while WE slept: USTs 'modest' bid on light volumes; Bostic and Duds SAY? Techs Thurs; "Bonds Are Still Crashing"; large language models = FED HIKE b4 CUT

Good morning … what a rough go of it for Team Rate Cut. Here are a couple examples of why I’m saying that…

Bloomberg: Fed’s Bostic Says Many Inflation Measures Moving to Target Range (Bostic IS a voter … #FOMC101 HERE)

Says Fed may be in a position to cut rates in fourth quarter

Breadth of inflation still quite high, Atlanta Fed chief says

Bloomberg: The Fed Thinks It’s Fighting Inflation. Think Again. (Duds latest OpED. NOT a voter but …)

Even at more than 5.25%, the central bank’s short-term interest-rate target might not be high enough to cool the economy.

Bloomberg(Authers OpED): Throwing in the Towel on Rate Cuts Everywhere (NOT a voter but some say opinions all created equally and HIS — Authers’ — apparently is one that is viewed to be more equal than others … fwiw)

Higher for longer can’t go on forever without damaging the economy. Real estate stocks are already paying a price.

… And it appears to ME that markets, generally speaking, are responding accordingly. Supply indigestion as the week began and there appears to be some steady / calm out there as the week and month comes to a close (tomorrow) … here’s a humble attempt to visualize the longer end of the curve …

… but … momentum. Famous last words (earlier in the week suggesting an overbought condition made supply items RENTABLE and that couldn’t have been further from truth or reality and so, noting the same here … well, maybe that axiom where even a stopped clock will be right 2x a day?

Take this all with a very large grain of salt. ALSO note Team Rate CUT appears to weigh in … you’ll see more below BUT …

… Investors holding cash or money market funds, or those with expiring fixed-term deposits, should consider managing their liquidity through bond ladders, structured investment strategies, or balanced equity-bond portfolios…

Moving along then and a quick recap (sans victory lap) of yesterday … Dallas Fed Mfg, 7yr auction ahead of Beige book made for another day in paradise …

ZH: 'Worst Since The Great Recession' - Dallas Fed Services Survey Slumps In May As Respondents Fear "Inflation Is Getting Pretty Scary"

ZH: Yields Spike To Session High After Subpar 7Y Auction

ZH: Bond Yields Soar As Rate-Cut Hopes Plunge; Stocks, Oil, & Gold All Sold (Team Rate CUT yet to weigh in …?)

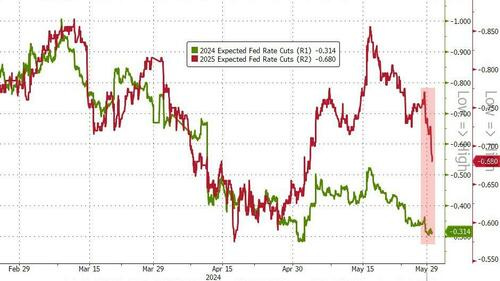

A quiet macro day in the US - mixed bag of regional Fed survey data (Richmond Manufacturing good, Richmond Biz Conditions bad, Dallas Services bad) and plunging mortgage apps) - followed a hotter than expected inflation print in Germany, which sparked a further hawkish shift lower in rate-cut expectations with 2024 falling back to a 50-50 coin toss for 2 cuts or 1; and 2025 tumbling to less than 3 more cuts...

… AND here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher, led by the belly, aided by constructive performance in Gilts/EGBs on most in-line inflation data in Spain. Flows have featured selling in the belly from CTAs, offset by some demand from real$. Commodity futures are weaker (HG -2.5%, CL -0.4%), with equity performance also souring in APAC (SHCOMP -0.6%, NKY -1.4%, KOSPI -1.6%). UST volumes are ~75% the 30d average, and S&P futures are showing -21pts here at 7:15am.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: US equity futures softer, DXY unwinding recent advances & JPY is bid; US Q1 GDP/PCE due … Bonds have bounced modestly from recent lows, with sentiment improving following a robust JGB auction … USTs have bounced modestly following Wednesday's soft 7yr auction, in part thanks to a robust JGB auction. USTs are near highs of 108-09+ vs Wednesday's 107-31 post-auction WTD base.

Rough estimate for direction of rebalancing needs We use the framework introduced in the report Pension fund rebalancing and UST demand to estimate the expected May month-end rebalancing flows. The rebalancing needs of a portfolio that contains two assets (with allocation weights w1 and 1-w1) and N assets under management is a function of the relative total performance of the two asset classes (r1-r2):

Rebalance = N * w1 * (1-w1) * (r1-r2)

With the S&P total return in the month to date at c.5.5%, the 10-year+ UST index c.3.5% total return over the same period, and corporates c.1.8%, the expectation is for rebalancing flows out of equities and into fixed income for the month (with corporates favored over USTs in the rebalance).

Our expectations for rebalancing flows In our framework (see below), we see c.-$36bn of rebalancing flows out of equities (the standard deviation of monthly equity rebalancing flows over the last three years is c.$21bn, so this is a -1.7σ rebalancing month). In the FI space, the flows break down as c.$3bn into Treasuries (a +0.4σ rebalancing flow), c.$25bn into Corporates, c.$7bn into Agency and GSE-backed securities, and c.$1bn into Mortgages (the relative outperformance of USTs versus other FI assets is significant in the May rebalancing flows). Significantly, these results may be a decent gauge for a broader class of investors with relatively stable allocations and monthly/quarterly rebalancing needs.

Caveat 1 – Month-end versus quarterly rebalance … Caveat 2 – Rebalance in the broader context of de-risking …

View: A patient summer of buying dips Short term: MACDs and patterns say yields bounce back Medium term: 1H24 higher yields, 2H24 lower yields

Five things the US yield charts say

Upside risk for US 2Y Yield. A small double bottom targets 5.05-5.10% in June. In the weekly chart, we still cannot rule out a retest of cycle highs +/- 5.25%.

US 10Y Yield: Base case is to be long for this summer/fall. We prefer to nibble at 4.6%, buy 4.75%, and “load the boat” if above 4.85%.

US 10Y Seasonals: Since 1963, the seasonal peak for 10Y yield is May 13-20 (behind us). When the 10Y yield has been up in January, the peak has been +/- August 9 (patience?).

US 5-, 10-, and 30Y yield weekly chart uptrends YTD are still supported by trend lines and base patterns. We may see better levels to buy in June-July than now.

Macro mismatch: The US U-Rate has made three higher highs and higher lows and a two-year new high to favor buying UST dips. However, the BCOM index has a head and shoulders base and golden cross signal, implying a commodities rally. This may cause inflation to stick longer and supports yields this summer.

… US 10Y Seasonals One curve says peak in May, another August = Buy summer dips The average trend of the US 10Y yield since 1963 is up into May, it tops in May-August, and then it declines into year-end (dark blue line in Exhibit 1)…

…The red line in Exhibit 1 below graphs the YTD net change in US 10Y yield in 2024, normalized to the other curves. The rise in yield so far this year has been impulsively higher, exceeding all average comparisons. All lines suggest that the trend gets choppy in May.

Normalization after the March-April swing is likely to have driven payrolls up to 200k in May, we estimate. If early Easter pulled some hiring forward, 315k in March overestimated the underlying trend, while 175k in April came in short.

We project the unemployment rate to have remained unchanged at 3.9%. The breakdown of the flow into unemployment is key to watch with new layoffs contributing to the rise in the jobless rate in April.

The unemployment rate rising to at least 4.1% in both May and June, coupled with persistent weakening in payroll growth to below 100-150k over the next few months, would signal the labor market is at risk of a more rapid weakening than just a welcomed rebalancing, evidenced so far.

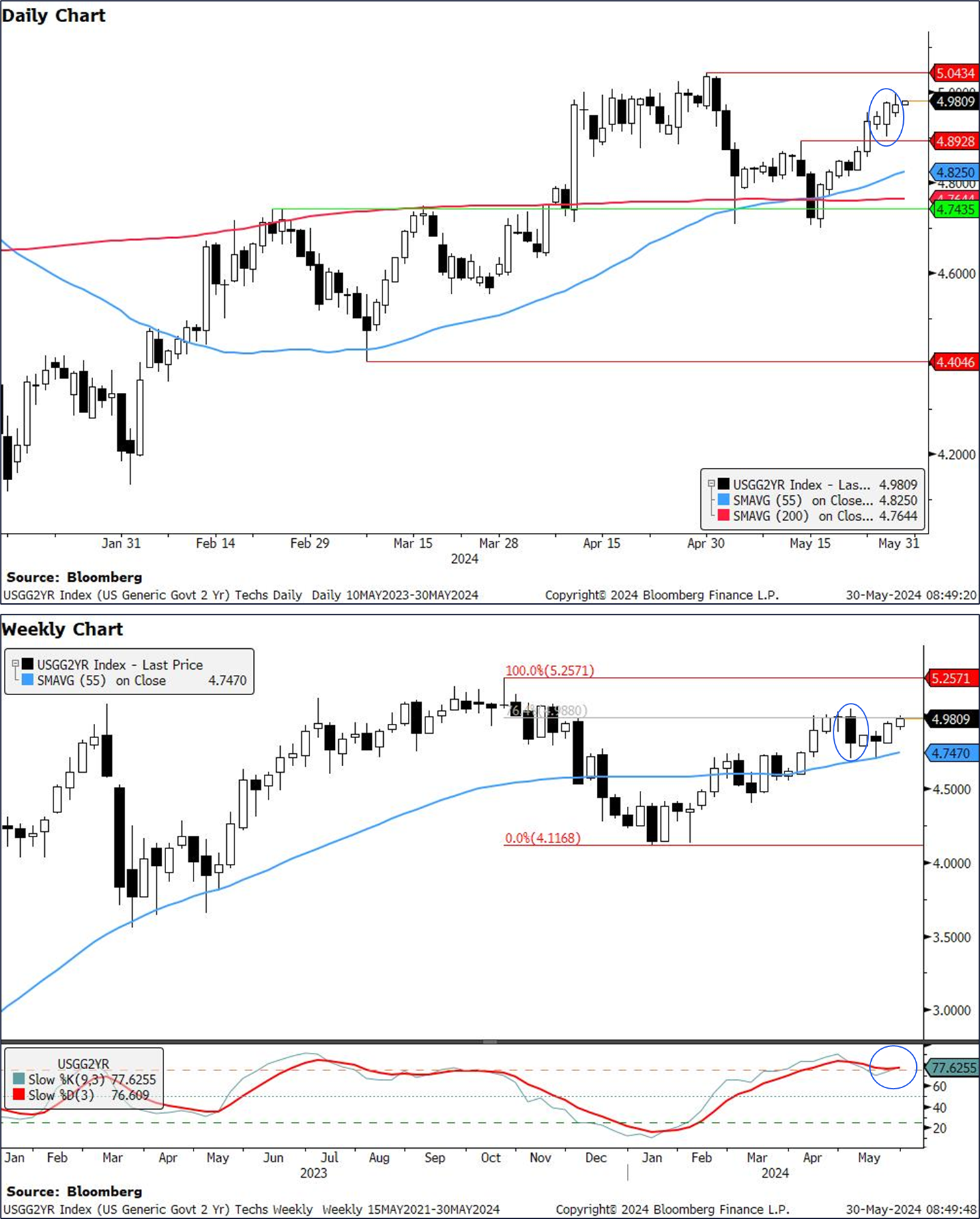

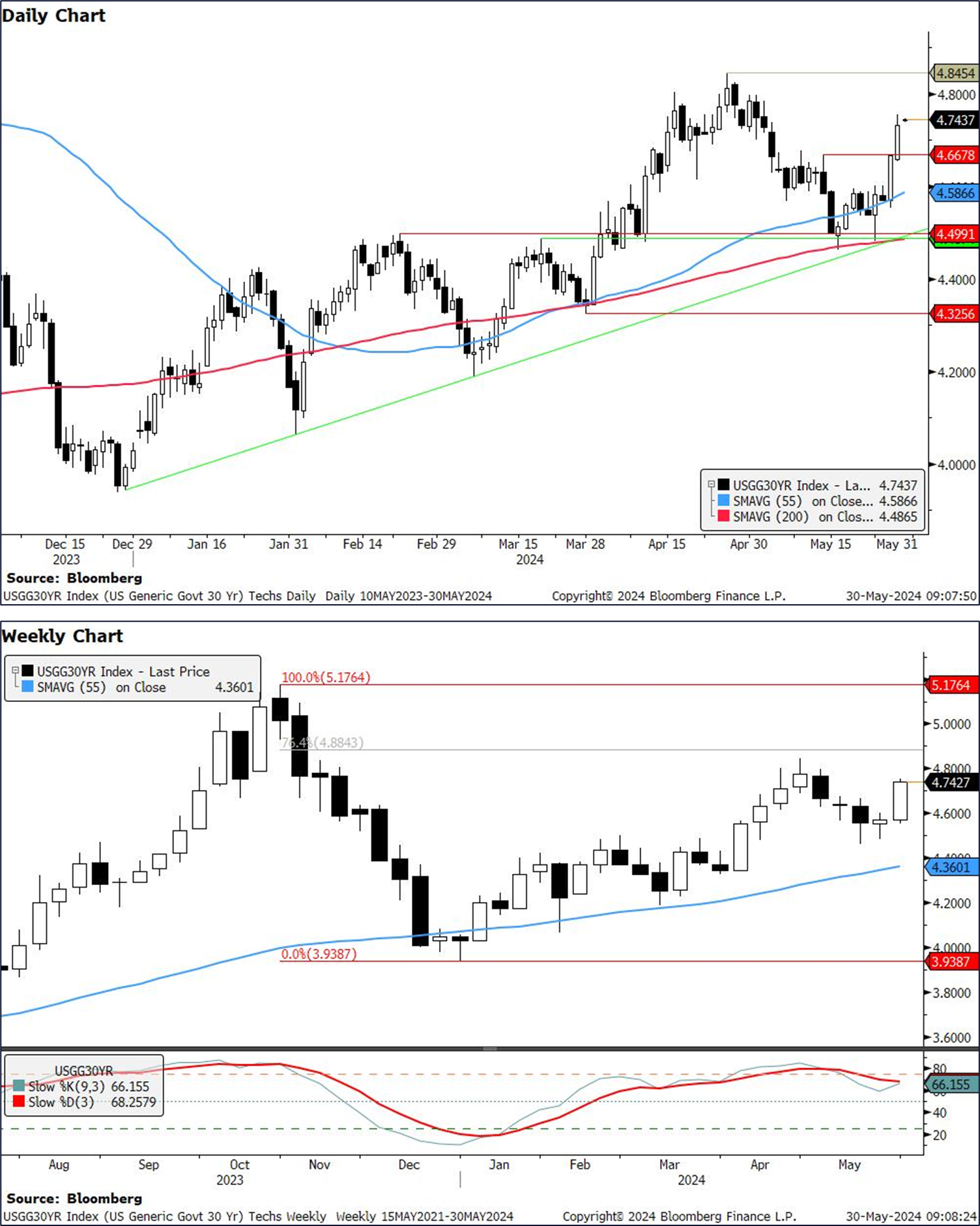

CitiFX US rates: Forced rethink (ahead of month end I’ll relay very front and back end but entire note / levels to watch / are of importance IMO)

Price action in treasuries has seen us breach some key levels, leaving us wrong-footed. Short term, techs now suggest we are likely to see a continuation of the US rates selloff as we head into core PCE data on Friday. Where we close there will be very significant in techs, since it is also the weekly & monthly close.

Key levels to watch:

US 2y yields: 4.98-5.04% resistance, 4.74-4.76% support

US 5y yields: 4.7%-4.75% resistance, 4.36% support

US 10y yields: 4.73% resistance, 4.35% support

US 30y yields: 4.84%-4.88% resistance, 4.50% support

More notes: The recent rates selloff means that we are now even further from closest cover levels in futures…

US 2y yields US 2y yields posted an 'outside day' candlestick on May 28 and we are now testing the key 4.98-5.04% resistance level (76.4% Fibonacci, April high, psychological level, and where we posted a weekly outside candlestick from post the last jobs data). This happens while weekly slow stochastics is looking like crossing back higher into overbought territory.

Short term, we expect yields to continue rising into the upper end of the band (5.04%). The key question here is IF we can sustain a weekly & monthly close above the 4.98-5.04% band, which would open up a larger move higher towards 5.26% (2023 high). On the other end, support can be found at 4.74-4.76% (200d MA, Feb high)

…US 30y yields Likewise, US 30y yields have another ~10bps to go before touching resistance at 4.84-4.88% (76.4% Fibonacci, April highs). Here, we are a little more skeptical that we could break higher, even if we see a beat in core PCE.

For support, we flag a convergence of multiple support points which makes the 4.50% level very strong.

Yesterday saw the release of the latest US money supply data for April. It was a significant milestone, as it marked the first time since November 2022 that the M2 money supply had been positive on a year-on-year basis.

If you want to explain the post-pandemic inflation surge in a chart, this is one of the easiest to use. After all, it was hardly surprising that increasing the money supply by 27% in a year would have some sort of consequences…

… At current growth levels M2 will likely be back at the pre-Covid trend by around the end of the year. What happens then is a big outstanding question. To maintain economic growth at current levels the money supply will likely have to start growing faster again soon. The main ways this could happen is by 1) the Fed loosening policy (rates or balance sheet activity), 2) banks lending more or 3) more expansionary fiscal policy.

This is all possible but is still an important thing to watch over the next few months. The fact that we now have YoY growth is a small step in the right direction.

With the US election less than six months away, we are taking deep dives into the economic policy issues that will have the greatest impact on the outlook. Recently, we assessed the budget deficit over the coming years and the potential effects of a change in immigration policies, especially for inflation (see "Fiscal outlook: A chicken in every pot is costly" and "How large was inflation mitigation from immigration?"). In this report, we consider the impact of the election on US trade policy.

Our focus is on changes that could come under a second Trump administration, the election outcome with the clearest differences from the status quo. We provide an initial assessment of the potential impact of another round of trade restrictions, with particular focus on growth, the labor market, inflation, and the Fed.

The experience of 2018-2019 serves as a useful, although possibly watered down, template for how these policy changes could proceed and how they might impact the economy. Our analysis suggests that the considerable tariffs – e.g., a 10% universal baseline tariff, tariffs of 50-60% on imports from China, and others – could raise substantial revenues, though at the expense of weaker growth and higher inflation. We provide an initial quantification of these effects.

Ultimately, trade protectionism would act as a negative supply shock. Such a shift could counteract at least some of the positive supply dynamics that are currently allowing strong growth to coincide with disinflation. With inflation already well above the Fed's target, and upside inflation risks still top of mind for monetary policy makers, we see trade policies as possibly adding another reason to keep the Fed on hold into 2025. This is a hawkish risk to the Fed outlook we detailed in our last update report (see "(Pushed) Back to December").

… 1. Spike in trade policy uncertainty The trade war in 2018-2019 lifted trade policy uncertainty to unprecedented levels, at least dating back to the early 1960s. As evidenced in Figure 2, trade policy uncertainty, as measured by the Federal Reserve Board staff or the Baker, Bloom and Davis methodology (2016), rose to record high levels during the last Trump Administration. According to Fed staff estimates based on historical statistical relationships, the two spikes in trade policy uncertainty in 2018 and 2019 were likely to subtract more than a percentage point from GDP into the first half of 2020.

Yesterday equities were a little upset because bonds were a little upset because of weaker demand at a US bond auction. Should investors be upset? This is not a US version of the UK’s Truss debacle. Markets are not disorderly and government policies are not destabilizing. The absolute level of debt is not a concern—many countries (including the US) have had and do have higher debt ratios. The political polarization that prevents a policy for a sustainable deficit is a concern, but is probably more a background worry for now.

The Federal Reserve’s Beige Book was somewhat downbeat. Risks to economic growth were highlighted (political bias may have had an influence on responses). Consumer rebellion against price increases was noted—the final stage of a profit-led inflation episode…

With inflation easing, we expect most major central banks to initiate their rate-cutting cycles over the coming months.

While we can't know for certain exactly when or how deep central banks will cut their policy rates, we think it likely that they will remain below current levels for some time to come.

Investors holding cash or money market funds, or those with expiring fixed-term deposits, should consider managing their liquidity through bond ladders, structured investment strategies, or balanced equity-bond portfolios.

… Positioning before it is too late We cannot know for sure the exact timing of the next policy moves from central banks, but we can be reasonably certain that the direction will be lower. By the time the cuts come, markets will have already repriced for lower policy rates, resulting in reduced return opportunities for investors. Investing ahead and in anticipation of the cutting cycle is the best way to avoid this, in our view.

Yesterday, Minneapolis Fed President Neel Kashkari told CNBC that he wants to see "many more months of positive inflation data" before he's ready to cut rates. He also didn't rule out a hike. Fixed-income investors are starting to realize that this is the new party line from the Fed. Earlier this year, we argued that there was no reason for the Fed to rush to lower the federal funds rate (FFR) and wrote that in a March 25 Financial Times op-ed.

The higher-for-longer outlook for the FFR weighed on demand across this week's 2-, 5-, and 7-year Treasury auctions as evidenced by weaker bid-to-cover ratios (chart)

The 2-year and 10-year Treasury note yields rose to 4.96% and 4.61% today (chart). In our normal-for-longer scenario, the 10-year yield remains rangebound between 4% and 5%, which is where it was before the Great Financial Crisis which was followed by abnormally low interest rates.

The higher-for-longer scenario also weighed on stocks in recent days with the S&P 500 equal-weight index significantly underperforming the market-cap-weighted index (chart)…

… And from Global Wall Street inbox TO the WWW,

AllStarCharts: Bonds Are Still Crashing (yea and these ‘allstars’ aren’t simply throwing out clickbait ?? hey, it works, they’ve got a thriving clickbait biz and i’ve got … well … this :) anways, BONDS are NOT TLT … TLT simply reflect moves after the fact and I know given my former seat on the front lines … they are 2nd or 3rd deriv from trading desks and actual derivs traders … but … well, whatevs, i’m now not even an armchair QB yellin’ at the TV when the rabbit ears antenna force my picture to lose some clarity … )

This historic bond market crash continues.

And to be fair, it might not seem like a “Crash” because bond market volatility is still relatively low.

So it’s just been a slow painful grind lower.

But there’s no evidence that it’s over.

You can see the Japanese Yen continuing lower as well….

So what are the implications?

Well, think about it.

Falling bonds = Rising Interest Rates.

Falling Yen = Stronger Dollar.

Higher Rates & Dollar = Headwind for stocks.

We’ve seen it for most of this year.

Yes, the Nasdaq Composite closed at a new all-time high yesterday…

Apollo: Quantifying Fed Sentiment

The Bloomberg natural language processing model analyzes Fed speeches and currently shows FOMC members moving toward a tightening bias, see chart below.

Note how the model never predicted rate cuts in 2024. Instead, Fed sentiment has simply been less hawkish in 2024 than in 2022 and 2023.

The bottom line is that this Fed sentiment model using data back to 2009 shows that Fed communication continues to favor Fed hikes rather than Fed cuts.

The weak US Treasury auctions over the past two sessions have helped push yields higher and resteepen curves. But the backdrop is still too-hot inflation and other data continuing to suprise to the upside. The focus in the eurozone today is on regional inflation data from Spain and Belgium

ING FX Daily: Bond sell-off softens risk environment

A series of softer US Treasury auctions and a sell-off in the longer end of the bond market is weighing on risk assets and providing some support to the dollar. This may well just be a short-term swing ahead of Friday's key US data release, but it is a trend worth watching. Elsewhere, we are seeing some profit-taking in Mexican and South African currencies

WolfST: Corrected: Status of Banks’ Unrealized Losses in Q1: Worsened after Brief Rate-Cut-Mania Relief

Rate-cut-mania soothed the pain, but it’s over.

… AND what is said in the tweet to be one of the funniest video I've seen in a long time … hard to disagree … watch THIS and enjoy.

Our man Simon White has an interesting twofer today on ZH-It won't be a shock to see another bank failure; and Yellen pivot is fading. Can't wait for your reaction!

Amazing video I LOVE the incredulous look of the judge!

Our man Simon White has an interesting twofer today on ZH-It won't be a shock to see another bank failure; and Yellen pivot is fading. Can't wait for your reaction!