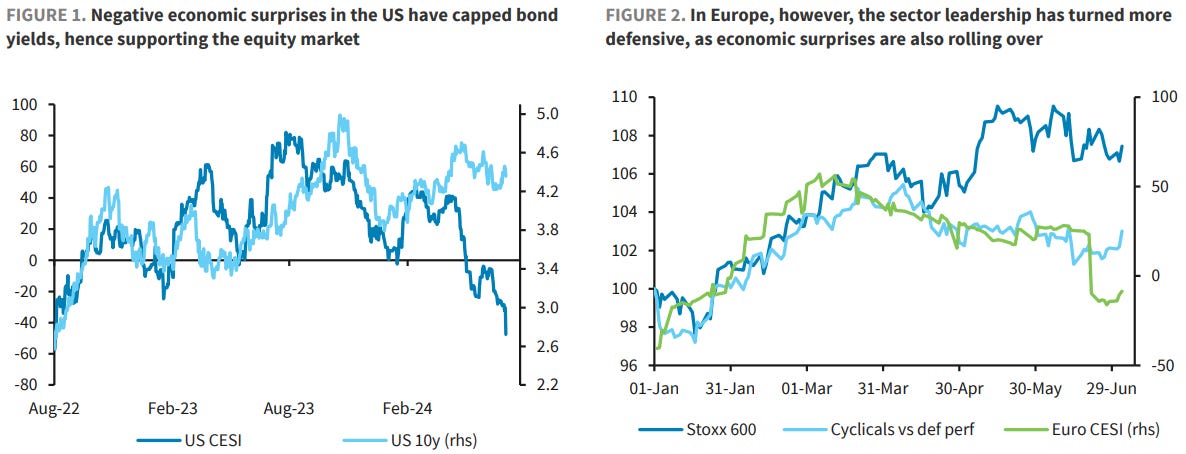

Good morning … A short note before the all-important NFP report up in couple hours AND just a few words in addition TO what I noted HERE yesterday … Yesterday I had a couple visuals of long bond futures as futures were open for biz, as usual and today the entire market is open for biz AND for an entire session.

Interesting setup as the ‘A’ team will be remaining on holiday (Hamptons hedge put into effect Wed morning shortly after last data point) and I’ll not labor the point as I’m clearly (and barely even) on the other team. Before I head out, a quick look at the belly …

5yy WEEKLY where momentum is overBOUGHT and daily, inset (overbought, too but less so)

… Clearly today will be impacted by NFP print and the algos / ‘B’ team who are ‘here’ to manage … and given summer holiday time in full swing, am not quite sure if the report will elicit a response from Global Wall but if it does, I’ll have some comment on it over the weekend … for NOW, all eyes on … a couple things ahead of NFP.

First, Williams speech in India

FRBNY: Managing the Known Unknowns (concluding sentences brought forward … but the idea here is that they’ve made progress ON ‘flation BUT reads to me as very clear to him the job is not yet done)

… Uncertainty in the Years Ahead I have talked about how the key tenets of inflation targeting—ownership of price stability and independence of action, transparency about goals and strategy, and a focus on anchored inflation expectations—have served us well in managing the extreme shocks and uncertainty of the past four and a half years. But uncertainty does not only dwell in the past.

Despite the very best efforts of economists and others to understand how the economic environment is changing and what it means for monetary policy, we must accept that uncertainty will continue to define the future. These principles and lessons provide a strong foundation for monetary policy that is robust to uncertainty. And I am confident they will continue to serve us well against any challenges and uncertainties we may face ahead.

… AND from the official words to the unofficial key take from today’s NFP … the URATE and specifically in the SAHM RULE context …

NEWSQUAWK: US Market Open: DXY slips as GBP & EUR lift, NFP looms … Fixed benchmarks generally firmer but only modestly so, EGBs unreactive to data and German fiscal updates … USTs a touch firmer with the US yield curve mixed but slightly steeper into Payrolls.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

ABNAmro: US - Schrödinger’s excess savings | Insights newsletter

Pandemic induced excess savings have not been depleted. Depending on where you look, excess savings were either never there (low income households), or still there (high income households). Middle income households obtained and depleted excess savings. Depletion of excess savings coincides with normalization of consumption and the rise in credit card and car payment defaults. Remaining excess savings in upper tail of income distribution unlikely to boost consumption.

BARCAP: Equity Market Review - Goldilocks and the Three Elections

'Bad is good' and contained political angst have preserved the goldilocks narrative for equities. In UK, a large Labour majority clears up the outlook and could boost the bid for domestic stocks. In France, a hung parliament may prompt more dip buying, but uncertainty won't all go away. In the US, the Trump trade is back on.

The UK general election result is now clear (for the benefit of US readers, many countries are able to get a definitive result within hours of voting having concluded). The result was entirely as expected by markets, with the Labour Party winning a sizable majority. Former Prime Minister Truss (who presided over the Truss debacle in markets) lost her seat.

Two larger points from the UK vote: the UK has generally avoided the prejudice politics that has emerged elsewhere (and which will be visible in France in the weekend’s elections); it also appears that the Israel-Hamas war impacted votes. In a world of social media, international events may seem more local, and have a bearing on elections that they have not traditionally had.

The US employment report is likely to continue to give mixed signals on the US labor market. Remember that over half the companies asked for payrolls numbers do not give any response. While the fear of unemployment seems contained, the broader picture hints at some labor market cooling.

ECB President Lagarde speaks again, updating markets with just how much has changed since she last spoke. On Wednesday. US President Biden is giving a television interview, but markets are not likely to react to this specifically.

US payroll numbers have continuously surprised expectations to the upside, yet soft data keeps pointing at a weakening labour market. A consensus reading or lower would help build a Fed cutting narrative for September, helping both US and euro rates to fall. The French election outcome is unlikely to stir markets as tail risks have faded

AND on JOBS, no matter WHAT the print Global Wall be like…

… AND AND … if this guy were runnin’ HERE in the USofA, Rick Astley likely would have MY vote cuz …

… inspired BY this morning’s OpED by John Authers and … THAT is all for now — perhaps something more over the weekend but for now, I’m off to the day job…

I remember this song.........

FUN TIMES !!!!!

https://youtu.be/lYBUbBu4W08