weekly observations (05/28/24): Rational exuberance (BNP on US consumer); flattening floundering (BMO) and ... Fed’s Favorite Underlying Inflation Gauge Is Seen Cooling (HOPE springs eternally...)

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP lets deal with a couple / few things items from Friday …

ZH: Durable Goods Orders Suffer Yet Another Downward Revision (Team Rate CUT celebrates … as bad = good — i hate this — and so stonks caught that early bid…)

… It was not just the headline data that was revised lower (prompting a 'first glance' beat for April) with Durable Ex Transports' 0.2% MoM rise revised to unchanged in March and Orders non-defense ex-aircraft also revised from +0.1% MoM to -0.1% MoM.

Furthermore, Capital Goods shipments non-defense, ex-aircraft was revised from unchanged to -0.3% MoM - a big drop for a key signal of business spending and GDP.

How many times can a data series be downwardly revised before conspiracies about manipulated data flip from theory to actual 'standard operating procedure'?

… Reasonable questions and points, to be sure … A(dur)able Goods revisions aside …

ZH: UMich Sentiment & Inflation Expectations Worsen In May (But Bounce From Flash Prints)

… While the university’s final May consumer sentiment index improved from the preliminary reading, it still registered a notable 8.1-point decrease from April and stands at a six-month low of 69.1…

… In addition to high prices and borrowing costs that are raising concerns about the cost of living, respondents in the survey grew anxious about the labor market. They expect the jobless rate to rise and income growth to slow.

That represents a challenge for President Joe Biden in his bid for re-election…

… see whatever part of that h’line / zinger you wish (worsen or BOUNCE … bad or good or is it good and bad or who cares cuz bad IS good and worse is AWESOME?)

To THAT point, by days and more importantly, WEEKS end …

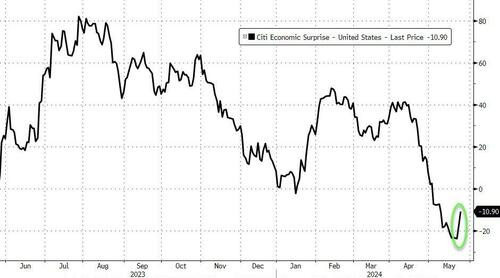

ZH: 'Best' Macro Week In 4 Months Is Bad News For Most; But Nasdaq And Ethereum Surged

After six straight weeks of 'weakness', US Macro Surprise data surged higher this week (Good News) - it's biggest positive weekly shift since January.

2yy: Concession? breaking badly back up into the years TREND?

5yy: same as above … NOT a good looking WEEKLY close and might need more concession early … time to see IF the flattening / cheapening will be enough to entice Team Rate CUT to put some $$ to work …

… AND again, get those bids in early and often … 2s @ 1130a and 5s @ 1pm …

… Ok I’ll move on TO some of THE VIEWS you might be able to use. THIS WEEKEND, there are only a couple / few things which stood out to ME as many / most seem to have taken advantage of the holiday long weekend …

While global manufacturing recovers, services inflation remains elevated across regions. We now expect the BoE to cut in August at the earliest and the ECB to wait until September for its second cut. The FOMC minutes also point to a more hawkish Fed. Next week's focus: US core PCE, euro area HICP inflation and China PMIs.

BMOWeekly, “Floundering Flattener?” (so, ‘bout that YEAR OF THE STEEPENING?? eventually it’ll arrive?)

… After entering our 2s/10s flattener position in the wake of last Wednesday’s CPI update at -37.5 bp, we booked profits on a portion of our trade after the curve reached our initial target of the 200-day MA on May 22nd at -43.0 bp. Our position has been trading further in the money, and we’ll continue targeting a deeper inversion with our sights now set on the March 12th CPI-day flat (and YTD flat) of -48.6 bp. While the technicals suggest the move is overdone, we suspect there is more room for the flattening to extend even if a period of consolidation precedes a deeper inversion. We'll note that we've moved our stop level up to the post-CPI high close of -40.7 bp to protect against losses in the event of a reversal.

As for our forward-entry long in the 10-year space, benchmark rates have been nearing levels we'd look to add duration exposure, although we've bumped up our buy level to the NFP-day open of 4.565%. 10s have more-thanreversed all the post-CPI gains and there is little in the way of immediate support in the event 4.50% is definitively breached. We suspect rates have backed up to levels that increasingly advocate for a long bias in light of the recent evidence of moderating inflation and consumption that's implied further economic cooling across the coming months and quarters.

Politics are again in the spotlight. In the UK, reduced political uncertainty and the BoE staying higher for longer should bode well for the GBP.

We see asymmetric risks going into South Africa’s elections this week and are positioned long USDZAR accordingly.

Potential uncertainty in India’s elections, coupled with the start of dividend season, suggests tactical risks to our bullish INR view.

BNP: US Consumer: Rational exuberance (hmmm … Team Rate Cut, what say you?)

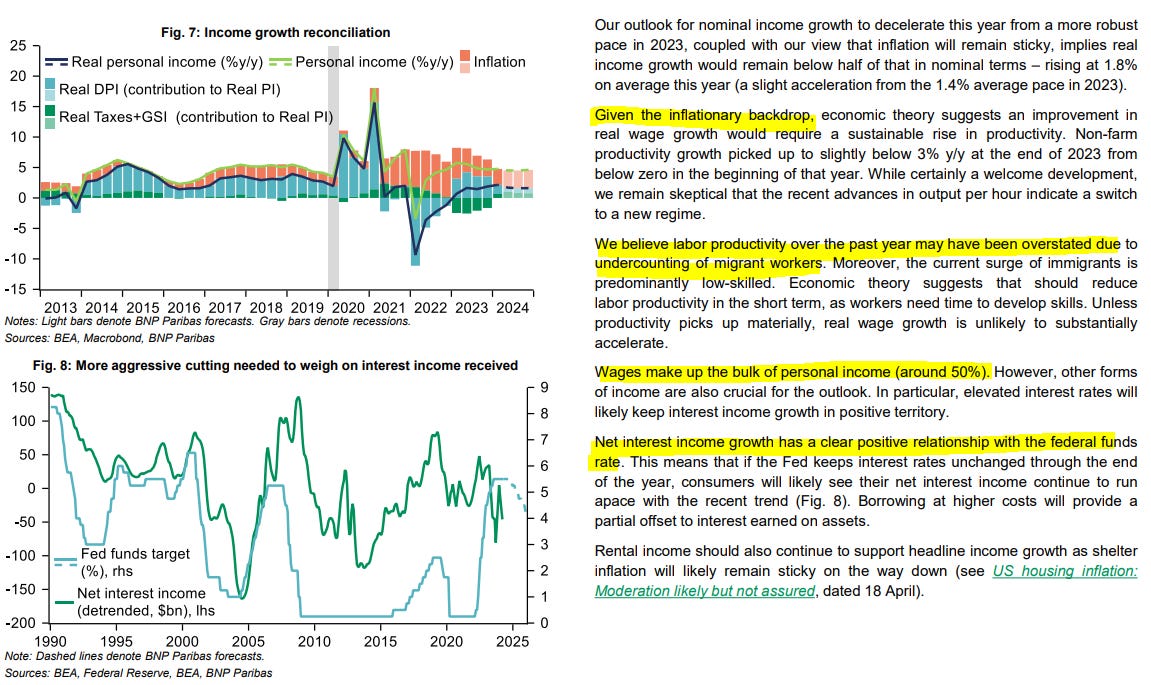

The US consumer outlook for 2024 remains optimistic as a healthy labor market and abating inflation are set to support income growth.

We project consumer spending growth to modestly decelerate going into H2 in line with ongoing rebalancing in the labor market. A more abrupt weakening in the labor market is a key downside risk.

Immigration is supporting income growth with a steady stream of extra paychecks. We estimate the impact of population growth this year compares to at least half the size of Cost-of Living Adjustment to Social Security payments in 2023.

A USD12trn increase in household net worth in 2023, — roughly half of the size of the economy — driven by real estate and equity gains as well as a new-found source of wealth in the cryptocurrency market – is set to prop up solid consumer spending this year.

Consumer balance sheets remain healthy with debt service ratios still historically low, despite increasing non-mortgage debt payments.

… Personal income: High rates still propping up interest income

MS: Sunday Start | What's Next in Global Macro: Sunny with a Chance of Rain

… Our economists envisage stable growth, moderate disinflation and policy easing in most DM economies ahead. Global growth remains steady at just over 3%Y in 2024 and 2025 in their base case. While growth slows, it does not crash, and the upside surprise to inflation in 1Q24 turns out to be a head fake and inflation decelerates globally. Both the ECB and the BoE cut policy rates in June on the back of soft inflation while the Fed follows with a rate cut in September, lagging because of noisy inflation data. We see 75bp of Fed cuts in 2024 followed by 100bp in 2025, but the path depends almost exclusively on the inflation outcome. For the ECB, we also see 75bp of cuts this year and 100bp of cuts next year, as the ECB almost reaches neutral. In contrast, the BoJ is hiking in our forecast, as inflation becomes entrenched..

… Given the many changes to market pricing of the Fed’s rate cuts year to date, driven by higher-than-expected inflation, the path ahead for US inflation was also debated heavily. Our economists argued that the acceleration in goods and financial services prices, which explains a substantial portion of the 1Q24 reflation, should decelerate from here and that leading indicators point to weaker shelter inflation ahead. Their analysis also showed that residual seasonality contributed to the unexpected strength in 1Q24 inflation, suggesting a payback in 2H24…

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

Net foreign purchases of US credit have increased dramatically since the Fed started raising yield levels, see chart below.

Bloomberg: Fed’s Favorite Underlying Inflation Gauge Is Seen Cooling

Core PCE measure could see smallest advance of 2024 so far

Euro-zone inflation may pick up, but ECB remains poised to cut

… The overall PCE price index probably climbed 0.3% for a third month, according to median projection in a Bloomberg survey. Increases this year stand in contrast to relatively flat readings in the final three months of 2023, underscoring uneven progress for the Fed in its inflation fight.

Fed Chair Jerome Powell and his colleagues have stressed the need for more evidence that inflation is on a sustained path to their 2% goal before cutting the benchmark interest rate, which has been at a two-decade high since July….

FACTSET: HIGHEST NUMBER OF S&P 500 COMPANIES CITING “AI” ON EARNINGS CALLS OVER PAST 10 YEARS

NORDEA Macro & Markets: Everything is about interest rates

Strong economic growth and inflation above the Federal Reserve’s 2% inflation goal is likely to put upward pressure on bond yields and downward pressure on the economy at a time when the rest of the financial reflects a strong economy.

Yahoo: No one gets in trouble owning too many tech stocks (irresponsible?)

ZH: Goldman Again Changes Forecast For First Fed Cut, Pushes Back To September From July (this actual note was, well, noted HERE for all who aren’t paid up PRO ZH subs … whatever that means)

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

https://www.dailywire.com/news/biden-pushes-world-to-not-censure-iran-over-its-illegal-nuclear-program-as-it-nears-critical-mass-report

Barchart: Fun Fact 🚨: Nvidia $NVDA is now worth more than $META, $TSLA, $NFLX, $AMD, $INTC, and $IBM combined