while WE slept: USTs 'modestly twisting steeper'; 'mkt removing CB CUTs'; "Disinflation Dissipating: reflation risk rising..."

May 28, 2024

Good morning … #Got2s? How about 5s?

Beginning our holiday shortened week with (not so) new, improved and much shorter by half SETTLEMENT OF TRADES …

Bloomberg: Wall Street Returns to T+1 Stock Trading After a Century (welcome to the club as bonds, best I reckon, was and remains T+1 with CASH … ie same day … always an option …)

Trades will settle in one day for the first time in 100 years

SEC sees potential for ‘short-term uptick’ in failed deals

… Lets start by ripping the <supply>bandaid off — a couple of WEEKLY visuals HERE which aren’t necessarily confidence inspiring BUT … perhaps a bit of early HOPE will shine through (or more of a concession) and entice folks (Team Rate CUT kindly step up to the SUPPLY plate) to buy ahead of week - ending PCE …

2s DAILY look overSOLD (concession then makes 2s a decent looking rental)

5s DAILY look overSOLD (concession then makes 5s a decent looking rental)

… and away we go but first, here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly twisting steeper with a bit of long-end softness seen in Tokyo on a poorly subscribed auction and some CTA paying. Some less market pertinent comments were seen from Bowman and Mester ahead of the London open, with focus to shift towards the double-barrel supply later with $69bn new 2s and $70bn in new 5s (14y and 17y supply in Germany as well). Some steepeners and payers of 2s5s10s were seen from FM accounts in swaps. Commoditiess are well bid here at 7am, with CL +1.6% and HG +1.8% as well. APAC bourses were weak, with SHPROP leading downside at -2%, while SHCOMP dropped -0.5%, the NKY close to flat at -0.1%. DAX futures are flat, with S&Ps +0.1% currently…

… Conf Board Expectations - Present Situation Spread vs 2s10s Curve: our longstanding favorite coincident curve indicator, still suggestive of consolidation after making a trough in Q2 2023.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: US equity futures in the green, USD softer & Crude bid amid heightened geopol tensions; Fed speak due … USTs/Bunds are mixed and relatively contained, whilst Gilts outperform playing catch-up to Bund strength in the prior session … USTs are modestly firmer but with action relatively sparse and overall rangebound into a particularly busy week highlighted by PCE on Friday; docket for today is sparse, but focus will be on US 2yr & 5yr supply. Currently trading within a tight 108-28+ to 108-22 range.

We examine the gap between the CPI and PCE core inflation measures, which remains much wider than historical norms. Stepping back from month-to-month fluctuations, we focus on the broader drivers of recent swings in these indicators, key contributors, and implications for the upcoming inflation trajectory.

… We expect the gap between core CPI and core PCE price inflation to unwind only gradually. The weighting-related portion of the CPI-PCE gap from shelter is likely to persist this year, as we forecast only a modest deceleration in shelter inflation. In addition, while both the CPI and PCE measures of healthcare services inflation have accelerated since late last year, the CPI measure has increased more rapidly, reflecting private insurance costs, while the PCE measure has been held down by prices under government-sponsored health programs, which are usually slower to adjust. Finally, we think the firming in the out-of-scope components in the PCE in Q1 may be hard to sustain, which would help narrow the gap slightly. Our forecast implies a gradual narrowing of the gap to about 50bp over the course of 2024, with core CPI up 3.4% Q4/Q4 and core PCE up 2.9% Q4/Q4 at end-year. We expect the gap to normalize toward historical averages in 2025, with core CPI up 2.6% Q4/Q4 and core PCE up 2.3% on a Q4/Q4 basis.

… Bottom Line: Everything that can happen to the global economy will happen, but the fraction of “world lines” where a soft landing occurs is unlikely to be very high. Stocks could still rally for a few more months if concerns over inflation subside before concerns over a recession resurface. However, the equity bull market is getting long in the tooth.

Brent and WTI: Oil prices have come very close to the very pivotal 200w MA support. From here, the case for a short term move higher is much stronger:

Firstly, both Brent and WTI have come close to testing support at the 200w MA (79.85 and 75.86), which has held since 2023. This provides a strong base for price to bounce higher from, and will likely limit weakness even though weekly slow stochastics continues to move lower. At the same time, we flag that there is a potential double bottom formation in both charts with necklines at 84.49 and 80.60 for Brent and WTI respectively. These also coincide with the 200d MA resistances.

IF we see a bounce higher off the 200w MA base and break past the double bottom necklines, it would suggest gains of >4% towards 87.93 for Brent and 84.50 for WTI…

…WTI Futures:

OTHER TECHNICAL DEVELOPMENTS WORTH NOTING … US 2y yields: Contrary to our expectations, yields broke past 4.89% (May 14 high) sharply last Thursday. This brings focus onto the ~5% handle which holds a series of resistances (76.4% Fibonacci, psychological level, April highs). While we retain our bias for lower yields, we turn much more cautious here with weekly slow stochastics on the verge of crossing back higher.

US 10y yields: We have held below the 4.49%-4.53% resistance range (Apr 19 low, May 14 high, psychological level). We continue to think a medium term dip in yields is likely after crossover from overbought territory in weekly slow stochastics. This is supported by the weekly evening star in early May and bearish outside week the week prior. Key support to watch is 55w MA at 4.22%

… German IFO missed, steady at 89.3 in May, consensus looked for a 1pt rise. Current situation index weaker, offsetting a small rise in expectations. Despite the miss, the trend improvement over recent months is consistent with a modest activity recovery in Q2…

… Chart of the day Germany IFO weaker than expected in May; but trend improvement in recent months points to activity rebound in Q2

Echoes of tariffs past and prospects for the future mean that the theme will be with us for a while. We revisit the 2018 tariffs to sift through various effects.

ECB Chief Economist Lane stated the central bank is ready to cut rates. We have heard this from other ECB governing council members, but Lane’s remarks come with the added authority and insight that only a chief economist can bring. Europe has (on a like-for-like basis) the same inflation as the US or the UK, and the ECB is not known for the speed of its decision-making. That the ECB looks to be first to cut rates may be due to the narrative around European growth, rather than the substance of economic data.

There are expectations of easing in the Anglo-Saxon world. The Federal Reserve’s Beige Book of anecdotal evidence is due on Wednesday and should point to a need to ease. This report may be increasingly vulnerable to politically partisan distortions, however…

Wells Fargo: Commercial Real Estate Activity Remains Challenged by High Interest Rates

Commercial Real Estate Chartbook Summary High interest rates continue to loom large over the commercial real estate market. In particular, tight monetary policy remains as a considerable headwind for construction, transaction volume and valuations. Although still a challenging environment, there are plenty of reasons for cautious optimism that a turnaround is on the horizon. If economic growth remains sturdy as we currently expect, then CRE demand should also stay afloat. Meanwhile, the pullback in new development suggests supply is adjusting to the current demand environment. What's more, the slower pace of price declines is a sign that the air of pessimism surrounding the asset class is beginning to dissipate as less restrictive monetary policy comes closer in view. While not likely a panacea, lower interest rates and more certainty on the direction of policy moving forward should help the commercial real estate market find more secure footing.

… And from Global Wall Street inbox TO the WWW,

Apollo: This Economy Is Not Slowing Down (um … so Team Rate Cut then NOT gonna stand up and buy 2s or 5s, at least not without more concession?? asking for a friend…)

Earnings growth is a three-quarter leading indicator for capex spending, and the continued strength in earnings suggests that we will see a strong rebound in business fixed investment over the coming quarters, see chart below.

Apollo: Market Gradually Removing Central Bank Rate Cuts (um … so Team Rate Cut then NOT gonna stand up and buy 2s or 5s, at least not without more concession?? asking for a friend…)

At the beginning of the year, the market was pricing six Fed cuts this year, six ECB cuts, and five BoE cuts, see chart below.

Today, the market is pricing two-and-a-half cuts by the ECB and the BoC, one-and-a-half cuts by the Fed and the BoE, and only half a cut by the RBA.

With inflation still a problem and continued strong tailwinds to the US economy from easy financial conditions and expansive fiscal policy, we continue to expect zero Fed cuts this year.

Bloomberg(via ZH): Yields Will Stay Higher For Longer With Commodities

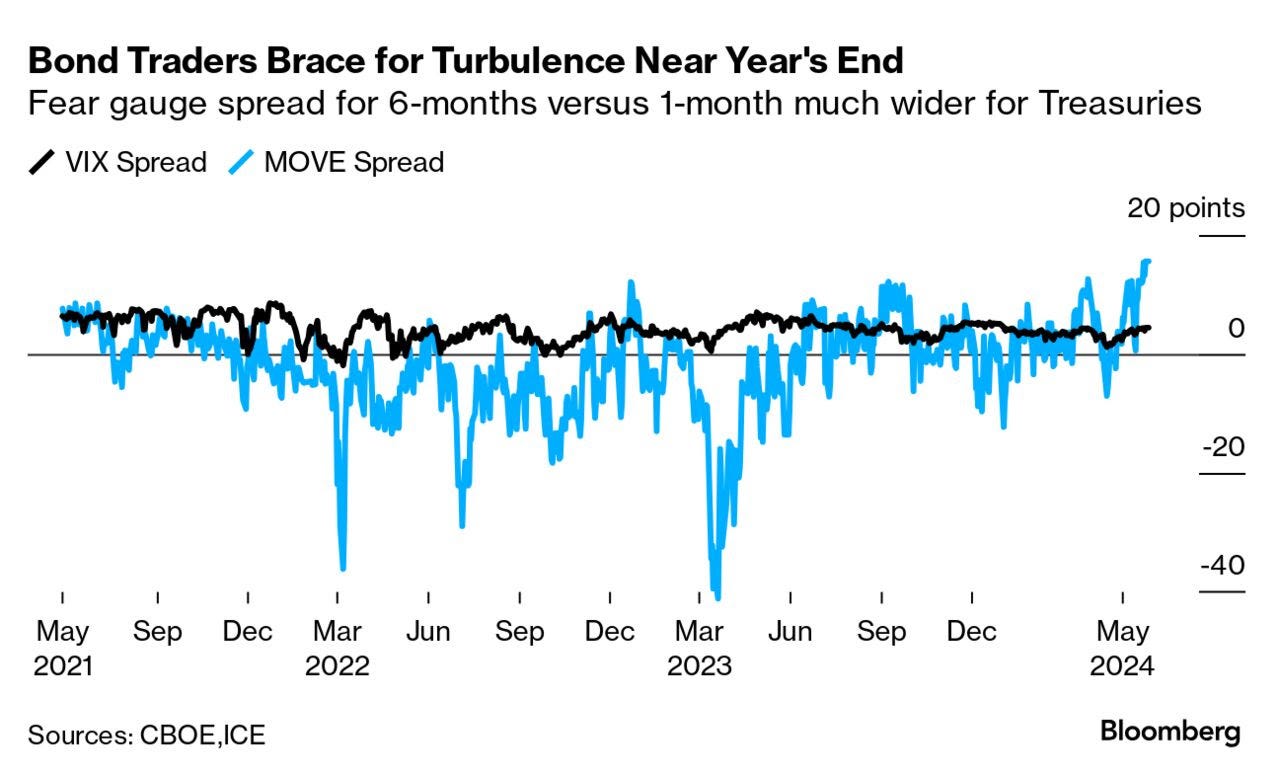

… Even in an environment where implied volatility readings are grinding lower, there’s some noticeable angst appearing around the November US elections. Bond traders look much more uncertain about the outlook for six months aheadthan they do for the coming month, which underscores the potential for turmoil with both presidential candidates leaning toward increased spending.

There’s also speculation that Donald Trump would follow through after his comments earlier this year that he wouldn’t reappoint Jerome Powell as Fed Chair if he wins the US election.

The so-called fear gauges for Treasuries are showing the widest gap since 2014 between expectations for yields swings six months from now and the expectations for a month ahead. That’s similar to the picture for a range of currencies — the yuan’s 6 month-1 month volatility gap is the widest since 2016. Equities look far less concerned, with the similar spread for the VIX only around the highest this year.

Bonds, and currencies for that matter, also have more than just the election on their plate when they look ahead toward the concluding weeks of 2024. Traders are seeing the November-December period as crucial for the Fed’s easing cycle, if it does indeed turn up this year.

OIS contracts show one reduction this year as the most likely outcome — with November or December the focus of bets for when the rate cut comes. As of the end of last week swaps priced in an 80% chance for a cut by the end of the November FOMC meeting, and signaled they were certain there would be at least one reduction for 2024 once the December meeting concludes. They even seem to envisage a scenario where the Fed carries out back-to-back easings in the final two meetings of the year.

The end of this year is seen as being at least as exciting on the economic front as it could be on the political side of things. Bond traders will be hoping they face a Happy New Year indeed after what they expect to be a relatively tumultuous run into Christmas.

Bloomberg: China’s Industry Threatens Entire Global Economy, France Warns (had me up until the very end … that part where FRANCE warned? i’m OUT. don’t care … sorry not sorry …)

Le Maire says determined to shelter own economic gains

French minister speaks with Bloomberg TV at Group of Seven

I’ve got a nice new weird indicator for you today (my favorite kind of indicator)…

… What we’ve got here is the net-percentage of countries who are seeing their inflation rates increasing vs decreasing. Negative readings mean more countries are seeing falling inflation rates (a global disinflation wave), positive readings mean more countries are seeing higher inflation.

Clearly the Great Disinflation of 2023 has troughed, and producer prices have already turned the corner back to reflation. So the underappreciated macro risk is the global disinflation wave is over and resurgence risk comes online, forcing central banks to keep interest rates higher for longer. Keep watch for bond market risk (and stocks/yield sensitives in the extreme), and upside opportunities in commodities — which are a key part of the turn in this indicator.

Key point: We have seen a climax in disinflation globally, and reflation/resurgence risk is very real (higher for longer risk for rates)…

Yahoo Finance: Wall Street is getting even more bullish on stocks (not sure who’s more irresponsible here — Global Wall or Yahoo … In Yahoo’s defense, the visual is clickable and customizable — kinda — and so, they get a hall pass)

… "The current environment is basically what the bulls were hoping for, and they are getting it," Bank of America US and Canada equity strategist Ohsung Kwon told Yahoo Finance. "It's basically a soft landing."

Kwon explained that while inflation data has come in hotter than expected to start the year, it still hasn't indicated that price increases are reaccelerating. Meanwhile, other data has signaled a slowing but strong economy, easing fears that red-hot growth could spark another inflation spike. In essence, this has fueled the soft landing narrative Wall Street bulls hoped for entering the year, per Kwon…

… and finally, in case you missed economic calendars mentioned HERE including a LINKthru TO this, MY personal fav, econ / event calendar …

… (1) PCED. The Cleveland Fed’s Inflation Nowcasting model shows headline and core PCED rose 2.68% and 2.74% y/y (0.27% and 0.23% m/m) last month (chart). That would be the lowest y/y reading for core PCED since March 2021.

We expect markets to welcome inflation's progress toward the Fed's 2.0% target, particularly after they were spooked by some of the hawkishness in the FOMC minutes released last week. That meeting occurred about two weeks before April's more-moderate-than-expected CPI and PPI were released.

Lagging rent disinflation continued to boost April's CPI. However, this category accounts for roughly 1/3 of the index, while shelter is only about 16% of the PCED. Also troublesome has been the health insurance premiums component of the CPI, which is extremely volatile compared to the comparable component of the PCED, which is much more subdued (chart).

{kind=link}