while WE slept: USTs soft; framework for a framework; JPOWs replacement to be tested; bet on bullish HARD data (Yardeni) evidenced by bets on only 1 cut (EBB)...

Good morning … Yesterday was truly a placeholder of a day. BMOs words (below) and it would appear there has been SOME progress. The US & China have apparently agreed to a framework for a further framework of a deal …

CNBC: China, U.S. officials reach agreement for allowing rare-earth, tech trade. Now it’s up to Trump and Xi

… with that AND Musk burying the hatchet

CNBC: Elon Musk says he regrets some social media posts he made about Trump

… no, not IN any more gruesome fashion … in mind, there’s very little need for me to add much here / now, ahead of this afternoons $39bb 10yr auction. And so I won’t.

Good morning, unless, of course, you read THIS and thought, hey, why not … lets give 3yrs a shot …

ZH: Tailing 3Y Auction Kicks Off Week Of Closely-Watched Supply

… Truth be known, not much in the way of damage as 3yy are still in / around 4.00% and ‘all eyes’ on Global Wall look onward and upwards TO this afternoons $39bb 10yr auction … which will have the benefit of CPI as hindsight …

10yy: support vs 4.50% (TLINE) and resistance vs 4.35 TLINE, 55dMA)

… this, as daily momentum grinding higher (towards, but not YET, overSOLD levels) which, in context, could help as it may be viewed as concession (ie DipOrTunity) … watching today AND tomorrows levels / auctions which again, will BOTH have benefit of CPI data in hand …

… with that little in mind and important data setting the table for supply just ahead, I’ll move along.

BUT FIRST … quick note — I’ll be outta pocket tomorrow traveling in / outta NYC and that means yer on yer own into / through long bond auction. I hope to be back and at regular spammation Friday morning. Sorry for any inconvenience. AND … here is a snapshot OF USTs as of 705a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US/China reach Geneva framework, markets await CPI … USTs softer but, compared to the above, are much closer to the unchanged mark. As we await updates from the US and/or China President, CPI and then 10yr supply (3yr passed without impact). Amidst this, yields firmer across the curve which is slightly steeper.

…IT'S ALL RELATIVE G7 debt markets are often a relative game.

Italy's debt-to-GDP ratio - long in excess of 100% - is no longer such an extreme outlier. Even though its current 137% tally remains historically high, the figures for other advanced economies are fast catching up. Italy's debt burden is also one of the few in the G7 that's not projected to keep rising over the rest of the decade.

Japan comfortably retains that mantle as the most indebted G7 nation relative to its economic size. But U.S. sovereign debt has zoomed through 100% of GDP, and U.S. President Donald Trump's 'Big Beautiful Bill' making its way through Congress is expected to make that worse.

More obviously within Europe, once frugal Germany has also lifted its self-imposed 'debt brake' and committed to fiscal stimulus that will arguably buoy euro zone growth at large even as some see its debt-to-GDP ratio hitting at least 100% within 10 years.

Expectations were for Tuesday to be a placeholder of a trading session for Treasuries and the day didn’t disappoint…

…The market will have the benefit of a fresh set of inflation numbers on Wednesday, an update that will be the most current look at consumer price pressures. Investors are understandably wary of the prospects for initial signs of tariffrelated reflation, even if the consensus is for a relatively benign 0.3% print (0.27% on an unrounded basis). Perhaps the more relevant takeaway from Wednesday’s session will be the degree to which investors are willing to setup to takedown the $39 bn 10-year reopening auction – we’re cautiously optimistic, emphasis on cautiously…

Quiet markets described AND offering time to consider other things, such as who’s to be next chair of the FOMC …

… Overnight, US and Chinese negotiators have said they've agreed on a framework of how to implement the agreement reached at talks in Geneva last month. The main details came from Commerce Secretary Lutnick, who said that “We do absolutely expect that the topic of rare earth minerals and magnets” will be resolved and that export controls implemented by the US should come down as China approves relevant export licenses. China’s trade representative Li Chenggang said that the US and Chinese delegations will now take the proposal back to their respective leaders, with Lutnick noting that “once the presidents approve it, we will then seek to implement it”. At the same time, there was no evidence of progress on topics such as the fentanyl-related 20% tariffs on China that the US has implemented since February. So while the mood music has stayed positive, investors may be wary of the pattern that emerged during the previous US-China trade talks in 2018-19, when apparently constructive in person meetings seemed to take a step back as the negotiating teams returned to their capitals. So there's perhaps a little disappointment this morning that we haven't yet got a bigger announcement, even though there's time to hear the full conclusions of the meeting …

… Ahead of the CPI print, US Treasuries were pretty stable yesterday with an ongoing flattening of the curve. For instance, the 2yr yield (+1.6bps) moved up to 4.02%, whilst the 10yr yield (-0.4bps) fell to 4.47%, marking the flattest level of the 2s10s slope in two months. Those modest moves came amid an uneventful 3yr auction that saw $58bn of notes issued +0.4bps above the pre-sale yield. This will be followed by a 10yr auction today, and then a 30yr auction tomorrow, which will be an important focal point given recent fiscal fears …

10 June 2025 DB: The next focus for markets: Powell's replacement

In response to a question about who would be the next Fed Chair, President Trump recently noted that news on this could be “coming out very soon” (see here). Jay Powell’s term as chair does not expire until May 2026 – and his Board seat does not expire until 2028, allowing him to stay on the Board for longer if he chooses. However, Governor Kugler’s seat will be up in January 2026, allowing Trump to potentially use that seat to appoint Powell’s replacement.

While it may seem early to focus on this topic, our sense from client conversations is that once Congress passes the “big, beautiful bill”, which we expect by midJuly, and as we (hopefully) get further clarity on trade policy over the next few months, focus will shift to the person Trump chooses to next lead the Fed. Indeed, as the “very soon” comment suggests, the President may support the idea, initially proposed by Treasury Secretary Bessent, of appointing a “shadow Fed chair” well ahead of time.

Who are the leading candidates? Several names have frequently appeared in news reports (see here) of who Trump might consider for the next Fed chair:

1. Kevin Warsh, a Fed Governor from 2006 to 2011 and current fellow at the Hoover Institute,

2. Kevin Hassett, director of Trump’s National Economic Council (NEC), and

3. Fed Governor Chris Waller, current member of the Board of Governors.

Given how early we are in the process, we would not be surprised for other names to make their way into contention. Indeed, we have received several questions from clients about whether Bessent could consider switching roles and leading the US central bank.

What will Trump look for in the next Fed chair? Based on his recent comments, including his call for the Fed to cut rates by a full percentage point to provide “jet fuel” for the US economy (see here), President Trump is likely to prefer a candidate with dovish policy leanings. Interestingly, Warsh, who is seen as the leading candidate by betting markets, historically has a hawkish policy bias. For example, he has been critical of the Fed’s use of QE. More recently, Warsh criticized the Fed’s 50bps rate cut in September and the still-elevated size of the Fed’s balance sheet. Conversely, Governor Waller has professed more dovish views on policy recently, arguing that the Fed may be able to look through tariff-driven inflation and reduce rates. This assessment is confirmed by DB’s AI tool, which places Waller as the second most dovish official since the start of 2024, behind only Chicago’s Goolsbee (see “DB AI shows Fedspeak most hawkish since early 2023”). Less is known about Hassett’s monetary policy leanings.

A dovish tilt is not enough…

The coming market challenge. Regardless of the choice, the market is likely to test the next Fed chair’s independence and the credibility of his or her commitment to achieving the inflation target – a challenge that could be more serious if the candidate comes from within the administration. These bona fides always need to be earned by an incoming chair. However, the requirement could be more acute in the current context, with the President’s threats to fire Powell and calls for steep Fed rate cuts at a time when the economy is resilient, and inflation looks set to rise driven by tariffs. Market-based inflation expectations may rise in anticipation of this, and the next Fed chair will have to decide whether or not he/she will reinforce the Fed’s hard won inflation fighting credentials.

Challenge to be accepted shortly after choices name crossed DJTs lips? To be continued … Lets see what CPI today might offer and then if any / all the above react.

Ahead of today’s CPI, a bit of optimism (?) …

10 June 2025 ING Rates Spark: US CPI should be benign enough for a breather

The UK government's spending review should remind markets of the tight fiscal headroom, providing upward pressure on Gilt yields. In the US, there is also an eye on a tax-cutting package that poses fiscal risks down the line. But we should have a breather nearer term as the CPI data should be tolerable enough. But that will change as the tariffs kick in ahead

Ahead of today’s 10yr auction and CPI report, an idea (and a look ‘round the world…)

TIPS breakevens curve has steepened over the past two months as front-end inflation gets repriced lower. 10-year breakevens have scope to widen from here based on signals from FCI and beta-weighted breakevens. Potential downside surprise in May CPI print and crude oil prices can push 2y point lower.

Key takeaways

10y breakevens have scope to widen from here based on signals from Financial Conditions Index, equities and beta-weighted breakevens

CPI fixings are currently pricing in 13bp M/M headline inflation for the upcoming May print and 23bp M/M for core, which is lower than Bloomberg consensus

A potential downside surprise in May CPI and a decline in oil prices can push 2-year point lower than 10-year point

We like to express this view in CPI swap space as 10y iota spread is at the tight end of its range whereas 2y iota spread is at the wide end of the range

The key risks to this trade are a big upside surprise in core goods inflation or the effective tariff rate going higher from here

In May, we published our Mid-Year Outlook for the 2025-26 horizon. With the outsized trade shock, we see slowing growth around the world, firmer inflation in the US, and a divergence between the paths of the Fed and other central banks.

In the US, we see a sharp slowdown in growth, from 2.5% 2024 Q4/Q4 to 1.0% in 2025 and 2026. The tariff-induced inflation impulse comes sooner than the growth drag: We see core PCE peaking at 4.5% q/q saar in 3Q25, while growth stalls by 4Q25 and 1Q26 as tariffs and restrictive immigration weigh on the economy. On the back of the inflationary impulse, we see the Fed on hold throughout 2025. The easing cycle restarts in March 2026, and we see 175bps by year end 2026…

… from covered wagons on globalization …

June 10, 2025 Wells Fargo: The World Cleaving into Trade Blocs: Economic Effects of Deglobalization

Summary

Globalization has been in retreat for the past decade or so, and recent events suggest that deglobalization has further to run.

Deglobalization has had its roots in the geopolitical and economic competition between the United States and China. Recent events raise the possibility of further cleaving of the global economic order. Specifically, the possibility that the European Union goes in its own geopolitical and economic direction is no longer unfathomable.

We split the global order into hypothetical trading blocs to help us think about the potential economic implications of deglobalization. Using the Oxford Global Economic Model, we find that the effects on global GDP are essentially trivial if just the United States and China levy 15% tariffs on each other.

If the 35 countries in our US bloc slap 15% tariffs on the 32 countries in our Chinese bloc and vice versa, then the negative effects on the global economy are more significant. The model projects that the level of global real GDP under this "bipolar world" scenario would be 0.6% lower in 2029 relative to the baseline forecast that assumes no additional tariffs.

The hit to the global economy relative to baseline are more consequential in our "tripolar world" scenario in which the EU bloc levies its own 15% duties on the other two blocs, and they respond in kind. The level of global real GDP is 1.7% lower relative to baseline at the end of the decade. In nominal terms, global GDP is nearly $4 trillion lower than baseline in 2029.

If global "welfare" is measured by the level of global real GDP, then deglobalization, which we model as a world that has cleaved into trading blocs with tariffs imposed on the other blocs, is welfare reducing relative to a global economy that does not fracture.

… Finally, from Dr. Bond Vigilante, things gonna be alright …

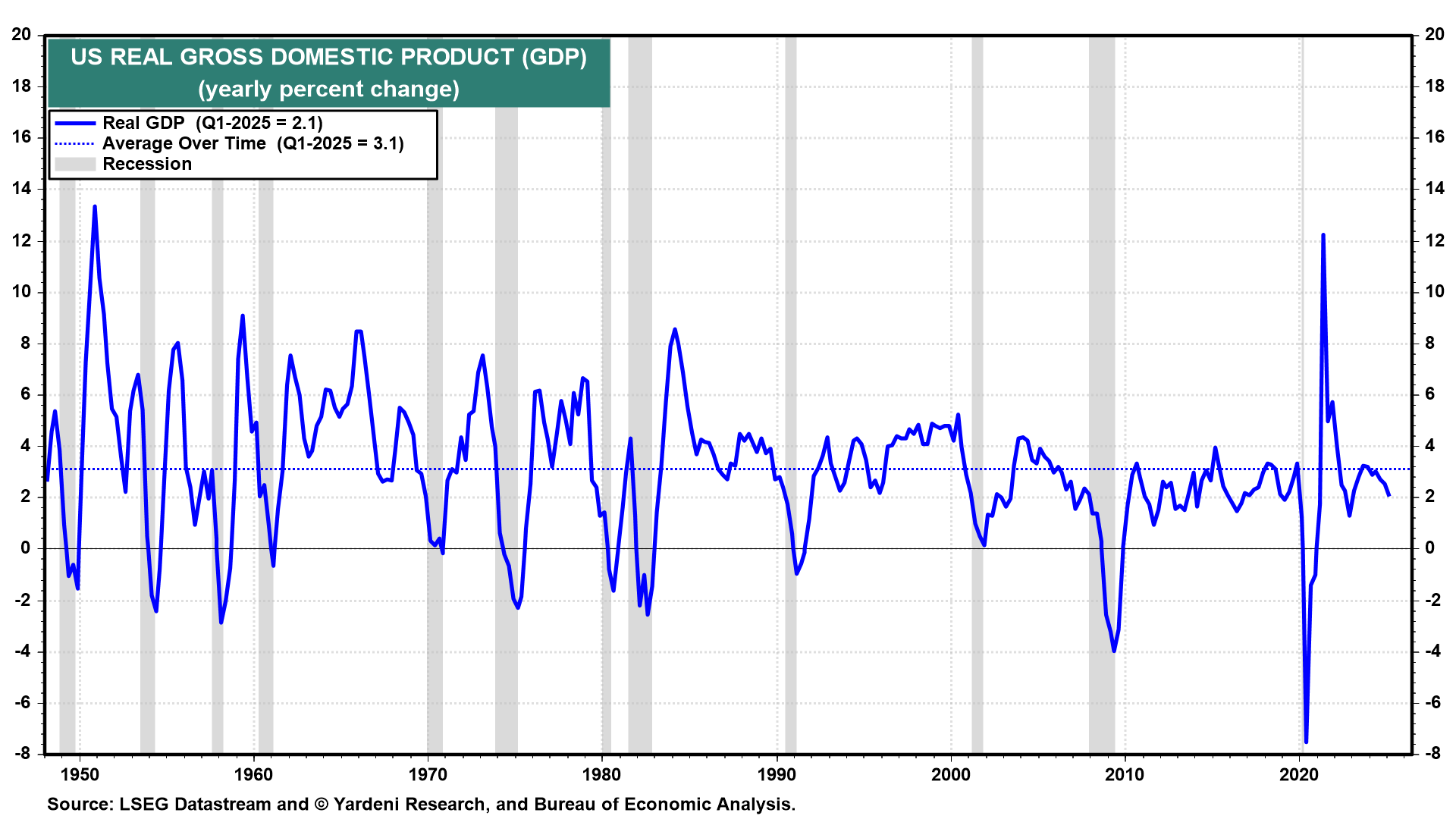

Jun 10, 2025 Yardeni: Betting On Bullish Hard Data, Not Bearish Soft Data

The “soft” economic data releases have been weak, while the “hard” data have been strong in recent months. The former includes surveys of consumers, small business owners, and purchasing managers. We've been betting on the resilience of the economy, as confirmed by the hard data. Stock investors seem to agree with our view.

The purchasing managers indexes for both manufacturing (M-PMI) and non-manufacturing (NM-PMI) remained weak through May. However, the M-PMI doesn't track the growth in real goods GDP as it did prior to the pandemic. The same can be said for NM-PMI and the growth in real services GDP. The growth of real GDP on a y/y basis remains solid (chart).

Measures of consumer confidence have also been depressed so far this year, especially the Consumer Sentiment Index (CSI). It remained so in May, while the Consumer Confidence Index rebounded smartly during the month. Meanwhile, consumer spending, which was depressed by colder than usual winter weather in January and February, bounced back solidly in March and April because the labor market remained robust…

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Positions. Lives. Matter …

June 10, 2025 at 8:30 PM UTC Bloomberg: Traders Boost Bets on Just One 2025 Fed Cut Ahead of CPI Data By Edward Bolingbroke

Traders are increasingly betting that the Federal Reserve will cut interest rates only once this year amid signs of resilient growth and sticky inflation.

Wednesday brings US consumer-price data for May, which is forecast to show a pickup that may reinforce the Fed’s wait-and-see stance toward further easing as it assesses the impact of tariffs. The central bank is widely projected to hold rates steady next week, and futures and options tracking expectations for its policy path show traders are moving to unwind the rate-cut premium built into the months ahead.

Swaps traders now see about 0.45 percentage point of easing by year-end, the smallest degree of reductions they’ve priced in since before President Donald Trump rolled out steep tariffs in early April. The announcement roiled markets and at one point in the following weeks led traders to wager on as much as a full point of Fed cuts by the end of 2025.

Stronger-than-forecast jobs data for May helped spur traders to exit easing bets. But the rate outlook had already been shifting in that direction, in part on hints of cooling trade tensions, which diminished further with talks between the US and China in London this week.

In options linked to the Secured Overnight Financing Rate, or SOFR, there has been a pickup in hedging activity targeting around just one or even no Fed policy moves this year.

Monday’s trading included heavy demand for hawkish protection via a range of structures looking to the end of this year and into early 2026, which Tuesday’s open interest showed were new positions. These types of wagers rise in value as rate-cut pricing fades from the futures underlying the options.

Here’s a rundown of the latest positioning indicators across the rates market…

… AND same web locale with a VIEW …

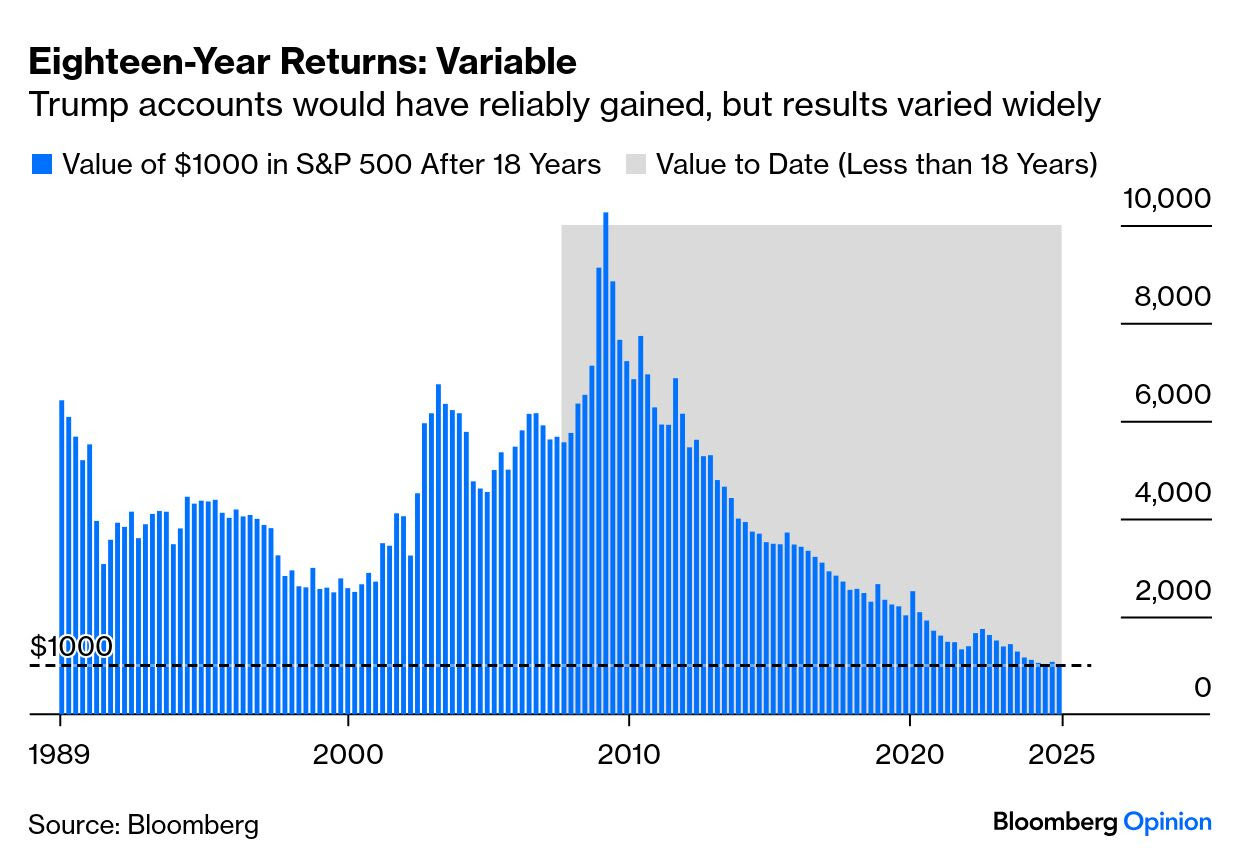

June 11, 2025 at 5:00 AM UTC Bloomberg: It's never too early to start a Trump Account A $1,000 investment fund for kids, untouchable until they reach 18, is a worthy idea.

… That leads to one of the prettier parts of the One Big Beautiful Bill. It would create Trump Accounts — every newborn American would receive $1,000 invested in a tax-privileged index fund, not to be touched before they turn 18. The man’s determination to put his name on things may grate, but this is a sensible idea.

The amount isn’t much more than a symbol, although over 18 years it’s likely to grow into a sum that could genuinely help young people embarking on their lives. During an 18-year span, the S&P 500 is overwhelmingly likely to deliver you a profit, and the discipline of having to leave the money untouched is a good life lesson. Going back to 1989, Trump Accounts would never have lost money by the time their holders came of age, and always made gains of at least 150%. That said, structuring it as a one-time payment adds risk. This is the 18-year total return of the S&P, starting in each quarter since 1989 (with returns to date for accounts that started less than 18 years ago):

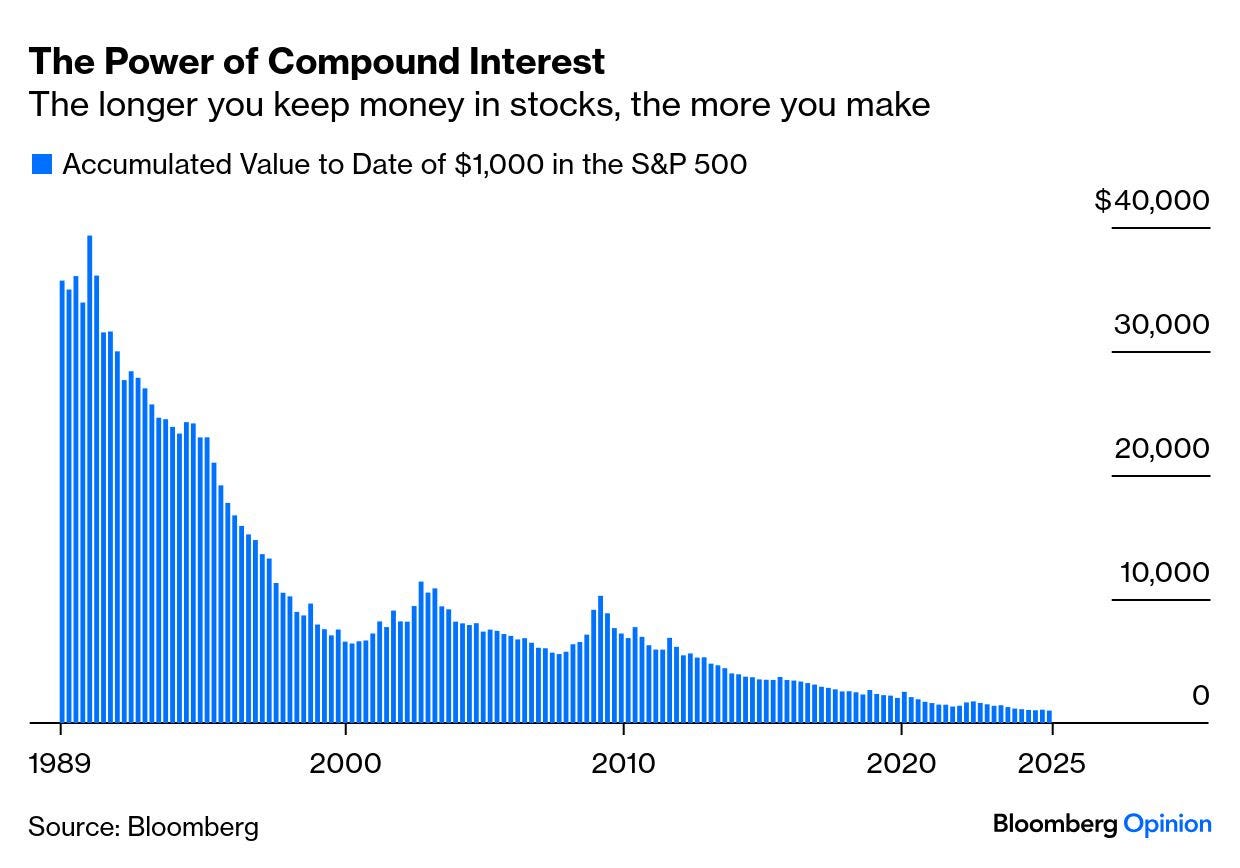

The nest eggs for anyone born in late 2008 or early 2009 would have been mightily impressive — which might be a hint not to trust this rally to keep going much longer. History also shows better returns for those who wait. The gains for those who bought after Black Monday in 1987, but before the 1990s bull market took hold, illustrate the power of compound interest, and patience:

Business executives are keen to back the idea, with many promising to top up the Trump Accounts of children born to their employees. The more obvious disadvantages apply to many other things: The accounts will be passive to keep costs down, so at the margin will amplify the distortions already caused by index funds. They provide a prod to invest in the US at a time when returns might well be better elsewhere — this proposal buttresses the move toward “national capitalism” and away from globalism.

The history of such ideas is patchy, understandably as they cost public money. Tony Blair’s government operated a similar program in the UK between 2002 and 2010 known as the Child Trust Fund(not the Blair Account for some reason). While the US is providing a universal basic amount, the British plan was means-tested, with bigger allocations for children born into poor backgrounds. And it built on the UK’s popular existing “baby bonds,” life assurance policies for newborns.

The UK plan ultimately fell victim to the financial crisis, growing steadily less generous before it was shelved by the Conservatives in 2011. Sadly, there are now websites to help you find your child fund, so people seem to have found it hard to keep track. Trump accounts might easily meet a similar fate.

But there are positives. It makes sense to encourage children to buy and hold and show them it works. And it’s a far better idea than giving teenagers trading accounts.

… THAT is all for now. Off to the day job (back to regular spammation Friday) …