while WE slept: USTs MIXED; in uncertain times, avoid stocks, stay in bonds -WSJ; WaPO story on TARIFF MAN; "Why 2025 can be another great year" -DB

Jan 06, 2025

Good morning … Today is likely to be first real day of trading and narrative creation with the “A” team likely back from holidays and ready to go.

This mornings Early Morning Reid recap of the week just past (ISM 9m high, Claims lowest since April, Johnson re-elected as speaker and all the Fedspeak) …

…In the meantime, we had comments from several different Fed speakers about the policy outlook over the weekend and on Friday. Generally, those comments have implicitly sounded quite cautious about the scale of further easing, which echoes the Fed’s hawkish shift in their December dot plot, where they only signalled 50bps of cuts for 2025. For instance, on Friday Richmond Fed President Barkin said he was “in the camp of wanting to stay restricted for longer.” Then over the weekend, San Francisco Fed President Daly said that inflation was still “uncomfortably above our target”, whilst Governor Kugler said that “we know the job is not done” with inflation still not at 2% yet. This backdrop has seen US Treasury yields move higher this morning, with the 30yr yield (+1.8bps) currently at 4.83%, which would be its highest closing level since November 2023. And this Wednesday coming up, we’ll get the minutes from the FOMC’s recent meeting in December, so it’ll be interesting to see how that debate unfolded given there was a dissenting vote…

No shortage of inputs for this global narrative creation … in addition TO Fedspeak, I’m going to guess we’ll see / hear / read more and more about possibility of importing de / disinflation from China …

… also likely to hear much ‘bout politics and rate cut pricing …

Bloomberg: Bond Traders See Fraught Year Ahead as Trump Shadows Outlook

Longer-term yields have jumped on inflation, stimulus risk

Futures pricing in only two quarter-point Fed cuts in 2025

… The market will see a test of demand with a slate of Treasury auctions that start on Monday, a day earlier than usual, because of the market’s closure Thursday to honor the death of former President Jimmy Carter. The auctions will include new 10- and 30-year securities.

Those will be followed by the Labor Department’s monthly employment report on Friday, which is expected to show that 160,000 employees were added to payrolls in December, a slight slowdown from 227,000 the previous month, according to economists surveyed by Bloomberg. Given how much yields have risen, JPMorgan’s Misra said there’s a chance that a sharper-than-anticipated slowdown in job growth could cause bond prices to bounce back some.

“A weak number will bring talk about a March Fed rate cut back on the table,” she said…

… I’ll quit while I’m behind and wish one / all a terrific (unofficial)start to 2025 … and as I do I’ll note a WashPO story which hit earlier …

WashPO: Trump aides ready ‘universal’ tariff plans — with one key change President-elect’s aides look at universal import duties, but only on certain sectors, among first big moves of presidency…

… followed by a WSJ story noted by PiQ below …

WSJ: In Times of Economic-Policy Uncertainty, It May Be Best to Avoid Stocks. Research suggests that stocks, and especially small-caps, outperform bonds when uncertainty falls. But bonds are the place to be when uncertainty flares, as it has recently.

… which means to me, we’re right back to those known unknowns and as such, 3s likely to garner a decent bid later on today … here is a snapshot OF USTs as of 652a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK: European tech lifted after Foxconn posts record Q4 revenue, USD dips lower … USTs are pressured ahead of 3yr supply; Gilts underperform after a survey showed that 55% of UK businesses intend to lift prices in the next three months (prev. 39%) … USTs are pressured following the downside seen last week post-data and as the region awaits a hefty and frontloaded supply schedule. Furthermore, JGBs influenced overnight with the contract to a fresh low after remarks from Ueda who stated that he plans to increase interest rates with continued economic improvements but added the timing of an adjustment is dependent on the economy and inflation. As it stands, USTs are at lows of 108-12, matching the 30th December base with support from the session’s proceeding at 108-11+ and then the 108-06+ contract trough.

WSJ: In Times of Economic-Policy Uncertainty, It May Be Best to Avoid Stocks. Research suggests that stocks, and especially small-caps, outperform bonds when uncertainty falls. But bonds are the place to be when uncertainty flares, as it has recently.

Opening Bell Daily: Mag 7 vs. everyone … The S&P 500 barely moves without the Magnificent 7 … The benchmark index would have been flat for two years without Big Tech.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ … With the “A” team only likely to be just getting back into the swing of things, the inbox has been relatively tame which then normally means one thing — ‘they’ will look to catch up and I’d expect an overwhelming amount of ‘narrative’ (re)generation in the days and weeks just ahead. As always, will curate and limit to things I used to read / pass along / discuss with institutional FI client base in years past … that said, jumpin’ in …

In this note, from the same shop / stratEgerist as noted above near the beginning …

DB: Mapping Markets: Why 2025 can be another great year

As market strategists, we spend a lot of time thinking about what might go wrong. But the last two years have also demonstrated how the macro news can surprise well on the upside.

After all, most years are normally quite good for markets. In fact since 2008, the S&P 500 has only posted a negative total return in two out of 16 years. Elsewhere, the STOXX 600 and the Nikkei don’t have quite as stellar a record, but they’ve still only posted 4 out of 16 negative years.

So as we look forward to 2025, it’s worth remembering that there's the potential for a lot to go right. After all, many of the most obvious risks are already priced in. There’s no sign of an economic downturn. Financial conditions are very accommodative. Several leading indicators of a US recession are now pointing away from one again. Even if we do get a downturn, central banks now have plenty of scope to cut rates. And whilst there are plenty of geopolitical risks right now, that hasn’t been a factor that markets have traditionally reacted much to.

So what's the upside case for 2025?

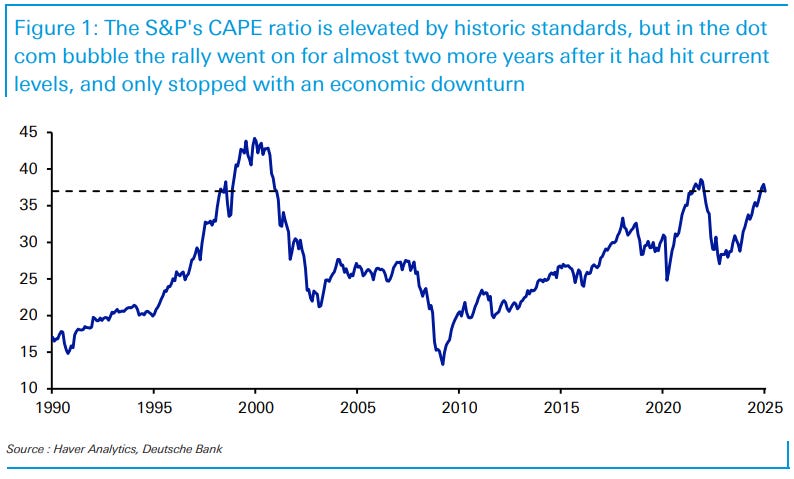

1. Starting valuations might be high and evoking comparisons to the dot com bubble, but the dot com bubble burst alongside an economic downturn, of which there’s no sign today…

The current backdrop of rate cuts taking place in a soft landing (rather than a recession) has been incredibly favourable for risk assets historically…

3. Over recent months, a lot of leading indicators that historically signalled a US recession are no longer pointing towards one…

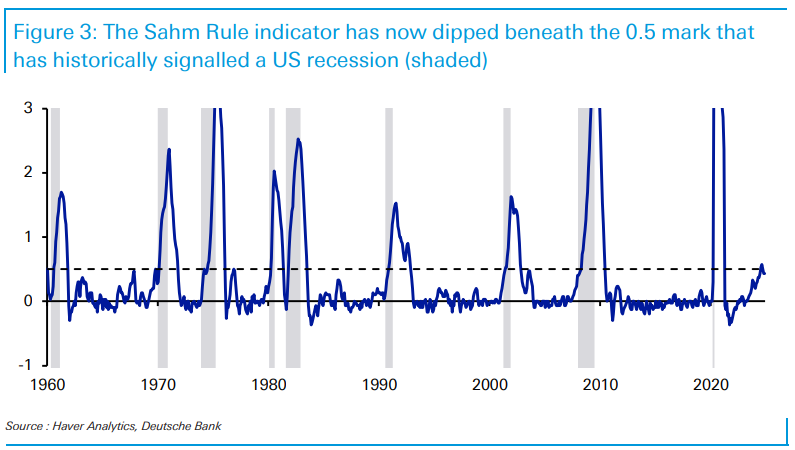

…Third, the Sahm rule (which signals a recession when the 3m average of the unemployment rate moves up by half a point within a year) is also no longer signalling a recession. That moved above 0.5 in the July jobs report, which was a major contributing factor behind the summer market turmoil as investors feared a US recession. But that’s since dipped beneath 0.5 again.

4. Whilst it might not be the base case, there's a further upside scenario for markets if inflation started surprising on the downside again…

5. A lot of key downside risks are already priced in…

…So as we look forward to 2025, we shouldn't let a pessimism bias overtake us. Of course, random and unexpected shocks are likely to hit at several points. But the current market backdrop is an incredibly favourable one, meaning that 2025 is capable of being another strong year.

… used to be a saying (and it’s made a comeback with rate HIKES in 2021), cash is king but perhaps there’s a new saying out there on Global Wall …

…2. Bonds are king. Another reason investors have been unwilling to maintain elevated cash balances is an expectation that sooner or later central banks would be cutting rates to neutral or below neutral levels. In turn, this expectation has created higher than normal demand for duration as investors try to lock in still elevated bond yields before central banks cut rates too much . The $1.3tr entering bond funds last year, a record high, reflects to a larger extent this demand for duration (Figure 2). In addition, another source of demand for duration likely stemmed from last year’s unexpectedly large equity price appreciation that induced some investors to buy duration as a hedge again their rising equity allocations…

For as long as retail investors continue to pour money into the AI theme, the AI led boom in stock markets is likely to continue.

Deviations from fair value persistent in equities. Deviations from fair value more mean reverting in rates.

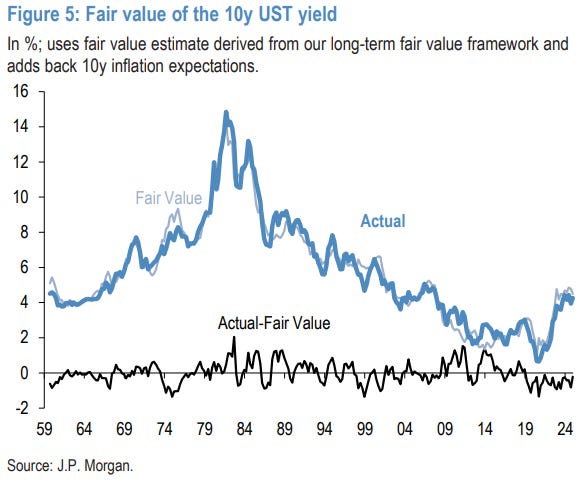

…5. Deviations from fair value more mean reverting in rates. For bonds, we can similarly use our long-term fair value framework for 10y real UST yields, which models the 10y real rate as a function of the real Fed funds rate, inflation vol as a proxy for term premia, and three major components of net demand for dollar capital: government, corporate and emerging markets. We measure these as the government deficit, the corporate financing gap (the difference between capex and corporate cash flow), and the EM current account balance, all as a % of US GDP. In addition, the model captures the effect of central bank balance sheet policy via a flow effect, where we subtract Fed net bond purchases from the overall government deficit, and a stock effect, measured as the ratio of reserves divided by the stock of government and agency securities held outside the Fed (for further details, see F&L, May 23rd 2024). Figure 5 Fair shows the actual and fair value of the 10y UST yield, as well as the residual. Compared to our model for the S&P 500, where the gap between actual and fair value has lasted on average around 4 years since the early 1990s, this gap has on average lasted 6 or 7 quarters for 10y USTs. Moreover, for 4Q24, our long-term framework suggests a fair value for the 10y real UST yield of around 2.2%, around 20bp above the 4Q24 average real yield and broadly in line with current real yields on 10y TIPS implying we are starting 2025 broadly fair.

US corporate sector health and their ability to service their debt is deteriorating very slowly pushing back the risk of US recession.

Do not overemphasize risk scenarios when investing.

Markets underestimated a Trump win in 2024, they might be underestimating Trump policies in 2025.

Risk of sustained deflation is the elephant in the room in China.

The “debasement” trade is here to stay.

… this next note is on commodities specifically but these are the sorts of narratives that matter to us all, not just those tasked with setting monetary policy …

MS: The Oil Manual: 2025 Outlook: Balancing Act Continues

We still estimate the oil market in a modest surplus in 2025, although significantly smaller than before the December OPEC+ meeting. This likely anchors Brent around $70/bbl, but not lower than that.

Same shop with a couple weekly VIEWS … on stocks and global economics …

Equities are rate-sensitive again as the 10Y yield has pushed through the 4.50% threshold we highlighted. This has driven narrower breadth recently. We favor the quality factor (key screens in today's note) and industries showing strong EPS revisions (Software, Financials, Media & Entertainment).

Equities Are Rate Sensitive Once Again...In early December, we highlighted that 4.00%-4.50% on the 10-year yield was likely the sweet spot for equity multiples. We thought that a break above that threshold driven by either less dovish monetary policy expectations or a rise in the term premium would likely serve as a headwind for multiples as it did in April of 2024. Recently, these drivers have pushed the 10-year yield above 4.50% and the correlation of equity returns to bond yields has flipped decisively into negative territory (yields up, stocks down and vice versa)—something we have not seen since last summer. Meanwhile, economic surprise indices have fallen and, thus, are not the driver of higher yields. The combination of these factors makes rates the most important variable to watch in early 2025, in our view.

Exhibit 1: Recent Rise in Interest Rates Has Been Driven Mostly by Term Premium Which Has Started to Weigh on Multiples

Exhibit 3: The S&P 500 Is Trading Rich Relative to Underlying Breadth – Will It Continue?

…While not a perfect measure, we do find that the y/y change in global M2 in US Dollars is a good way to monitor key inflection points.

Exhibit 4: Y/Y Change in Global M2 in USD Has Coincided with Important Swings in Equities

MS: The Weekly Worldview: Our Global View After the Holiday Break

…The US economy comes into the year on solid footing, with healthy payrolls and strong consumption spending. Disinflation continues, and the inflation data for November were in line with our forecast, but softer for PCE inflation than the Fed had expected. While the Fed lowered the policy rate by 25bp in the December meeting, Chair Powell’s tone was very cautious and the Fed’s projections had inflation risks skewed to the upside. The Chair noted that the FOMC was only beginning to build in assumptions about policy changes from the new administration. We have conviction that tariffs and immigration restrictions will both slow the economy and boost inflation, but we have assumed the policies are phased in gradually over the entirety of the year. Consequently, the material stagflationary impetus is reserved for 2026, not this year. Similarly, we assume that effectively, the entire year is consumed by the process of tax cut extensions. So, we have penciled in no meaningful fiscal impetus for this year. Indeed, with the bulk of the process simply extending current tax policy, we have very little net effect, even in 2026…

… here in this next note, the Swiss economist pushing back on US tax policy …

US President-elect Trump has been posting on social media in support of a single budget bill through Congress. A single bill might take longer to pass, delaying policy implementation. Trump advocated taxing US consumers of foreign goods to pay for an abolition of taxes on tips. (Tipping has been a hidden inflation force in the US, raising the cost of services without being recorded in inflation data)…

Finally, with some NFP precaps already behind us (weekend and Friday), another from Dr. Bond Vigilantes shop …

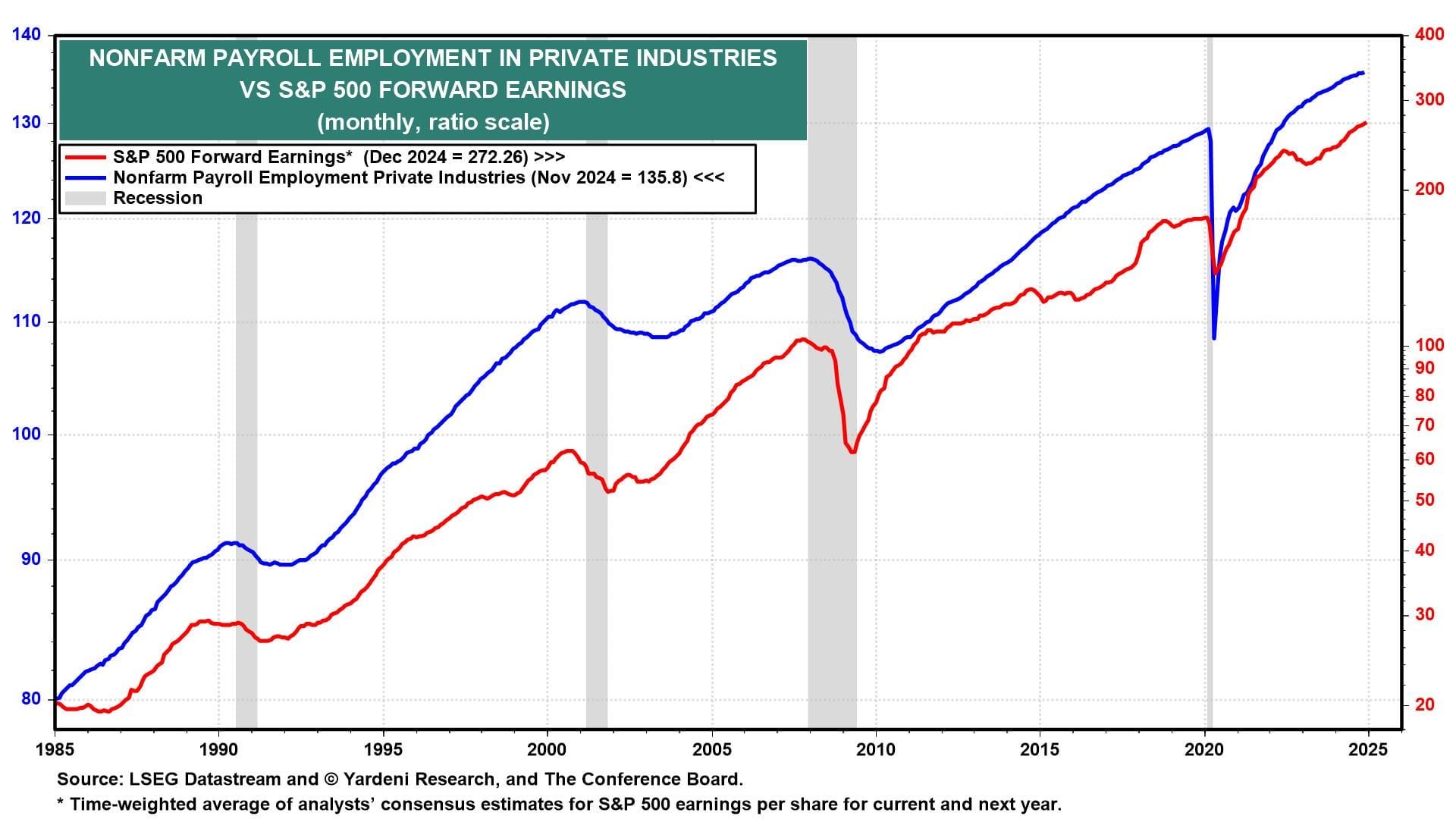

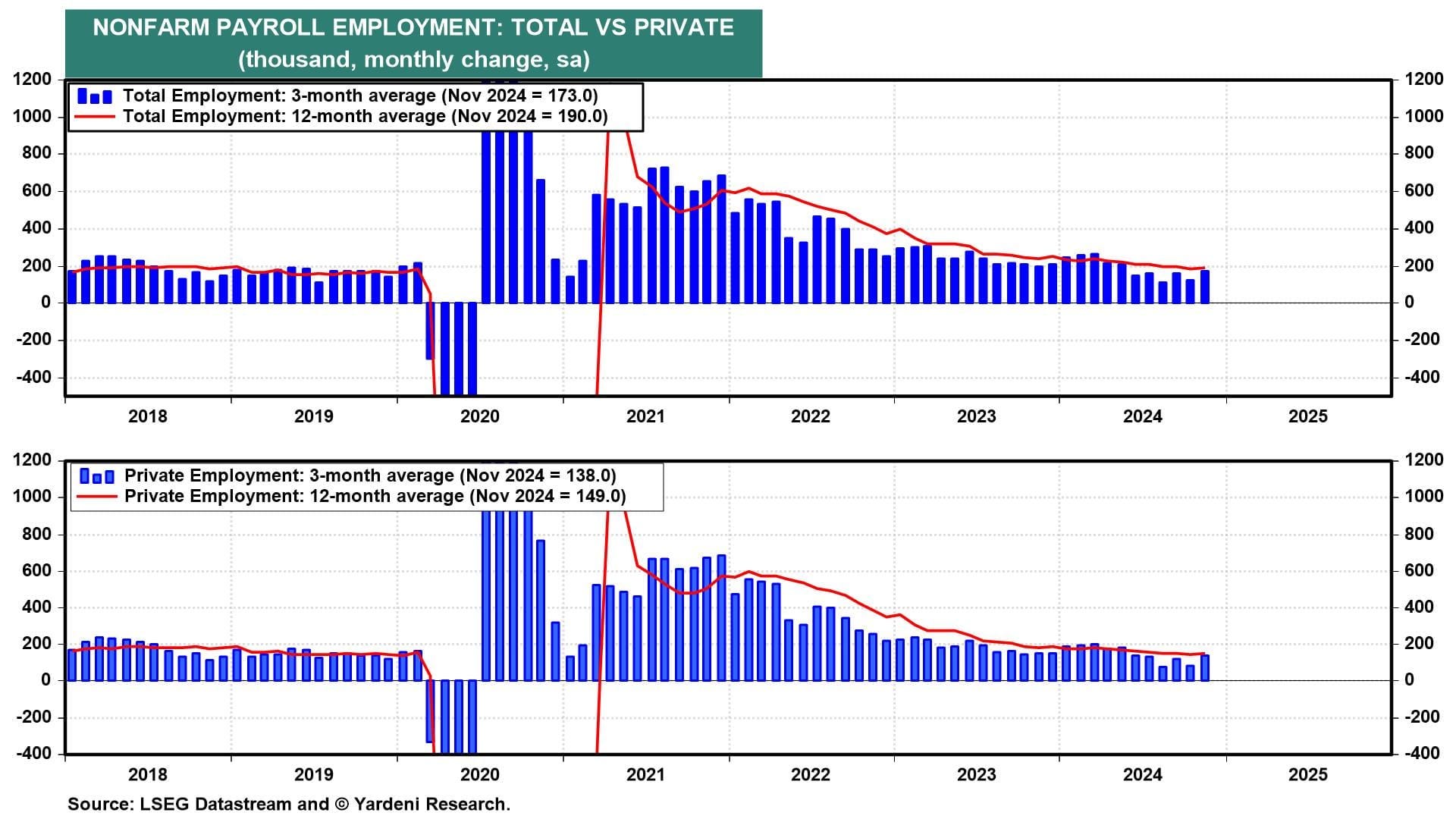

The economic week ahead is chockful of labor market indicators for November and December. We're expecting them to beat expectations. As long as corporate earnings continue to reach new record highs, companies are likely to hire more workers and increase real wages (chart). Ultimately, that supports consumer spending and stock prices.

Still, there are a number of potential headwinds for stocks, not the least of which is rising bond yields. Better-than-expected economic data could put further upward pressure on the 10-year Treasury yield, which is already at 4.60%. On balance, we still expect good economic news to be good news for the stock market. Here's more on what we're expecting this week:

(1) Employment. December's employment report (Fri) should show payrolls rose between 175,000-200,000 to a new record high. This is the first "clean" monthly employment report after October's was depressed by hurricanes and strikes and November's was boosted by returning workers from both. We still expect the three-month gain in payroll employment will average 200,000 per month by January's employment report (chart).

Additional hiring thanks to Trump 2.0 is highly likely, both due to potential new policies (i.e., deregulation and lower corporate tax rate) as well as general increased certainty following the presidential election. The unemployment rate likely stayed around 4.2% in December as initial unemployment claims (Thu) remain low…

… And from the Global Wall Street inbox TO the WWW … a few curated links …

First UP, if the consumer is in ‘excellent shape’ then we’ve got rate HIKES to come OR it is because the Fed CUT RATES and will likely continue to do so, making the consumer even more excellent’er … please choose one as you read …

Apollo: 10 Charts Showing the US Consumer Is in Excellent Shape

The US consumer is in incredible shape.

Specifically:

– The incoming weekly data shows continued strength in consumer spending, and outlook surveys show continued strength ahead (Charts 1 to 3).

– Credit card debt as a share of disposable income is below pre-pandemic levels (Chart 4).

– The effective interest rate on mortgage debt outstanding is only 4% (Chart 5).

– Households are reporting that it is easier to get access to credit, and banks are more willing to lend to consumers (Charts 6 and 7).

– HELOC balances are rising, and savings are rising for most households across the income distribution (Charts 8 and 9).

– Debt to disposable income is declining, and US households are in much better shape than households in Canada and Australia (Chart 10).

The bottom line is that incomes are high, stock prices are high, home prices are high, debt levels are low, interest rate sensitivity is low, and banks are more willing to lend to households.

There are significant upside risks to US growth, inflation, and interest rates as we enter 2025.

… this next item from BBG over the weekend of particular interest to those in FI markets whereas spreads (wide / tight) are often a direct reflection of risk off / on and so, Fed policy transmission …

Bloomberg: How Low Can Bond Spreads Go? Five Numbers to Watch

Corporate-bond premiums could approach all-time lows in 2025

Buyers find comfort in improved market liquidity, quality

… “While fixed income spreads are tight, we believe a combination of deteriorating fundamentals and weakening technical dynamics would be needed to trigger a turn in the credit cycle, which is not our base case for the coming year,” said Gurpreet Garewal, macro strategist and co-head of public markets investing insights at Goldman Sachs Asset Management.

… chalk this next one up for those in favor of seasonals and patterns and things like the Santa rally …

After an unusually weak December (S&P500 was -2.5%), without its typical Santa Claus rally, the debate continues as to how will the US (& other) equity markets perform in 2025. Most Wall Street strategists are bullish for the year.

We outlined our short term (1 – 4 month) views on US equity markets in our latest ‘Tactical Equity Asset Allocation’ publication (available to ‘Tactical’ subscribers, published in early December & titled: “This Bull Run (since Oct ’22) is Tired!, A.k.a. But Stay Tactically OW (for now)”); as well as our longer-term views (i.e. 6 months to 2 years) in our latest ‘Strategic Global Asset Allocation’ publication (published just prior to Christmas – see snippet below).

Elsewhere the January effect is often watched closely to give clues as to the outlook for the year. There’s a view in markets that “how goes January, so goes the year”. Those relationships, however, are weak. Our analysis of the correlation of the performance of both the first trading day and the first week of January with the year found, in both instances, only a trivial R squared (of 0.01 and 0.001). That is, there’s no clear evidence for the ‘January effect’ over the 85 years of data that we examined (1929 – 2014).

Next week brings the first full trading week of the year. The key data comes out at the end of the week with the US monthly non-farm payrolls, average hourly earnings and unemployment rate released on Friday. Ahead of that, ISM services data is released on Tuesday; with various other labour market data coming out over the course of the week (including JOLTS on Tuesday; ADP on Wednesday; & Challenger job cuts on Thursday). It’s also a key week for inflation data (EZ CPI is on Tuesday; Chinese CPI and PPI are on Thursday). A full list of key events next week is laid out below.

Key chart: Global S&P1200 equity index shown with key moving averages

… and once again risking the diversion of your attention TO the Fed (will they / won’t they / do they really need to IF consumer in such good shape — Apollo above — this next note tries to un-divert yer attention …

Sam Ro from TKer: For stock market investors, focusing on Fed rate cuts is misguided

… One of the biggest questions among market participants is how many times the Federal Reserve will cut rates in 2025. Some have even floated the possibility of a rate hike during the year.

The Fed and its decisions on monetary policy are important. Central bank actions affect the cost and availability of money, which can move the needle on the economy.

In the wake of arguably hawkish monetary policy news in December, there’s some concern out there that fewer-than-expected rate cuts from the Fed is bearish for stocks.

But for stock market investors, this narrow focus on rate cuts is misguided. How many times the Fed cuts rates is not the right question.

Rather, what matters are the developments in the economy that are causing the Fed to adjust its outlook for monetary policy…

…Fewer rate cuts? No problem … “Financial markets have sharply reduced their expectations for US monetary policy easing,” Goldman Sachs’ Jan Hatzius observed in a Dec. 23 note to clients. “Fed funds futures now imply 2025 rate cuts totaling less than 40bp, down from 125bp right after the 50bp cut in September.”

Expectations for rate cuts have fallen over the past three months. (Source: Goldman Sachs)

A popular view is that rate cuts would be bullish for risk assets like stocks. So any developments that lower the odds of a rate cut in the near term would therefore be bearish. All other things being equal, this view makes sense…

… hmmm IF what matters is the economic developments, and the Fed can either continue to add wind in the economic sales OR choose to become more prohibitive ‘er, then aren’t we all sayin the same thing? Sam here just trying to stand out, be different but am just pausing and asking cuz … not for nothin’ … seems like we’re all saying / thinking same just that some are trying to get paid for their OPINION and narrative?

Finally, preparing for latest bout of snowMAgeddon here and passing along latest PSA …

Stop hoarding we need some of that snow out west here after the holiday crowds thrashed everything. I'm tired of skiing on ice lol!