Good morning and now we know … we just yesterday witnessed the moment in time whereby the narrative shifted (again) from when not IF TO IF, not when.

WSJ Timiraos: Fed Rate Cuts Are Now a Matter of If, Not Just When Central bank officials started the year with the wind seemingly at their backs. No more. ByNick Timiraos April 10, 2024 9:00 pm ET

And for that “Uh Oh…” moment viewed by 2yy reflexing TO CPI, feel free to continue scrolling all the way to the end for that sort of widely disseminated visual.

For now, I’m going to start with a comment on the move yesterday …

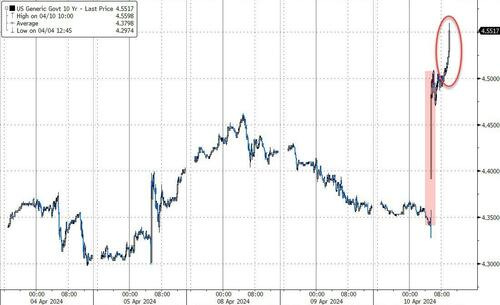

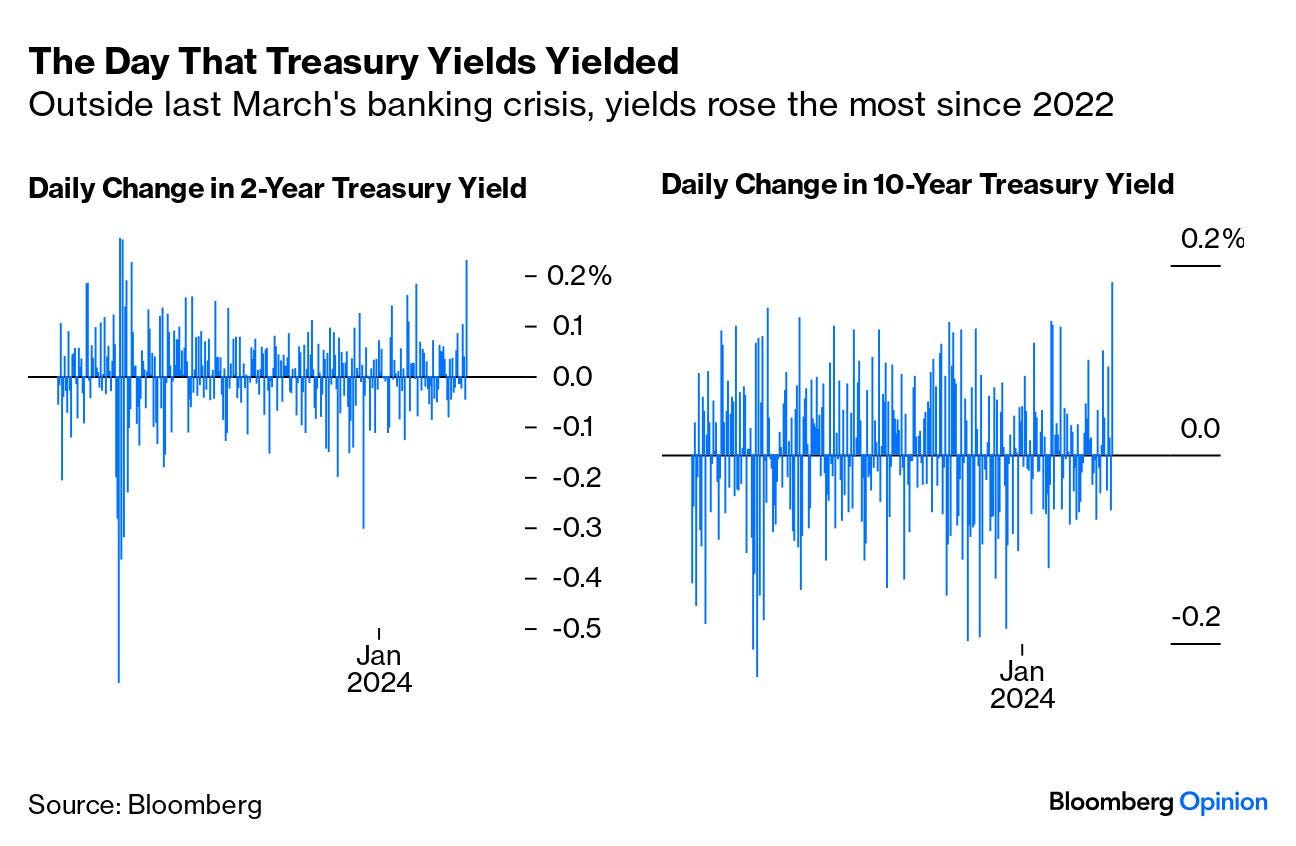

Markets saw an aggressive selloff yesterday, as another upside surprise in US inflation meant bonds and equities both slumped. That included the biggest daily rise in the 10yr Treasury yield (+18.2bps) since September 2022, while futures priced out a full 25bp rate cut from the Fed by year-end. The main takeaway from the report was a +0.4% monthly print for core CPI in March, contrary to expectations for a slowdown to +0.3%. But the bigger picture is that this is now the third consecutive month that core CPI has been at +0.4%. So it’s getting increasingly difficult to dismiss this as just a temporary bump, and the major concern is that inflation is ending up sticky above the Fed’s target. Indeed, there are increasing echoes of late 2021, when it became apparent that the initial spike in inflation was proving persistent, which in turn laid the groundwork for much more hawkish policy from the Fed. That’s been clear today as well, with investors pushing out the likely timing of rate cuts until later in the year, and pricing in a more hawkish policy stance ahead… -DBs Early Morning Reid (11 April 2024)

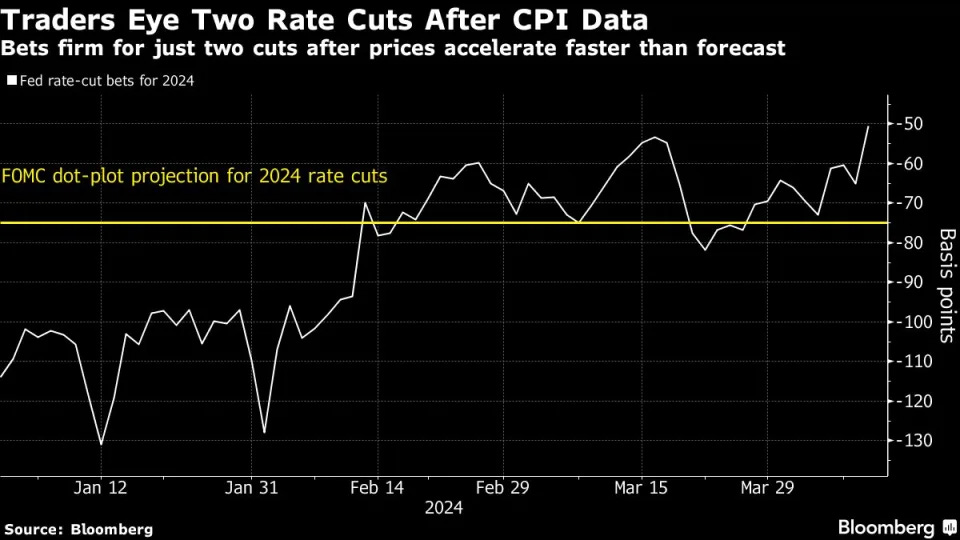

… I’m ALSO told this move brought with it a decent decline in rate CUT ODDS in June (from 60% chance to about 21%) and JULY chances fell to approx 50% (from a near certainty the day before) …

Team Rate CUT had a(nother) rough go of it and I’ll not fester but rather, keep moving along and head straight TO a look at bonds. Long bonds. Ahead of today’sfinal installment of reFUNding — 30yr auction …

30yy: momentum has now become overSOLD, not a sign of a BULLISH turn, cross, but reaching top of ‘channel’ — make of it what YOU will …

… a concession, YES but enough of one? remains to be seen … watching channel extremes up nearer 4.70 for support at the moment …

… Now, a few curated links which I’m leaning on to catch up on the day that just was on heels of an absolutely breathtaking move in rates …

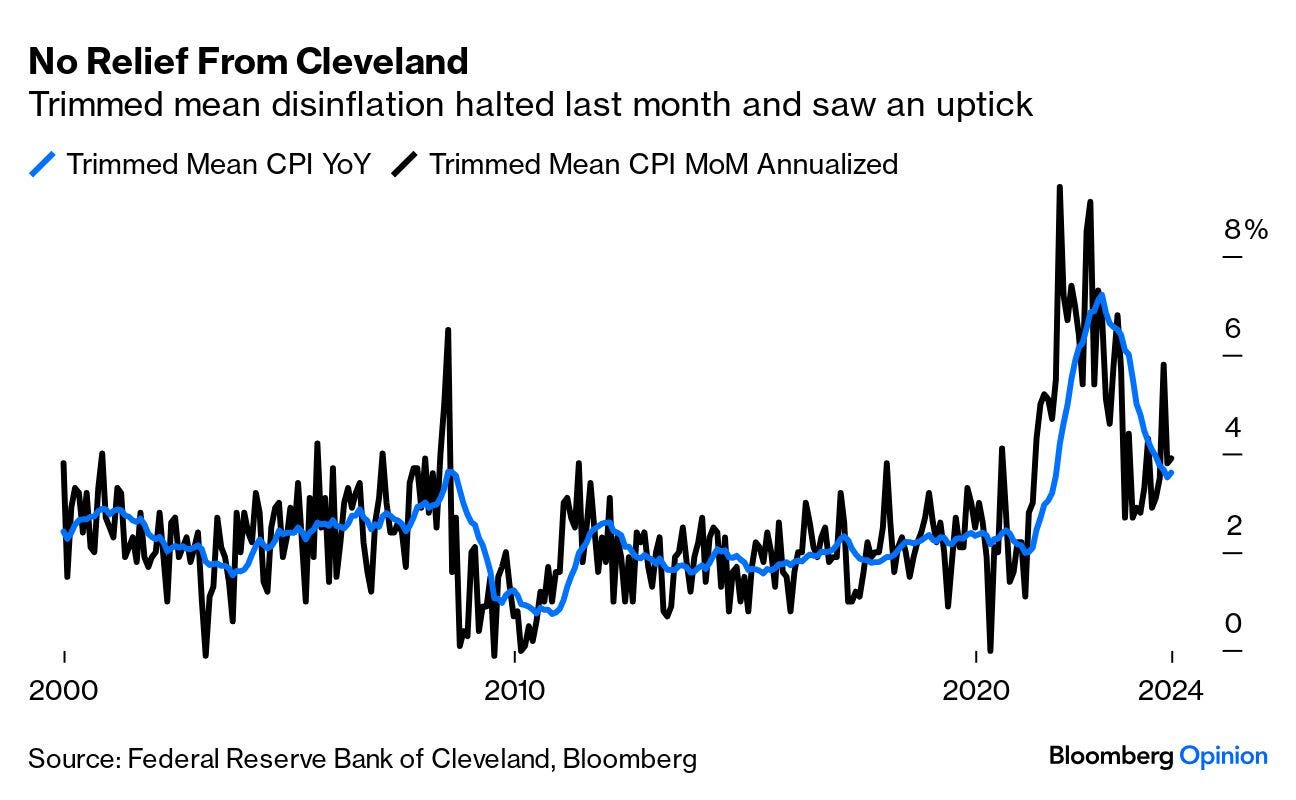

CalculatedRISK: BLS: CPI Increased 0.4% in March; Core CPI increased 0.4% CalculatedRISK: YoY Measures of Inflation: Services, Goods and Shelter CalculatedRISK: ClevelandFed: Median CPI increased 0.4% and Trimmed-mean CPI increased 0.3% in March

ZH: Consumer Prices Print Hotter Than Expected, Led By Surge In Energy & Shelter Costs ZH: Surveying The Post-CPI Market Carnage... ZH: "Obviously, This Is Very Bad News For Biden": Wall Street Reacts To Today's Red Hot Inflation Print

… and all this helped / hurt (please choose one depending on your view and the view of your risk managers and / or PnL) the auction process …

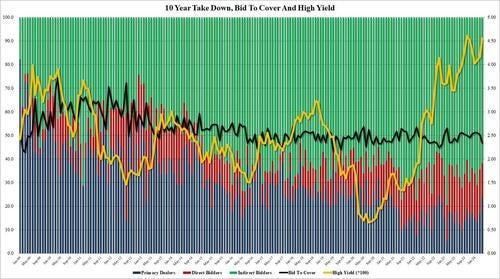

ZH: Yields Soar After Catastrophic 10Y Auction Shocks With 3rd Biggest Tail On Record

… The internals were even uglier, with foreign buyers tumbling from an already low 64.3% to 61.8% the lowest since Oct 23 and far below the six-auction average of 65.9; and with Directs also sliding to just 14.2%, the lowest since Nov 21, Dealers ended up stepping up bigly and taking down a whopping 24.0%, the highest since November 22.

The market reaction was instantaneous and brutal with 10Y yields, already trading at session and 2024 highs, spiking by 6 bps to another day high of 4.56%, and fast approaching a level where not only stocks will tumble but the entire economy collapses as it grinds to a halt, similar to where Biden's approval rating will be in the very near future.

… and with that, we’ll look ahead to this afternoons 30yr auction … so much for that ‘bullish momentum’ noted HERE yesterday on 10yy …

#GotBONDS? Whatever … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mixed with the curve pivoting steeper around an unchanged intermediate sector. DXY is little changed while front WTI futures are lower (-0.65%). Asian stocks were mixed despite NY's weakness, EU and UK share markets have followed lower (SX5E -0.5%) while Es futures are showing -0.25% here at 6:45am. Our overnight US rates flows saw one of the most volatile Asian sessions for Treasuries of this year (a big tail in a 20y JGB auction adding to the ride there). Buyers in the front end led the way early before sellers emerged in intermediates. During London hours, the price action was more subdued and constructive as real$ dip-buyers were seen in the belly. Flows in the back-end were notably light ahead of today's bond auction. Overnight Treasury volume was ~135% of average, led by 5's (167%) and 10's (154%).

… Treasury 2yrs, daily: 2yr yields spiked directly to their next support level at 4.98% derived by their late November high. The selloff has stalled there in recent hours so that's your support-of-interest heading into PPI. Above there, the next solid support appears to be around 5.20% and just above it, October's move highs. In the lower panel, daily momentum is now oversold but not yet indicative of an improving balance of flows that one typically sees at a trend turning point. The chart of Treasury 5yrs looks predictably similar but yields are already above their equivalent support (to 4.98% in 2yrs) after the belly led yesterday's sell-off. The key levels for 5yrs that we're eyeing are shown in the grid below.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities lower, USD/JPY on a 153 handle & Bunds dip ahead of the ECB; US IJC/PPI due … USTs contained at post-CPI lows whilst Bunds dip lower ahead of the ECB

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ and just how they are ‘splainin’ that there JUNE TO SOON CPI report (and yes there are a couple updated FED CALLS, I know yer shocked, too) …

BARCAP March CPI: One too many bumps for the FOMC (updated call to follow …)

Core CPI surprised to the upside, holding steady at 0.36% m/m (3.8% y/y), driven by an acceleration in core services. 3m and 6m saar core CPI have accelerated from December, as have "supercore" measures, making it increasingly difficult for the FOMC to characterize this report as another "bump" on the road, in our view.

… All told, we think the March inflation data highlight the risks of fewer rate cuts this year. Core inflation has not materially eased this year, and even smoothing through the monthly data, we find that the 3m and 6m annualized rates for both core CPI and the supercore measures have accelerated since Q4 2023. All told, we think it is becoming increasingly difficult to characterize the run-up in inflation this year as "bumps" on the road to disinflation. While we think there is some scope for a payback on the core services side next month from categories like medical care and transportation services, where the increases appear outsized, we think it is likely to be limited.

With March's CPI inflation surprising to the upside amid continued tightness in the labor market and a resilient economy, we now expect the FOMC to cut rates just once this year, by 25bp. We thus expect the fed funds target range to be 5.00-5.25% at end-2024 and 4.00-4.25% by end-2025.

BARCAP China: A big miss in CPI, PPI deflation to stay

We think the beyond seasonal drop in CPI inflation and worsening PPI deflation suggest: 1) the risks of entrenched deflation expectations remain; and 2) a sustained rebound in growth momentum is still in doubt. With a deteriorating labour market and household debt overhang, we expect CPI to remain muted at 0.3% in 2024.

March: 0.1% y/y for CPI, and -2.8% y/y for PPI

Bloomberg consensus forecast (Barclays): 0.4% (0.3%) y/y for CPI, and -2.8% (-2.7%) y/yfor PPI

February: 0.7% y/y for CPI, and -2.7% y/y for PPI

BMO: Core-CPI at +0.4% takes June cut off the table

… This is problematic for the Fed as it hints of stickiness and will roll forward rate cut expectations into Q3. It has now become very difficult to envision 75 bp of rate cuts this year and we're now looking for the biggest move at the June meeting to come in the form of a higher 2024 dot (as well as 2025-2026) … Within the details, we see OER was 0.438% and Rent was 0.406%. Airfares were -0.375% and hotels +0.045%. Overall, the figures materially undermine the Fed's assumption that Jan/Feb were simply a bump in the road toward normalization…

The details of the March CPI report provided little respite for the Fed, with stronger non-shelter services inflation factoring into the concerning third straight upside surprise for the core.

We continue to think inflation moderates this year, but more resilient non-shelter services is likely to make this moderation more gradual. We lift our 2024 core CPI and core PCE forecasts by 0.1pp to 3.4% and 2.8% q4/q4, respectively.

In our view, the March CPI print makes a June rate cut untenable, while our forecast for a more gradual decline in inflation makes two cuts this year more likely than three. We revise our Fed call to two cuts this year, in July and December (from three cuts in June, September, and December previously).

Preliminary April CPI forecast: 0.3% m/m headline, 0.3% core.

Bloomberg BNP US March FOMC minutes: Still looking for confidence

KEY MESSAGES

The March FOMC minutes reinforce that Fed officials have been acutely focused – and uneasy – about near-term developments on the inflation front, even as they generally expect bumpy disinflation to continue.

The recently released March CPI data pose a clear challenge to both the three-dot median estimate and own pre-release view for three cuts. In the wake of that report, we changed our call to just two cuts this year, starting in July.

While “almost all participants judged that it would be appropriate to move policy to a less restrictive stance at some point this year,” the Fed lacked sufficient “confidence” to initiate rate cuts given the recent data backdrop.

The minutes confirmed the Fed’s readiness to start the process of tapering QT “fairly soon”, which we see as aligned with our QT taper call for a May announcement with implementation in June.

CitiFX: Techs - More to come in US yields, stocks and dollar (uh oh…)

US 10y yields: 10y yields are testing strong resistance at the 4.51%-4.54% (Nov 27 high, 61.% Fibonacci retracement) level. However, these levels look likely to give way, and IF we see a weekly close above, we think we will see another 15bps move higher towards the 4.70%-4.73% (November 13 high, 76.4% Fibo retracement) levels

We remind we had held a view of higher yields earlier as well, especially with the weekly trend clearly being upwards, while weekly momentum (slow stochastics) is showing no signs of crossing over. This leaves little in the way of contra-indicators suggesting a move lower could be on the cards.

DBDaily: US CPI beats on headline & core (NOTE — chARTwork here where the big thick lines look to be DOWN so DE / DISINFLATION and the axis labels quite large BUT far away from where the lines are … likely on purpose because if you study closer you’d notice blue line - CORE - disinflation trend is STALLING and both are well ABOVE 2% … but again, if you frame it this way, we are NOT supposed to realize how bad things really are ?? is it working??)

… Chart of the day US CPI beat in March: headline trending sideways for ~9mths

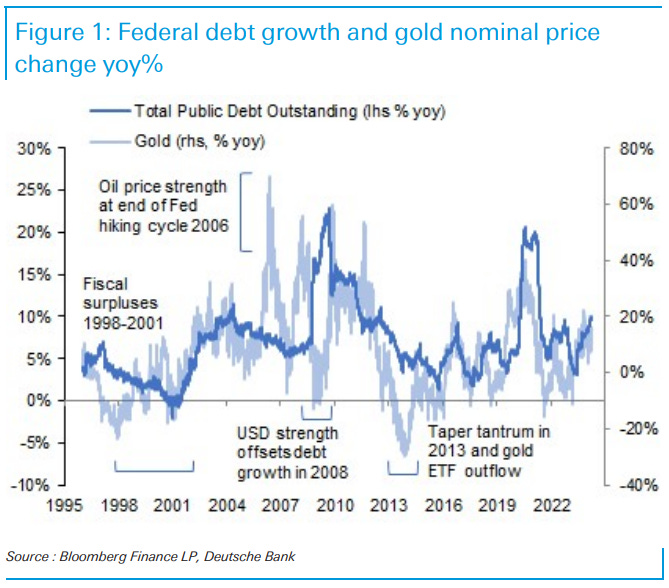

DB: Federal debt and gold fair value (NOT a gold bug BUT visual caught MY attention, make of it whatever you wish … good note, though, thought provoking)

Financial modeling and visible investment flows have both failed to account for gold's strength since March, but we argue this should not cause us to abandon financial modeling entirely.

In seeking to enrich our understanding of gold's financial drivers, we propose a variation of the valuation model where US federal government debt stands in as an explanation for the long-term magnitude of gold's appreciation. We think this version of the model provides a fuller understanding of gold's drivers.

Its relevance for today is that it helps to quantify the scope for a correction for gold that investors may reasonably expect, which we think is probably limited to around USD 2,200/oz.

We also note the indication of China investor demand seen in the rebound of the China gold premium to USD 51/oz today, and a 5d average of USD 38/oz. This could also function to limit a gold correction, though conditional on CNY downside pressure abating.

Finally it is one more point of triangulation for the size of investor inflows this year, with a 400-450 tonne flow sufficient to explain the move. This equates to 13-14 mm troy oz, in the ballpark of the 10 mm troy oz estimate we described earlier by observing weekly ETF investments.

Goldilocks: Auto Services Drive Third Straight Core CPI Beat (updated call)

BOTTOM LINE: March core CPI rose 0.36%, 6bp above consensus expectations and matching its February pace. The year-on-year rate was unchanged at 3.8% against expectations for a decline. The composition of the report was not as strong, as primary rent inflation slowed somewhat and the jump in car insurance CPI will not flow into the PCE measure. However, the strength in car repair and apparel prices will boost PCE prices, and we now tentatively expect core PCE prices rose 0.29% in March (mom sa). We will update our estimate after tomorrow’s PPI data. We are pushing back our forecast of the first rate cut from June to July. We continue to expect cuts at a quarterly pace after that, which now implies two cuts in 2024 in July and November.

Goldilocks: FOMC Minutes Suggest Tapering Will Start “Fairly Soon,” Note Strength in Recent Inflation Data

BOTTOM LINE: The minutes to the FOMC’s March meeting noted that “participants generally favored reducing the monthly pace of runoff by roughly half from the recent overall pace,” and that the Committee preferred to “adjust the redemption cap on U.S. Treasury securities to slow the pace of balance sheet runoff.” We have been assuming that the FOMC will reduce the cap on Treasury runoff from $60bn per month to $30bn per month, but we now see a risk that the minutes might imply reducing the Treasury cap a bit further in order to slow the realized pace of overall runoff by half. The minutes also noted that “almost all” participants judged it would be “appropriate to move policy to a less restrictive stance at some point this year.” While participants noted that “the recent data had not increased their confidence” that inflation was moving toward the Fed’s 2% target, they also “anticipated that there would be some unevenness in monthly inflation readings as inflation returned to target.”

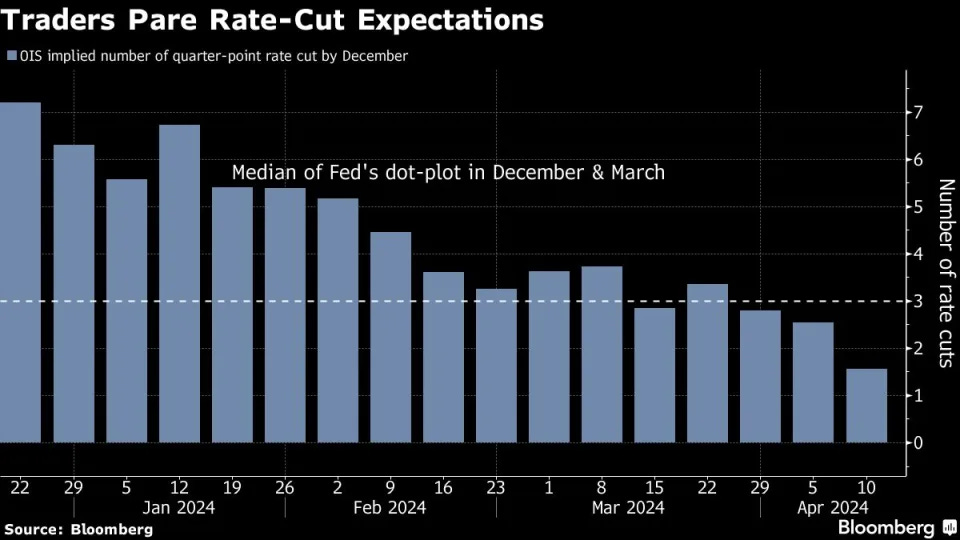

… Market views … Given the strength of services, markets have continued to price a later start and shallower path of Fed easing: OIS forwards are not pricing a full 25bp ease until after the September FOMC meeting, and just 40bp of easing in 2024 (Figure 1).

…Overall, the broad bulk of data flow has been positive in the last 3 months, pointing to stronger growth: as we discussed last week, we have revised up our 4-quarter ahead growth forecasts by about 1%-pt YTD (see Treasuries, US Fixed Income Markets Weekly, 4/5/24). Indeed, data has broadly outperformed expectations over the last 3 months, and our US EASI is now back at its highest levels since last fall (Figure 2).

Overall, we do not want to overreact to this data, and we continue to project the first cut in July and 3 cuts in 2024 … However, we are reticent to add duration at current levels, because it will take multiple softer inflation and labor market prints for market participants to feel confident the Fed can begin to normalize monetary policy. Moreover, absent a catalyst, we think it’s challening to recommend duration longs in a world in which the curve remains inverted and carry in these positions remain negative. As a result, we wonder if more mediumterm dynamics may prevent a quick mean reversion in our valuation framework.

Incorporating inputs from CPI, we preliminarily forecast core PCE inflation increased 0.31%M in March vs. 0.26%M in February. This would lower the y/y from 2.78% to 2.76%. Headline PCE is preliminarily forecasted at 0.32%M vs. 0.33%M in Feb-24. Core services ex housing translation points to 0.36%M in Mar-24 vs. 0.18% prior. We will update our PCE forecast after the PPI release tomorrow, in particular watching airfares, healthcare and financial services components.

The upside surprise in core CPI is moving the inflation data further away from the convincing evidence the Fed needs to start cutting in June. While shelter showed some progress, core service ex housing re-accelerated. Dependent on the PPI data tomorrow, this print tilts the Fed toward a later start to the cutting cycle than our current forecast for June…

NatWEST: US Consumer Price Index (updated call follows…)

The March core CPI report disappointed, with the core CPI rising by another 0.4% (consensus +0.3%, NatWest +0.2%). The unrounded increase in the core was 0.359%in March—virtually matching the 0.358% gain in February. On a three-month annualized basis, the core CPI picked up from 4.2% in February to 4.5% in March, while the six-month annualized rate stayed at 3.9%. On a year/year basis, the core CPI held steady at 3.8%. The headline CPI also increased by 0.4% (consensus and Natwest +0.3%) in March, as food prices ticked up by 0.1% and energy costs increased 1.1%. The year/year headline CPI rate rose from 3.2% to 3.5%…

… In light of the stronger-than-expected inflation data to start 2024, our call for the timing of a June rate cut, along with the magnitude we have been assuming in total rate cuts this year now looks too aggressive.

NatWEST US: Update to Fed Call (updated call, but then, you knew that by the title…)

… f anything, throughout this cycle officials have erred heavily on the side of caution because the “transitory” fiasco has made officials determined not to be caught on the wrong side of the inflation story for the second time in the same cycle. Consequently, we now expect the first cut (25bps) to occur at the September 17-18 FOMC meeting (instead of June 11-12) followed by two additional cuts this year (November and December) and six additional 25bps cuts next year—reaching 3.0% by the end of Q3 2025 (instead of our earlier expectation for the end of Q1 2025).

RBC: U.S. inflation inched higher with strong details

… Bottom line: The Fed has reiterated that the recent upticks in inflation readings do not reshape the overall view on expected price growth going forward. But the string of upside surprises is getting longer, calling into question just how much inflation can sustainably slow without the economy softening more than it has. There are still reasons to expect inflation will drift lower going forward - lower hiring demand is slowing wage growth even with unemployment still very low. Consumer inflation expectations have ticked lower and we do expect unemployment to edge higher this year. But the breadth of the upside surprise in March CPI will worry Federal Reserve policymakers who were already starting to waffle on the amount of cuts that might be warranted this year.

UBS: Strong data likely to delay rate cuts (updated call)

We are removing the June rate cut from our base case for the Fed.

We now look for the first cut in September with 50 basis points of cuts by year-end.

In our view, it is unlikely that high inflation will force the Fed to hike rates further.

UBS (Donovan): Inflation comes unstuck (never uncertain about himself…)

Inevitably markets reacted to US consumer price inflation headlines, but the details did matter. There is very strong evidence against inflation stickiness. Aside from rents and fictitious owners’ equivalent rents, there is deflation in almost every consumer price subcategory somewhere in the US. With collapsing clothing prices in Tampa or plunging communication prices in Chicago, it is difficult to argue that structural inflation stickiness exists when every key sector has deflation somewhere in the country.

Food prices were falling in a third of US cities surveyed, as profit-led inflation retreats. Durable goods deflation is also significant, but high frequency purchases shape consumer (or voter) perceptions. Gasoline prices fell in some areas, but were generally higher—also a high frequency purchase, but gasoline inflation can reverse more quickly than food price inflation…

… That said, today's inflation data are likely to keep the FOMC's doves on the defensive while providing more ammunition to the Committee's hawks, who are increasingly of the view that there is no rush to start cutting the fed funds rate. Even if the inflation data cool gradually in the months ahead as we expect, a solid labor market and tranquil financial conditions afford the FOMC more time to await additional data that confirms inflation is on a downward-albeit-bumpy path back to 2%. We now project two 25 bps rate cuts in Q3 and Q4 of this year as our base case for the fed funds rate. We will publish our monthly economic forecast update tomorrow morning that will more fully flesh out our views and projections for economic growth, inflation and interest rates.

Yardeni: The Last Mile (seems like an updated NO CUTS AT ALL this year call…)

Will the Fed start raising the federal funds rate again? We expect to be hearing this question more often following today's hotter-than-expected CPI inflation report. The previous two reports for January and February were also hotter-than-expected. We don't think that the Fed will raise rates again this year, but we've pushed back against the widely-held notion of several cuts this year and argued that no cuts at all was increasingly likely. Now that's our base case scenario. So is a 4.75%-5.00% yield on the 10-year Treasury bond in the next few months. We've been expecting the stock market rally to pause and suggested taking some profits, but we still expect the S&P 500 to end the year around 5400.

We also still believe that inflation hasn't stalled, and will continue to moderate to 2.0%-2.5% by the end of this year. The so-called "last mile" may not be as hard to travel as suggested by today's CPI report. Consider the following CPI developments..

… And from Global Wall Street inbox TO the WWW, where ‘pundits’ here too are obsessed with CPI in one way or ‘nother …

Bloomberg: Bond Traders Shift Thinking to a 5% Yield, No Rate Cut World

Schroders is shorting 2, 5, 10-year Treasuries on higher rates

Ten-year yield has topped 4.5% for first time since November

Bloomberg: Traders See Fed Waiting Until After Summer to Cut as Yields Soar

Swaps pricing of rate cut moves to November from September

Hot inflation data lofts 10-year yield to 2024 high 4.5%

Bloomberg(via ZH pre CPI): Renewed Inflation Risks Aren't Scaring Buyers Yet (did this age well?? asking for a friend :) )

Bloomberg: When even the Fed's favorite inflation metric stops falling (Authers’ OpED)

The scramble to adjust to a reality where the US can’t cut and other central banks are under pressure to is on.

… The numbers don’t get better on closer examination. Using the trimmed mean (in which outliers in both directions are excluded and an average taken of the rest) shows inflation picking up a little, and not continuing what had appeared a clear trend of disinflation:

Research teams at the Fed also care about “sticky” prices, which take a while to move and very rarely go down. Here again, the index kept by the Atlanta Fed shows disinflation halting and beginning to reverse — at a level above 4% and far too high for the Fed’s comfort:

If there is an extenuating factor, it concerns motorists…

… As a result, yields on two-year Treasuries rose by more than 20 basis points, their biggest increase since the confusion of the regional banking crisis in March 2023. The 10-year yield jolted higher by the most since the UK gilts crisis of September 2022. So a not-that-surprising data release was treated with the same gravity as those incidents, both of which briefly appeared to threaten a systemic financial crisis:

Despite this, financial conditions more broadly remain quite easy, a consequence of the Fed’s pivot toward promising rate cuts at the end of last year.

FirstTRUST: The Consumer Price Index (CPI) Rose 0.4% in March

Implications: … After large monthly increases in January and February, that measure jumped another 0.6% in March, driven by higher prices for motor vehicle insurance (+2.6%) and medical care services (+0.6%). In the last twelve months, this measure is up 4.8% and has been accelerating as of late; up at 8.2% and 6.1% annualized rates in the last three and six months, respectively. And while inflation remains stubbornly high, workers are no longer being compensated for it. Case in point, real average hourly earnings were unchanged in March. These earnings are up only 0.6% in the last year, a headwind for future growth in consumer spending. Putting this all together, the Fed has little reason at this point to start cutting rates. How they respond to the incoming economic data in the months ahead could determine whether we repeat the inflationary 1970s.

ING: US inflation quashes the chances of a June Fed rate cut

US inflation came in at 0.4% MoM for the third consecutive month, more than double the rate we need to consistently hit to bring inflation down to 2% YoY. Expectations for a June Federal Reserve interest rate cut have collapsed with the higher for longer narrative on rates firmly in place. September is going to be the earliest opportunity for any policy easing …

Core CPI MoM%, 3M annualised and YoY% changes

at WalterDeemer (8:14 PM · Apr 10, 2024… think this tweet VERY technical, from one of the better in the biz over the years … HOPE you can comprehend)\

Uh oh…

WolfST: Beneath the Skin of CPI Inflation, March: Inflation Behaves Very Badly, Saga Far from Over

Ugly inflation in services drives up 3-month “core CPI” for 7th month, to 4.5% annualized, worst in a year, and 3-month overall CPI to worst since Nov 2022.

WolfST: Treasury Yields Spike, 3-Year by 25 Basis Points. Mortgage Rates Hit 7.34%. Services Inflation Smacks Down Rate-Cut Mania

A Bloodbath was had by all?

… Today’s 19-basis-point jump for the 10-year yield was the biggest since September 22, 2022 (also 19 basis points), and both had been the biggest since June 2022:

A bloodbath was had by all, but it was worse in the midrange, with the two-year yield jumping 23 basis points to nearly 5% and with the 3-year yield jumping 25 basis points to 4.77%.

6-month yield: +6 basis points to 5.40%

1-year yield: +16 basis points to 5.19%

2-year yield: +23 basis points to 4.97%

3-year yield: +25 basis points to 4.77%

5-year yield: +24 basis points to 4.61%

7-year yield: +21 basis points to 4.59%

At the auction yesterday, $57 billion of 3-year Treasury notes were sold at a yield of 4.55%.

In the secondary market today, the 3-year yield’s jump of 25 basis points was the biggest since June 2022. Today’s yield of 4.77% is just 26 basis points below the high in this cycle on October 18, 2023, of 5.03%, though inflation-denial is still driving this market, as we can see in this chart:

ZH: Oil Soars On Report US Sees Imminent "High-Precision Missile" Strike On Israel By Iran (seriously? today? on heels of CPI?)

ZH: Biden (Yes, Biden) Promises Rate-Cut By Year-End As Fed Minutes Signal Caution But QT Taper 'Fairly Soon' (and … ‘bout them FOMC mins…)

Listen to Powell's boss, President Biden, for cut timing ;)

Ouch !!!!

Great summary........