Good morning … fitting that we’re ‘celebrating’ this day — the day AFTER what was, at the time, largest single day percentage drop (22.6%) in the history OF the Dow — on heels of a (canary in the coal mine?) notification from the FDIC …

Street.com: Top Headlines From Black Monday and the Stock Market Crash of 1987 Many thought it was the crash was the start of the next Great Depression and the headlines of the day reflect it.

… as this all marinates, thankfully NOT during a trading day (am quite certain there will be plenty of remembrances offered tomorrow), I would ALSO like to mention today is the day after another important (personal) milestone and day in financial markets history … the day some of my thoughts and rantings made it into to an official Fed speakers speech … for more on that, scroll down a bit and for now, here are a couple / few more things from the Global Wall inbox …

First up on changing distributions of risk …

BNP: Sunday Tea with BNPP: Data dependency amid US exceptionalism

KEY MESSAGES

As policymakers, academics and representatives of the business world gather in Washington for the annual International Monetary Fund meetings, the theme of US exceptionalism is squarely back on the table and in the price, following recent resilient data.

By contrast, the eurozone economy is struggling to overcome headwinds, and the outcome of last week’s ECB meeting suggests markets are right to expect continued back-to-back cuts, unless and until data show signs of improving.

The week ahead is light on US data but heavy on Fed speakers, while this week’s European data, most notably the flash PMIs for October, carry most significance, in our view. We think markets will be more sensitive to an upward surprise in European data.

Finally, with less than three weeks until the US election, opinion polls suggest that the outcome remains a coin toss. This makes the medium-term outlook for the USD more uncertain, with a Red Wave more supportive of continued strength.

… Changing risk distribution: We think the stronger economic data have also shifted the distribution of risks around our central case of a soft landing for the US economy and a material recovery in the eurozone. Indeed, whereas in our Q4 2024 Global Outlook, we perceived risks to growth as decisively skewed to the downside in the US, recent data suggest a less uneven risk distribution. After all, a more resilient picture for growth now lowers the probability that firms will decide to lay off workers, with the labour market a key cause for concern in recent months.

… and on looking back …

MS: Sunday Start | What's Next in Global Macro: Looking Back from Over There

… Discussions about the Fed kept returning to whether the 50bp cut at the September meeting was a policy mistake. My personal view is “no” in that we will not see a resurgence in inflation because of that decision, but I do believe the Fed would have delivered only 25bp had the FOMC known that the September jobs report would be so strong, especially with the revisions to previous months. Against that backdrop, I heard very little pushback against our baseline call for a string of 25bp rate cuts. In short, we are on track for our soft landing. The front end of the curve is pricing our Fed call, the 10yr sits in the middle of the range and is consistent with our rates strategy team’s view, and risk assets seem supported by the moderation we expect.

Despite required civics classes in the States, I find myself reminding clients here as well as across the pond that meaningful changes to fiscal policy require control of both houses of the Congress, an outcome that current polling does not predict.

On immigration, I stress that it has provided a substantial, positive labor supply shock, supporting more than 3% GDP growth last year against a backdrop of continued disinflation. A sharp reversal of immigration, therefore, would be a stagflationary shock, slowing growth while boosting inflation. But a key secondary point is that immigration is likely to slow on its own, though the counterfactual is nearly impossible to know. Thus, the effects of immigration policy changes are a bit murky.

Bloomberg: The World’s $100 Trillion Fiscal Timebomb Keeps Ticking

IMF urges debt reduction as finance chiefs meet in Washington

Canadian interest rate cut, Russian rate hike anticipated

… somewhat more on same topic …

Bloomberg: US Interest Burden Hits 28-Year High, Escalating Political Risk

Treasury’s 2024 interest bill exceeded US spending on defense

The climb reflects a historically big fiscal gap, higher rates

… a note on the best lookin’ horse in the glue factory …

WolfST: Which Foreign Countries Bought the Recklessly Ballooning US Debt: An Increasingly Crucial Question. Many Piled it up. Cleanest Dirty Shirt?

Foreign investors had a big appetite all year for Treasury securities. But China lost interest, Japan struggled with the yen.

… The chart also shows how the importance of Japan and China has dwindled over the past 12 years, from being by far the top two foreign creditors in 2012, to being far below the financial centers and the Euro Area in 2024

The share of foreign holdings had dropped from the peak of 34% in 2015 to a low of 22.2% by October 2023, as the US debt ballooned faster proportionately than foreigners increased their pile of it – they increased their pile but more slowly than the debt grew…

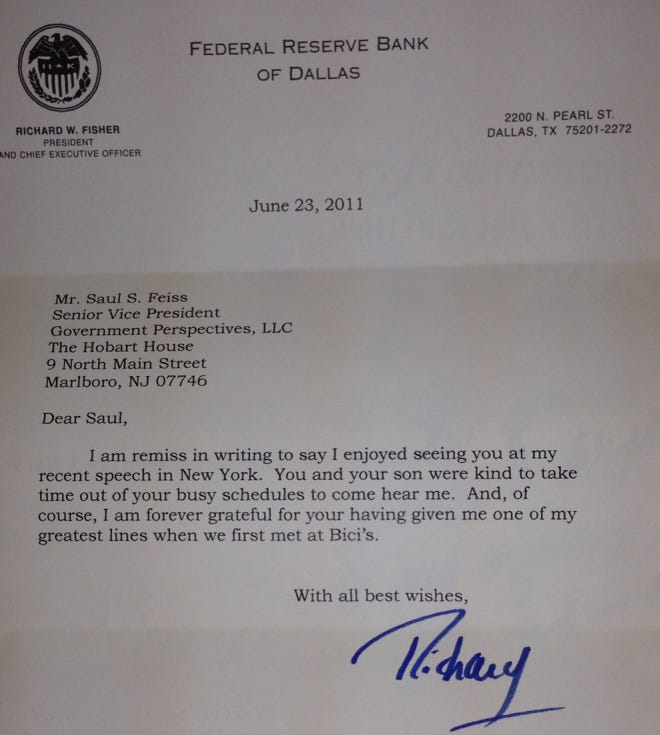

… And finally, in as far as the ‘glue factory’ reference as it relates TO TICS and holdings of USTs, i’m reminded of that time my partner (my father) and I ran in to then Dallas Fed president Dick Fisher at a restaurant (Bici, NYC) and got to talking about who was buying USTs and why … having large German bank clients trading (renting) in USTs vs Bunds, it was obvious to US being on the front lines, that folks weren’t doing so as any sort of political commentary but rather because it made RELATIVE sense … mentioning to Richard and using the analogy of how USTs play the role of the ‘best lookin’ horse in the glue factory’ …

FRB: Rangers, Yankees and Federal Open Market Committee: One Game at a Time October 19, 2010 New York, N.Y.

… Before concluding, I want to return to the TIC data I mentioned earlier. Yesterday, I asked a trader of sovereign debt how he interpreted the recent numbers. His answer: “We are still the best-looking horse in the glue factory.” It was a witty reply. But it was disturbing. This is America. Whether we are Ranger or Yankee fans, Texans or New Yorkers, we have been blessed to live in the most prosperous nation on earth. We cannot now accept simply being the “least worst” among major economies. We must be better than the rest.

This cannot be accomplished by the FOMC alone. Whatever we do with monetary policy will be of limited utility, if not counterproductive, unless it is complemented by sensible fiscal policy that restores confidence and puts the American people back to work. We are not glue-factory horses. We are thoroughbreds. It’s time to put us back on track.

… and while our relationship didn’t go too far, I would say he’s one of the best ever to come from state of TX and is not surprising that he and Danielle DiMartino Booth worked so closely and she’s now one of the best in the biz …

the Wall Street Journal was founded in 1889 by Charles H. Dow, of Dow Jones & Co.The paper is now a subsidiary of News Corp., part of its Dow Jones news business that remains separate from the Fox News television station.")

What an honor! Good day go Yanks! As a Giants fan can't stand Dodger blue and the Mets just feel artificial.