers in the U.S. Overall, the slowdown in labour market conditions is evident but slow, just as the progress with easing inflation. That means the Fed will need more time and more data before committing to lowering interest rates. We think won’t come until December.

Wells Fargo: June Employment: From Sizzle to Fizzle

Summary Nonfarm payrolls gains were solid in June, rising 206K, but the underlying details of today's employment report clearly signal that the U.S. labor market is softening. June job growth topped consensus forecasts by 16K, but this was more than offset by 111K of downward revisions to job growth in April and May. The composition of job growth continues to be led by sectors that are less cyclically sensitive. Nearly 75% of June's employment growth could be attributed to government (+70K) and health care & social assistance (+82K). The separate household survey also showed a cooling labor market. The unemployment rate once again ticked higher to 4.1%, above both its post-pandemic low (3.4% in April 2023) and its pre-pandemic average (3.7% in 2019).

The cooling in the labor market extends beyond just the data released in the monthly employment report. The number of job openings per unemployed person is back to its pre-pandemic level, while the share of workers quitting their jobs and small business hiring plans are below pre-pandemic averages. Wage growth remains a bit elevated compared to 2019, but we believe this indicator will continue to slow with a lag. The slower inflation data over the past couple months, when paired with the softening labor market, bolster the case for the FOMC to begin reducing the fed funds rate as early as its September 18 meeting. Our forecast remains for two 25 bps rate cuts this year at the September and December FOMC meetings.

Source: U.S. Department of Labor and Wells Fargo Economics

… The unemployment rate vacillates little when the economy is in an expansion, which makes an upturn in it notable as momentum in the labor market can be difficult to change once established. The recent increase has not triggered the widely watched Sahm rule (chart), which finds that the economy is in a recession if the three-month average of the unemployment rate is 0.5 points above its low of the past the 12 months. Yet it underscores a marked deterioration in labor conditions that is not reflected in the payroll survey.

More temperate wage gains are following in the wake of the softer jobs market conditions (chart). Average hourly earnings advanced 0.3% in June, driving the year-over-year gain to a three-year low of 3.9%. That still keeps average hourly earnings outpacing inflation over the past year. However, the moderation in hiring alongside nominal wage growth points to aggregate income derived from the labor market slowing more sharply, which is likely to keep downward pressure on overall consumer spending and inflation.

… Topic of the Week: Because I Was Inverted Charlie: So, lieutenant, where exactly were you?

Maverick: Started up on his six, when he pulled in through the clouds, and then I moved in above him.

Charlie: Well, if you were directly above him, how could you see him?

Maverick: Because I was inverted.

Two years ago today, the yield on the 10-year Treasury note fell below the yield on the two-year note. The yield curve has remained inverted since, marking the longest period in U.S. history in which the 2s-10s has been inverted and the economy has not slipped into recession. An inverted yield curve is often thought of as a recession predictor. There have been six recessionary episodes in the U.S. economy since 1978, and each one has been preceded by the inversion of the yield curve, however brief (chart). Yet, the yield curve has now been inverted for two years, with a recession yet to follow. Is this time really different?

When the yield curve first inverted in the summer of 2022, economic conditions were strained. In March, the Federal Reserve kicked off the soon-to-be fastest rate hike cycle in decades, bumping the federal funds target range to 0.50% from 0.25%. By June, headline inflation had peaked at 9.1% year-over-year, and the Federal Open Market Committee (FOMC) had enacted a surprise tightening of 75 bps. By the end of the year, the target range had reached 4.50% with more tightening expected, and headline inflation had only cooled to 6.5% year-over-year. At this point, most economists forecasted a recession in 2023, with the expectation that higher inflation would erode real income and high interest rates would weigh on interest rate-sensitive spending and push the economy into contraction. According to a Bloomberg survey of economists, the U.S. recession probability forecast peaked at 65% by year-end 2022, up from 15% in January of that year (chart).

Today, while recession probability has come off its highs, market participants are still anticipating the Fed to begin its rate-cutting cycle as inflation has come closer to target. The economy has remained surprisingly resilient in the current high-interest rate environment, and as a result, the FOMC has remained on hold at 5.50% as it waits for the lagged effects of monetary tightening to bite harder and push inflation on a sustained trajectory back toward its 2% target.

We continue to anticipate that the FOMC will begin reducing the federal funds rate before the year is out. Our base case looks for two 25 bps rate cuts—one each in September and December—although it will be a close call between one or two cuts this year. As the FOMC eases rates, we expect the spread between the 10-year and two-year Treasury notes to narrow before returning to the green in Q1-2025. Until then, the yield curve will remain like Maverick: inverted. (Return to Summary)

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

…This uptick triggers the Sahm Rule, a real-time recession indicator, suggesting that the US economy is in, or is nearing, a recession. The Sahm Rule, developed by former Fed economist Claudia Sahm, is designed to identify the start of a recession using changes in the total unemployment rate. According to the rule, a recession is underway if the three-month moving average of the national unemployment rate rises by 0.50 percentage points or more, relative to its low during the previous 12 months. With the June 2024 U-3 rate of 4.1 percent, the average of the last three months being 4.0 and the lowest 12-month rate of 3.5 percent in July 2023, this criterion has been met.

Sahm Rule indications (1960 – 2024)

AllStarCHARTS: Global Yields Soar – Just Don’t Tell Tech Stocks (where, ‘global yields SOARING are JGBs … i know it’s important but … i dunno … clickbait??)

Apollo: Daily TSA Travel Data Still Strong (Team Rate Cut will discount this one)

The TSA has daily data for the number of people scanning their boarding pass with a TSA agent, and it continues to show no signs of the economy slowing down, see chart below.

Crescat(for better or worse, being without a Terminal, I can appreciate interesting / funTERtaining visuals despite the source!)

This week, economic surprises have plunged to nearly decade-low levels, while last week, inflation expectations surged to their highest in over three decades. This spells stagflation loud and clear. The Fed’s dual mandate of managing inflation and labor market stability is poised to shift toward financial repression to ensure the government can service its debt. Ultimately, that is what sets the stage for a supercharged environment for real assets to outperform.

Fed in Print: Exploring the TIPS‑Treasury Valuation Puzzle

Abstract: Since the late 1990s, the U.S. Treasury has issued debt in two main forms: nominal bonds, which provide fixed-cash scheduled payments, and Treasury Inflation Protected Securities—or TIPS—which provide the holder with inflation-protected payments that rise with U.S. inflation. At the heart of their relative valuation lie market participants’ expectations of future inflation, an object of interest for academics, policymakers, and investors alike. After briefly reviewing the theoretical and empirical links between TIPS and Treasury yields, this post, based on a recent research paper, explores whether market perceptions of U.S. sovereign credit risk can help explain the relative valuation of these financial instruments.

ING: Cooling US jobs market keeps September rate cut in play (Team Rate CUT!!)

Jobs growth is cooling, particularly in the private sector and the unemployment rate has now broken above 4%, which is helping to keep wages in check. With inflation also looking better behaved the chances of a September interest rate cut from the Federal Reserve continues to build

A brief review of all key upcoming events across the major regions of the globe & an overview of key recent market trends.

The State of Markets: A Goldilocks Market For Equities? Evidence for a slowdown in the US economy continued to build this week. In particular, Monday’s ISM manufacturing print was disappointing; Wednesday’s ADP employment and ISM services were both weaker than expected; and, while headline payrolls beat expectations yesterday (by 16k), there were significant downward revisions in May (-54k) and April (-57k). With that, the unemployment rate was higher than expected (4.1% vs. 4.0%).

Unsurprisingly, therefore, US yields moved lower across the curve (e.g. with US 10 year yields down 20bps since Monday’s close, see chart below). As such, and with the dollar lower (DXY: 0.94% last week), US equities performed well (especially the tech/growth heavy parts of the market). Most notably, both the S&P500 and NASDAQ100 broke out of their recent trading ranges and made new record highs.

The key question, therefore, is whether next week’s CPI release will add to that emerging theme (i.e. of weaker growth and inflation – and therefore expectations of looser Fed policy). All eyes will be on that CPI data (due Thursday at 1:30pm London time). Other key US data points will include NFIB small business optimism (Monday) as well as PPI inflation and the University of Michigan Sentiment (both on Friday). Elsewhere Powell will be giving his (second) semi-annual testimony to Congress (on Monday & Wednesday). Tomorrow is the second round of French elections and earnings season gets going this week (please see below for a full list of key data, events, and earnings reports).

Fig A: US 10 year Treasury yield (%), shown with 50, 90, & 200 day moving averages

However, this is down from 218,000 in May. The three-month moving average is at a low 177,000.

… The cooling demand for labor has come with a cooling pace of wage growth. Average hourly earnings were up 3.9% from the previous year, the lowest rate since June 2021.

Wage growth continues to cool. (Source: BLS via FRED)

“The trend is clear: the labor market is cooling off,” Indeed Hiring Lab’s Nick Bunker said. “The question is whether the recent run of data is simply a continuation of the relatively painless moderation of the past few years or the beginning of something more damaging. The labor market chugging along for now, but evidence is mounting that iif it continues to slow down, it could stall.” …

WolfST: Job Growth Back to Normal Pre-Covid Pace, Wage Growth Still Higher: Longer-Term Employment Trends by Industry

Huge undercount of immigrants since 2022 messes up employment data in the household survey. Census Bureau needs to adopt Congressional Budget Office’s population estimates or go home.

… Bottom Line We still have the drama unfolding in D.C., which we think warrants hedging against geopolitical risk (Don’t Assume) and lots of questions about valuations and breadth, but we can see an initial “goldilocks” type of reaction to the data.

Treasury yields should do ok, as both the obvious and not so obvious aspects of this report support the Fed and lower yields. Having said that, we are near the lower bound of 4.3% on our 4.3% to 4.5% range, so trimming exposure here makes sense. The one thing that seems consistent in D.C. is that no one cares seriously about closing the deficit to do anything about it and that should weigh on the longer end of the yield curve.

Equities could continue their bounce by cherry picking the good aspects of the report, and building on the momentum that has driven the Nasdaq 100 higher by 2.5% in this holiday shortened week. With trading volume expected to be very light today, that could continue. But, and this remains a big but, the risk that the data is deemed to be negative for the economy, such that it hurts equities is increasing, and we think vigilance on the geopolitical front is well warranted.

Credit. Rangebound rates and a decent (even moderately slowing economy) shouldn’t pose a threat to credit spreads. Supply should ease, and there is fierce competition amongst lenders, for all but the weakest companies. Credit should remain boring, and generally continue to tighten over the summer.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Is that air brushing or embalming liquid percolating within the Brandon there?

That was Awesome & Exhaustive, where do you find the time? Hunkered down w/my fans & low energy window ac (MUCH cheaper than HVAC!) only a toasty 112 currently outside, had to do pre-dawn yardwork & repairs, thanks for the entertainment & knowledge between soccer matches today!

Be interesting how much Team Rate Cutlets likes their medicine once they get it :)!

Is that air brushing or embalming liquid percolating within the Brandon there?

That was Awesome & Exhaustive, where do you find the time? Hunkered down w/my fans & low energy window ac (MUCH cheaper than HVAC!) only a toasty 112 currently outside, had to do pre-dawn yardwork & repairs, thanks for the entertainment & knowledge between soccer matches today!