Good morning … a BULLISH monthly view of 30s and a somewhat less bullish weekly view of 30s put forth over the weekend … just in time for a somewhat SOFTER START to the day, week and month ahead …

30yy DAILY: TLINE etched in and ‘at risk’ …

… this, as momentum hooking HIGHER so path of least resistance here / now favors a tactical SHORT (not unlike what was suggested in the front-end by Jamie Dimon’s group over the weekend…)

Moving on, you’ll ALSO note some dissention in the ranks of GDPNow-casts where Atlanta SAYS activity has collapsed TO -1.5% in Q1. Why?

…After recent releases from the US Bureau of Economic Analysis and the US Census Bureau, the nowcast of the contribution of net exports to first-quarter real GDP growth fell from -0.41 percentage points to -3.70 percentage points while the nowcast of first-quarter real personal consumption expenditures growth fell from 2.3 percent to 1.3 percent…

All is NOT lost because the folks on Liberty Street who report TO Williams, well, they are thinking something else …

The New York Fed Staff Nowcast for 2025:Q1 is 2.9%, with the 50% probability interval at [2.0, 4.0] and the 68% interval at [1.4, 4.5].

News from this week’s data releases left the estimate largely unchanged…

… Um … largely unchanged with a review of all the very same data? I realize this was all noted over the weekend … I dunno.

What I can say is I’ve no idea who to believe and KNOW more folks talk about the Atlanta Fed than FRBNY but we’ll watch / listen to Bostic (non voter) as we will Williams (voter) in the days ahead.

For now, though, here is a snapshot OF USTs as of 719a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are bear-steepening after opening softer in Tokyo, with our desk seeing better selling out the curve post month-end from real$. Better selling in London has seen bunds under heavy pressure (+9bps in 10y) post inflation and on defense spending speculation. Gilts are sympathetically weak while USTs have moderately outperformed alongside some modest peripheral tightening. Overall volumes have tapered off in the past hour or so, but sentiment from accounts remains to sell strength in the near-term with tens back above 4.25%. S&P futures are showing +30pts here at 7am, with Crude Oil flat and DXY -0.6% (EUR & GBP leading upside).

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US futures gain, USD lower & EUR benefits post EZ HICP, EGBs sink amid expectations of EU defence spending … Bonds are weighed on by developments around geopols/defence, currently at session lows … USTs are a touch softer as the latest geopolitical/defence developments don’t have quite the same ramifications for the US as they do for Europe. Currently at the lower end of a 110-27+ to 111-03 band, with recent pressure coming alongside the pressure seen across the pond. US newsflow is very much focused on the fallout from Trump-Zelensky, as we await concrete details into a potential Italian-led gathering, and the implementation of tariffs on Canada and Mexico tomorrow. Ahead, focus will be on US ISM Manufacturing PMI which will be scoured for tariff-related movements in input prices, as this could be indicative of a resurgence in inflation in the months ahead.

Max Dividends — who doesn’t wanna retire early and often and live off the land of high dividends? Have a point and a click thru for more and I believe this site may very well help one / all achieve some sort of comfort through insight …

President Trump’s policies potentially pose non-linear risks to growth and inflation – in opposite directions.

We continue to like 2s10s flatteners and 10Y TIPS as stagflation risks increase.

We think that discussion of a multi-lateral effort to weaken the USD is overblown.

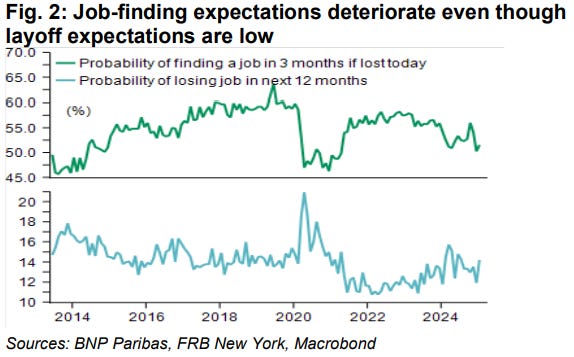

… We are skeptical that developments in Washington will have much of an impact on the February payrolls. That said, anxiety about job security does appear to be rising (Figure 2). Fed surveys show households still see a relatively low chance of losing a job (a positive factor), but dimmer prospects of finding one if it were lost today (a negative development). Such a dynamic could, over time, promote more precautionary savings and softer spending growth.

Against this backdrop of increasing stagflation risk, we continue to like our core US rates positions – 2s10s flatteners and long 10Y TIPS. Queries for the word ‘stagflation’ in Google searches have been rising (see Figure 3). And the last time such concerns rose in 2024, we saw the curve flatten. Although recent search trends for stagflation have risen, they remain well below 2024 levels, suggesting that the stagflation narrative could go a lot further – directionally consistent with our forecast for slowing growth and higher inflation.

… and …

MS: Sunday Start | What's Next in Global Macro: What If a Truce Is Weeks Away?

Amid rapid developments on Russia/Ukraine, investor attention has understandably shifted to the myriad implications for risk assets in the event of a resolution. At the time of writing, we estimate that Ukraine sovereign credit is already pricing a ~60% probability of a lasting ceasefire. Investor optimism on European equities has been strong so far this year, and the potential for a peace deal has added fuel to a ~10% rally year to date in European equities. Against this backdrop, we believe a look below the surface of recent headlines, which we attempted recently in Russia/Ukraine – Addressing Misperceptions, is warranted…

…In all potential Russia/Ukraine peace deal scenarios, we see higher costs for Europe. Our economists believe that this will ultimately put more pressure on public finances and is likely to end up in cuts to welfare spending and/or higher taxes. While the easing of EU fiscal rules can create some room for more defence spending in the near term, it is unlikely to solve medium-term budget challenges in countries like France and Italy.

Undoubtedly, the key from here will be additional details and the conditions of any sustainable proposed ending to the Russia/Ukraine war. Meanwhile, European leaders are in London today and are scheduled to meet for a special summit on March 6 to discuss joint plans on defence and security.

Moving along and to a few things dropped into the inbox since …

… and no better way to kick off the day / week and month than with a look back and an officially unofficial recap of the month that was …

February was an incredibly eventful month for markets, with most assets making steady gains, despite the threat of US tariffs. Initially, the tariff threat meant markets got the month off to a difficult start, but a last-minute extension for Canada and Mexico led to a subsequent relief rally. So at first, that helped risk assets to do quite well, with the S&P 500 reaching an all-time high on February 19. But towards month-end, a more risk-off tone developed as tariffs came back on the agenda, alongside some weaker data out of the US. That hit the Magnificent 7 in particular, which posted their worst month since December 2022, which in turn dragged down US equities more broadly. Nevertheless, it wasn’t all bad news, with European equities continuing their outperformance, whilst the move towards haven assets meant sovereign bonds and gold advanced…

…Which assets saw the biggest gains in February? Sovereign bonds: US Treasuries did particularly well given the risk-off tone towards month end, and the 10yr yield fell -33bps on the month to 4.21%. That was the biggest monthly decline in yields since July 2024. Meanwhile in Europe, 10yr bund yields also came down -5bps to 2.41%…

…Which assets saw the biggest losses in February? US equities: The slump in tech stocks hit US equities more broadly, with the S&P 500 down -1.3% in total return terms. The Magnificent 7 (-8.7%) were a particular underperformer, posting their largest monthly decline since December 2022.

… AND from a monthly recap to an overnight / early morning look to the day ahead (and NFP) …

… With regards to payrolls, our economists expect headline (160k forecast vs. 143k previously) and private (150k vs. 111k) payroll gains to rebound from weather-related and potential seasonal-factor related drags in the prior month. However there is a drag factored in from the start of federal government layoffs even if March may see a larger impact. DB think the unemployment rate will tick up a tenth to 4.1%. Today’s manufacturing ISM (DB at 51.8 vs. 50.9 last month) and Wednesday’s services ISM (DB at 52.1 vs. 52.8) will have employment components that along with Wednesday’s ADP report may sharpen the street’s forecasts as the week progresses …

… On Friday, we also got the latest PCE inflation data for January, which is the Fed’s target measure. That was broadly as expected, with headline PCE at +0.33% on the month, and core PCE at +0.28%. However, it meant both headline and core PCE were still lingering above the Fed’s 2% target on an annual basis, at +2.5% and +2.6% respectively. The other important release was the merchandise trade deficit, which unexpectedly surged more than +25% to $153.3bn in January (vs. $116.6bn expected). The surge likely reflects companies seeking to import goods before tariffs come into place, with gold shipments one potential factor. The release caused a big hit to Q1 GDP estimates with the Atlanta Fed’s GDPNow estimate plummeting to show an annualised contraction of -1.5%, though traditional nowcast models may need to be heavily discounted given the nature of the trade distortions.

For sovereign bonds, the risk-off tone pushed yields lower around the world, with the 10yr Treasury yield falling -22.3bps last week (-5.2bps Friday) to 4.21%. That’s the 7th consecutive weekly decline for the 10yr yield, which is the first time that’s happened since June 2019. Meanwhile in Europe, yields on 10yr bunds fell -6.4bps (-0.8bps Friday) to 2.40%. And over in Japan, the 10yr yield fell -5.2bps (-2.3bps Friday) to end a run of 7 consecutive weekly increases …

… Finally, same shop with an effort to detail several reasons to stay positive …

DB: Mapping Markets: 4 reasons to stay positive on markets

Last week saw a clear risk-off move, particularly in the US. But although it’s raised alarms about what might be next, it’s worth remembering it was only a week-and-a-half ago that the S&P 500 closed at a record high, and the index is still just 3% beneath its peak. Moreover, markets are inevitably going to experience corrections from time-to-time, and despite a relentless bull market since late-2022, that’s a normal thing to happen.

Looking forward, there are still lots of reasons to stay positive on risk assets. First, the data we’re seeing is hardly recessionary, and the weakness has been more in surveys rather than hard data. Second, we’re not seeing conditions that have coincided with big equity slumps previously. Third, even if growth does weaken, central banks now have a lot of room to cut rates. And fourth, markets have already proven highly resilient to several risks this year, including tariffs and geopolitics, suggesting it would take a much bigger shock to cause a large selloff.

1. In absolute terms, recent data remains pretty strong and is not pointing towards a recession. Moreover, the weakness has been clearer in surveys rather than hard data.

…2. Even if growth did weaken, central banks have a lot of scope to cut rates today. That’s different to the 2010s (when rates couldn’t go any lower) or 2022-23 (when high inflation prevented rate cuts).

…

MS offering an equity centered week ahead …

MS US Equity Strategy: Weekly Warm-up: Focus on Relative Value As Policy Uncertainty Persists

New tariff headlines add to the policy uncertainty. While growth expectations are slowing, the good news is it's been a rich environment for relative value trades. We see relative outperformance continuing for Financials, Consumer Services over Goods, Software over Semis and Quality.

The Reason Why Rates Are Falling Is Important...Stocks' rate sensitivity has diminished as the 10-year yield has settled below our 4.50% level. In other words, lower rates are currently not benefitting equity returns to the extent they were just a couple of weeks ago given the reason why yields are falling—softer growth expectations. What this means for the time being is that growth (both economic and earnings) is now the prominent driver of equity indices…

MS offered an economic world view …

MS: Global Economic Briefing: The Weekly Worldview: Will spring bring a thaw in Europe?

Euro Area growth will be driven by consumption, while investment lags. But risks to the growth outlook remain.

Here’s an economic week ahead primer from Switzerland which I missed over the weekend … sharing for the NFP pre-cap …

UBS: US Economics Weekly Employment report and maybe tariffs 28 February 2025

…The Week Ahead: payrolls, Powell and more tariffs? We project nonfarm payroll employment climbed 175K with help from seasonal adjustment and government employment — we preview the report starting on page 17. Chair Powell will speak at the Monetary Policy Forum after the employment report, an opportunity for his assessment and potentially an update on the inflation data, and inflation expectations. We expect overall he will hew closely to the message in January, which was the message in December, that the economy remains strong and they can wait to assess the trajectory of inflation before resuming lowering interest rates. We expect the ISM manufacturing composite was little changed in February. Lightweight vehicle sales give the first look at consumer spending in February, we think they improve to a 16.2 million (saar) pace. The financial accounts for Q4 will imply aggregate consumer balance sheets remain robust, but we await the distributional financial accounts released with a lag to see how this is split across the income distribution. Last but not least, we will see if administration goes ahead with the Mexico, Canada and China tariffs that appear to be scheduled to go into effect Tuesday …

…Establishment survey details: wide range of risks Continuing claims for unemployment insurance are running 10K or so higher over the month, net of filings in California the second week of January, and initial claims are little changed over the month, and even net of residual seasonality. Claims filings in California appear to have largely normalized after being elevated in January. We would expect the wildfires held down January nonfarm payroll employment by ~10K jobs and expect the bulk of that returns in February. The state data is not yet available to make a more detailed assessment, and upon revision the assessment of January might change, adding uncertainty to this assessment.

… Finally, Dr Bond Vigilante on the economic week ahead …

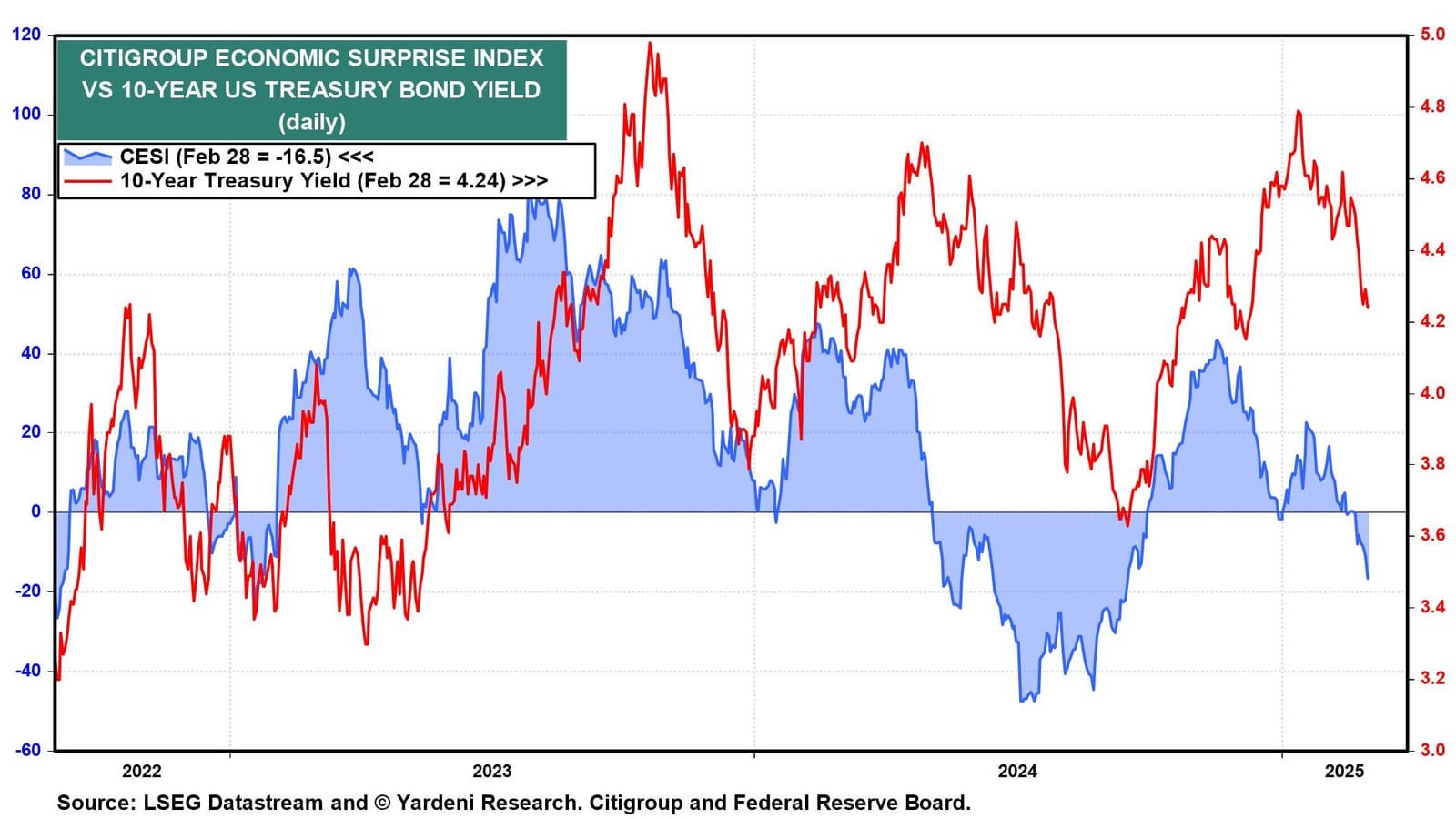

February's batch of economic indicators for January was mostly downbeat, the sort of numbers suggestive of a severe economic slowdown. They caused a few economists to raise their odds of a recession but not us. Indeed, the Citigroup Economic Surprise Index fell to -16.5, the weakest since the summer of 2024 (chart). The 10-year Treasury bond yield fell to 4.24% on Friday from a peak of 4.81% in January.

We think much of this soft patch was caused by January's ice patch, which was the coldest January since 1988. If so, then February's batch of economic indicators is likely to be mostly stronger than expected.

Let's review the outlook for some of the key economic indicators coming out this week…

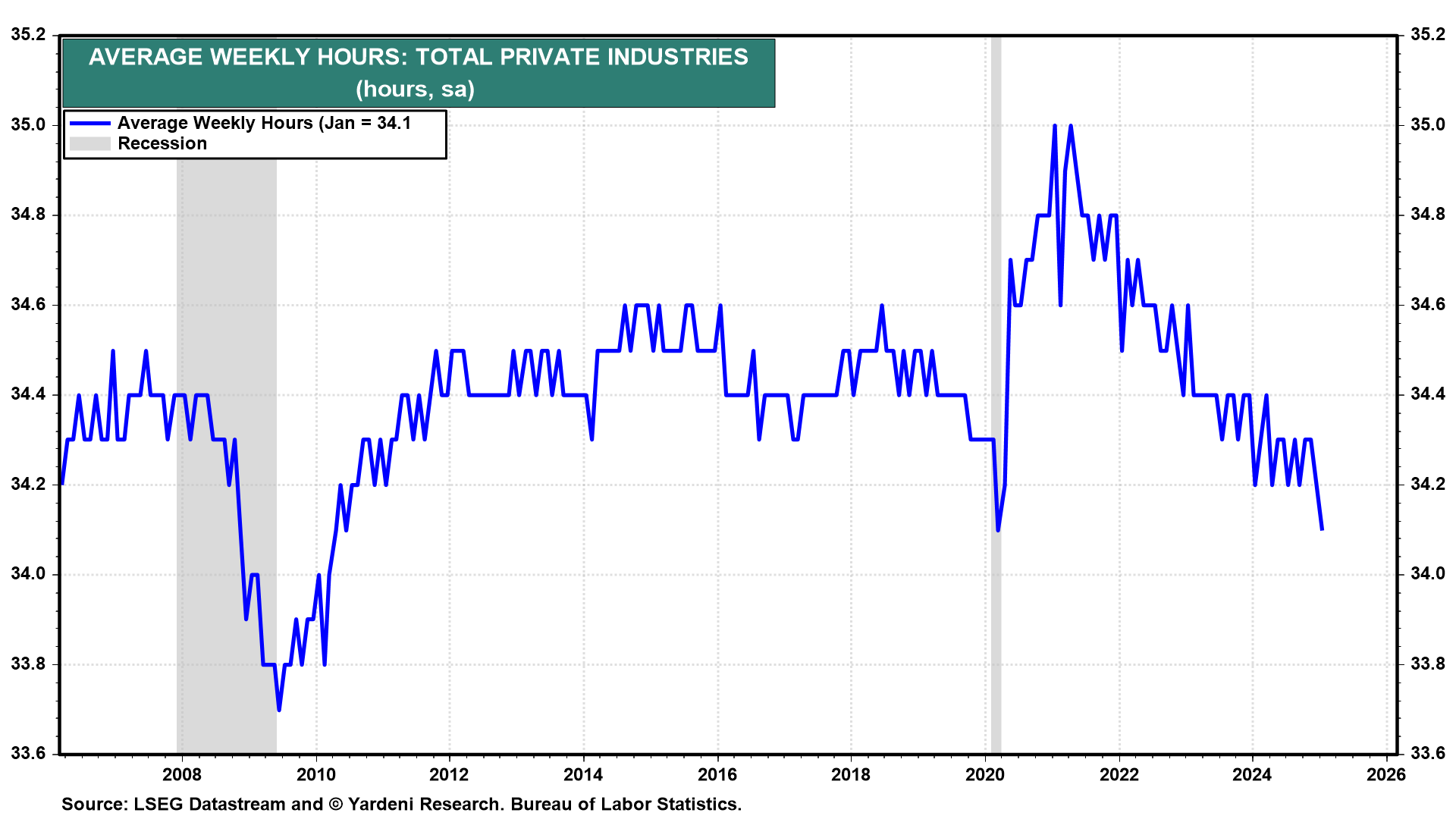

… (2) Employment. January's labor market indicators were almost certainly weakened by January's Arctic blast, which brought record-breaking low temperatures and fueled a winter storm that dropped historic snowfall for parts of the South. Payroll employment rose only 143,000, and the average workweek fell (chart). Both should show rebounds in February's employment report (Fri). We are expecting that federal job loses attributable to the DOGE Boys won't show up until the March employment report. But they did start to show up in initial unemployment claims during the February 21 week.

On balance, we are expecting that the first batch of February economic indicators this week will push the bond yield higher. Stocks might also have a relief rally on better-than-expected economic indicators. Then again, President Donald Trump said on Thursday that 25% tariffs on goods imported from Canada and Mexico would go into effect Tuesday, alongside yet another 10% layer of duties on China following the one that took effect this month.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

First up, if OER moves higher in 2025 then what ‘bout rest of the ‘flation complex and so, rate CUTS …

Since the Fed began to raise interest rates in March 2022, housing starts have declined significantly, in particular, multifamily housing starts for rent have declined almost 50%, see the first chart.

Given it currently takes on average 17 months to build a multifamily property, see the second chart, we can produce a forecast for the number of multifamily homes coming to the market this year and next year. The conclusion is that multifamily completions will decline significantly in 2025 and 2026, see the third chart.

Combined with a historically low rental vacancy rate, solid household formation, and an all-time high share of Americans saying that they would rent if they had to move, the bottom line is that rent inflation will start to rise later this year, see the fourth, fifth, and sixth chart below.

Rising rents put upward pressure on OER in the CPI index and will keep inflation higher for longer. With inflation higher for longer, the Fed will also keep interest rates higher for longer.

The bottom line is that inflation remains well above the Fed’s 2% inflation target, and it will require interest rates higher for longer to get inflation back to 2%.