Good morning … yesterday was the proverbial day ‘bout nothing (see Dr. Ed’s commentary below) and more than likely due to the EZ celebrating May Day. With holiday theme in mind AND with Japan out overnight, calm (before the storm) impact on flows / liquidity remains.

That said (and stealing some thunder from an early morning REID, below) …

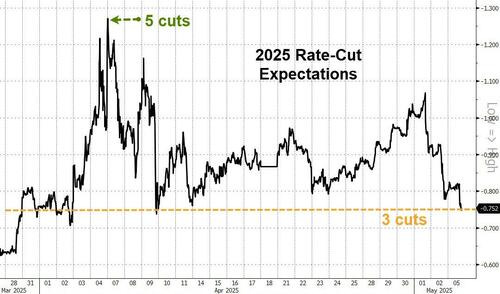

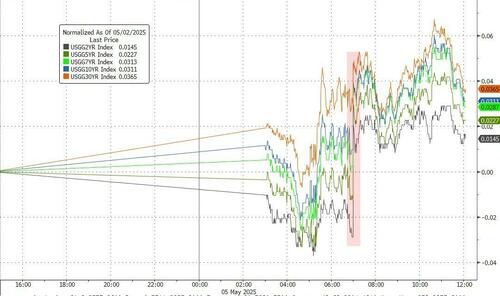

… The stronger data saw markets pare back their expectations of near-term Fed rate cuts. Notably, only 23bps of cuts are now priced by the July meeting, which is the first time since late February that the next cut is less than fully priced by July. The amount of cuts priced by year-end fell by -4.0bps to 76bps. Treasury yields moved higher, especially at the long end, with the 10yr up +3.5bps to 4.345% and the 30yr up +4.6bps to 4.835%. An +18.2bps rise in 10yr yields over the past three sessions may place some extra attention on today’s 10yr auction. There has been no trading overnight due to a Japanese holiday …

… one mans selloff in the 10yr note is another’s concession into this afternoons $42bb 10yr auction … Let’s help Secy Bessent put the FUN in reFUNding …

10yy DAILY (monthly HERE): support is nearby (4.375% or thereabouts) …

… while momentum REMAINS BEARISH and i’ve got more questions (noted) than answers … I will note trend(lines) are your friend ‘til they bend (and so I’ve taken liberty to redraw TLINE support in effort to try and find some level — concession — of support to watch into this afternoons $42bb 10yr auction …)

… AND In as far as some of the funTERtaining data points helping create the price action … Services beat and USTs bear steepened …

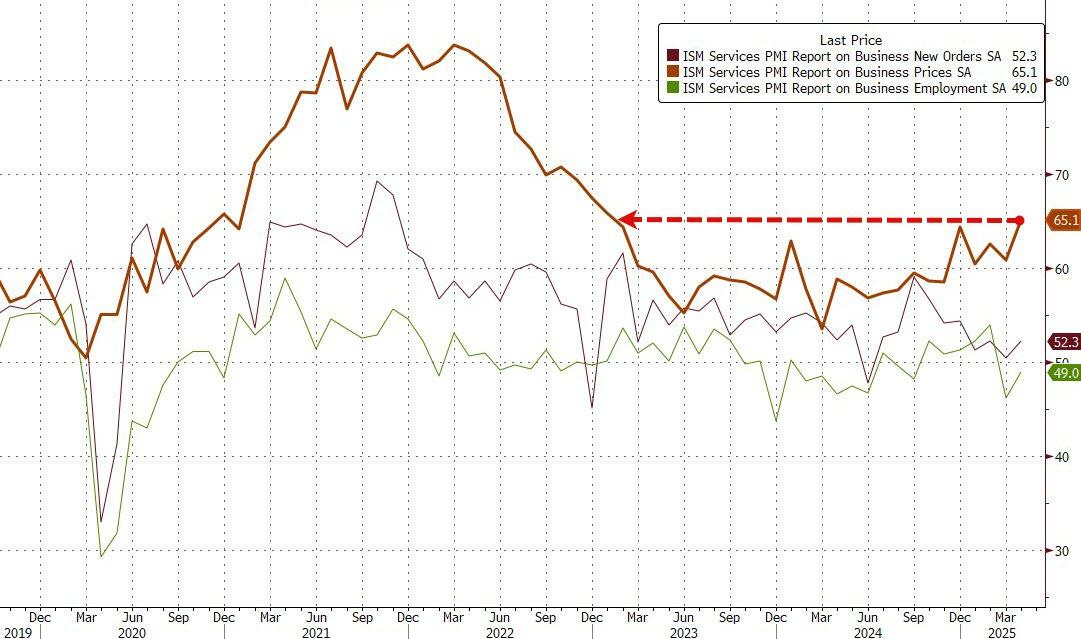

ZH: ISM Services Survey Surprises To Upside As Prices Paid Surge

… The ISM print was better than all but one expectations...

Under the hood, the picture is not so pretty with Prices Paid at the highest since Jan 2023 (even though New Orders and Employment picked up modestly)...

“The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for April (51.6 percent) corresponds to a 1-percentage point increase in real gross domestic product (GDP) on an annualized basis,” according to PMI.

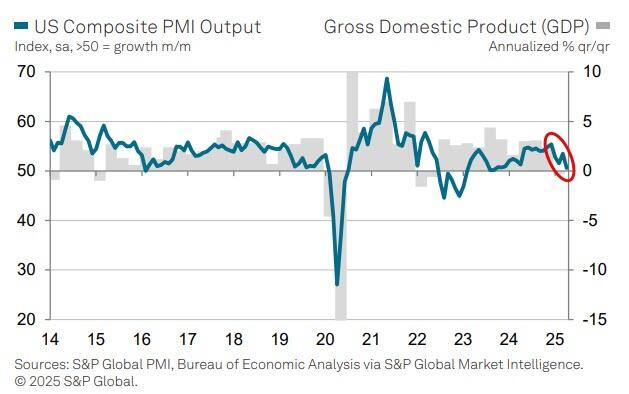

The S&P Global US Composite PMI® fell to 50.6 in April, down from March’s 53.5 and its lowest level since September 2023.

"While tariff announcements mean manufacturing dominates the news, a worrying backstory is developing in the vastly larger services economy, where business activity and hiring have come closer to stalling in April amid plunging business confidence," Chris Williamson, Chief Business Economist at S&P Global Market Intelligence warns that:

"Business and consumer facing service providers alike, and especially financial services firms, are reporting markedly weaker growth prospects, citing intensifying uncertainty over the economic outlook amid recent tariff announcements and ongoing federal spending cuts."

"A key area of weakness is slumping exports of services, which is now falling at rate not seen since 2022, but domestic demand is also reportedly waning as confidence slides lower.

But the stagflationary aspects seen in the Manufacturing survey are also showing up in Services...

"Higher prices paid for imports due to tariffs are also driving up service sector firms’ costs, feeding though to higher prices, notably in consumer-facing industries such as restaurants and hotels.

"The resulting bottom line from the services sector is a heightened risk of stalling growth and rising inflation, or stagflation."

Bad enough news for Fed cuts? Or hot enough stagflation to leave Powell on pause for longer?

… AND movin’ right along for somewhat more on MIXED data and rate cut interpretations …

ZH: Gold Gains, Crude Crushed As Stocks' Big Win-Streak Ends Abruptly

…Mixed PMIs today but all the focus was on ISM data showing strength overall and Prices Paid accelerating...

That sent rate-cut expectations still lower, now pricing in just 3 cuts this year...

…Treasuries were sold during the US session with ISM's Prices Paid sparking yields to jump notably higher...

AND I’m done … I’ll quit while I’m behind … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries saw another relatively slow start with Tokyo out again, spreads drifting tighter on the back of better receiver flows across the curve, with the curve saw initial steepening before better flattening flows arrived in London in 2s5s, 2s10s and 5s30s. Our desk also saw FM receivers of 5s10s30s vs payers of 2s5s10s on both spot and fwd structures. USTs are largely unchanged as we enter the US session, mildly outperforming Bunds as Merz fell short of a majority in German parliament. We see activity levels in both US and EU running below 1mth historical averages - UST around 20% lower, EGB around 10% lower (but more than 50% at the front end). S&P futures are showing -0.6%, Crude Oil +2.4%, DXY -0.1%, Gold +1.3%, and 2s10s curve +1bps steeper…

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Sentiment hit after HKMA says it is diversifying into non-US assets, Bunds volatile on Merz … USTs are holding around the unchanged mark in a 110-27+ to 111-03 band. Came under modest pressure overnight on the return of China and generally supportive tone, despite weak Chinese PMI; though, once again, Japan was on holiday and as such conditions were thinner than normal with no cash trade. Into the European morning, USTs began to pick up alongside fixed income generally amidst commentary from the HKMA that they are diversifying into non-US assets. The update had more of an impact on US equity futures and the DXY than it did on Treasuries. Ahead, supply is the main scheduled event stateside in the form of a 10yr tap. Follows Monday’s 3yr sale which was much better than the prior.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Alternative data, you say? Well, then … today’s yer luck day …

5 May 2025 Barclays: High-frequency alt data: Services spend pullbacks

High-end shoppers look to be pulling back more in the past few weeks of data than discount shoppers, for services categories including travel. Goods spend had been holding up, but the front-running in motor spend ended abruptly, with spending falling below seasonal momentum.

Best in show recap of data (and the day that was)…

May 5, 2025 BMO: ISM Services 51.6 vs. 50.3 expected -- TSY sell off

…The release noted that "Regarding tariffs, respondents cited actual pricing impacts as concerns, more so than uncertainty and future pressures." Overall, it was a report that was definitely strong and reinforced the idea that the US is entering the trade war on solid footing…

May 5, 2025 BMO Close: Reckoning with the Refunding

… Monday’s selloff extended the recent backup in Treasury yields as the market readies to absorb the 10-year refunding auction. An unexpected bounce in ISM Services activity pushed rates higher, with the update on business sentiment reinforcing the understanding that the US economy is entering the trade war on solid footing. In the wake of a solid pre-auction concession that left yields at the session highs, the 3-year auction stopped-through by 0.2 bp and nondealers took an above-average allocation of 86.1% – a solid departure point for the quarterly refunding process. The 20 bp climb in 10-year yields since the end of April bodes well for investor demand in the primary market for tomorrow’s 10-year offering. While further supply-driven cheapening should be on the radar as a classic pre-auction concession, we remain constructive on this week’s marquee supply event and anticipate solid sponsorship from endusers, regardless of the direct/indirect bidding breakdown …

… 10-year yields reached as high as 4.369% on Monday and we’re watching for support at an opening gap from 4.371% to 4.381% as the new supply comes into focus. Note that daily stochastics are mid-range with a bias for higher rates in the near-term. Should we see the aforementioned gap filled, there is another unfilled trading zone from late-April at 4.395% to 4.401%, above which is the all-important 100-day moving-average of 4.411%. In the event of a bullish reversal, the 200-day moving-average comes in at 4.223% with the month-end/local yield low close from April 30th at 4.162%. If that level is traded through, 4.120% was the yield low mark reached in the wake of last Thursday’s spike in jobless claims and through there, resistance is sparse in the path back toward 4.0% …

With growth apparently holding up well and serious inflation risks on the horizon, we expect the FOMC to remain on hold this week.

Chair Powell will likely say policy is well positioned “for the time being,” indicating that a rate cut in June is not the base case.

We see market pricing for cuts as directionally consistent with recessionary tail risks and not as a “problem” Powell needs to “solve.”

An update from a shop and a stratEgerist who had the day off, yesterday and a note asking / attempting to answer question ‘bout why stocks bounced AND what next …

… Yesterday’s reversal in equities came despite a decent ISM services release for April that pointed to a still resilient US economy and followed a solid payrolls print last Friday. The headline index unexpectedly rose from 50.8 to 51.6 (vs. 50.2 expected), with new orders rising to a 4-month high of 52.3. The ISM survey also pointed to elevated price pressures, with the prices paid index rising to 65.1, its highest level since January 2023.

The stronger data saw markets pare back their expectations of near-term Fed rate cuts. Notably, only 23bps of cuts are now priced by the July meeting, which is the first time since late February that the next cut is less than fully priced by July. The amount of cuts priced by year-end fell by -4.0bps to 76bps. Treasury yields moved higher, especially at the long end, with the 10yr up +3.5bps to 4.345% and the 30yr up +4.6bps to 4.835%. An +18.2bps rise in 10yr yields over the past three sessions may place some extra attention on today’s 10yr auction. There has been no trading overnight due to a Japanese holiday.

Those moves come ahead of tomorrow’s Fed decision, where our US economists expect the FOMC to keep rates steady and avoid explicit forward guidance about the policy path ahead. They continue to see the next rate cut coming in December and while risks are tilted towards earlier easing, in their view this would require a clear weakening of the labour market. See our economists’ full preview here. Central banks will also be in focus in Europe this week, with policy decisions from the UK, Norway and Sweden all due on Thursday. Our UK economist expects the BoE to deliver a 25bp cut (see preview here), while Norges and Riksbank are expected to keep rates on hold.

06 May 2025 DB Mapping Markets: Why has this sell-off unwound so quickly, and what now?

Given the market turmoil after 'Liberation Day', one of the most surprising features was how quickly the sell-off unwound. The S&P 500 has almost entirely erased its losses since April 2, as has the STOXX 600 in Europe. US credit spreads have pared back most of their widening. And, whilst long-end Treasury yields have moved a bit higher, it doesn’t stand out relative to the last couple of years.

This is very positive from an economic standpoint, because the market recovery means we’re more likely to avoid the negative wealth effects and tighter financial conditions that follow from that. So by itself, the lack of a big market correction actually makes an economic recession less likely as well.

Looking forward, this situation has a lot of echoes of last summer. Back then, the data deteriorated sharply, and markets were briefly in turmoil as investors genuinely feared whether the US might head into a downturn. The Fed even cut by 50bps in September. But, as it became clear a recession would be avoided and the data wasn’t contractionary, markets recovered very quickly. Many of those parallels have been playing out again today. We also look at some other lessons, and note this isn’t the first time that serious doubts have been raised about US exceptionalism.

…So why did the sell-off unwind so quickly? 1. Despite widespread fears of a recession, the data simply hasn’t backed that up so far…

…2. Lower oil prices are acting as a stimulus for consumers, and by reducing inflationary pressures they’ve also helped to keep the prospect of rate cuts alive…

…3. Policy shifts have made a recession less likely, including the 90-day tariff extension, whilst there’ve been positive noises on trade deals…

…4. Equity positioning had become very underweight after the initial sell-off, whilst the outperformance of the Magnificent 7 since 'Liberation Day' (as in 2023-24) has lifted the S&P 500 more broadly…

…The fact that markets have unwound the losses is very positive from an economic standpoint…

…So what lessons can we take from this? 1.This situation has several echoes of last summer, when markets were briefly in turmoil, but a strong bounce-back followed…

…2. Some have argued that it would be bearish if we don’t get the rate cuts that are priced in. But recent experience has shown that can still be positive if the reason for that is upside growth surprises….

…3. This might be an unloved rally, but plenty of unloved rallies have gone on for some time…

…4. This is not the first time we’ve heard a narrative around the end of US exceptionalism…

… short term OK, long term …

May 5, 2025 First Trust: No Recession Yet, But Risks Remain

Noise about tariffs, business uncertainty, a constitutional fight, and a drop in stock prices had already created fear of a recession. When real GDP declined in the first quarter of 2025, some started to question if a recession is already here. Let’s take a deep breath and consider the facts.

Yes, real GDP dipped at a -0.3% annual rate in Q1, the first decline for any quarter since 2022. But the main reason was that trade with other countries accounted for the largest drag on the economy for any quarter since at least 1947, as both consumers and companies loaded up on goods from abroad before higher tariffs kicked in. Since GDP is designed to measure domestic production, imports are subtracted even though Americans buy them because they were produced abroad. We aren’t saying GDP is a flawed statistic, we are saying it needs to be viewed correctly…

…Another signal that the US wasn’t in recession in the first quarter was that industrial production was up at a 5.4% annual rate while manufacturing rose at a 5.1% annual rate…

Gold gains as USD weakens; USTs bear-steepen after beat in ISM services; AUD gains after the weekend's election; softer-than-expected Swiss inflation; TWD extends sharp gains; oil prices fall after OPEC+ agrees to production cut; DXY at 99.78 (0.2%); US 10y at 4.343% (+3.5bp)

…USTs bear-steepen (2y: +1bp; 30y: +5bp) after an unexpected improvement in the ISM Services survey; the sell-off loses momentum after the 3y UST auction comes 0.2bp through the when-issued yield…

Of course this next note is from Paul…see, sir, whatever side you’d like to see …

The manufacturer of Barbie dolls has warned that higher prices are coming to US consumers, as a direct consequence of tariffs. Moving production to the US does not seem to be an option. Rationing dolls to two per child while raising prices has limited consequences, but US President Trump has signaled medicines will be next. Rationing medicines with higher prices may have more significant consequences (raising health insurance prices, for instance).

US March trade data is due. In the past, this was almost ignored by markets, but politics has elevated the status of trade. Being March data, this reflects the before times, and will probably show a sizeable deficit as companies and consumers rushed to buy before tariffs forced them to hand over sizeable amounts of money to the US government…

… and one of THE 64k dollar question asked by covered wagons (along with a precap of NEXT WEEKS CPI)…

May 5, 2025 Wells Fargo: A Reprieve in ISM Services, Will It Last?

Summary Service-providers are by no means immune to tariffs, even if the impact is less direct than for manufacturers. The ISM Services Index rose slightly in April, but prices paid rose to a two-year-high and business activity slowed.

May 6, 2025 Wells Fargo: April CPI Preview: The Trend Is Your Friend

Summary After an unexpected slide in March, the monthly change in the CPI in April is likely to rebound to its six-month trend. We look for the headline CPI to rise 0.2% in April, leading the year-ago rate to dip to a four-year low of 2.3%. We would not be shocked to see a 0.3% rise if some volatile components bounce back more than expected. Excluding food and energy, we forecast the core CPI to rise 0.25%, keeping the annual rate unchanged at 2.8%. Preemptive inventory building and fears of consumer pushback should keep the anticipated acceleration in consumer prices at bay until at least May. Yet beneath the surface, the subsiding trend in core services inflation will be juxtaposed with core goods inflation that is incrementally strengthening.

… Finally, no wonder I don’t have much to say (above), as Dr Bond Vigilante notes …

May 5, 2025 Yardeni: A Seinfeld Kinda Day: Nothing Really Happened

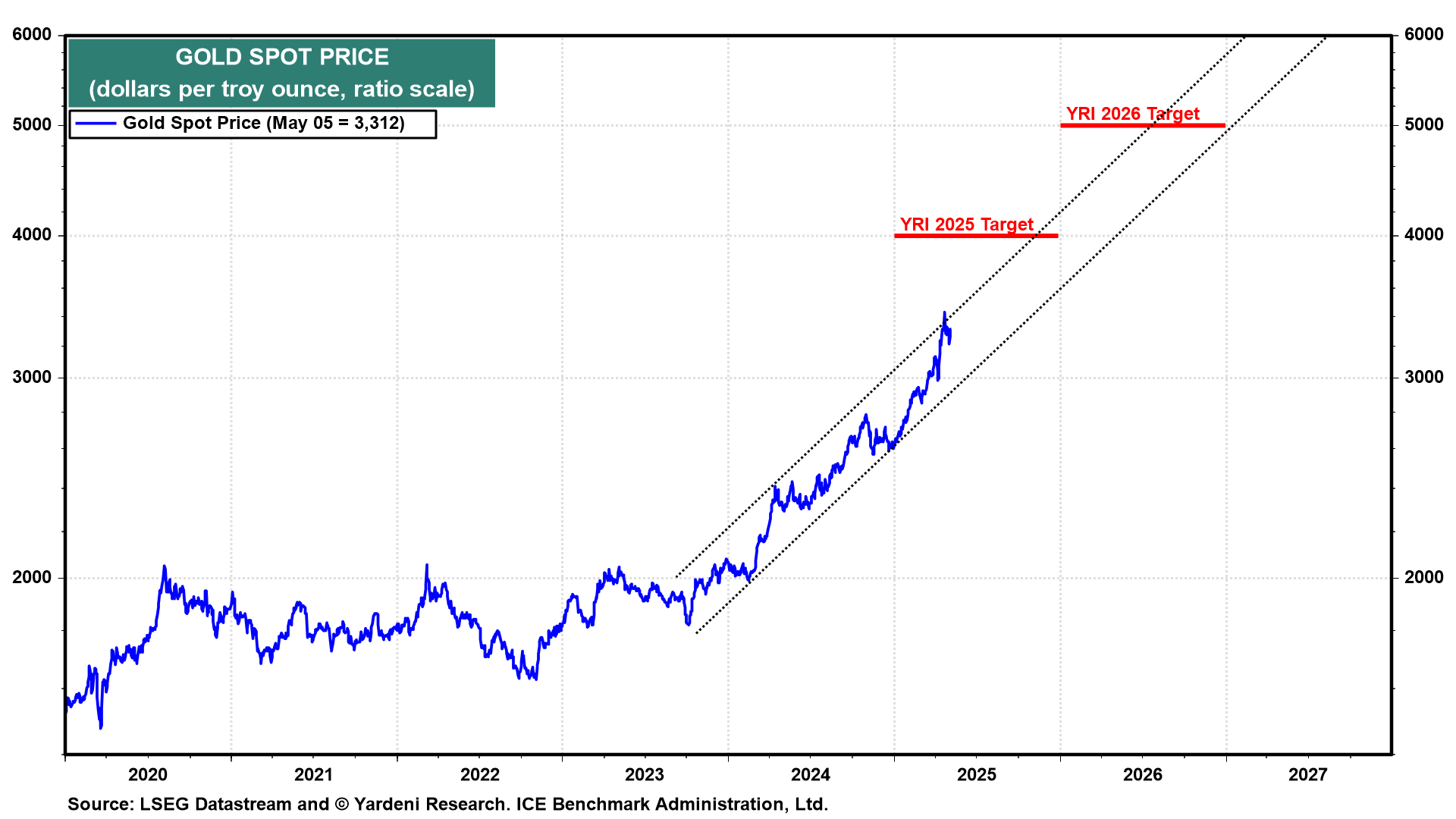

Not much happened today in either the stock market or the bond market. Dull days are good for a change. The markets are no longer responding to every comment coming out of the White House. On Sunday, President Donald Trump called Fed Chair Jerome Powell "a total stiff." But he also said that he will not remove the Fed Chair. Today, Treasury Secretary Scott Bessent observed, "The United States is the premier destination for international capital." The dollar index (DXY) edged up slightly. On the other hand, the price of gold jumped sharply higher to $3386.60 this evening (chart).

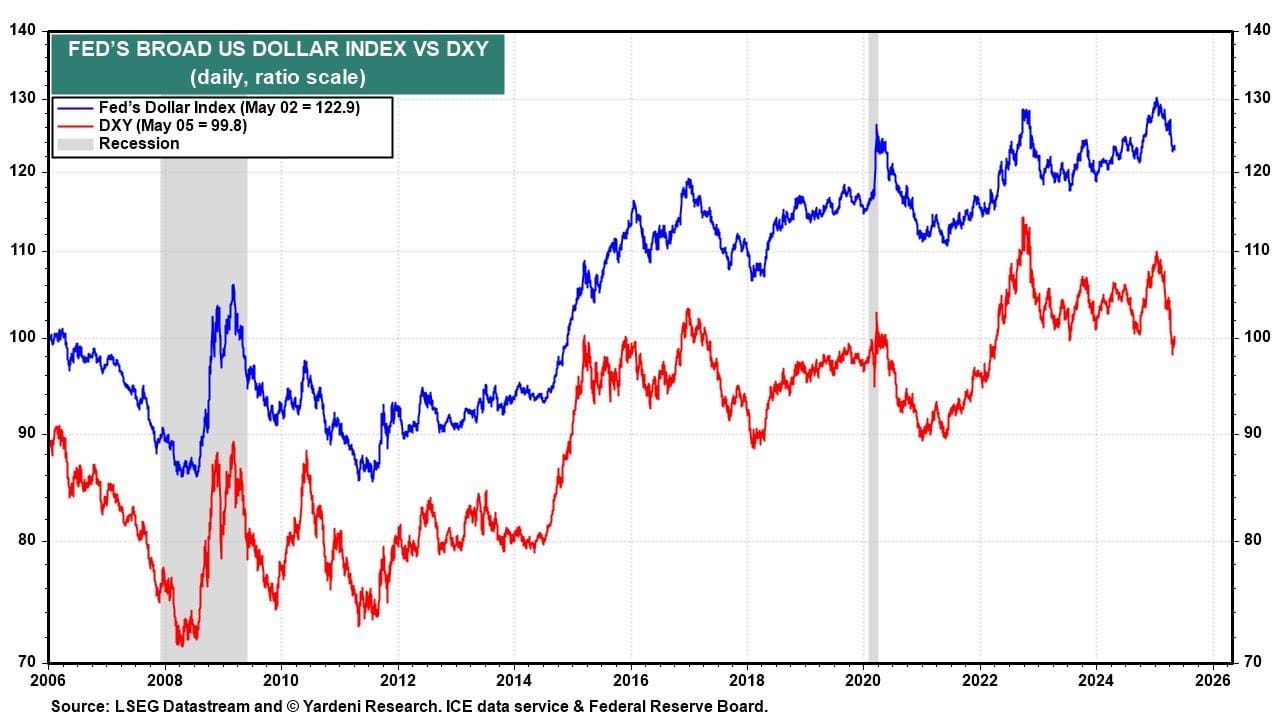

The Fed released last week's daily readings for the "broad" trade-weighted dollar. It hasn't been as weak as DXY, which is a fixed-weight currency index with the euro having a weight of 57.6% (chart)!

Not to dismiss the recession debate that seems everywhere you turn these days, but it's beginning to give off a "yadda-yadda-yadda" energy. Chatter about a tariff-driven downturn often seems at odds with the data and market dynamics. Case in point: the yield curve is ascending (chart). That doesn't tend to happen before an economy slides into the red.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Wing-O-metrics insight and translation into what we are all wanting to know …

May 5th, 2025 SurplusProductivity: Here's What The Treasury Market Is Really Saying

Anywhere but in the lurch

Professional business services productivity max

No escaping the economic procession

As we pointed out in Friday’s missive, last week’s employment report is emblematic of a much bigger problem in the economy few, if any, care to, assuming they’re even able to really address. The economy is in much too volatile of a place for the data to do much of anything with regard to accuracy. While on the surface this might not seem like to all much of a problem for no time limit exists on the economy. But that’s a half-truth as decisions still need to be made, or decided to be not made, regardless of how long it takes for everything to get sorted out in the wash. The problem is, it is taking much, much longer for the economic truth of the matter to be discovered; leaving all in the lurch which is about as far from anywhere you’d like to be when it comes to understanding the economy and its needs. The unpleasant nature of the lurch, in fact, has been what the U.S. Treasury yield curves have been communicating about for some time, leaving the uncomfortable impression that the gap between what the economy is doing and what it should be doing is growing further by the moment.

The current breakdown in the yield curve correlation signals a deeper problem.

Flying blind might seem apropos when attempting to ascribe the current situation of unusable economic data and projecting the economy…

May 5, 2025 WolfST: NY Fed’s “Multivariate Core Trend” Inflation Measure Hits 3.0%, Worst in Over a Year, Predicts Acceleration of PCE Price Index

Driven largely by non-housing services. Just in time for the Fed meeting.

Back in April 2022, when the Fed’s favored inflation measure, the PCE price index, was surging towards its June 2022 high of 7.2% year-over-year, and core PCE to a high of 5.6%, the New York Fed came out with an inflation measure to track inflation’s “persistence.”

This “Multivariate Core Trend” (MCT) inflation measure is based on the some components of the PCE price index, but aggregates them differently. This MCT inflation rate, on a year-over-year basis, decelerated sooner than the core PCE and overall PCE inflation measures in 2022 and 2023, in effect successfully predicting their deceleration months in advance. And now it is predicting the resurgence of PCE inflation.

The MCT inflation rate for March accelerated to 3.0% year-over-year, the worst reading since February 2024 (red in the chart), according to the New York Fed today. The re-acceleration was driven largely by non-housing services and to a small extent by “core goods” components, even as the Fed-favored core PCE inflation (blue line) and overall PCE inflation (purple dots) decelerated year-over-year (my discussion of PCE inflation for March).

… and finally, from ZH, a Goldilocks > Muppets zinger …

ZH: What Recession: Goldman Now Expects Q2 GDP To Surge To 2.4%