Good morning … Yesterday’s ISM (services) combined with Neel Ka$hkari (nv, MN) and JPOWs commentary over the weekend reaffirming what it is most everyone knew … March rate cuts have left the building and while Global Wall now trying to coalesce ‘round May, one would have to assume that TOO is now suspect.

Putting these bond market moves into SOME sorta of context …

DBs Early Morning Reid: … So there was plenty of fresh momentum behind the selloff. Indeed, since the jobs report on Friday, the 10yr Treasury yield has risen by +27.8bps, which is the biggest 2-day jump since June 2022, back when the Fed suddenly geared up to hike by 75bps for the first time since the 1990s. So we shouldn't underestimate the moves or the volatility…

… AND from The Terminal …

Bloomberg: Treasury Yields Jump as Traders Move to Price Out March Fed Cut

Powell says Americans may have to wait beyond March for cuts

Two-year yield rises to one-month high after his comments

… Monday’s move extend a rout that kicked off last week after data showed the US labor market was holding up far better than economists expected. It’s the latest tussle between makers betting the central bank is poised to unwind its aggressive string of interest-rate hikes, and policymakers wary of declaring victory over inflation, even as it slows from a four-decade high of 9.1%.

Goldman Sachs Group Inc., Bank of America Corp. and Barclays Plc are among Wall Street banks who last week pushed back their calls for the timing of the first Fed rate cut from March…

Thanks … Thanks for pushing back yer calls NOW …. This all is likely to be source / fodder of a CoTD sometime in the near future and if / when it pops up from those with far more capabilities than I, well, I’ll keep you posted.

I’ll leave YOU to infer whatever you’d like in changes of pricing of the past couple days, however it is you can / will. At this rate, I’m only able to fuss ‘round with CMEs FedWatch Tool (HERE).

While the changes / nuance here important to keep in mind along with ALL incoming Fedspeak, days like YEST and Neel’s commentary in mind, as a NON VOTER this either a trial balloon OR simply doesn’t matter … that’s for YOU to decide and as a reminder, as we’re playing along here at home, with litany of Fedspeak coming, keep your friends close and your #FOMC101 list of who’s who CLOSER) essay (Policy Has Tightened a Lot. How Tight Is It?)

In any case, seems like the markets are trying so hard to tell us something … perhaps they are buying in TO no chance of 6 CUTS in 2024?

That horse left the barn and on the positive side, today there IS a liquidity event (3yr auction) and one COULD view recent (semi historic) selloff of the past couple days as a concession …

… and with 3yy moving from overBOUGHT to overSOLD so quickly AND yields up near psychologically important 4.25% I’d ask IF 3yy are worth a stab, at least tactically here / now?

Food for thought…#Got3s?

Now in as far as the ISM (services) came and went….

CalculatedRisk: ISM® Services Index Increases to 53.4% in January ZH: ISM Services Accelerates, But Prices Surge Most In 11 Years

… oh, ok maybe JPOW not a complete idiot, then?? But wait, what then of banking and loan demand …

CalculatedRisk: Fed SLOOS Survey: Banks reported Tighter Standards, Weaker Demand for almost All Loan Types

ZH: Banks Report Tighter Standards, Weaker Loan Demand But Some Improvement As Financial Conditions Ease

… The January SLOOS also included a set of special questions inquiring about banks’ expectations for changes in lending standards, borrower demand, and loan performance over 2024. Banks, on balance, reported expecting lending standards to remain basically unchanged for C&I and RRE loans, but to tighten further for CRE, credit card, and auto loans. In addition, banks reported expecting loan demand to strengthen across all loan categories, and loan quality to deteriorate across most loan types.

In other words, banks anticipate further tightening lending standards across most categories, even as consumer fight with each other for what little loan availability exists (all of this, of course, is moot once the next round of the regional bank crisis arrive in March when the Fed's BTFP program expires, and when most lending once again grinds to a halt).

… kinda a push. Like kissin’ yer sister (i’m sure she’s lovely, don’t take that the wrong way)

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher and the curve a touch steeper ahead of Treasury supply and a brace of Fed speakers. DXY is marginally higher (+0.07%) while front WTI futures are too (+0.5%). Asian stocks saw massive gains in China and mixed outcomes elsewhere, EU and UK share markets are little changed while ES futures are showing UNCHD here at an early 6:30am. Our overnight US rates flows saw real$ buying across the curve during Asian hours. During London's morning session the desk reported better buying too (real$ in 5's to 7's a feature) despite prices drifting back to unchanged after rallying in Asia. As colleagues noted, "That buying has remained consistent throughout the back-up." They added that there appears to be renewed/refreshed demand for the front-end after recent adjustments to Fed pricing. Overnight Treasury volume was decent at ~120% of average with 30yrs (176%) seeing the highest relative average turnover overnight…

… and for some MORE of the news you can use » The Morning Hark - 6 Feb 2024 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

February Can be a Tough Month We have studied the monthly, quarterly, and annual returns in the stock market since 1980 -- and February is not one of the best months. On average, stocks rise less than 0.1% in the shortest month of the year. Only the months of August and September have generated weaker average returns. Yes, there have been some strong Februarys, including 7% gains in 1986, 1991, and 1998, as well as a 5.5% surge in 2015. But there have been some clunkers as well, including a 6% drop in 1982; a 9% plunge in 2001 during the "dot-com" bust; an 11% collapse near the bottom of the Great Recession and bear market in 2009; and, of course, the 20% bomb in February 2020, as the coronavirus began to spread around the world and the economy tumbled into a recession. Last year was nothing to write home about, with a 1.9% drop during the month. This time around, February is starting with a bit of positive momentum, as returns have been in the black for each of the past three months. Earnings season continues and, as usual, companies are outperforming Street expectations. However, equity investors got a surprise message from the Federal Reserve last week that interest rates probably won't be coming down as fast as the Street had expected. While we continue to think the general fundamentals for stocks are positive (profits are rising, valuations are reasonable, the economy is growing, and rates are headed lower), we still suggest that equity investors focus on well-managed companies with clear growth prospects and clean balance sheets -- especially in February.

BARCAP: US Economics: ISM services confirms re-acceleration

The ISM services composite jumped 2.9pts in January to 53.4, led by a rebound in employment, corroborating the pickup in activity in recent months. An increase in the prices paid component to its highest reading since February further intensifies risks that the Fed will deliver fewer rate cuts this year than markets expect.

BARCAP January SLOOS: More evidence of a soft landing

January's Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) showed net tightening in lending conditions continuing to retreat from levels that had resembled a credit crunch earlier in 2023. Although loan demand continued to contract, conditions appear to gain considerable traction at the close of 2023.

BNP Quant Trades of the Week: Equity RV, US 5s30s steepener and short USDMXN (**NOTE** taking profit on 10yy SHORT from 1 FEB)

KEY MESSAGES Market Themes

Equities appear overbought, but we think it is not yet the time to position outright short equities. We continue to favour RV opportunities in equity, adding long US consumer discretionary vs consumer staples.

US and EUR curves appear too flat and US real yields have scope to move higher. We are entering a US 5s30s steepener.

We are short USDMXN as the USD continues to appear overbought.

New trade Ideas: USD 5s30s steepener, Short USDMXN, Long EU Oil&Gas (SXEP) vs EU Autos (SXAP), Short US Consumer Staples (XLP US) vs long US Consumer Discretionary (XLY US)

… Initiating USD 5s30s steepener: Following last week’s rates rally, MarFA™ Macro sees back-end USD rates as too low (Figure 2), with USD 30y and USD 20y appearing 12.8bp and 10.5bp too low, respectively, while front-end USD rates are starting to appear too high (Figure 1). This suggests an attractive risk-reward opportunity for USD curve steepeners, with USD 5s30s appearing 21.5bp too low, according to MarFA™ Macro (Figure 3).

DB: US Economic Perspectives - Outlook update: Back in (the) black and (so far) done dirt cheap

When we first adopted a mild recession as our baseline forecast, a key element was that, with an economy far from the Fed's objectives, the history of central bank-induced disinflations showed the path to a soft landing was narrow if not unprecedented. We now think the economy will land on this narrow path and that a recession will be averted with limited cost in the labor market.

The US economy performed as well as could have been hoped for in 2023. The labor market returned to better balance without unemployment rising materially and core PCE inflation fell below 2% annualized in the second half of the year. We see virtuous dynamics at play that could extend these positive developments, including an easing of financial conditions that has trimmed downside risks to growth.

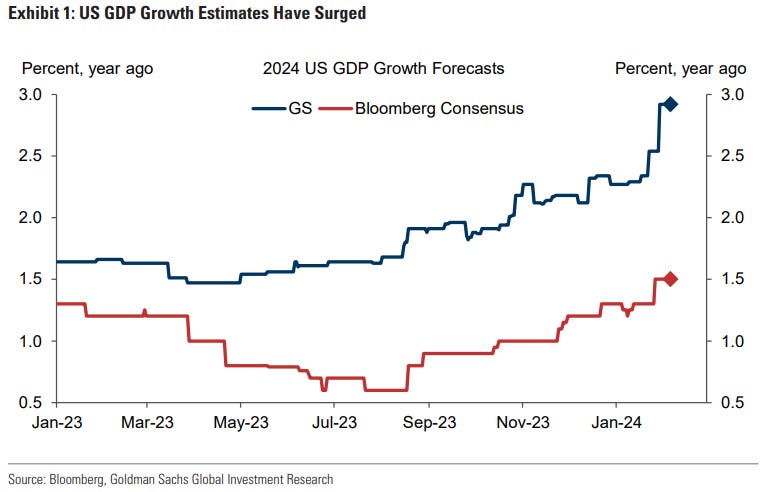

Our updated forecasts now see growth this year at 1.9% (Q4/Q4), up meaningfully from our prior forecast of 0.3%. Consistent with our more optimistic view on growth, we also anticipate that the unemployment rate will rise only modestly to 4.1% over the year ahead as payroll gains slow and labor force participation rises somewhat further.

Although inflation could firm some in the near-term, we ultimately believe it is sustainably falling towards the Fed’s target. Stronger growth is unlikely to derail this trajectory. Our inflation forecasts are little changed at rates within a few tenths of a percent of the Fed's objective, with core PCE and CPI ending the year at 2.2% and 2.6%, respectively.

These revisions maintain a case for Fed rate cuts this year, though less than in our prior forecast. We continue to anticipate that the first rate cut will come in June but that the Fed will only cut rates by 100bps this year. Next year, we expect the Fed to gradually move rates closer to a neutral level of 3.5%. Risks are balanced around our Fed expectations this year, but we see longer-term risks skewed towards a higher nominal neutral rate (e.g., 4%).

Risks around our new growth view are also reasonably balanced. Downside risks remain from the potential for greater pass through of prior Fed tightening and elevated geopolitical risks, which keep recession probabilities somewhat higher than unconditional historical averages. Conversely, we see reasonable prospects that growth continues to surprise to the upside, particularly as financial conditions have eased and with the potential for stronger productivity to continue to provide a boost.

We have been writing for some time that a key driver behind US growth exceptionalism is the economy's massively reduced sensitivity to interest rate hikes compared to the rest of the world. The 2010-2020 decade of Fed QE led to a big reduction in private sector interest rate risk, mostly thanks to the capital market intensity of the US economy. Below we update some of our favourite charts on the topic.

Starting with the corporate sector, we can see that interest expense continued to collapse through Q3 of last year, remarkably reaching the lowest since the early 1960s (chart 1). US corporates continue to earn money from higher cash holdings while paying interest on low-coupon fixed debt. Moving on to the household sector, net financial obligations are still below pre-COVID levels and the healthiest for more than three decades (chart 2). US households are very far from being financially stressed.

Comparing net corporate interest expense across the G10 shows just how unique the US has been so far in this cycle: it is the only developed economy where interest cost has gone down sharply (chart 3). In turn, relative policy transmission continues to do a great job at explaining relative growth surprises across the G10 over recent quarters (chart 4).

Does it make sense for the market to be pricing similar cumulative rate cuts from the Fed, ECB and many other central banks given the above? Does it make sense that the terminal rate gap between the Fed and ECB is a little above 1%, close to the historical average of the last three decades? As we argued last week, we don't think so. The real debate is not if the Fed cuts a few weeks sooner or later, but if it cuts by less or more than the rest of the world over the next two years. We continue to see the risks skewed towards less Fed tightening and therefore in favour of the USD.

Prima facie, the recent US data does not suggest much of a slowdown. If the next couple of quarters of forecasts are regularly based both on recent momentum, plus a view on financial conditions, there is not a particularly strong case to be made for much slowing. The market is then being forced to contemplate the "no landing" scenario much more actively. Below we distinguish between two very different "no landing" scenarios, as fully fledged members of four main "landing" possibilities. Thereafter, we outline the USD implications for each of these four scenarios, and how the part of the probability distribution that is USD negative is shrinking fast. All of a sudden, the burden of proof is on the USD bears not the USD bulls to make their case.

Goldilocks: ISM Services Increases Above Expectations

BOTTOM LINE: The ISM services index increased 2.9pt in January, somewhat above expectations. The composition of the report was strong, as the employment and new orders components both increased while the business activity component remained unchanged in expansionary territory.

BOTTOM LINE: The Federal Reserve’s January 2024 Senior Loan Officer Opinion Survey—conducted for bank lending activity over the fourth quarter of last year—reported that standards tightened at a slower pace versus the prior quarter. A smaller share of banks reported tightening standards for commercial real estate (CRE), but the level remained tight. Demand for both commercial and industrial loans weakened, but by less than in 2023Q3. On the household side, credit standards tightened on net for residential real estate loans and consumer loan categories, but by less than in the previous quarter. Demand for residential real estate categories and for credit card, auto, and other consumer loans weakened on net but also by less than Q3.

Our most out-of-consensus global view over the past 18 months has been that US growth would remain solid alongside declining inflation. Recently, however, some key indicators have been more than just solid, with GDP growing at an annualized rate of 4.1% in 2023H2 and nonfarm payrolls rising 353k in January. Both numbers are well above our estimates of the long-term sustainable trends in real output and employment. This raises the question whether the US economy is now growing too quickly to sustain the disinflationary trend. Are we seeing too much of a good thing?

2. We think the answer is no. Beyond GDP, we track two other measures of US growth, namely gross domestic income (GDI)—a conceptually equivalent measure of GDP that is calculated by adding up all income as opposed to all spending in the economy—and our current activity indicator (CAI). None of the three measures is perfect, but both GDP alternatives indicate a more muted growth pace. GDI is not yet available for Q4 but grew just 1.5% in Q3 on a quarter-on-quarter annualized basis and our CAI grew 0.8% in Q4, both considerably below the corresponding GDP growth rates. Based on these indicators, we still think that real output is at most growing modestly above potential, despite the much stronger GDP data…

… 3. We would also heavily discount the 353k January payroll gain because it was boosted by seasonal factors that anticipate larger start-of-year job separations than what is likely in the current low-turnover labor market with its subdued rates of hiring and separations…

… 8. Our market views remain broadly optimistic. While Fed cuts are likely to arrive at least somewhat later than we had anticipated before Wednesday’s FOMC press conference, the direction of travel remains clear and the pace of easing might be somewhat faster than we had thought earlier. We therefore don’t expect markets to pull back much further on their pricing of Fed rate cuts, barring significant upside surprises in the upcoming inflation data. Combined with our dovish views on the ECB and BoE, this implies modest downside for US and European rates in coming months. Meanwhile, global growth is on a good path, with manufacturing showing early signs of recovery after a lengthy malaise, which supports the constructive views of our equity, credit, and commodity strategists.

Former President Trump says that if elected to a 2nd term, he will not renominate Chair Powell when his term expires. Investors have asked about implications of this scenario. We expect Fed independence to endure but, while not our central case, there's a risk that communication changes & dissent grows.

SLOOS indicates lending standards historically associated with recessions The Federal Reserve's Senior Loan Officer Opinion Survey continued to report widespread tightness in lending standards today. The willingness to lend to consumers (make consumer installment loans) was little improved from that seen through 2023 and recorded a -17.9% net balance. Lending standards tightened across credit card, auto, and other consumer lending. Meanwhile, banks continue to indicate that demand from households for the same types of credit remains weak. This breadth in tightening of lending standards, alongside depressed demand for credit, has generally been associated with US economic contractions. However, in an interview on Bloomberg TV this morning, FRB of Chicago President Goolsbee — who saw the SLOOS report prior to its public release alongside last week's FOMC meeting — noted that while credit conditions had tightened in the past 18 months, he did not feel they were considerably tighter than one would expect given the increase in the federal funds rate…

… This report was largely consistent with our expectations last week: continued restrictive credit conditions. Looking ahead, in response to special questions in the January survey, banks indicated a cautious outlook for 2024. On balance, banks reported expecting lending standards to continue to tighten for CRE, credit card, and auto loans, and they anticipate standards for C&I and RRE loans to be little changed i.e. remain tight. While banks expect loan demand to strengthen across all loan categories given expectations that rates will begin to decline, they also anticipate a broad deterioration in loan quality in 2024 reflecting beliefs that the economic outlook will be less favorable.

ISM non-manufacturing index rises in January to 53.4

… Among the components of note, supplier delivery times lengthened after several subsequent months of easing, moving up 2.9 points to 52.4 (not seasonally adjusted). The prices index spiked up 7.3 points to 64.0, although that figure is well below its peak during the inflation run-up and within a standard pre-pandemic range. It is also the case that this is at odds with the S&P Global services PMI, in which both the input and output price indices were actually softer in January. The inventory index contracted again, and backlogs of work moved up 2.0 points to 51.4. The employment index traced its 7.4- point plunge in December — which marked its worst recorded level outside of a recession — but at barely above breakeven, it remained weak for an expansion. Stepping back, while the composite index is over 50 for the 13th consecutive month, the level of 53.4 is still relatively low for an economic expansion, and other services surveys have been soft too. While the services sector has been supported by strength in consumer spending, the levels in the ISM survey are relatively weak historically.

Roadmap - February 2024 Rally Continues, Leadership Shifts The S&P 500 rose 1.7% in January (18.2% in the post-October rally). TECH+ leadership was mixed for the month, with TSLA and AAPL down -24.6% and -4.2%. Small cap, high beta, and econ-sensitive stocks—which led the past 2 months—all lagged.

Robust Economic Releases Support Further Market Upside Economic releases have been particularly strong YTD, including payrolls, consumer confidence, and PMIs. Economic surprises have surged, while GDP forecasts improved and recession forecasts have fallen. This is reflected in fewer expected Fed cuts.

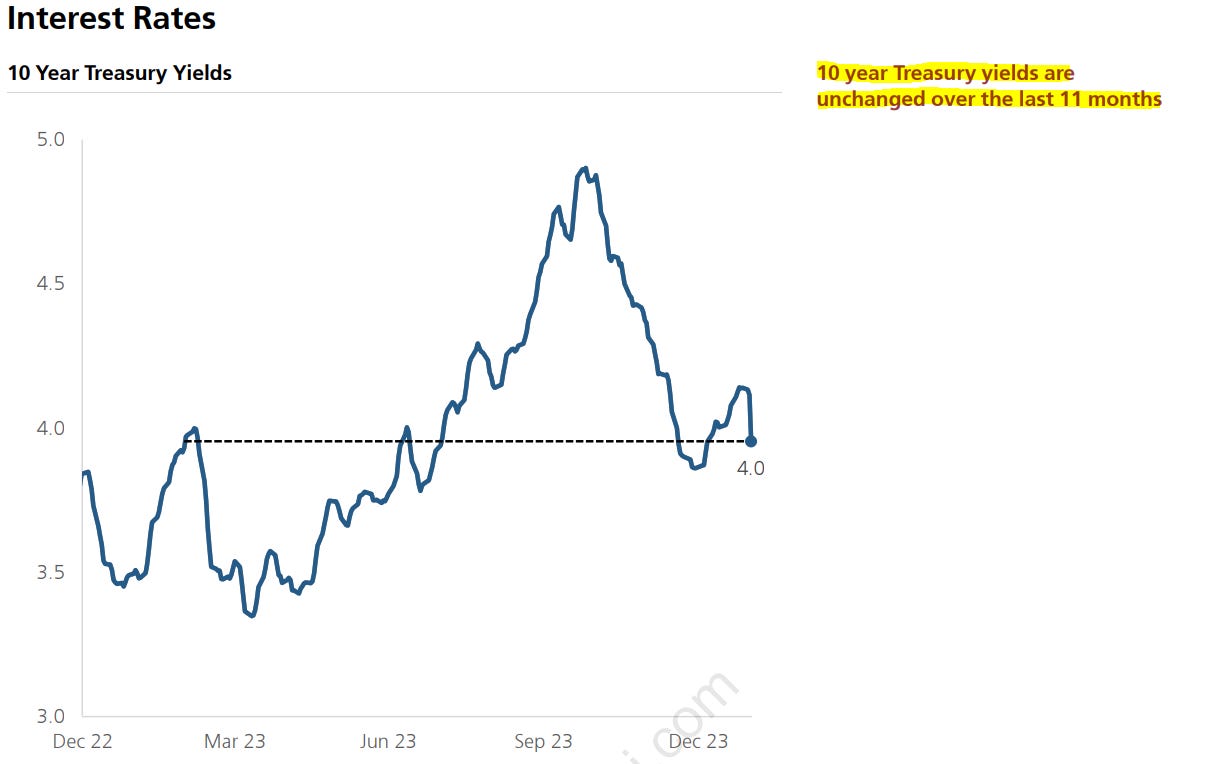

Fundamentals—Not Rates—Driving Stock Prices Interest rates have been of secondary importance to stock prices over the past 13 months (10-year yields are roughly flat over this period). Throughout the post-October rally, stocks have risen by similar amounts on both up and down interest rate days.

S&P 500 Target from 4850 to 5150, 2024 EPS from $225 to $235 …

There is a narrative that rising equity markets are good, and falling equity markets are bad. This is not true. Fairly valued equities are good, and bubbles or disorderly markets are bad. If the latest barrage of equity market measures by China’s government are aimed at correcting irrational pessimism and disorderly markets, they are economically beneficial. If they are driven by a desire to see equities higher just because they want equities higher, they are economically negative.

Wells Fargo: ISM Services Too Hot, Especially Prices

Summary The prices paid component stole the spotlight in today's ISM services report by posting the largest monthly percentage gain since 2012. Take a breath and remember that diffusion indices such as these are measures of breadth not magnitude. Still, it's hardly supportive of the case for rate cuts.

… And from Global Wall Street inbox TO the WWW,

Bloomberg (via ZH): Treasuries Reckon If Fed March-Cut Isn't Likely, Neither Is May

Bloomberg: Good Times, Bad Times, the Fed's not in a hurry (Authers’ OpED)

ING: Tight lending conditions to remain a constraint on US growth

US banks continue to tighten lending standards and expect loan quality to deteriorate with write-offs anticipated to rise through 2024. At the same time, loan demand continues to weaken. The economy performed very strongly through the second half of 2023, but high borrowing costs, tight lending conditions and a reluctance to borrow point to a slowdown

ING: ISM services rebound, but continue to track weaker than official US data

The disconnect between very strong official economic data, such as non-farm payrolls and GDP growth, and third party private data sources remains very wide. Today's ISM services report did improve after December weakness, but is at a level consistent with GDP growth closer to 1% than 3% and payrolls rising perhaps 50,000, not 350,000

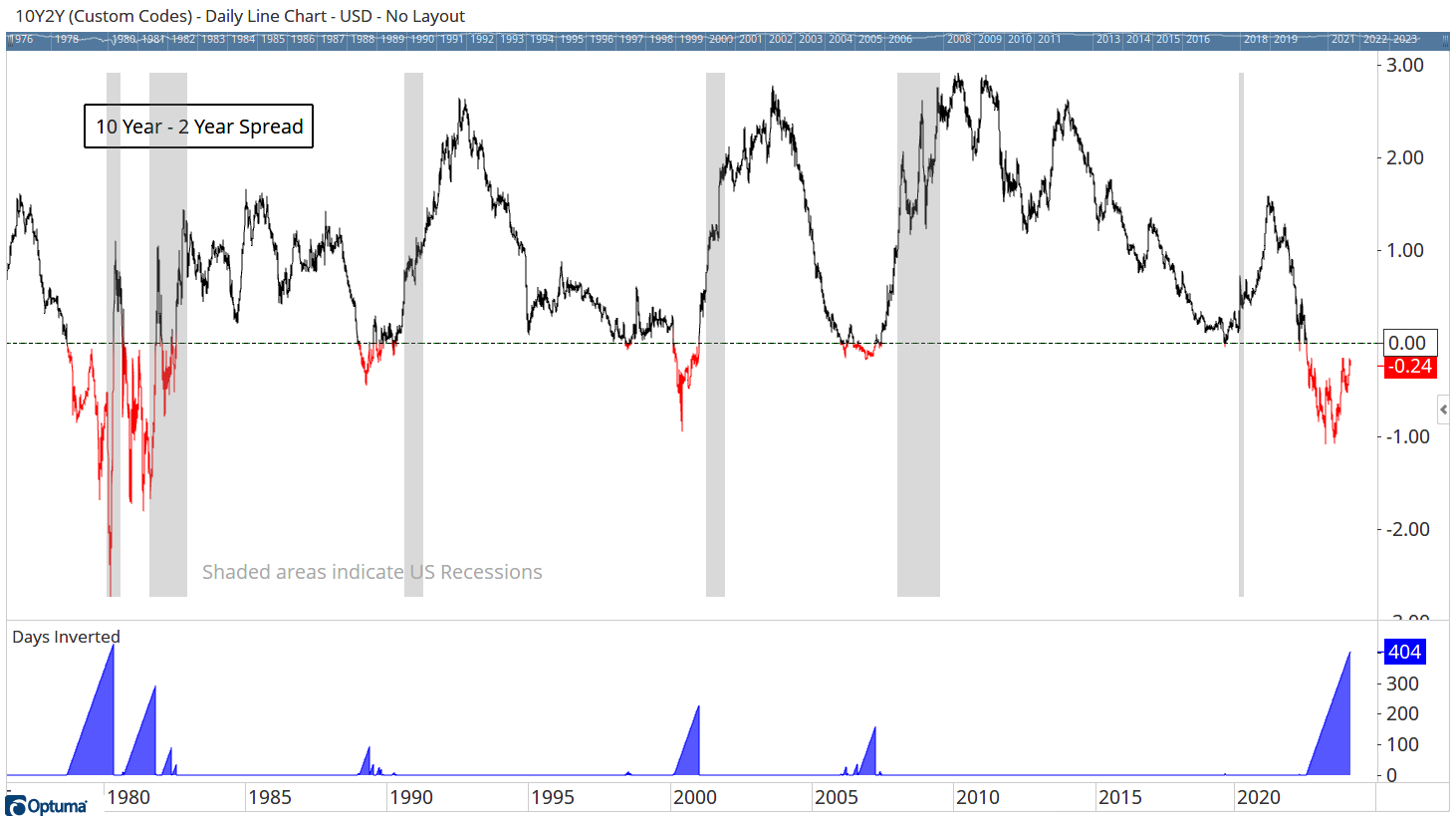

… 3/ 2nd Longest Period Inverted Yields Yields on Bonds are a reflection of the risk that the lender is taking when loaning money to the borrower (company, or Government). The longer money is loaned, the higher the risk that an event will occur that will cause default on the loan. This is why a longer-term loan usually has a higher interest rate (yield).

Inverted Yields occur when short term rates are higher than long term rates. The FED increases rates, and a higher yield is achieved in short term bonds than longer terms. Why would you lock up money for 10 years when you can get a higher return with a 2-year lockup?

We often talk about Inverted Yields being a warning of a recession and what is evident when we look at Chart 3 is that it usually is an early warning of an impending recession. There are some reasons to question that, however.

Our current period of Inverted Yields is now the second longest in the last 50 years. At 404 days (at time of writing) we’ve not entered into a recession and all around the world, central banks are beginning to talk about lowering rates once more.

Will we avoid a recession? The economic effects of recent rate increases will still take more time to filter through, but there are three facts that are positive and may make this time different:

We have gone this long without a recession.

The spike of inflation was due to supply issues rather than overconsumption. Unlike 2008.

Rates are more likely to start falling soon.

These, and the fact that the S&P 500 is powering ahead (see below) are all good signs that we are in for a few good years to come.

…. AND before signing off for the day,

RIP, TK … THAT is all for now. Off to the day job…

Wish Trump would lay off of Powell already, I don't believe ripping the FOMC chair has ever helped a Pres or candidate....does Trump realize just how many COMMIES there are on the FOMC board & within the Eckles building? A mandatory debate question, that certainly WONT be asked is who does big Trump have in mind for a FOMC chair, Yellen-Bernanke types? Much as I want to rip Greenspan & Powell, they're FAR superior in comparison.

Will read soon....car appointment....wanted to post this:

In Memorial:

https://youtu.be/aIq1LvzSLsk

Toby Keith - Should've Been A Cowboy (Official Music Video)

He was 62.

Wish Trump would lay off of Powell already, I don't believe ripping the FOMC chair has ever helped a Pres or candidate....does Trump realize just how many COMMIES there are on the FOMC board & within the Eckles building? A mandatory debate question, that certainly WONT be asked is who does big Trump have in mind for a FOMC chair, Yellen-Bernanke types? Much as I want to rip Greenspan & Powell, they're FAR superior in comparison.