Good morning … and happy original BREXIT day to all who celebrate!

I’ll begin with an attempted look long bond futures (ZB1 via TradingView) …

ZB1 DAILY: momentum overSOLD, prices bouncing from triangulating support

ZB1 WEEKLY: range rules here to BUT momentum on slightly longer term look, is more BULLISH (supportive of dip buying) and in to the week ahead, where we’ll get 3s, 10s and bonds, perhaps a better level straight ahead? NFP to decide?

And with this limited look in at bond markets / futures which appear to be open, I’ll offer a quick review of yesterday and spare any attempted look ahead TO tomorrows NFP.

IF there are any post data, weekly writeups of interest, I’ll organize and send along something over the weekend … For now, lets tackle some MATH …

Bad = good … pre 4th July math with a HEAVY dose of ‘I dunno’ who / what to believe at moment. Said another way, see whatever you wanna see and join which ever team (Rate CUT of the other guys) you wish …

CalculatedRISK: ADP: Private Employment Increased 150,000 in June

ZH: ADP Payrolls Disappoint In June - 3rd Straight Monthly Decline In Additions

ZH: Construction Industry Suffers Largest Layoffs 'Since Lehman' As Initial Jobless Claims Disappoint (Again)

ZH: WTF Are S&P Global Services PMI Respondents Drinking?

… but the BEST ‘bad’ news of the day, of course, surrounding Biden potentially bowing OUT (and so, very same coin flipped other day when Trump looked to be IN and so, BEARISH for bonds … Wednesday it was then bullish? I noted earlier how moves (either direction) ahead of 4th were / are useless and I’ll stick with that but …

ZH: Stocks, Bonds, & Bullion Soar Amid Political Panic & Macro Meltdown On Holiday-Shortened Day

… but wait, there was MORE as markets officially and fully closed for the DAY (not the week as we’ll all be back here Friday for payrolls, right)…

ZH: FOMC Minutes Show "Vast Majority" Expect Economy To Cool, See Deflationary Effects Of AI

… and for some MORE of the news you might be able to use…

NEWSQUAWK: Europe Market Open: APAC followed suit to the Wall St. gains into Independence Day … Fed Minutes stated that most saw the current policy stance as restrictive and several participants said if inflation were to persist at an elevated level or rise further, the Fed Funds Rate might need to be raised, while a number of participants said that policy should stand ready to respond to unexpected economic weakness … WSJ's Timiraos posted on X that while there isn't an obvious signal about the policy path in the FOMC minutes, the discussion about inflation and labour market developments provides little to suggest fear of overheating or policy being too loose.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ after ADP and FOMC minutes and just ahead of tomorrows NFP …

ABNAmro: Global industry still expanding, despite disturbances

Global manufacturing PMI drops marginally in June, remaining in expansion territory. Outperformance emerging economies continues. Excess supply conditions continue. Container tariffs keep rising, pick-up in industrial input/output prices more moderate so far.

Stock Valuation Improves Our stock/bond asset-allocation model, which we call the Stock Bond Barometer, is indicating that bonds are the asset class offering the most value at the current market juncture. But not by much. The model takes into account current levels and forecasts of short-term and long-term government and corporate fixed-income yields, inflation, stock prices, GDP, and corporate earnings, among other factors. The output is expressed in terms of standard deviations to the mean, or sigma. The mean reading from the model, going back to 1960, is a modest premium for stocks of 0.16 sigma, with a standard deviation of 0.97. In other words, stocks normally sell for a slight premium valuation. And that's where we are today. The current valuation level is a 0.19 sigma premium for stocks, just above the historical average but well within the normal range -- and down from a 0.34 sigma premium last month. Other valuation measures also show reasonable multiples for stocks. The current forward P/E ratio for the S&P 500 is approximately 20, which is within the normal range of 13-24. The current S&P 500 dividend yield of 1.3% is below the historical average of 2.9%, but is 29% of the 10-year Treasury bond yield, compared to the long-run average of 39% and the all-time low of 18% in 1999. Further, the gap between the S&P 500 earnings yield and the benchmark 10-year government bond yield is about 320 basis points, compared to the historical average of 400. Lastly, the ratio of the S&P 500 price to an ounce of gold is now 2.3, within the historical range of 1-to-3. We expect the results from our stock/bond valuation model to tilt more toward stocks, as interest rates head lower in 2024 and EPS growth picks up. Based in part on the output from our Stock Bond Barometer, our recommended asset allocation for growth accounts is 70% growth assets and 30% fixed income.

BARCAP: Taking profits on short 10y USTs (out July 2 w/10s about 10bps cheaper than yest close so another job well done)

We are turning neutral on our recommendation to be short 10y USTs. While the consensus remains pessimistic about the economy, yield levels are not as mispriced and event risks, both political and economic, reduce risk-reward in remaining short duration.

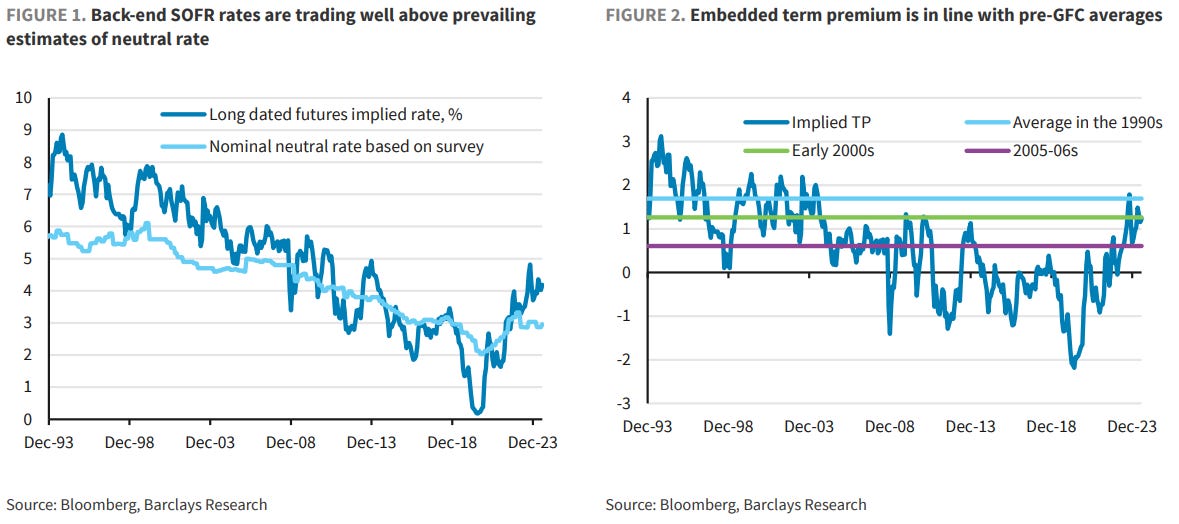

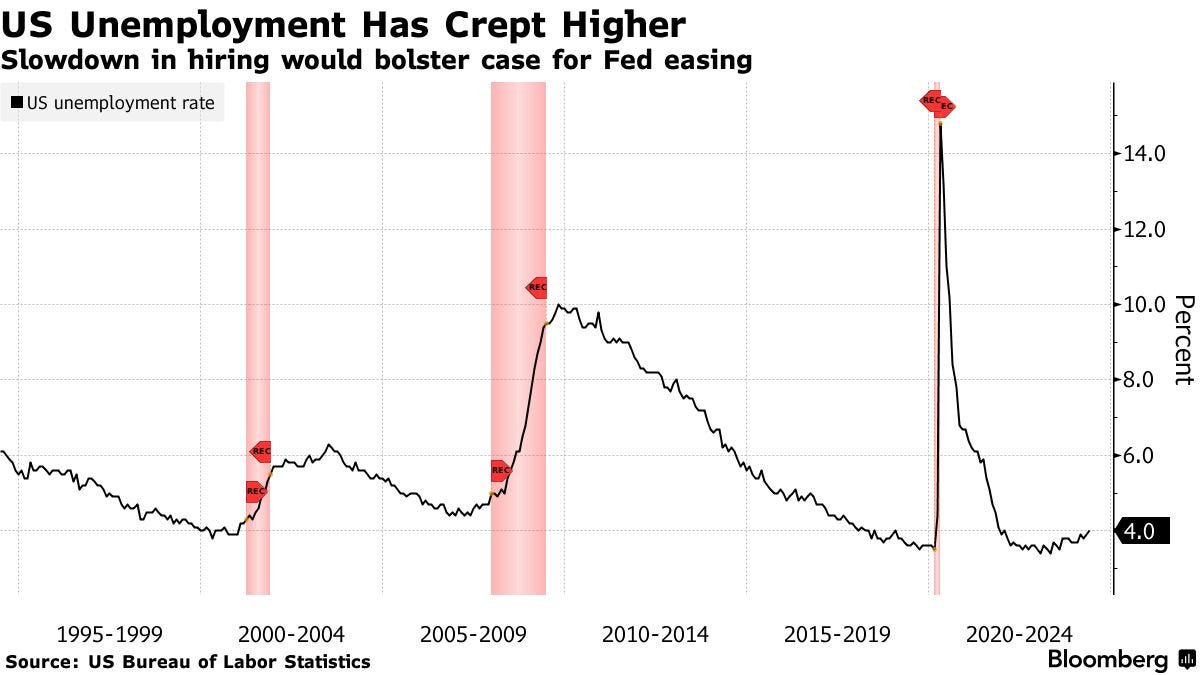

… Key things to note First, yield levels are not as mispriced. Figure 1 shows back-end SOFR rates (7yf) against prevailing estimates of the long-run neutral rate. At 4.25%, they are trading at about a 125bp spread to survey-based estimates of a 3% long-run neutral rate. That reflects a healthy term premium, in our view. Figure 2 shows that it is line with pre-GFC averages. If we assume that the fed funds rate will be gradually lowered to 3% over time, the expectations component in 10y USTs would be 3.4-3.5%, rendering 10y term premium close to 100bp at current yield levels…

Participants emphasized that they would gain greater confidence that inflation is moving toward the 2% target -- a key condition for starting to cut rates -- only after seeing additional favorable data. The minutes also revealed differing views about the degree of monetary policy restrictiveness.

The ISM services PMI dropped into contractionary territory in June, continuing the recent string of volatile readings that began in April. Although services are slowing, we think June's downswing exaggerates the trend. Friday's hard data on employment should help clarify the signals.

Initial jobless claims have edged up on balance since end-April to levels not seen since early summer 2023. Last week's reading of 238k was about 30k above where the index stood two months earlier. Although this might indicate significant softening in the labor market, we think seasonal adjustment issues are to blame.

We forecast a 0.05% m/m SA increase in headline CPI, bringing the annual rate down to 3.1% y/y. We project that core inflation firmed by about 6bp, to 0.22% m/m (3.4% y/y), led by payback in a handful of core services categories that were unusually weak in May. We forecast that the NSA index will print 314.581.

BMO Weekly: Back to the New Norm (stopped OUTTA 2s10s flattener for small loss)

… Range trading with a bias toward lower yields and a flatter curve remains our base case for the next few weeks. Supply is once again topical in the week ahead as 10s ($39 bn) and 30s ($22 bn) will require some type of concession – either outright or on the curve. While we see no reason to expect a soft reception, the market will underwrite 10s on the eve of CPI – bringing into question whether investors will be willing to bid aggressively for supply. Ultimately, inflation will define US rates and the path of yields in the near-term – certainly more so than the immediate auction dynamics. The market is pushing back on the recent curve steepening, particularly in 2s/10s. The bearish nature of the recent spike that brought 2s/10s to -27.8 bp has come in contrast to widely held expectations for this year’s big macro trade to be the cyclical bull steepening of the curve. A further steepening retracement resonates, albeit limited to the confines of the 200-day MA at -38.9 bp …

… Away from the macro fundamentals, Treasury supply returns in the week ahead in the form of $58 bn 3s, $39 bn 10s, and $22 bn 30s. Recall we haven't seen a coupon auction tail since the 3-year offering on June 10th. Since then, 2s, 5s, 7s, 10s, 20s, 30s, and 5-year TIPS all stopped-through with above-average non-dealer allocations driven by elevated indirect bidding. A quick look at the investor class data shows that overseas demand was a key driver of the strong result for the benchmark tenor. Specifically, at the 10-year offering, foreign buyers took a 17.2% allocation which was the highest at a reopening auction in 2 years and five percentage points above the 12.2% 6-reopening average. The recent politically inspired bearish repricing creates a unique setup for the duration offerings, and we'll be curious to see if what has appeared to be durable shift into dip buying mode in the primary market manages to persist in the wake of the recent political drama.

Core PCE inflation continued to slow in May, with the annual inflation rate falling 21bps to 2.57% and the monthly inflation rate dropping to 8bps, the slowest pace since last November. Updating our suite of statistical models, we find that our monthly mean estimate for trend inflation declined by 4bps to 2.7%, while the median estimate dropped by 15bps to 2.8%. While trend inflation is still well above the Fed’s objective, it is now tracking the disinflation path observed in other price data.

As Chair Powell highlighted earlier this week, recent inflation data have provided some confidence that the disinflation process may be on track after stronger prints to start the year. Nonetheless, Fed officials have emphasized that a continuation of good inflation data is needed to gain enough confidence to cut rates. This leaves the door open for a rate cut before the election, though in our view, such an outcome could also require some additional evidence of a softening labor market and weakening growth (See (Pushed) Back to December).

Speculation about President Biden dropping out of the Presidential race has surged in the aftermath of last week’s debate. We remain skeptical that Biden will drop out, which we discuss below, but we readily concede this risk has risen substantially. In this note, we discuss mechanics and market implications (or lack thereof) of Biden leaving the race. In terms of mechanics, there are no modern precedents for how the Democrats would select a new nominee. We loosely assume VP Harris would be the front runner in that scenario, but with low conviction. For markets, we do not think that Biden leaving the race would be game changer from a policy perspective, and as a result would not change our assessment of the market impact of various election scenarios. A non-Biden Democrat would likely pursue a similar policy agenda as Biden. Our expected market scenarios on a Biden win are largely a factor of pricing out a Trump win rather than pricing in a Biden win. That dynamic remains regardless of which Democrat sits atop the ticket.

UBS: Stable democracy (? attempt to escape? shaking my head do NOT get this guy … some times … and how it is he’s so friggin popular … truthfully knows NOT what he speaks of … I’ll take ‘Merica any day of the week and 2x on Sunday … )

US markets are closed as the country celebrates its attempt to escape rule by a monarch. There has been media speculation about US President Biden’s candidacy for re-election. Markets are not likely to react to such speculation at this stage. Politically, markets primarily focus on the probabilities of economic policy change.

The UK is demonstrating the stability of the democratic process under a constitutional monarchy with its general election. Markets, rightly or wrongly, think that they know the likely outcome and are unlikely to react strongly (especially today with a media blackout until the polls close).

The Federal Reserve minutes of the June meeting suggested a desire for more evidence of cooling inflation before cutting rates. Some economists (including this economist) are getting frustrated. Harmonized inflation is below 2% and there is deflation for almost every sector of the economy somewhere in the US; how much more slowdown is required? …

Wells Fargo: Service Providers Spark Concern in June ISM

Summary The ISM services index slipped into contraction for the second time in three months, sparking concern for service-sector resilience. But the outturn may overstate current weakness as the details are more consistent with a moderating rather than contracting sector.

Source: Institute for Supply Management and Wells Fargo Economics

… And from Global Wall Street inbox TO the WWW,

Apollo: Rapid Increase In T-Bill Supply Is a Growing Risk

The supply of T-bills has increased by $2 trillion over the past 12 months, and the share of T-bills outstanding as a share of total debt outstanding has trended significantly higher over the same period, see charts below.

Why is the rapid growth in the supply of T-bills a problem? Because a big increase in supply requires a big increase in demand. Growing the amount of T-bills outstanding while the Fed at the same time is doing QT increases the risk of an accident in funding markets, which is what we saw in repo markets in September 2019.

In other words, the strong growth in the supply of T-bills will require a continued increase in demand from banks, money market funds, and households. If the Fed starts cutting rates, say, in September, we could see lower appetite for T-bills from households and money market funds, which ultimately would put upward pressure on short rates because of the big supply of T-bills not being met by similar strong demand.

Bloomberg: US Jobs Report to Show a Substantial Slowdown in Hiring in June

Forecasters see 190,000 rise in payrolls, wage growth below 4%

Numbers would support case for multiple Fed rate cuts in 2024

… The unemployment rate is seen holding at 4%, the highest level in more than two years.

Such a gradual cooling in the labor market would support Federal Reserve policymakers seeking multiple reductions in interest rates this year. Investors are currently putting good odds that officials on the Federal Open Market Committee will cut rates when they meet in September and December, according to futures…

Markets got the start to 2024 that we were looking for. The S&P 500 and NASDAQ 100 are up over 15% and 18.5%, respectively. Inflation is cooling, and cash rates will likely be lower from here…

… AND with this in mind and before I hit SEND — not knowing / thinking really IF there’s a reason to send anything BEFORE tomorrows NFP as it will likely only be the ‘B’ team in / around to read / think / trade / manage the PnL … a couple / few visuals …