Another day, another dollar and another moment outta pocket … I’ll rip through a few things I missed and then have healthy linkfest below but apparently overnight, the Nikkei reported that the BOJ will discuss whether to end negative rate policy and scrap YCC next week.

Markets are continuing to internalize this and so far, without incident … Meanwhile, in other news, I find the price action NOT all that shocking as we digest CPI and supply (couple links in a sec) ahead of this mornings ReSale TALES …

The price action which I’m referring to specifically was mentioned HERE Tuesday and one of the first things I noticed this mornings was 10yy trading @ 4.20 … aka 200dMA. Now what? I’ve since etched in a TLINE drawn off 5.20 cheaps back in October and today said ‘support’ comes in a touch above 4.20

10yy: 200dMA (4.198), TLINE supp (4.21) and THEN another (red)TLINE (4.30)

AND now … a couple things of what I deem important since I was outta pocket yesterday, which I have been reading

ZH on CPI: Inflation Hot: Consumer Prices Hit New Record High, Up 19% Since 'Bidenomics' Began ZH on 10y: Ugly, Tailing 10Y Auction Sees Lowest Foreign Demand Of 2024 ZH on 30y: Stellar 30Y Auction Sees Biggest Stop Through Since Jan 2023

AND with all THAT said and in mind, the rest is UNLIKELY (see BBG and other links below of the Hobbits recent commentary about where rates are headed) this will be quick and SO, jumpin’ in … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mixed with the Tsy curve twisting steeper around an UNCHD 7-year point this morning. News was scant this morning (links above), DXY is little changed while front WTI futures are +1% higher. Asian stocks were mixed, EU and UK share markets are mixed-higher while ES futures are showing +0.35% here at 6:30am. Our overnight US rates flows saw real$ selling in the long-end during Asian hours after a 2.6bp tail in a JGB 20-year auction acted as a drag on prices.After the London crossover, flows were quite subdued with some action/selling at the US point by fast$ about all that was flagged by our desk. Overnight Treasury volume was about average across the curve except for the 2-year (saw 200% of ave volume).

… Our first two attachments check back in with Treasury 30yr yields after they held channel resistance last week, ultimately rejecting it. If you look in the lower panels of each chart, you will see momentum aiming toward higher yields. The idea here is that the bear channel in place since late last year is dominating the price action still. Moreover, the price action and set-up in Treasury 10's is exactly the same as it is for 30yrs at the moment. So there's that …

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities firmer & Dollar flat ahead of Tier 1 US data and ECB speak, Crude at session highs … Bonds hold a bearish tilt, continuing price action seen in the prior few days; Bunds caught a slight bid following dovish remarks from ECB’s Stournaras

Reuters Morning Bid: Oil smudges inflation view, Tesla in slow lane (NOTE VISUAL of, “US mid-year interest rate cut PROBABILITIES. Traders have slightly LOWERED their bets after February’s CPI cata”

…The bond market seemed to reflect bets for a higher-for-longer U.S. rates scenario, with the two-year Treasury yield notching a two-week high on Thursday. The dollar, however, was still largely on the back foot.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … a combination of CPI recaps and victory laps and other, assorted notes for those of privilege with credentials …

BARCAP: February CPI: Unlikely to instill much confidence

Core CPI decelerated on the margin, but continued to round up to 0.4% m/m in February, and was up 3.8% y/y, amid an upside surprise from the core goods category, which posted its first increase since last May. Although core services inflation moderated, price pressures remain elevated after smoothing through monthly data.

… All told, we think the February inflation data highlight the risks of fewer rate cuts this year. In our view, the run-up in core goods prices, a category that has played a key role in the disinflation to date, is likely to raise some concerns. In addition, with core PCE estimates also poised to look firm in February, we think the data skew risks that the FOMC will show fewer cuts in next week's dot plot than the three shown by the median participant in December. We retain our call that the FOMC will cut three times this year, with every-other-meeting cuts starting in June, but acknowledge that outcomes remain highly data dependent.

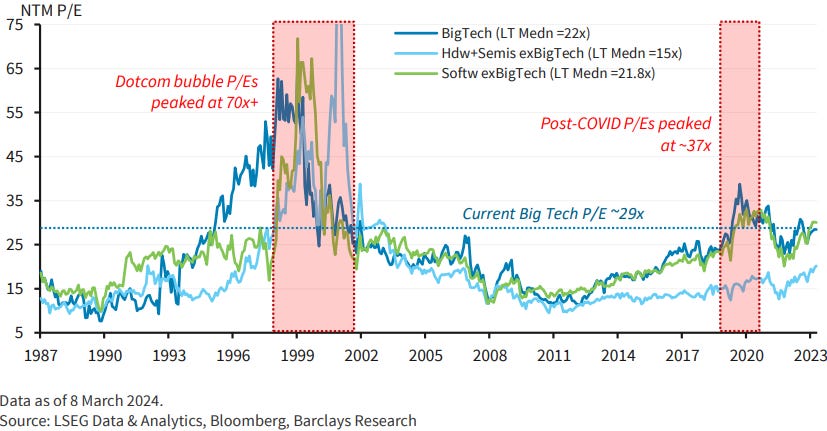

Mega-cap Tech has driven a historically high degree of concentration in US equities, leading many to ask whether the rally is sustainable. A deep dive into our six-stock Big Tech group leads us to believe that, while not without risks, fundamentals remain supportive of Big Tech over the near to medium term.

… Figure 6. Current Tech valuations are well below post-COVID and Dotcom bubble peaks

BloombergBNP US February CPI: Underlying pressures linger, goods inflation stirs

KEY MESSAGES

While core CPI surprised to the upside for the second straight month in February, the details were somewhat more benign than the rounded print may suggest.

Specifically, sequential shelter inflation fell substantially, allaying fears that January’s strong print may be the new normal through H1 2024.

At the same time, non-shelter services inflation remained firm, while the second straight month of non-vehicle goods sector price gains raises the risk that the end of goods deflation comes sooner than we expect.

Overall, we think the print supports our above-consensus expectation for CPI to rise by 3.0% q4/q4 this year.

he February readings for both headline (0.44% vs. +0.30% in January) and core (+0.36% vs. +0.39%) CPI came in slightly stronger than expected. Taken together, the year-over-year rate for headline ticked up a tenth to 3.2%, while that for core fell by the same amount to 3.8%. While the twelve-month inflation rate for core continues to decline, the shorter-term trends have firmed some, with the three- and six-month annualized rates picking up to 4.2% and 3.9% respectively.

At the component level, core goods prices actually rose by a tenth, the first monthly increase since May 2023. Much of this was driven by positive payback in categories that showed particularly large price declines in January, namely used car and trucks and apparel. While this is just one month's data, it is illustrative that continued declines in good prices cannot be counted on to offset stronger services inflation.

Services inflation remained sticky. Owners' equivalent rent decreased as expected, however primary rents jumped a tenth, causing us to pencil in a slower pace of rental disinflation over the rest of the year. Medical services were a downside surprise, while strong transportation services inflation helped to keep core services excluding rents elevated.

In terms of the implications for the Fed, while the core print was only a few basis points higher than expectations, the component level data did little to provide FOMC participants with further confidence that they can begin the process of normalizing policy. Indeed, this data should all but eliminate prospects of a cut before June, absent an unexpected softening in the economy. That being said, there is still plenty of scope for the next few inflation prints to soften and give the Fed a path to cutting that month. Chair Powell's press conference and the updated Summary of Economic Projections next week will show just how wide that path is.

Our initial read on the March core CPI data is that it should come in at +0.25% m/m and 3.7% y/y. We now expect core CPI to end the year two-tenths higher at 2.9% (Q4/Q4). Further out, our forecasts are largely unchanged at 2.5% and 2.4% for 2025 and 2026. We will update our views on PCE in the wake of Thursday's PPI data. Right now, we have penciled in 0.33% for the February core PCE print.

US rates have had a clear bias to decline on FOMC meeting days this cycle, which likely reflects a premium for exposure to a potentially hawkish Fed. For those able to bear the risk, shorting rates in the days leading into the FOMC and going long on meeting Wednesday has offered attractive returns.

US rates have overwhelmingly declined on FOMC meeting days this cycle

Goldilocks: Core CPI Beats Again but OER and Non-Housing Services Both Normalize

BOTTOM LINE: February core CPI rose 0.36%, 6bp above consensus expectations, and the year-on-year rate fell by less than expected to 3.8%. The composition was disinflationary however, with a sharp normalization in non-housing services inflation and a return to the Q4 trend for the owners’ equivalent rent category. We also expect the rise in used car prices to more than reverse this spring. On the positive side, communications prices increased sharply for the second straight month and will boost the PCE measure. We now tentatively expect core PCE prices rose 0.27% in February (mom sa) and will update our estimate after this week’s PPI and import price data. We continue to expect the FOMC to leave the Fed funds rate unchanged at the March meeting and to begin the easing cycle in June.

We expect changes to the SEP to paint a picture of optimism around supply-driven growth. The median dot remains at 3. Inflation and balance sheet in focus for the Q&A. Fed remains patient. First cut June. Our strategists stay neutral duration.

With rate cuts coming, attention will turn to central bank balance sheets. In this note, we lay out where the balance sheets are now and where they are going.

… We draw four lessons from the cross-country comparison:

QT is not the opposite of QE. QE took place amid market disruptions and widespread slumps in growth; QT is happening with healed markets, amid growth and inflation. With QE, central banks bought securities in the secondary market; some central banks are making sales, but most have passive QT where the Treasury issues the debt, often at different maturities. QE helped central banks to signal that low policy rates would stay; QT cannot have the reverse role away from the lower bound.

Central bank balance sheets differ substantially across economies. The US relies more on capital markets, so QE took the shape of asset purchases. The European economy relies heavily on bank lending, and so the ECB created TLTROs (Targeted Long-Term Refinancing Operations) for banks in addition to QE. The market has to absorb securities shed through QT, but early prepayments of TLTROs have no such analog.

Central banks can clearly make losses. We highlight how negative income and negative equity at some central banks do not have macroeconomic ramifications. The clearest example is the Czech National Bank, which operates regularly with negative equity. However, political considerations of central bank independence might come to dominate accounting.

Balance sheets should shrink substantially but not revert to the past. The Fed has committed to an “ample reserves” regime that we expect will have over $3 trillion in reserves. Likewise, the ECB decided to continue operating the floor system for steering short-term money market rates in its recent operational framework review, albeit with an emphasis on incentives to reduce banks' reserve holdings as much as possible.

…US In June 2022, the Fed began running off its balance sheet following monthly aggregate reinvestment caps that are now $60 billion for UST and $35 billion for MBS. The result has been a steady reduction in the Fed’s assets, with a short-term blip in March 2023 due to an increase in loans to depository institutions (DIs) amid financial stress in some regional banks (Exhibit 20).

Exhibit 20: There has been a steady decline in the Fed's assets, which we expect to continue

…Bottom line: February’s US CPI readings provided a small relief after January's surprise - different gauges of core inflation all showed improvement, and the breadth of inflation pressures also narrowed. But prices are still rising faster than normal, raising concerns on upside inflation risks against a very resilient economic backdrop. Fed chair Powell recently reiterated a commitment to move rates lower this year. We continue to expect the Fed to start cutting in June, with risks to a slower pace after than we were previously expecting.

… Our rates strategists stay neutral on duration and look for whether the Fed has gained confidence on the path of inflation toward 2%. If the dot plot realizes in line with our expectations, term premiums in the front end will be highest in the last year – making duration attractiv

The considerable uncertainty that we had for the February CPI was not an issue, with a strong, but not worrisome, report…

… Slowing core expected in March We project smaller monthly increases for both headline and core CPI next month. Currently the headline CPI is projected to increase 27bp in March (seasonally adjusted) and the core CPI to increase 23bp. The smaller March increase is a result of a slowing in OER and a decline in used vehicle prices. 12-month core CPI inflation is projected to edge down a handful of basis points to 3.7% in March and slow further in coming months as a result of base effects. In general, we expected core CPI inflation to trend down through the year amid increasing goods supply (particularly for motor vehicles), the pass-through of slower new lease rents into CPI rents, and a generally easing economy…

UBS(Donovan): What price discounting can do (ReSale TALES)

US producer price data is mercifully free of problematic used-car prices and fantasy owners’ equivalent rent. It is also less susceptible to profit-led inflation, covering prices further up the supply chain. The final demand measure has been below 2% y/y for almost a year now, and the overall picture should be of benign inflation pressures.

US February retail sales data include price effects, and some spending on having fun—restaurant spending is included (not the international norm). Profit-led inflation has gone into retreat and retailers have started to profess their love for their customers, so consumers seem more inclined to spend money. It is wonderful what some careful price discounting can do…

The February consumer price data came in a touch stronger than expected. In our view, the details of today's CPI report generally were encouraging. That said, we doubt today's report fills the FOMC with the confidence it needs to begin cutting rates. We expect disinflation progress to resume in the coming months, but we think the FOMC will need to see it to believe it. The first rate cut from the FOMC looks increasingly likely to occur this summer…

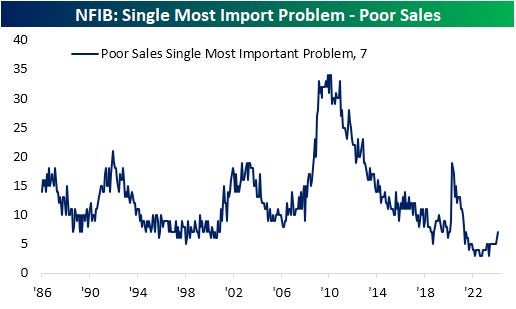

Wells Fargo: NFIB Small Business Optimism Index Dips in February

NFIB's Small Business Optimism Index fell to the lowest level since May 2023 during February. Firms reported seeing improvements in terms of labor availability, while a lower share of firms raised selling prices during the month. Expectations for real sales and better credit conditions also notched improvements during the month. On balance, however, most other components slipped, notably hiring and capex plans. What's more, the share of small businesses reporting inflation as the single most important operational problem rose during the month, overtaking labor quality at the top of the list

Wells Fargo: March Flashlight for the FOMC Blackout Period

Summary

We do not expect the FOMC to change the federal funds rate or alter its current pace of balance sheet runoff at its upcoming meeting on March 19-20.

Since the Committee last met, the U.S. inflation data have come in a bit stronger than expected, while the labor market generally has remained resilient. With payroll growth still solid and inflation proving to be a bit stickier recently, we suspect the FOMC will still be seeking greater confidence at the end of its meeting next week that inflation is headed back to 2% on a durable basis.

That said, beneath the robust headline figures, we see building evidence that the labor market is cooling and inflation is still slowing on trend. Chair Powell testified to Congress shortly before the March blackout period that the Committee is "not far" from the confidence needed to dial back the level of policy restriction.

We now expect the FOMC will initiate the first cut to the federal funds rate at its June 12 meeting (our previous expectation was at the May 1 meeting). We look for 100 bps of easing in total this year and another 100 bps of easing over the course of 2025 to bring the fed funds target range to 3.25%-3.50% by year-end 2025.

In light of the recent slate of data and Fed-speak, we see few changes to the post-meeting statement after a meaningful rework following the January meeting.

The March meeting will include an update to the Committee's Summary of Economic Projections (SEP). We do not expect material changes to the median projections for real GDP growth and the unemployment rate.

The story is similar for inflation. Our most recent forecast projects headline and core PCE inflation of 2.3% and 2.5%, respectively, in 2024. The Committee's median projection in the December SEP was 2.4% for both headline and core PCE, suggesting that the current outlook is not materially different from December for most FOMC members. We think the core PCE inflation median for 2024 will rise by a tenth or so, putting it closer to the midpoint of the central tendency range from December.

That said, even if the magnitude of the changes to the outlook for growth and inflation are relatively small, the direction of the revisions likely will be toward a hotter outlook, i.e. faster growth, and higher inflation. Will the dots follow suit?

Our base case is that the median dot for 2024 will remain unchanged at 4.625%, but the risks are skewed toward a higher median given the distribution of the prior dots and the recent run of inflation data. Similarly, we expect no change to the 2025 and 2026 median dots, though here too we think the risks are skewed to the upside.

A slowdown in the pace of the Fed's balance sheet runoff program also appears to be coming closer into view, and the Committee is likely to have a broad discussion of the central bank's plan for quantitative tightening (QT) at the March meeting.

Our base case remains that the FOMC will announce a plan to slow the pace of QT at its June meeting, although we would not be shocked if the Committee decided to do so one meeting earlier or later. Specifically, we expect the runoff caps for Treasury securities to be reduced to $30 billion while MBS caps are dropped to $20 billion starting on July 1. We anticipate this slower pace of QT running until year-end 2024.

…Poor Sales There's an often overlooked reading in the monthly NFIB Small Business Survey that we like to monitor closely. Each month in NFIB's survey of small businesses, survey-takers are asked what their single most important problem is. Options to choose from include things like inflation, quality of labor, taxes, red tape, and interest rates, but the option we pay most attention to is poor sales.

When business is good, small-business owners can select options like quality of labor or taxes as their single most important problem. But when business starts to weaken, poor sales immediately becomes front and center. If you're not selling, all of the other problems become meaningless anyways.

Yesterday, the latest monthly NFIB Small Business survey results were released, and notably, the poor sales reading ticked up yet again.

Below is a historical chart showing the percentage of small businesses citing poor sales as their most important problem going back to 1986. Note how high this reading got during the worst months of the Financial Crisis. But also note that the reading started to tick higher from low levels as early as 2006.

A couple of years ago, this poor sales reading hit its lowest level ever as other problems like inflation and cost of labor were cited much more often. While poor sales is still very low on the totem pole as the biggest problem for small businesses, it has started to tick higher in recent months, which is definitely worth keeping a close eye on.

Bloomberg: Fed Says Basis Trade ‘Significantly’ Smaller Than Estimated

Researchers use TRACE data for new basis-trade proxy

As of January, the ‘lower bound’ estimate was $317 billion

Bloomberg: Yellen Says Rates ‘Unlikely’ to Return to Pre-Covid Levels

Treasury chief answers question on new White House forecasts

Yellen says new projections reflect market ‘realities’

… “I think it reflects current market realities and the forecasts that we’re seeing in the private sector — that it seems unlikely that yields are going to go back to being as low as they were before the pandemic,” Yellen told reporters Wednesday in Elizabethtown, Kentucky.

The yield on 10-year US Treasury notes averaged 2.39% in the decade through 2019 — low by historical standards. It spiked above 5% last October after the Federal Reserve raised rates aggressively to combat inflation, and now sits just below 4.2%…

…Higher Forecast The three-month rate, for example, will average 5.1% this year, up from the 3.8% projected last March, White House officials said. The 10-year yield projection rose to 4.4% from 3.6%.

The latter projection might have been even higher but for the intervention of Lael Brainard, director of the National Economic Council, according to people familiar with the matter prior to the release.

Higher rates on the growing burden of US debt add significantly to the overall deficit and debt figures. Under the current assumptions, the White House expects the US to spend about $890 billion, or 3.1% of gross domestic product, on net interest expenses this year…

Bloomberg: Why the Stock Market Doesn’t Care About Rate Cuts (Authers’ OpED NOTE visual of, “It’s the Lack of Earnings Growth, Stupid. Companies in the developed world outside the US haven’t grown profits”)

First, it’s convinced they’re coming eventually. Second, profits at the tech giants dominating the S&P 500 are so high that the discount barely matters

… Note that the picture for the MSCI EAFE (Europe, Australasia and Far East) index of developed markets outside the US is radically different. Profits have still failed to top their level from 2007, before the Global Financial Crisis. Growth is unexceptional:

Providing the profits of the big US companies prove to be sustainable, and the predictions for the future are broadly accurate, then the market is comfortable that the rally can carry on a while longer. Stronger profitability would tend to imply a better economy and less need for rate cuts, but the calculation is that a higher rate isn’t a problem if it’s discounting substantially higher profits…

As readers of this page know, I think the trimmed mean (and the median) are better measures of underlying inflation than the traditional core. Both remove outliers and are better correlated with future inflation than the traditional core.

For today’s data, however, it didn’t matter which metric you focus on: underlying inflation is starting to reaccelerate. In recent months both Fed officials and many economists have been focusing on the 6-month annualized rate of inflation as a gauge of the underlying trend in inflation. Six months is long enough to smooth out the monthly gyrations in the data but short enough to capture changing trends…

WolfST: Higher Forever? Even Yellen Starts to Get it: Higher Inflation & Higher Yields Are Here to Stay

“It seems unlikely that yields are going to go back to being as low as they were before the pandemic”: Yellen.

{kind=link}

📈💤 Looks like we've got some intriguing market dynamics brewing overnight.