RTRS: China cuts key lending rates to support growth

China cut benchmark lending rates as anticipated at the monthly fixing on Monday, following reductions to other policy rates last month as part of a package of stimulus measures to revive the economy.

The one-year loan prime rate (LPR) was lowered by 25 basis points to 3.10% from 3.35%, while the five-year LPR was cut by the same margin to 3.6% from 3.85% previously.

The lending rates were last cut in July…

… and as this was widely anticipated, markets really seem to NOT care …

Thanks for reading The BondBeat! Subscribe for free to receive new posts and support my work.

Bloomberg: Chinese Stocks Edge Higher in Choppy Trade After Bank Rate Cuts

LPR cuts beat expectations, follow central bank stimulus

Companies rushed to tap loan scheme to fund buybacks: reports

… from China back TO the US and while some might argue the Fed’s GOT to cut rates by some order of magnitude in November or risk a pause they’ll regret (see Opening Bell just below), a quick look at the belly …

5yy Daily: 200dMA up above (4.117%) as support … problem is TLINE …

… as TLINE gives way, momentum on move again and not YET overSOLD suggesting time to buy may not be just now …

… AND from China to 5s today, a quick note that over the weekend I mentioned some levels some of the best in the biz are looking towards as a DipOrTunity (10s vs 200dMA) and wished one and all a happy Crash(and Glue Factory)-A-Versary … from there we’ll go right TO a snapshot OF USTs as of 653a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are drifting lower and marginally flatter with Bunds leading underperformance among semi-core peers ahead of bond sales from the EU and Belgium (EU €5b 6- and 30-year debt; Belgium offering €2.5b 5-, 10- and 30-year notes). Some selling has been evident in the US point, according to the desk, a ~1bp cheapening seen vs the wings, with weakness more acute in futures after TYs slipped through the 112-00 level. Since then, some light dip buying has been seen out the curve from real money in the 30yr point, but overall price action remains weak. Volumes running ~90% the 30d average. Crude Oil is also higher by 2%, XAU +0.3%, S&P futures -9pts here at 6:45am.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US futures mixed ahead of Fed speakers; dollar firmer and bonds pressured … Bonds are entirely in the red, Bunds were initially lifted by soft German producer prices, but ultimately succumbed to selling pressure … USTs are modestly lower but holding at a 112-00 trough which equals last Thursday’s base with support at 111-31 and 111-29+ below that.

Opening Bell Daily: Ending the everything rally: The US economy could be too strong for its own good … If the Fed does anything other than cut interest rates in November, the everything rally could unwind.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

First up, one I missed but one that reads much like others — ie buy on dips … with a twist or it’s very own nuance …

BAML: Global Rates Weekly 18 October 2024 Poll position

…US: US data & election risk drive higher rates; fade elevated likelihood of US expansion. Election sweep is bear steepening risk; we favor buying real rate dip on sweep.

US macro: so good it hurts US rates modestly increased & curve bear steepened in the past week. Driving the move was stronger than expected US data and a shift in market-implied US election probabilities (Exhibit 4, Exhibit 5). Investor conviction to take duration risk remains light ahead of US election due to sweep bear steepening risks…

… Our views: Duration: we continue to like buying the dip. We have argued for trading US duration tactically, believing near-term 10Y range will be 3.5-4.25%. We think it makes sense to tactically add duration exposure towards the upper end of the range; our preferred duration add point remains the belly (5Y).

Our model for assessing market implied expansion vs slow down (derived from breakeven inflation moves) now sees expansion > slowdown (Exhibit 6, see: Range of outcomes). As the market implied likelihood of a US slowdown declines, we see scope to add duration exposure. Adding exposure when 5Y or 10Y OIS is 3.75% or so implies elevated chance the Fed stops cutting around 4% & seems somewhat asymmetric to us.

Curve: we maintain our long standing 5s30s curve steepening bias. Election considerations now dominate this trade and are likely to build into the risk event…

…Technicals: US 10Y dip buyers emerge in 4.10-4.20% area Technicals suggest US10Y dip buyers may emerge in the 4.10-4.20% area. We favor this while yield remains < 4.40% which is the guiding line of the 2024 cyclical bull.

US 10Y Yield: Declining range in 4Q24-1Q25 In a soft-landing scenario, we thought US 10Y yield would decline below the low of wave (A) of 3.78% and would reach 3.50% with risk skewed to the downside. It reached 3.60% in September. Downside risk remains since wave (C) tends to extend and wave II tends to be deep retracement of I, such as 3.50-3.22% and the rising 200wk SMA now at 3.06%. The impulsive move higher in yield from 3.60% is testing yield resistance in the 4.10-4.20% area. We think this is a place to consider adding to longs for a turn down to 3.50-3.22%. However a break higher leads to the next trend line at 4.40% which is the cyclical bull market line in the sand. One could add to longs here, too, for turn down to 3.75-3.50%. However above 4.40% and the narrative may be changing to a sideways or no landing scenarios. Please see the Rates Technical Advantage: Soft landing promotion 14 October 2024 report for more detail.

… now, same firm earlier last week (another one I missed til now) suggesting there maybe plenty of ROOM TO BUY if / when yields (continue) to rip …

BAML: Global Fund Manager Survey 15 October 2024 Bull Charge

Bottom Line: the biggest jump in investor optimism since Jun'20 on Fed cuts, China stimulus, soft landing (Chart 2); allocation to stocks surges and to bonds sinks, as FMS cash level falls to 3.9% from 4.2% (triggering ACWI “sell signal”); froth on the rise but BofA Bull & Bear Indicator up to 7.1, not yet the big “sell signal” level of 8.0…

… a few words from fan fav and German bank stratEgerist …

It doesn't feel like its going to be the most exciting week ahead of us. Although with earnings season now in full throttle and with a seemingly extremely tight US election just two weeks tomorrow there is undoubtedly plenty to think about and react to.

Having said the election is tight, over the last two weeks the probability markets have been shifting back towards Trump. PredictIt has moved from a 45% probability of a Trump win on September 20th to 56% this morning. At the start of October a Republicans sweep was a 28% probability on Polymarket.com but that's now shifted to a 42% chance. A Democrats sweep has fallen from 21% to 14%. Outside of the tax and spending implications, Mr Trump last week said that "the most beautiful word in the dictionary is tariff". So that should have reminded markets that he is serious on this matter if he gets elected. In terms of fiscal, you'll remember from last week that our US economists believe that the deficit will be between around 7 to 9% from 2026-2028 whatever political configuration we have in the White House …

… and same shop askin’ / offering answers (w/more questions and some context) …

DB: Mapping Markets: Can this rally go much further? 4 hurdles that lie ahead

The cross-asset rally is becoming increasingly relentless. The S&P 500 has posted 6 consecutive weekly gains for only the second time since the pandemic, and has seen its strongest YTD performance since 1997. In credit, last Thursday even saw US IG spreads reach their tightest since 2005. Sovereign bond spreads have tightened too, with the spread of Italian 10yr yields over bunds at the tightest since November 2021.

But can this rally go much further? Traditional valuation metrics are looking increasingly stretched by historical standards. Geopolitical risks remain elevated, and with a soft economic landing increasingly priced in, it feels more difficult to get further upside growth surprises from here. And that’s before we’ve considered issues like debt, which are rapidly rising up the agenda again.

So given these warning signs on the dashboard, we run through some of these hurdles to the current rally and consider why it's worth remaining cautious.

… So what hurdles does the current rally now face?

1. Valuations – The impressive rally means that traditional valuation metrics now look stretched by historical standards.

2. Growth – Markets have been lifted over 2023-24 by upside growth surprises. But with a soft landing increasingly priced in, further upside surprises will be more difficult to achieve…

3. Geopolitics – There are still heightened tensions in the Middle East that have led to a market pullback in previous episodes.

4. Debt – With global public debt levels still rising, this is likely to be something that markets increasingly focus on…

…conclusion …So even as the global economy is in a fundamentally strong position right now, it's worth remaining cautious given the strength of the recent market rally and the upcoming headwinds on the horizon.

… a couple / few words on stocks …

MS: US Equity Strategy: Weekly Warm-up: Stick with Cyclicals as Financials Stand Out From the Pack

We continue to have conviction in our cyclical shift & Financials upgrade. Earnings season has been strong for Financials & the stocks have responded well to EPS beats (best performing sector over the last 2 weeks). As focus turns to the election, we dissect market implications of various scenarios…

… Markets Appear to be Rotating More Toward the Trump Win Scenario...Over the past several weeks, equity market leadership has looked more like the 2016 election playbook. Meanwhile, bonds have sold off, and several precious metals and crypto currencies have continued their upward momentum. Given these dynamics, markets may now be offsides to some extent should Harris win. Although, other factors (fundamental and policy related) have also been driving price action and should be considered when dissecting returns this month. We discuss related developments in the note and how to position.

…While some argue a Trump win would be a headwind for growth and, therefore equity markets, due to tariff risks and slowing immigration, we think there's an additional element from the 2016 experience that is worth considering—animal spirits. Trump's probusiness approach led to the largest 3-month positive impact on small business confidence in history (40+ years) as Exhibit 11 shows. This also translated into a spike in individual investor sentiment ( Exhibit 12 ). We think it's fair to say that markets may be trying to front run a repeat of this outcome as Trump's win in 2016 came as a surprise to pundits and markets alike. As a result, a Harris win could lead to some reversion in terms of overall equity market performance and leadership. Bonds could potentially rally with defensive/quality growth outperforming like earlier this year. Secondarily, even with a Trump win, certain areas of the market may be vulnerable to a sell the news phenomena if the upside is already priced amid heavy positioning. On this front, we would also point out that the economic set-up today is very different than 2016 when the economy had much more slack and could absorb additional pro-cyclical policies like tax cuts/fiscal stimulus. Bottom line, in the absence of a major swing in election probabilities and/or global liquidity between now and the election, equity markets are likely to trade with a bullish tilt both at the index level and from a sector/style/factor standpoint.

Lastly, it appears to us that the S&P 500 has performed even better than what a Trump win would suggest in isolation. As noted, some of this may be due to better than seasonal earnings revision breadth. However, with valuations already very high (top 5-10th percentile on several measures), we think it may be due more to the improving liquidity picture since June. In addition to more dovish monetary policy from the Fed and other central banks, we have also seen a dramatic rise in global Money Supply (M2) in US Dollars. This is one of our favorite observable measures of global liquidity and since June, we have seen an increase of almost $4T in this metric, which is 18% growth on an annualized basis. This surge in global money supply growth has been driven by an outright expansion in M1 in China and Japan, as well as a weaker dollar through the end of September. The recent strength in the US dollar may slow the pace of this money supply growth in the near term and is an important variable to monitor going forward.

… on the cutting of rates … here, there and everywhere …

German September producer prices are expected to stay in deflation (this is not a surprise, they have been in deflation for over a year). While other factors will add noise to consumer price data, producer prices are a better reflection of corporate pricing power. The deflation signals should secure expectations for further rate cuts from the ECB.

China’s central bank cut the reference rates for personal and business mortgages. The move was widely signaled. The optimistic reading is that this reiterates the authorities’ intent to offer significant support to the economy. The pessimistic spin is that the cost of credit is not the problem with China’s domestic demand, and more needs to happen to reduce fear about the future.

There are several Federal Reserve speakers on the agenda today. Fed Chair Powell’s “data dependency” policy has added uncertainty about policy, especially as the data quality is not very dependable. The symbolic dissent at the September policy meeting also raises questions about the policy path. The importance of individual comments by Fed members is therefore increased.

The US election season enters its final and more frantic stages. Economics are not driving politics (economic perception and economic reality are increasingly opposed). Investors are giving limited attention to policy proposals at the moment.

… ‘bout them Animal Spirits …

Wells Fargo: Short-Term Outlook Shaky for Animal Spirits

Summary

The Animal Spirits Index (ASI) fell in September to 0.65 from 0.78 in August but remains elevated from a historical perspective.

Every component was subtractive in September, with the exception of the S&P 500 Index.

While the ASI may fall further this year, there is little cause to believe it will dip into the red, as economic growth continues to run at a sturdy pace. That said, the upcoming presidential election and its aftermath may create volatility in the near future.

… Every component contributed negatively to the index in September, with the exception of the S&P 500 Index. The equity market's optimism has not been shared by the bond market. The yield spread between the 10-year and 3-month Treasuries remained negative in September, though it narrowed to -100 bps from -118 bps in August. The stock market provided a bit more relief to the ASI over the month as the S&P 500 Index rose roughly 114 bps to reach another record high. Year-to-date, the index is up 19% and has contributed positively to the ASI for eight of the nine months of 2024. That said, stock market volatility also rose over the month, and the VIX Index reached its highest level since October of last year…

… on a very quiet economic calendar this week with stocks at new ATHs and bond yields rising supported by data and so, not YET getting in the way of stonks …

The economic week ahead will provide updates on the overall economy, manufacturing, and housing. Last week's jobless claims (Thu) will also be important for gauging how significant bad weather and worker strikes impacted the labor market. We expect more upside surprises during the current earnings season for Q3. The Nasdaq is likely to rise to a new record high before the end of the month and is currently on course to hit 20,000 before the end of May 2025 (chart).

The S&P 500 closed last week at a new record high while the 10-year US Treasury was around 4.10%. Investors may be wondering how high bond yields can go before they weigh on stock prices. As long as bond yields are being driven higher by strong economic growth–as evidenced by the rising Citigroup Economic Surprise Index–stocks should benefit (chart). Rebounding inflation would be the scenario that raises bond yields and hurts stocks.

Let's assess the outlook for this week's major economic indicators …

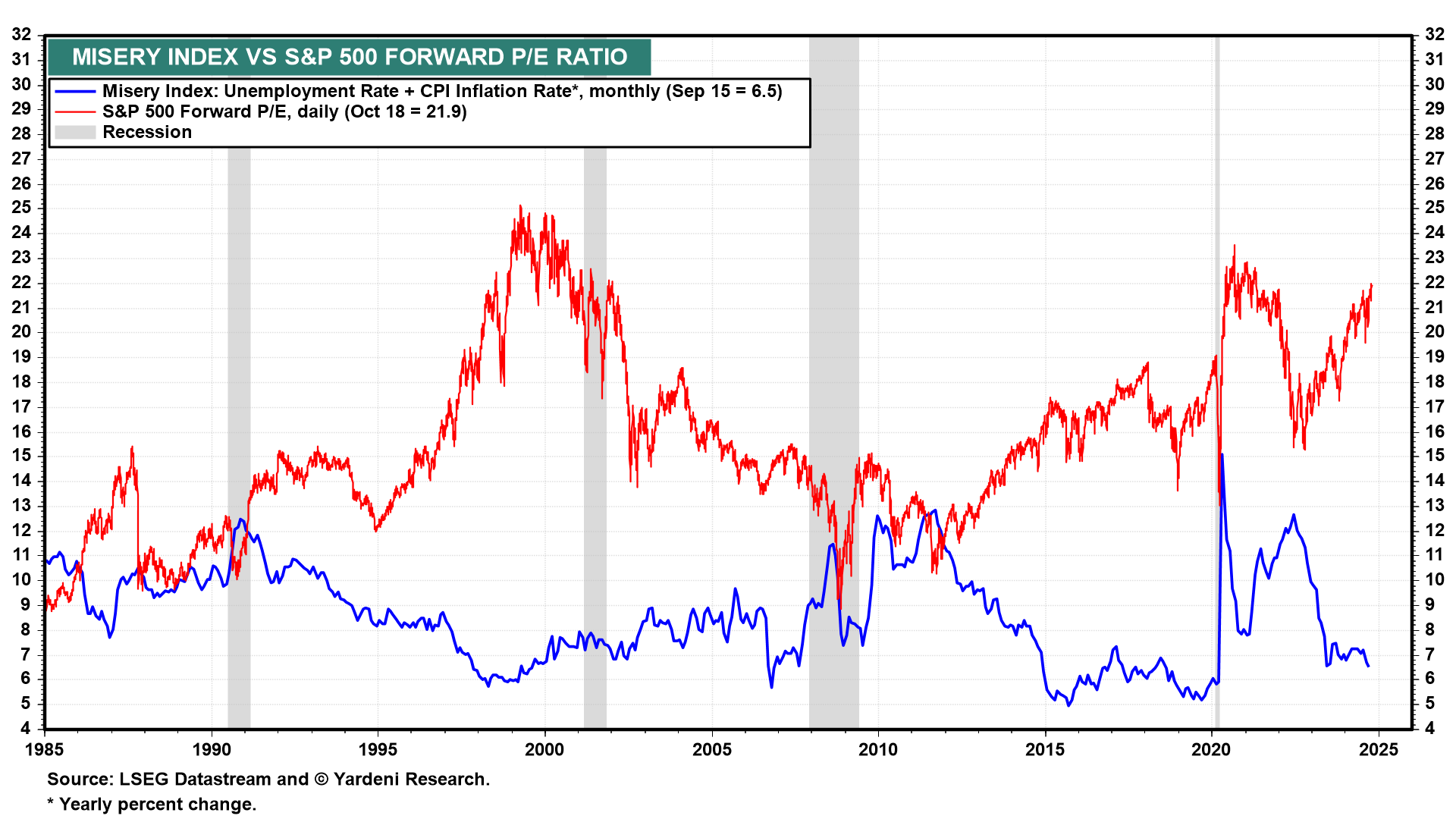

… the same shop offering a visual of Misery Index and the fwd PE ratio …

As the S&P 500 continues to rise to new record highs, we are frequently asked how we define a meltup and are we already in one? One simple answer is that the S&P 500 is melting up whenever the S&P 500 forward P/E is rising much faster than S&P 500 forward earnings per share, suggesting mounting “irrational exuberance.” In his December 5, 1996 speech, Former Fed Chair Alan Greenspan famously asked, “But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions .…” In a stock market bubble, investors must have very high expectations for earnings growth and very low risk assessments to justify the market’s lofty valuation levels. These assumptions might be irrational thus setting up the meltup for a meltdown, or at least a severe correction.

Are we there yet? Hard to say, but we may be getting closer to that scenario …

… Since the start of the latest bull market on October 12, 2022, the forward P/E of the S&P 500 has increased 43.0% from 15.3 to 21.9 on Friday (chart). Over that same period, forward earnings per share increased 13.9%. The forward P/E is inversely correlated with the Misery Index (i.e., the unemployment rate plus the inflation rate), which is historically low currently. So, while the low Misery Index hasn’t been boosting consumer confidence, it has been justifiably boosting investor confidence.

Nevertheless, the forward P/E is fast approaching its previous two cyclical peaks (22.6 and 25.5 during January 2021 and July 1999).

… And from Global Wall Street inbox TO the WWW …

… TRowe NOT Team Rate CUTS …

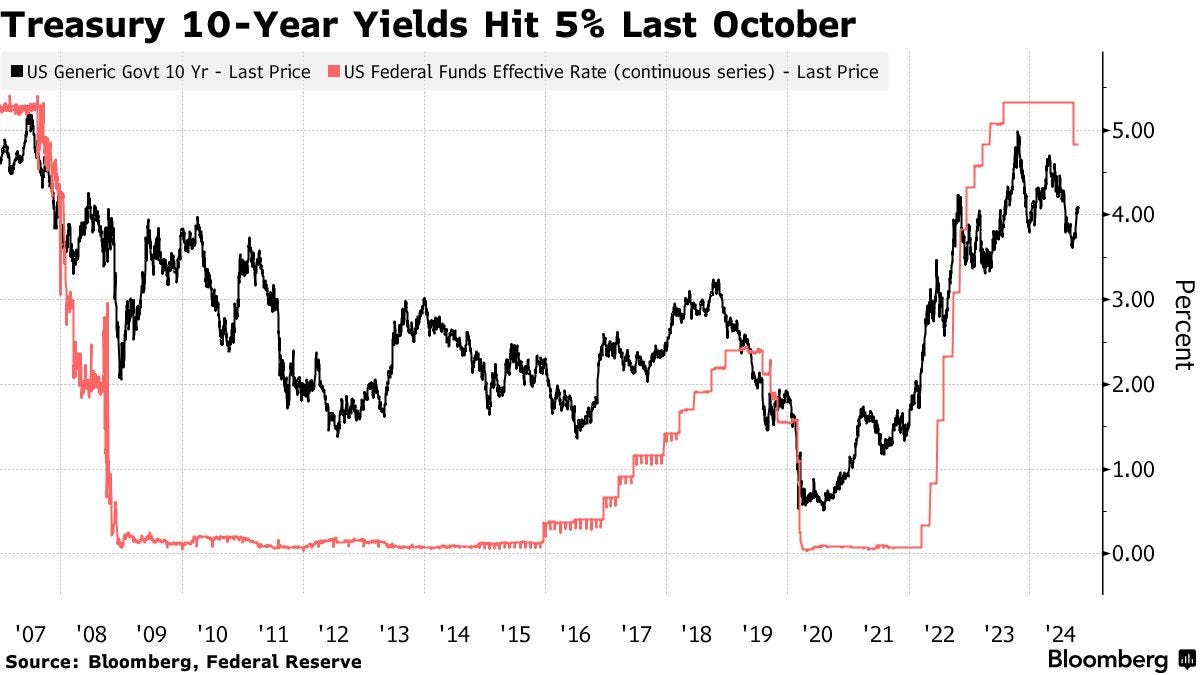

Bloomberg: Treasury 10-Year Yields May Hit 5% in Six Months, T. Rowe Says

Shifting supply, demand will push up long-term yields: firm

Debt costs are rising, fueling concerns among bond investors

… Yields on 10-year Treasuries most recently traded at 5% last October, hitting their highest level since 2007 as fears of a prolonged period of high interest rates gripped markets. Turbulent repricing could be on the cards if Husain’s prediction proves accurate, with strategists currently expecting yields to fall to an average 3.67% in the second quarter.

Ten-year Treasury yields held at 4.08% on Monday.

Husain, a near three-decade market veteran, said ongoing issuance by the Treasury to fund the government deficit is “flooding the market” with new supply. At the same time, the Federal Reserve’s policy of quantitative tightening — an attempt to reduce its balance sheet following years of bond-buying — has removed a key source of demand for government debt.

The yield curve is likely to steepen further because any rises in the yields of short-maturity Treasury bills will be limited by rate cuts, said Husain, who is also T. Rowe Price’s head of fixed income…

… and on the stonk mkt which, in case you didn’t know, almost always goes up …

Sam Ro from TKer: The stat explaining why the stock market gets so much negative news coverage

…The stock market usually goes up. Historically, prices have been in bull market over 80% of the time. Investors who can commit the time usually do well. Just this past week, the market rallied to new highs.

If this is the case, then why does so much news about the stock market seem to be negative?

But there’s another much simpler explanation: The stock market experiences a lot of down-days.

“On any given day in the stock market, your odds of a positive return are just 53%, little better than a coin flip,” Creative Planning’s Charlie Bilello.

If you’re in financial news, and you have to report on the markets every day, then about 47% of your days come with the stock market trading lower that day.

On any given day, the odds the stock market trades lower is relatively high. (Source: @CharlieBilello)

Unfortunately, most people won’t accept that prices are down that day “just because.”

That brings us to markets reporters and editors — one of which I have been in a variety of capacities over the last 18 years — who are in a very tough spot. All of their reporting and researching may have them conclude that the balance of news and risks is positive. But if prices are down, many are still under pressure to spin up or back into some narrative.

This leads to weird headlines like “Stocks fall as traders take profits” or “Stocks close lower as optimism fades” or “Stocks pull back on heightened uncertainty.”

Meanwhile, there’s never a shortage of bearish pundits happy to offer quotes with their thoughts on why prices are down on a given day. And their bearish assessments seem much more compelling when the live charts we’re all looking at are red. Sometimes, they’re right. Most of the time, they’re just amplifying the noise…

…All that said, TKer is here to help. TKer is written for long-term investors in the stock market. Two of our more popular reads are the weekly “Review of the macro crosscurrents” and “Putting it all together”* sections. The former provides roundups of new data with context and the latter provides an up-to-date big picture summary for that data.

While the short-term noise is often unsettling, TKer continues to find that the long-term outlook for the stock market and the economy remain favorable…

AND … THAT is all for now. Off to the day job…

Thanks for reading The BondBeat! Subscribe for free to receive new posts and support my work.