Good morning … Not sure if one can or desires to infer some market interpretation from last nights rumble in the jungle (?) but a couple charts / points of interest on heels of the Trump Inflation BOMB! narrative …

ZH: 'Beware The Trump Inflation Bomb!': New 'Experts Agree' Narrative Just Dropped, Nobel Laureate Edition

… I could go on but won’t. I’ll just assume you watched the debate last night and have made your own conclusions.

AND ahead of all important flation report and then week, month and QUARTER END, I’ll be looking in TO the longer end for some clues because … of said inflation BOMB narrative AND, well …

30yy: momentum is bearish but we’ll have a look at weekly, monthly and quarterly charts in days ahead …

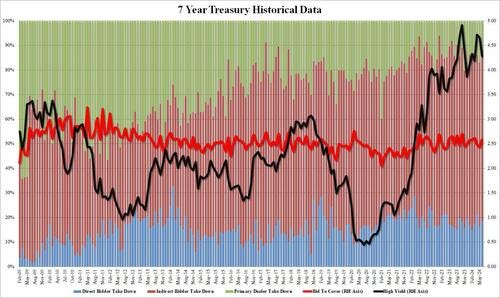

… In as far as the turnout for 7yy ahead of months end, before the debate …

ZH: Stellar 7Y Auction Sends Treasury Yields To Session Low

… The internals were even better, with Indirects awarded 69.65% up from 66.88% and the highest since March. And with directs awarded 18.5%, up from 16.1% last month and above the recent average of 17.6%, Dealers were left with just 11.9%, the lowest since October '23.

Overall, this was another very strong auction, and not surprisingly yields promptly slid to session lows in the secondary market with the 10Y down to 4.278%, at session lows, and about 5bps down on the day.

… and these results may have been impacted by yesterday’s data which seemingly skewed towards and in favor OF … Team Rate CUT …

BondDad: Initial claims remain positive, while continuing claims break out negatively from 12 month range

CalculatedRISK: Q1 GDP Growth Revised Up to 1.4% Annual Rate

ZH: Continuing Jobless Claims RIse To Highest Since Nov 2021

ZH: Final Q1 GDP Print Confirms Sharp Consumer Slowdown

ZH: Core Durable Goods Orders Decline In May, Shipments Plunge

… Core Capital Goods Orders (non-defense, ex-aircraft) plunged 0.6% MoM (well below the +0.1% exp), matching the biggest drop this year.

Furthermore, Capital Goods shipments non-defense, ex-aircraft plunged 0.5% MoM - a big drop for a key signal of business spending and GDP.

How many times can a data series be downwardly revised before conspiracies about manipulated data flip from theory to actual 'standard operating procedure'?

ZH: US Pending Home Sales Unexpectedly Plunged In May To A New Record Low (ahem … on a YoY — so economically workbenched — basis)

… That dragged the YoY change down 6.6% to a new record low...

… and with that in mind, HOPE apparently is still an ‘official’ FOMC voting strategy …

Bostic: Renewed Hope on Inflation but More Confidence Needed (i got nuthin)

… here is a snapshot OF USTs as of 715a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are moderately cheaper and steeper on ~95% 30d volumes, some light selling seen in the franchise as markets digest the US presidential debate ahead of the PCE data. The OAT-RX spread is back to widening (+3.75bps) alongside weaker French equities (-0.3%), while USDJPY is stable above 160 after some verbal intervention overnight from Suzuki. Commodities are buoyant (BCOM +0.7%, CL +0.8%, HG +1.2%) as well, with Chinese equities bouncing (SHPROP +0.7%) alongside Japan (NKY +0.6%). S&P e-minis are showing +20pts here at 7am.

… US 10y Yields: saw the local range support at 4.33% respected yesterday, with the range-lows now at 4.18%. Daily momentum is turning bearish from overbought territory.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US equity futures bid, USD flat and Bonds subdued post-Presidential debate; US PCE due … Bonds are subdued following the Presidential debate which saw the odds of a Trump victory inch higher … USTs came under pressure in APAC hours as the US election debate got underway. A debate which saw Biden perform particularly poorly with the odds of a Trump presidency lifting. Currently trading around 110-05 ahead of US PCE.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BARCAP: Third Q1 GDP estimate: Still in decent shape (Team Rate Cut be like, ‘This Is Fine’)

The third estimate of Q1 GDP growth was marked up by 0.1pp, to 1.4% q/q saar, reflecting upgrades to business fixed investment, inventories and net exports, which were partly offset by weaker consumer spending estimates. Final sales to private domestic purchasers were up 2.6%, indicating still-firm domestic demand.

BARCAP June employment preview: Gradual moderation (early or is it just me?)

We expect a 200k increase in nonfarm payroll employment in June, slower than May's 272k gain, with average hourly earnings rising 0.3% m/m (3.9% y/y). On the household side, we look for the unemployment rate to round up to 4.0%.

The trade deficit widened to $100.6bn in May, while durable goods orders rose a modest 0.1% m/m. The combination of these data and the third estimate of Q1 24 GDP led to composition changes in our Q2 24 GDP tracker, but our tracking estimate remains unchanged at 2.1% q/q saar.

Job growth slowing to an estimated 175k in June (from 272k prior) would reflect a modest uptick in jobless claims and the recent decline in vacancies. The data would still be consistent with the Fed’s labor market “rebalancing” definition.

We project the unemployment rate to remain unchanged at 4.0% following two consecutive increases as the spike in young adult unemployment subsides. Hitting the Sahm rule would require the jobless rate to rise to 4.2%.

A more modest increase in hourly wages (0.3% versus 0.4% prior) would push the y/y rate down to 3.9%, the lowest reading since the pandemic. Growth of around 3.0% is more consistent with the Fed’s 2% inflation target.

Polls immediately after the US presidential debate declared former President Trump the winner. While incumbents often “lose” debates, US President Biden reportedly lost by a large margin. This invites increased investor scrutiny of Trump’s policies, especially around trade. The economic consequences of tariffs are relatively obvious, but there is uncertainty about how many campaign pledges will translate into policy action.

The cold economic realities offer US May consumer spending and income data, and the price deflator. While price data is the focus, consumer spending figures follow negative revisions within first quarter GDP. The monthly change in the consumer spending deflator should be benign, and the main concern about US inflation amongst economists is why Federal Reserve Chair Powell has seemingly not noticed rising real interest rates…

Summary Durable goods orders rose again in May, but the data are still consistent with a sector struggling to find its footing. Our read on the monthly volatility is that the industrial space is stabilizing and remains some time off from a true recovery.

The economy has experienced neither a hard landing nor a soft landing since the Fed started tightening monetary policy in March 2022. It has experienced a few rolling recessions in industries like housing and retailing, which spurred soft patches in overall economic growth. The economy may be going through another soft patch, as evidenced by the Citigroup Economic Surprise Index, which has been modestly negative since May 3 (chart).

After today's soft batch of economic indicators, the Atlanta Fed’s GDPNow tracking model revised Q2’s real GDP estimate down from 3.0% (saar) to 2.7%. That's still relatively strong. Neither the bond nor stock market reacted much to today's numbers.

Let’s have a look at today’s indicators, which might have brought some (fleeting) joy to the diehard hard-landers:

(1) Unemployment claims. Weekly jobless claims fell 6,000 to 233,000 (sa) in the week ended June 22, remaining at historically low levels (chart). A bit of labor market weakness could be gleaned from continuing claims, which rose 18,000 to 1.839 million—the highest since November 2021—in the week ended June 15.

However, as Reuters noted today, the jump in continuing claims was driven by a rule change last year in Minnesota that allows non-teaching educational staff to file for unemployment during the summer months. Minnesota was the largest contributor to continuing claims for the week, rising by 8,834 (nsa).

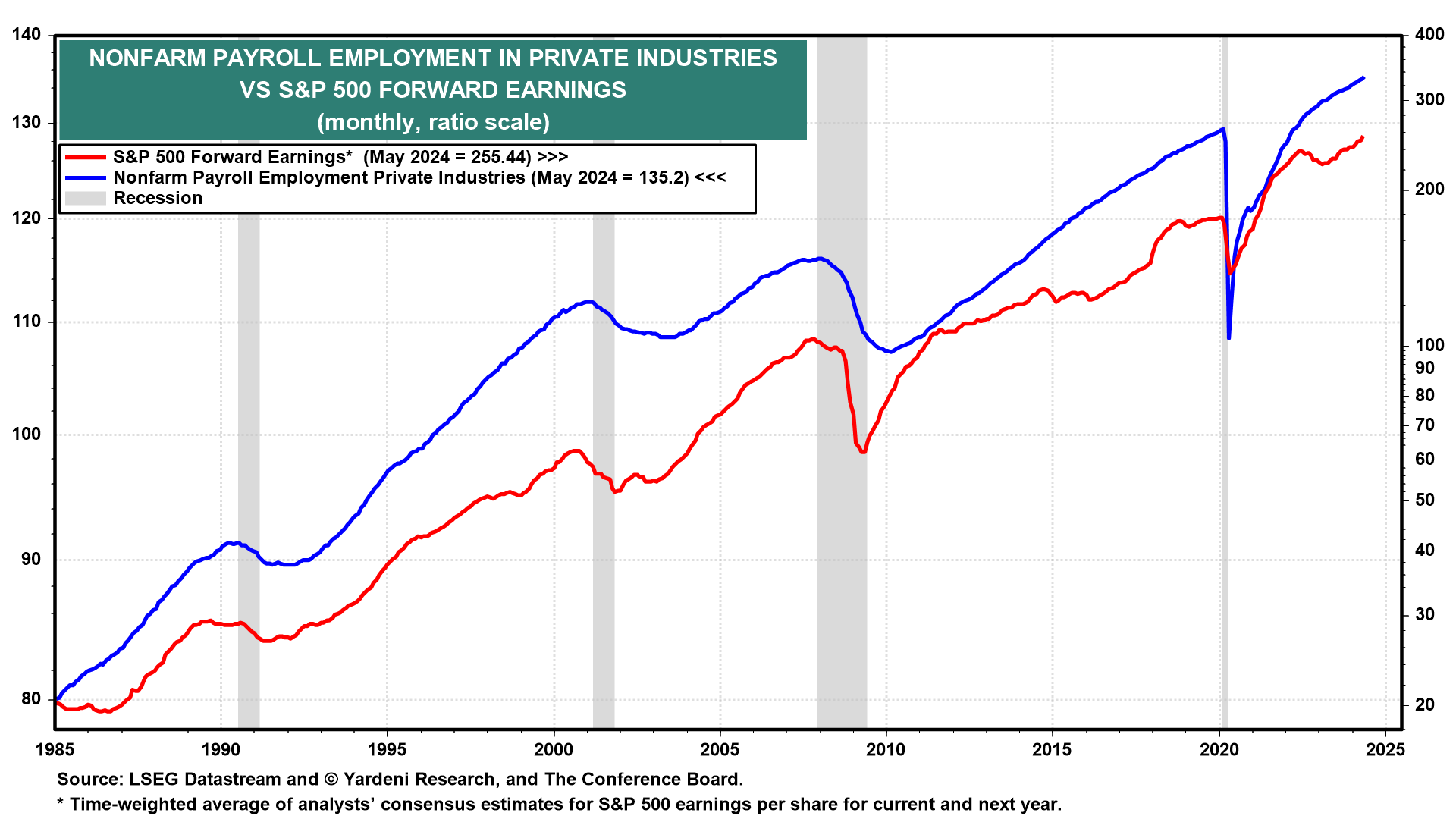

Everyone seems to be on the lookout for signs of weakness in the labor market, including several Fed officials. One important reason why we aren’t concerned is that private payroll employment is driven by profits, and S&P 500 forward earnings continues to rise to record highs (chart). Profitable companies tend to expand their payrolls!

… And from Global Wall Street inbox TO the WWW,

Atlanta FED: Are Real Wages Catching Up? (i kept hitting ENLARGE buttons in the article hoping it would ENLARGE my paycheck … has not worked yet … keep you posted)

… In sum, the data have unfolded in a way consistent with the notion that the big shift to remote work provided a substantial offset to the real wage growth catch-up that many economists were anticipating in the wake of the 2021–22 inflation surge. Moreover, firms continue to see nominal wage pressures slowing over the year ahead. Our results suggest that it will still be some time before real wages return to their pre-inflation surge level (first quarter of 2021), let alone catching back up to the trend they were on prior to the surge. Indeed, we may have seen a permanent downshifting.

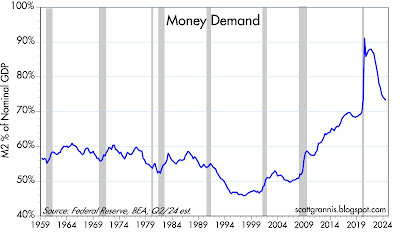

Chart #3 is another way to measure the demand for money, by dividing M2 by nominal GDP. This is a proxy for the amount of liquidity people are comfortable holding as expressed by a percentage of their annual income. Here too we see things are returning to what might be considered "normal," or pre-Covid levels.

To sum up, the monetary situation has for the most part returned to normal. This lends strong support to the belief that the Fed has essentially managed to once again tame inflation. Interest rates are quite likely to decline going forward, and the only question is one of timing. Meanwhile, the Fed has lots of "dry powder" to unleash (in the form of lower interest rates) should the economy stumble.

The biggest obstacle the economy faces now is fiscal policy, which will depend to a great deal on the outcome of the November elections. Much as I detest Trump's personality and his affinity for tariffs, I strongly believe his policies (e.g., lower tax rates, reduced regulation, smaller government) would result in a stronger economy than if Biden were granted another term in office.

… I’ll leave this one here … “Winner gets the Oval…”

Didn't watch the 'Debate'. There're so many ways to go, your parting pic provides me better focus. Of all the 'Debate' highlights (Trump's anyways) for me was Trump nearly toppling over at Brandon's claim his golf handicap was a 6 as VP :)))

Didn't watch the 'Debate'. There're so many ways to go, your parting pic provides me better focus. Of all the 'Debate' highlights (Trump's anyways) for me was Trump nearly toppling over at Brandon's claim his golf handicap was a 6 as VP :)))