Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP, a couple CHARTS in effort to wee out some signal from the noise …

30yy MONTHLY: TLINE broken, bullishly …

… momentum BULLISH…

30yy WEEKLY: TLINE brake looks even MORE impressive BUTT…

… momentum become stretched AND yields romancing 50wMA which coincides with psychologically important round numbers (4.50%) …

Next up some of the COMMENTARY and snark as it relates TO the data in puts, helping create the price action / visuals …

CalculatedRISK: Personal Income increased 0.9% in January; Spending Decreased 0.2%

ZH: Americans' Savings Rate Soars As First Official Signs Of DOGE Success Emerge

ZH: Atlanta Fed Model Suddenly Signals US Recession As Stagflation Takes Hold

AND as the day, week and monthcame to a close, remarkably without incident after world leaders being thrown OUT the oval …

… Alrighty, then. I’ll leave the escortation OF Zelinsky OUT the oval aside, except to say how impressed I was that month-end position squaring needs outweighed the circus at the WH … I wonder if we’ll see a similar (delayed)reaction like the one we saw with NVDAs earnings … To be continued but for now, calling all of Team Rate CUT.

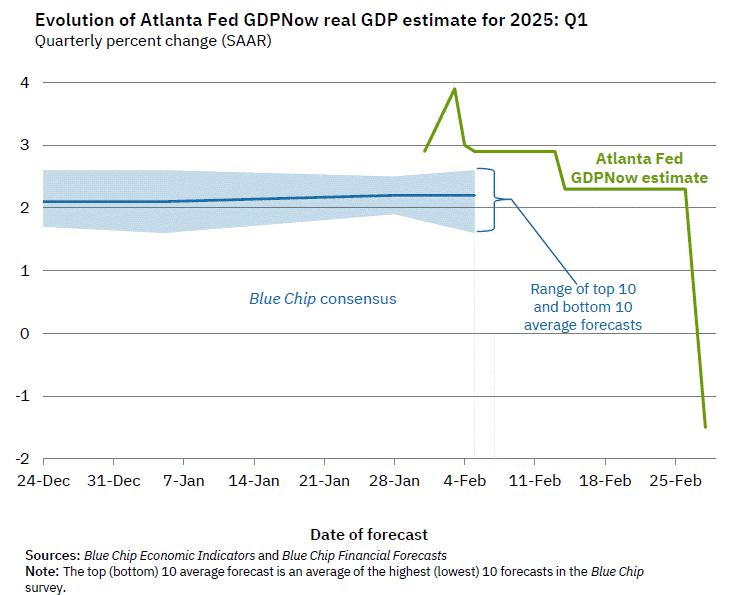

They have continued to try and say it … in the case you hadn’t yet heard / seen, yet … GDPsNOWs ….

First up, the one the popular kids follow … Atlanta SAYS …

…The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2025 is -1.5 percent on February 28, down from 2.3 percent on February 19. After recent releases from the US Bureau of Economic Analysis and the US Census Bureau, the nowcast of the contribution of net exports to first-quarter real GDP growth fell from -0.41 percentage points to -3.70 percentage points while the nowcast of first-quarter real personal consumption expenditures growth fell from 2.3 percent to 1.3 percent.

The next GDPNow update is Monday, March 3. Please see the "Release Dates" tab below for a list of upcoming releases.

The New York Fed Staff Nowcast for 2025:Q1 is 2.9%, with the 50% probability interval at [2.0, 4.0] and the 68% interval at [1.4, 4.5].

News from this week’s data releases left the estimate largely unchanged.

Negative surprises from personal consumption and housing data were largely offset by positive surprises from disposable personal income and manufacturers’ durable goods data.

Make of it whatever you will but I’ve a question …

I’ll move on TO some of Global Walls WEEKLY narratives — SOME of THE VIEWS you might be able to use. A few things which stood out to ME this weekend from the inbox

Setting up the week ahead, THE bank of the land weighs in …

BAML: Global Rates Weekly Whack a tariff | 28 February 2025

…Rates: Honeymoon is over US: US survey data justifies our soft duration long & belly outperformance views. House bill passage marginally raises risk of early debt limit resolution.

… Bottom line: policy uncertainty is hurting sentiment indicators & driving rates lower. We recommend investors be at worst neutral their duration benchmark if not still softly long with potential for rate range to shift lower, especially if hard data follows the surveys. We expect belly to outperform wings; we hold M5Z6 flattener. House reconciliation passage marginally raises risk of earlier debt limit passage.

…Technicals: US 10Y reaches target, fade Feb, buy by May US10Y yield reached its head & shoulders target of 4.30%. Tempting to fade Feb rally for March dip and buy by May. Seasonals agree. Steeper 5s30s if > 30.

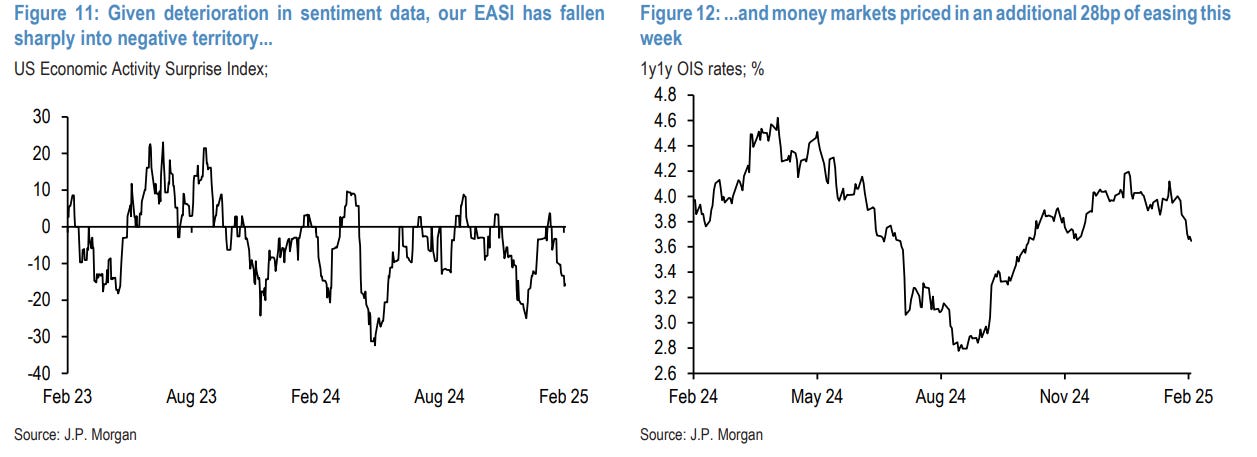

The high uncertainty about tariffs, DOGE, budget deficits and a Ukraine peace deal has started to weigh on US activity. While we revise down our growth forecast, we see Fed easing still restrained by inflation. Next week, tariff deadlines, US payrolls, the ECB decision and China's NPC are in focus.

…US Outlook Appetite for disruption: The softening Incoming data suggest that the enduring resilience of consumer spending and the labor market may finally be under threat. We revise down our near-term outlook to allow for less spending momentum amid indications that tariff front-running dynamics had been a bigger consumer tailwind in Q4.

… and from the very best in the biz … buy LONG bonds if a dipORtunity …

In the week ahead, our constructive bias for Treasuries will remain intact as the payrolls report looms. The fact that 10-year yields managed to dip to 4.21% on Friday has contributed to a shift in sentiment in the US rates market. There have been a few key recent developments that reinforce the idea that lower yields could soon prove the path of least resistance – our favored route. The tone change began with the first look at February’s services PMI (which printed <50), and was reinforced by the disappointing consumer confidence data, as well as the higher-than-expected jobless claims figures. Adding to the deteriorating data narrative was January’s downside surprise in consumption as personal spending shrank -0.2% and, in real terms, the move was -0.5%. When considering the widening trade deficit seen via the advance goods trade report, the market has become increasingly concerned that the momentum of the real economy has turned toward the downside and while a recession might not be in the offing, a subdued growth profile has quickly emerged.

Recall that the consumer has been the pillar of real growth and contributed to the outperformance of the US economy on the global stage. In the event that the tide has sustainably changed on the employment front, it follows intuitively that households will engage in preemptive savings as the perception of job security is undermined. Another key driver of growth within the last few quarters has been government spending, and clearly the trend in Washington DC has reversed, leaving Federal spending unlikely to be a key positive influence on real GDP in the near-term. As for fixed investment, it's difficult to be overly enthusiastic about the residential real estate sector given that mortgage rates remain elevated, even as Treasury yields continue retracing from the mid-January highs. Similarly, the prospect for net exports to propel realized growth forward in the coming quarters is difficult to imagine as trade war headlines continue to define the news cycle. As the March 4th implementation of tariffs on Canada, Mexico, and China approaches, further retaliation should be expected.

It's with such a backdrop that we’re particularly wary of any further evidence of headwinds in the labor market. With a consensus for headline payrolls at +158k and private NFP seen adding +130k, it strikes us that the market continues to see +28k of government hiring, although that includes the state and local levels as well. It’s too soon to anticipate the tone shift in Washington DC weighing on the BLS data. As a result, we suspect that any solid print on Friday will be downplayed as ‘dated’ information. The labor market is a lagging indicator and one that can take a while to turn. However, once a softer labor market narrative takes hold, it quickly becomes difficult to fade.

For the time being we’re holding our year-end forecast for 10-year yields at 4.0%, but as this target is <25 bp away, we’ll concede that it is tempting to move the goalposts into 3-handle territory. We’ll refrain from slipping into the revision trap if for no other reason than there are a lot of shifts to the macro-outlook that are yet to come as the combination of the trade war and an aging expansion create an array of potential economic pitfalls. The most obvious of which being a consumer-led slowdown in real growth that occurs at a moment when tariffs will be propping up realized inflation, thereby limiting the Fed’s flexibility in normalizing policy rates. Throughout most of this cycle, the FOMC has benefited from a resilient economy/labor market, but concern is growing that this dynamic might soon end as Q1 real GDP is now tracking at -1.5% (the lowest since Q1 2022 when real growth contracted -1.6%)…

…We see the top of the local yield range at 4.60%, and we'll look to buy a dip in 30- year bonds if yields retrace to the top of the current trading zone. The appeal of the long bond is also enhanced by its underperformance versus the 10-year sector since the recent rally in duration began on February 19th. For context, 10s/30s reached its steepest levels in over 4 months on month-end.

Germany weighing in on flows …

DB: Investor Positioning and Flows - Sharp Slide To Near Neutral

quity positioning slid sharply this week, falling back down to near neutral (z score 0.15, 50th percentile), wiping out the post-election bump. Notably, investor sentiment plunged to near record lows. The slide in positioning took the S&P 500 to the bottom of the narrow +/- 2% range of the last 3 1/2 months since the election as well as the tight trend channel in place since the October 2022 low. What’s behind the recent slide?

Economic uncertainty, rightly at the forefront of investor concerns, spiked a month ago and has not receded, likely rising further ahead of potential escalations next week;

Macro data surprises turned negative last week for the first time since September, but this is in keeping with regular cycles with alternating positive and negative phases of 4-5 months;

10y yields fell sharply over the last 2 weeks, along with equity positioning and equities, as is typical in periods of rising growth concerns. Defensive sectors and our end-cycle (recession) long/short basket of stocks have rallied hard since early last week, also indicating rising growth fears;

Sharp cuts of -3% in Q1 consensus earnings estimates have added to these fears. But these look only a little worse relative to history, with cuts going into earnings season the norm, and the first quarters of the year usually seeing the largest.

While equity positioning has now dropped nearly to neutral, fund flows remain strong with another $27bn pouring in this week, the largest in the last ten. As we have emphasized previously, we continue to see a cross-asset inflows boom, with bond funds ($24bn) seeing the largest weekly inflow since Oct 2020.

Equity positioning slid sharply to near neutral, wiping out the post-election bump

Data SAYS …

ING: US 1Q GDP growth concerns mount on weak spending and surging imports

The economy has started 2025 on a weak footing with the 'negatives' from President Trump's policy thrust taking an early toll via weaker consumer confidence and spending at the same time as importers look to front run the threat of tariffs

(one of)Jamie Dimon’s group(s) says …

JPM: Navigating rate risks: How bonds are better positioned in 2025

…However, fixed income does still help to diversify portfolios; it hedges them specifically from growth shocks regardless of increasing correlations with equities. As such, we’re reminding investors of some of the fundamental principles of fixed income investing to guide their 2025 portfolio allocation decisions.

Bonds can still hedge against growth slowdowns S&P 500 index level and 10-year U.S Treasury total return

Source: Bloomberg Finance L.P. Data as of February 26, 2025. 10-year represented using the Bloomberg US Government 10 Year Term Index Total Return Index. Tech wreck measures Jun '00-Dec '03, GFC measures Sep '07-Dec '09, U.S. debt downgrade measures Dec '10 to Nov '11, China currency devaluation measures Jun '15-Feb '16, Fed tightening fears measures Sep '18-Jan '19, Covid-19 measures Jan '20-March '20, Sahm rule triggered measures 2 Aug '24-5 Aug '24, Softer growth data measures 18 Feb '25-26 Feb '25.

Bonds today are better positioned against a rate sell-off. A concern often raised by investors who held bonds through the rate sell-off of 2022 is the risk of adverse performance if rates increase again. The critical difference between a rate sell-off now and the rate sell-off that began in 2022 is that an investor today receives much more income because of the higher starting yield.

We can see an example of this if we compare the performance of the 10-year Treasury in early 2022 to late 2024. The 10-year Treasury yield increased by approximately 80 basis points over the first quarter of 2022 and the fourth quarter of 2024, but the starting yield at the start of Q1 2022 was only 1.5%, while the starting yield at the start of Q4 2024 was 3.8%. Performance was 200 basis points higher in 2024 because the starting yield was more than double that during 2022. In other words, investors received more than twice the income they had received two years earlier to offset a similar shift in rates. Higher yields can provide a cushion to adverse moves (rising) in rates, and compound on top of price appreciation in an advantageous scenario (falling rates).

Starting yield can be a very good indicator of future return. About 88% of the five-year annualized Bloomberg U.S. Aggregate Bond Index return can be explained by the starting yield. Even without a regression analysis, this makes logical sense. Yield-to-maturity can be interpreted as the average rate of return that will be earned on a bond if it is bought now and held to maturity. As long as the issuer does not default, which is unlikely in investment grade sectors, an investor can expect to receive approximately the starting yield in annualized total return for the duration of their investment regardless of how rates and spreads change, or how the equity market performs…

… and from another of Jamie Dimon’s desks …

JPM: U.S. Fixed Income Markets Weekly 28 February 2025

…Governments The sharp decline in sentiment raises risks of a more abrupt slowdown as occurred in 2018-2019, but over the near term, we think the market’s worst fears should temporarily be assuaged by stronger labor market data in February. Position technicals have also extended and using history as a guide, suggest risks of higher yields in the coming weeks. We recommend tactical shorts in 2-year Treasuries. We also recommend 10s/30s flatteners as a lower beta way to position for higher front-end yields, with some relative value. TIPS valuations are cheap, but given downward revisions to near-term growth forecasts and event risks next week, we remain neutral on breakevens. The 1Yx1Y/5Yx5Y CPI curve has is back near its flattest levels since the election and we take profits on inflation swap curve flatteners…

…Treasuries I've got reservations, about so many things

Treasury yields declined further this week, reaching their lowest levels since mid- to late-fall...

Data broadly disappointed to the downside, as regional Fed surveys underscored falling business confidence, consumer confidence weakened further, and consumption data weakened, all indicating downside risks to growth in 1Q25...

...term premium declined further this week, and intermediate yields are fairly priced relative to their fundamental drivers for the first time since the fall

The sharp decline in sentiment raises risks of a more abrupt slowdown as occurred in 2018-2019, but over the near term, we think the market’s worst fears should temporarily be assuaged by stronger labor market data in February

Position technicals have also extended and using history as a guide, suggest risks of higher yields in the coming weeks. We recommend tactical shorts in 2-year Treasuries

The curve has steepened more than would be implied by medium-term Fed policy and inflation expectations: we also recommend 10s/30s flatteners: this represents a lowerbeta way to position for higher front-end yields, with some relative value

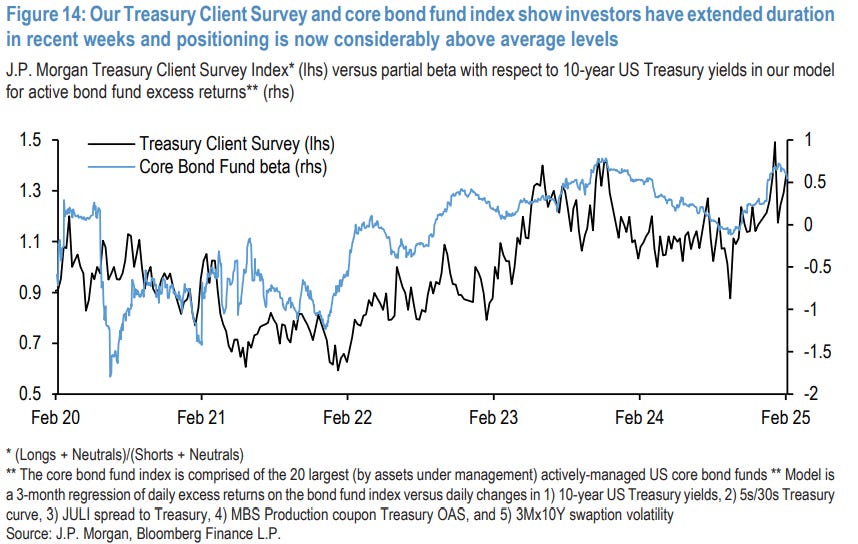

…We think positioning dynamics support some mean reversion as well: our Treasury Client Survey has extended in recent weeks and is now near its longest levels of the last 5 years, as is our core bond fund beta, which measures the duration exposure of the largest activelymanaged core bond funds in the US (Figure 14Our TeasyClint Surveyand corebnd fuiexshow investor havextnd uraionect wksandpoitg snwcoiderably oveargls ). With the Treasury Client Survey index now more than 2 standard deviations longer than its prior 1-year average, this indicates a risk that yields could move higher over the coming weeks (see Survey says: Using the Treasury Client Survey to predict rates moves, 7/21/23)…

Recent Fed communication sharpened focus on the balance sheet, signaling an earlier end to QT and desire to shorten the WAM of SOMA. A shorter SOMA WAM means more demand for bills, which we think needs to be met with more bill supply. Risks lurk, stay in SFRM5Z6 flatteners and short SERFFJ5.

Key takeaways

Recent Fed communication has brought renewed focus to balance sheet considerations, specifically QT as well as asset holdings, over the past few weeks.

Minutes of the January FOMC meeting firmly pushed back against the notion that QT would continue until after a resolution to the debt ceiling.

Dallas Fed President Logan expressed support for overweighting shorter-dated UST securities in the medium-term, when SOMA eventually needs to expand.

Since SOMA is underweight bills, bringing WAM closer to total USTs outstanding, means more demand for bills, which we think necessitates more supply.

We suggest investors remain in SFRM5Z6 curve flatteners, as growth concerns mount, and stay short SERFFJ5 on the emergence of frictions in funding.

Back across the pond to another update of the US economic situation from a UK shop … updating of it’s Fed call just in a nick of time …? Pops used to say if it weren’t for bad timing I’d have none at all …

NatWEST: US Weekly Economic and Strategy Brief 28 Feb 2025

Highlight of the week: The usual start of the month high-profile indicators are due in the upcoming week. We expect overall payrolls increased by 150,000, up slightly from the 143,000 jobs created in January, which would still put the three-month average in payroll gains at a healthy level of 200,000. We also look for the unemployment rate to have held steady at 4.0%. Meanwhile, the ISM measures are unlikely to show any big moves in February. However, light vehicle sales could have bounced back in February after cold weather weighed on auto sales in January….

…Update to Fed Call With so much in doubt, we’re taking rate cuts out Summary: In light of growing uncertainty around the economic outlook and uncharted policy shifts by the new administration, we no longer expect the Fed to cut rates in 2025 and, for now, are not showing any moves (in either direction) from Fed officials. While we think the hurdle for a near-term rate cut is high, we wouldn’t fully rule out any renewed action at some point down the road, but that may not happen until sometime in 2026.

United States: Consumer Hibernation After a solid finish to 2024, the U.S. consumer rested up in January. Spending fell 0.2% despite solid income growth. The Fed's preferred measure of inflation showed price growth easing a bit further on trend, but confidence data out this week show consumers anxious about future inflation as talk of higher tariffs continues to dominate headlines.

…All told, the Fed speak this week provided additional support for our view that the FOMC will remain in a holding pattern over the next several meetings as upside risks to inflation mount alongside rising economic policy uncertainty. Against this backdrop, we still expect that a few more rates are in the cards, though not until the second half of 2025.

… Moving along TO a few other curated links from the intertubes, which I HOPE you’ll find useful …

First up, as the facts shape shift, so to do narratives and here’s one that’s developing …

Apollo: A Modest Stagflation Shock But Not a Recession March 1, 2025

There are often adjustment costs associated with changing policies. Laying off government workers puts upward pressure on unemployment, and imposing tariffs increases prices and lowers demand for foreign goods. How significant the impact of these policies will be on the economy depends on the magnitude and duration of each policy.

The two first charts below show the impact of tariffs and DOGE on GDP and inflation, using a model similar to the Fed’s model of the US economy, FRBUS. The results show that over the coming quarters, inflation will be 0.2% higher and GDP will be 0.5% lower.

In other words, DOGE and tariffs combined are a mild temporary shock to the economy that will put modest upward pressure on inflation and modest downward pressure on GDP.

This is also what the incoming data is showing. This week, we saw inflation expectations move higher, a reversal of capex spending plans, and weakness in consumer confidence, see the third and fourth chart, and our chart book here. Jobless claims also moved higher, likely driven by government contractors and also by federal workers who had not received forms SF-50 and SF-8 and decided to file for unemployment benefits anyway to get the process started.

The bottom line for markets is that this is a modest stagflation shock to the economy but not a recession…

(not to forget …)

Apollo: Recession Probability Rising February 28, 2025

Macro strat from Team BBG …

Bloomberg: Basis Trade Is on Thin Ice as Credit Cycle Turns: MacroScope 02/27/2025

(Bloomberg) -- A deterioration in credit markets, anticipated by a rise in bankruptcy filings, could trigger a hedgefund unwind of the large bond-futures basis trade, leading to instability and illiquidity in the Treasury market and beyond.

Nothing exists in a vacuum, and nowhere is that more true than in markets. Instability across assets could arise from a symbiotic relationship that has developed between bond managers, hedge funds and Treasury futures, with credit a potential catalyst.

This dynamic could also explain why primary dealers have been left sitting on large inventories of bonds. That’s an ongoing risk for liquidity in the Treasury market and funding markets overall.

Watch credit spreads. They have remained a bastion of calm despite a weakening in underlying fundamentals and greater uncertainty. Spreads have stayed tight even as bankruptcy filings have risen

Charts … a money manager with a Terminal offering CHARTS …

…Interest Rates Yields are trapped between inflationary pressures and DOGEflationary drag. I don’t expect much fun in bonds as we should remain trapped 4.10%/4.50%. The front end might be tradable, but the fact that yields didn’t go lower on Thursday’s huge equity selloff probably tells you that the appetite for bonds at 4.25% is no longer voracious.

From the Wolf of Wall …

WolfST: PCE Inflation Hits 4.0% Month-to-Month Annualized, Worst since March. 3-Month PCE Hits 2.9%, Worst since April. But Massive “Base Effect” in Services Cools YoY Increases

December, prior months revised higher. Goods prices jump month-to-month by most since August 2023, turn positive for first time in a year.

… and

WolfST: No, Consumer Spending Didn’t Plunge in January and Auto Sales Didn’t Collapse, or Whatever, But the Huge Seasonal Adjustments Might Have Gone Awry

Year-over-year, consumer spending jumped by 5.6% and retail sales by 4.8% in January. So there’s that.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

February was great month for the Bond Market...

How much do Bond buyers love

Tariffs ???

Extrapolation: can Trump increase tariffs enough to force the Feds hand

on rate cuts ???

I'm not advocating that, but....

The new "knee jerk" trade is higher tariffs breed higher Bond prices and lower yields...

Who needs Jerome Powell, when

you have Trump and Bessett.

They might be smarter than people

think....Crazy, like a Fox....