Good morning … Overnight there was some good news from China where economic data was strong, IP rose 7% yoy vs f’cast 5.0% and ReSale Tales increased 5.5% vs f’cast 5.2%…

Bloomberg: China’s Growth Bump May Dent Urgency for More Stimulus

Economy seen as stabilizing but consumer demand remains weak

Production, investment strength may delay stimulus: economists

… but then, if this good news impact chance for more stimmy, is it really good at all? Moving on and not too long after hitting send making mention of Timiraos / WSJ Fed watching story, a friend sent me this …

FT: Fed will have to keep rates high for longer than markets anticipate, say economists

…The Federal Reserve will be forced to hold interest rates at a high level for longer than markets and central bankers anticipate, according to academic economists polled by the Financial Times.

More than two-thirds of those surveyed in the FT-Chicago Booth poll think the Fed will make two or fewer cuts this year as it struggles to complete the “last mile” of its battle with inflation. The most popular response for the timing of the first cut was split between July and September.

That is a later start than expected in financial markets, where traders expect three cuts this year, with the first quarter-point reduction coming in June or July. The Fed’s current forecast, which is due to be updated on Wednesday, also sees three cuts in 2024…

…“The US economy is still running quite hot,” said Stephen Cecchetti, a professor at Brandeis University. “There’s still some risk of a slowdown in the second half of the year, but not as much as I would have expected three months ago.”

Better growth could also weigh on the Fed’s willingness to cut rates, some respondents said. “I see demand in particular as stronger in the US than in European countries,” said Hilde Bjørnland, professor of economics at BI Norwegian Business School, who thinks markets will have to wait until November for the first rate cut.

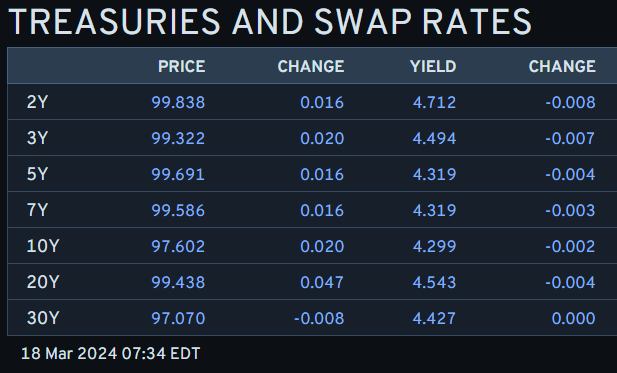

… AND so it goes … Global Wall (more on this below) and MSM slowly and surely coming around. Question remains what, if anything, will BoJ do and also IF the Fed will remove a cut from the ‘24 dots … an interesting and funTERtaining week ahead, for sure and for now … here is a snapshot OF USTs as of 734a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are twisting modestly steeper in quiet trade ahead of a big week for global central banks. JGBs bull-flattened (30y -3.1bps) in a pre-BoJ short-covering exercise, while China data was mixed (stronger IP, Retail Sales, higher unemployment). Major FX crosses are close to UNCh’d, while S&P fut’s are +25pts following rises seen in APAC indices (NKY +2.7%, KOSPI +0.7%, SHCOMP +1%). ~85% volumes seen in TY futures overnight, belly spreads tightening alongside a 1.5bp steepening through 5s30s. No tier-1 US data today.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities firmer amid constructive risk tone, JPY softer and Crude bid as geopols remains in focus … Bonds are incrementally weaker, though with price action contained …

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … today’s edition might be deemed the, ‘When the facts change, I change, what do YOU do sir’ edition and in addition TO RATE GUESS updates noted HERE yesterday … I present …

Stronger IP data (supported by exports) suggests a sequential recovery in Q1 growth as China's GDP statistics are production-based. We think the disappointing retail sales reflect more secular headwinds. A continued negative feedback loop between weak sales and developer defaults bodes ill for property investment.

DB: China Macro - Jan-Feb activity: better than expected

China's economic activity indicators in January and February 2024 came out stronger than expected. Retail sales improved sequentially thanks to higher consumer spending during the LNY holidays, consistent with high frequency data that we observed earlier. Unexpectedly, industrial production also improved owing to higher output growth in a number of upstream industries, but the drop in sales-to-production ratio raises the question whether the improvement can be sustained, absent a pick-up in downstream demand. Investment was also stronger than expected, which may reflect an increase in government-led housing projects. Property sector remains a weak spot, with sales growth staying deeply contractionary and prices dropping further on both new and secondary markets.

All in all, our model estimates a 5.3% YoY growth in Jan-Feb 2024, which is much higher than our current Q1 2024 growth forecast of 4.4% (1.3% QoQ) and market expectations of 4.3%. Notwithstanding a potential upward surprise in Q1 growth, our 2024 GDP growth forecast remains unchanged at 4.7% for now, considering that activity indicators tend to have higher volatility in the holiday season and therefore more data points will be needed to assess the near-term growth momentum, and also taking into account the relatively modest credit growth in the first 2 months.

Goldilocks: March FOMC Preview: Waiting for June (aNOTHER updated, higher yields ‘ish forecast … in addition to JPMs view noted HERE yesterday …)

■ Inflation has been firmer in recent months, but we think it is still on track to fall enough by the June FOMC meeting for a first cut. This has become less obvious though, and our inflation path for the rest of the year is now in a range where small surprises could have large consequences.

■ We now expect 3 cuts in 2024 (vs. 4 previously), mainly because of the slightly higher inflation path. We continue to expect 4 cuts in 2025 and now expect 1 final cut in 2026 to an unchanged terminal rate forecast of 3.25-3.5%. Our probability-weighted Fed forecast is similar to both our baseline scenario and market pricing in 2024 but somewhat lower than both at a 2025 horizon.

■ We suspect that the Fed leadership is also still targeting a first cut in June, and this combined with a default pace of one cut per quarter implies that the most natural outcome for the median dot is to remain unchanged at 3 cuts or 4.625% for 2024. We expect the median dots to remain unchanged at 3.625% for 2025 and 2.875% for 2026 as well. We expect the longer run dots to gradually drift higher over time, with a small tick up a bit more likely than not this week. The only significant change to the economic forecasts should be an increase in 2024 GDP growth.

■ The main risk is that FOMC participants might instead be more concerned about the recent inflation data and less convinced that inflation will resume its earlier soft trend. In that case, they might bump up their 2024 core PCE inflation forecast to 2.5% and show a 2-cut median.

■ The FOMC will also begin a formal discussion of slowing the pace of balance sheet runoff this week, but details will likely be left to the minutes. We expect the Committee to slow the pace of Treasury runoff from $60bn to $30bn per month after its May meeting and to then continue runoff through 2025Q1, at which point the size of the balance sheet should be about $6.7tn or 23% of GDP.

Goldilocks: Upgrading Our GDP and Payrolls Forecasts to Reflect Elevated Immigration (so to summarize, higher GDP, NFP and less rate cuts — MAKES COMMON SENSE — does then WHAT to markets …? awaiting any / all answers, thank you)

■ One of the biggest puzzles of the last year has been that the labor market has continued to rebalance and the unemployment rate has increased somewhat despite surprisingly strong payroll growth and GDP growth. The explanation appears to partly be that elevated immigration has boosted labor force growth and, by extension, potential GDP growth.

■ Recent studies suggest that Census data used for the household survey of the employment report understated immigration in 2023. We estimate that immigration was 1½mn above the trend of roughly 1mn per year in 2023, which implies an 80k boost to the monthly breakeven rate of job growth to 155k. We expect immigration to be about 1mn higher than usual this year, implying breakeven job growth of around 125k and a 0.3pp boost to potential GDP growth in 2024 from faster labor force growth.

■ We have updated our payrolls and GDP forecasts to incorporate the ongoing boost from above-trend immigration. We now expect payroll growth to average 175k/month this year and slow to 150k/month by year-end, though we expect this to only lower the unemployment rate a touch to 3.8% by year-end. We have also raised our 2024 real GDP growth forecast by 0.3pp to +2.4% on a Q4/Q4 basis (or +2.7% on a full-year basis), mostly by upgrading consumption growth.

Goldilocks China: January-February industrial production and fixed asset investment beat expectations, while property weakness remained

Bottom line: January-February activity data came in above market expectations. Industrial production growth edged up in January-February, against market expectation of a slowdown, as the boost from computer and ferrous smelting industries more than offset the drag from automobile and electric machinery industries. Fixed asset investment growth also accelerated in January-February, thanks to faster growth in manufacturing and "other" (mostly services and agriculture-related sectors) investment. Year-on-year growth in retail sales and services industry output both slowed in January-February on a high base last year (when pent-up demand was released right after China reopening). Most property-related activity worsened broadly and meaningfully in year-on-year terms in January-February, reflecting either unfavorable base effects or sequential weakness. Taking stock of January-February activity data and our high-frequency trackers for early March, we believe China's sequential growth momentum has been fairly solid in Q1 so far, especially for exports and government-led investment, although property weakness appears prolonged. We maintain our above-consensus GDP growth forecast for Q1 and full-year 2024, at 4.5% yoy and 4.8% yoy, respectively (vs. consensus: 4.3%/4.6% yoy), and believe more policy easing is still necessary to secure the ambitious "around 5%" growth target this year.

Will this week's Fed and BOJ meetings bring central bank policy back into focus for stock valuations, which have recently diverged from interest rates? We observe a recent broadening in large cap performance with Industrials, Energy and Materials exhibiting the strongest breadth.

Rates Back in Focus This Week for Equities?...While almost all of the equity market rally late last year was attributable to lower rates, stocks are now trying to move past their dependence on central bank policy. This week's Fed and BOJ meetings will be important tests to see if that trend holds. We view 4.35% on the 10-year US Treasury yield as an important technical level to watch for signs that rate sensitivity may increase for equities. While large caps have exhibited declining rate sensitivity over the past few months (large cap 2-month correlation versus rates is a modest -0.1), the correlation of small cap performance versus interest rates remains meaningfully negative (-0.4), indicating small caps are likely to show more rate sensitivity than large caps on a move higher in yields. The recent broadening within large cap leadership may be how the market is dealing with the inconsistency of higher rates and still elevated multiples for the large cap equity indices…

… Fast forward to this year, and the story has been much different. Bond yields have risen considerably since the beginning of the year as market participants have moved away from the long end and the Fed walked back several of the cuts that had been priced in for this year. Amid these dynamics, there still appears to be a divergence between the 10-year yield and what the market is pricing in terms of the near-term policy path. The flip side is that growth data has been weaker in aggregate which argues for lower rates—the main reason for our rate strategists’ more constructive view between now and year-end (Exhibit 3).

Exhibit 2: Divergence Exists Between 10-Year Yield and Market Pricing of Near Term Policy Path

Exhibit 3: But Softer Economic Growth Data Should Support 10-Year USTs

There is also the question of supply which continues to grow with the expanding budget deficit. While market participants are well aware of this dynamic, there's still a good deal of uncertainty around how well the bond market will absorb this issuance going forward, particularly if spending intentions continue to increase. From an equity standpoint, the rise in rates this year has not had the typical effect on valuations—i.e., P/E multiples have remained elevated in the face of rising rates. This informs us that, for now, equity investors appear to have moved past the Fed, inflation and rates and are now squarely focused on the better growth consensus expects to arrive this year.

Exhibit 4: Equity Valuations Have Diverged from Rate Cut Expectations

This week marks a new phase in the battle between markets and central banks about the timing of rate cuts. We are not at the end—no one is expecting the assorted central bank meetings to produce rate cuts this week. We are not at the beginning of the end—explicit forward guidance of rate cuts also seems unlikely. But we are at the end of the beginning. Ongoing disinflation forces continue to make a forceful case for rate cuts in the second quarter.

Rate cuts this year should not be considered to be policy stimulus. As inflation continues to slow, rate cuts are needed to prevent rising real rates, which would choke growth more aggressively. This year’s policies are anti-depressants, not stimulants.

The Bank of Japan is the exception to the rate cut story, and there is a chance that the long experiment with negative interest rates will end this week. Negative interest rates may start as a signal of cheap money, but they rapidly morph into a tax on the banking system (and larger savers)—a questionable stimulus.

The ECB avoids taking a decision this week. Eurozone consumer price inflation is due today but this is a final figure which rarely differs from the flash data.

Container transportation prices are slowly coming down from their peaks, but IMF data shows that traffic volumes through the Suez Canal continue to deteriorate, see chart below.

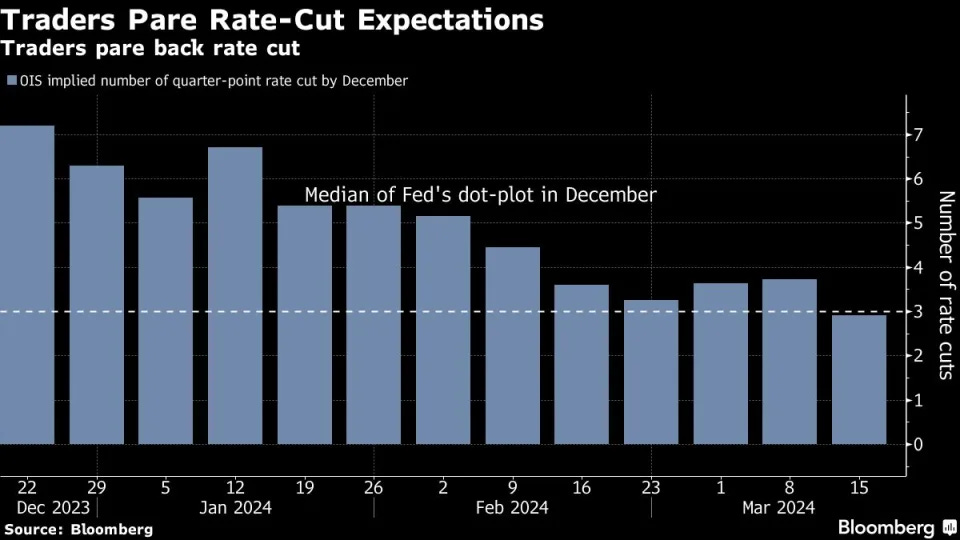

Bloomberg: Bond Traders Surrender to Higher-for-Longer Reality From the Fed

Investors set up for fewer rate cuts ahead of policy meeting

… As recently as December, bond traders were all but certain the Fed would start to ease at this week’s meeting. But after a raft of surprisingly strong data on growth and inflation, they see zero chance of action this week, slim odds of a move in May and only a 60% possibility of a cut in June. For the year, traders have penciled in expectations for a total reduction of 71 basis points, meaning a three full-quarter-point cut is no longer seen as guaranteed.

Hedgopia: Major US Equity Indices On Trendline Support From Last Oct, Or In Slight Breach, Even As Bears Hit Multi-Year Low

everybody talking about immigration as an excuse to revise their targets higher (10Y or FFR or NFP or GDP etc...)

September, might be more realistic for Rate Cuts to begin...

I'm growing more and more skeptical of a June Cut...

I don't think the Data will corroborate a Cut in June....