Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP, when yer hot yer hot and when yer not, well … this and this :)

Next time I chime in about short or long term buying / selling, I trust you’ll know what to do …

This in mind, what looked to be like a short-term ‘rental’, perhaps Friday still works out to be a ‘dipORtunity’ (?) … I’ll continue watching that double-top TLINE (4.85) and in somewhat more / bigger picture context …

30yy WEEKLY: double top ~4.84% and Oct ‘23 cheap up nearer 5.20% …

… with momentum overSOLD and looking ‘toppy’, rolling over and crossing would increase confidence in the idea of a ‘rental’ expressed (unsuccessfully) in the week just past …

… now with some context and levels in mind, WHY might one want to own FI (aside from a risk off / fund flows conduit noted HERE?

ZH: Global Manufacturing PMIs Drop Back Into Contraction As US Prices Paid Jumps

…The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2024 is 2.4 percent on January 3, down from 2.6 percent on January 2. After this morning’s Manufacturing ISM Report on Business from the Institute for Supply Management, the nowcasts of fourth-quarter real personal consumption expenditures growth and fourth-quarter real gross private domestic investment growth decreased from 3.2 percent and -0.7 percent, respectively, to 3.0 percent and -0.9 percent.

… stay tuned, next GDPNow update Tuesday 1/7 …

Alrighty, then.

I’ll move on TO some of Global Walls narratives — SOME of THE VIEWS you might be able to use. Unlikely to get normal ‘weekly' views as most of the “A” team remained on holiday. In other words, we get what we get and we don’t get upset, as our boys preschool teacher used to say. A few things which did hit the inbox and stood out to ME …

Here’s one that isn’t all that exciting … at least that’s what title says the data is (or isn’t) to me … its strength / improvement was, you know, TRANSITORY …

BARCAP: ISM manufacturing: No cause for excitement

The manufacturing ISM rose 0.9pts in December, ascending further into the upper-end of the range that has prevailed since late 2022. We suspect that December's improvement reflects transitory influences, as opposed to acceleration in underlying demand for domestic goods.

This next one, same shop, on energy (read: EARL) may very well impact consumer behavior, belief and ultimately, ‘flation expectations …

The recent rise in oil prices likely reflects greater confidence among market participants in improving oil market fundamentals. We reiterate our $83/b fair value estimate for Brent this year, $9/b ahead of the forwards curve at the time of writing.

… up next in the inbox, a rehash of an outlook — think RANGEZILLA — in case you hadn’t seen / read yet …

In the year ahead, the primary question will be whether the Fed is able to keep the prevailing positive momentum in the real economy intact given the crosscurrents of risks on the macro horizon. The debate between soft- or hard-landing has ostensibly been resolved in favor of no-landing – at least until there is a body of evidence that skews investors' angst back toward the sustainability of the current trajectory of growth. The ability of the consumer to maintain the remarkable pace of consumption demonstrated during 2023 and 2024 will be tested in the coming quarters as the impact of the Fed’s restrictive monetary policy stance continues to work through the system. Not only has the resilience of the US consumer been this cycle’s biggest surprise, it has also afforded the FOMC the needed flexibility to continue its battle with inflation largely unimpeded by concerns of slipping into a recession.

Powell’s decision to normalize policy rates after spending 14 months at terminal represents the Chair’s effort to preserve growth while continuing to allow realized inflation to drift back in line with the Fed’s objective. While the path toward the Fed’s inflation target has been appropriately characterized as 'sometimes bumpy', the reality remains that the acute risk of permanently losing the price stability assumption in the US economy has passed. Notwithstanding Trump’s victory and the GOP sweep, the progress already achieved has been sufficient to regain any credibility that the Fed might have lost as an inflation fighter.

There is always the chance of a reflationary surge that stalls Powell’s progress back toward neutral. However, such an eventuality would not be comparable to the challenge made to the Fed’s credibility as a result of the pandemic. By concluding that the Fed has successfully demonstrated to investors its willingness and commitment to reestablishing price stability, we’re not simultaneously suggesting that the FOMC’s job is completely done or that policy will never be tightened again. Instead, investors have come away from the last two years convinced that while the lagged impact of the Fed’s actions are difficult to estimate, the reality is that monetary policy still works – even if it remains akin to driving with solely the benefit of the rearview mirror.

Extending this logic a bit further, the Fed is cognizant that the rate cuts delivered in 2024 are unlikely to have an immediate impact on demand or the labor market. In effect, Powell’s initial steps toward normalizing policy were undertaken with an eye on the second half of 2025 before the influence becomes more tangible. As such, any fallout for growth, jobs, and sentiment during Q1 and Q2 are largely set to unfold regardless of the Committee’s current actions. Another meaningful conclusion to be drawn from the Fed’s response to the post-pandemic inflationary environment is that even when faced with decades-high levels of realized inflation, policy rates still only peaked at 5.50% – just a quarter-point above the 2006/2007 terminal. The significance of this cycle’s terminal rate derives its relevance from what it implies for future cycles. Specifically, barring another global event (pandemic or otherwise) that pushes realized inflation so high as to risk the price stability assumption, it is unlikely that the Fed will feel compelled to revisit policy rates above 5.50%.

With the upper bound of policy rates now established in an ‘emergency’ hawkish context, investors can rest assured that more typical, pedestrian tightening cycles will be more contained. As a result, the range for 10- and 30-year yields has been well established and reinforces our assumption that investor demand will continue to emerge during any material backup in yields that puts 4.50% or even 5.00% 10s on the radar. The array of risks facing the US rates market in 2025 certainly won’t prevent bearish episodes and an increase in yields. If based solely on the seasonals, we anticipate the beginning of the year to be biased in favor of higher yields as green shoots and animal spirits create a temporary bearish underpinning for Treasuries. That being said, peak 10-year yields for the cycle have already been established and any subsequent selloff will conform with those parameters…

Payrolls precap, you asked for, welp, this is yer lucky day … note commentary on what to expect in FEB (think downward revision to payroll growth in 23-24, upwards revision to population, labor force … )

BNP: US December jobs preview: Holding pattern before coming revisions

KEY MESSAGES

We look for a rise in nonfarm payroll employment of 165k in December and a steady jobless rate, a stable and trend-like report after the weather and strike effects that jostled the October and November prints.

We expect the Fed would require a clear miss in key dimensions to spur a rate cut this month (payroll growth well below 100k and a jobless rate above 4.3%) versus proceeding with the hold that is currently well priced in.

The pace of payroll employment growth in 2023-24 will likely be revised lower in next month’s report (due 7 February), but should still indicate a resilient job market.

Trend-like gain would greenlight a Fed pause: Our estimates for payroll growth and the unemployment rate in December (data due on 10 January) point to a soft landing for the US job market at the end of 2024. The projected 165k gain in payrolls would be around the 3- and 6-month average pace, while a 4.2% jobless rate would match the median FOMC official’s long-run estimate…

… and with this data precap in mind, what should one do? well buy (EZ) duration, of course ? yep …

Commentary for Monday: Despite the National Day of Mourning on Thursday, the week will be packed with data releases as well as Fedspeak for market participants to absorb. As a reminder, US fixed-income cash markets will observe an early close on Thursday while the federal government and US equity markets will be closed the entire day in honor of former President Carter's service to his country.

With respect to the data docket, it will be focused on the labor market and will culminate with Friday's jobs report for December. Relative to November, which was boosted by a rebound from prior weather disruptions and strikes ending, December's payroll gains should look more moderate. Specifically, we expect headline and private payrolls to grow by 150k (vs. +227k previously) and 125k (vs. 194k) respectively, both relatively close to their six-month moving averages. With respect to the other elements of Friday's report, the unemployment rate should tick up a tenth to 4.3%, given that it was less than half a basis point away from doing so in November. We expect hours worked to remain steady at 34.3 and average hourly earnings growth (+0.3% vs. +0.4%) to slow slightly.

A couple of data points will also inform labor market views heading into Friday’s release—namely, Tuesday’s JOLTS data for November and ISM services (54.3 vs, 52.1) for December, as well as Wednesday’s ADP employment survey (+125k vs. +146k). While the JOLTS data will give more context around November's strong job gains, we caution that the implied net hiring in the JOLTS is not a good predictor of revisions to nonfarm payrolls. Regarding the ISM services, we are looking for a bit of a bounceback in the headline after November's surprising four point drop; however, the employment component will be the more important one to watch….

… next up is a MAJOR note ‘bout bonds. Literally …

HSBC: The Major bond letter #56. Exceptionalism meets expected valuations

American exceptionalism is defined by the Encyclopaedia Britannica as the “idea that the United States of America is a unique and even morally superior country for historical, ideological, or religious reasons”. The term is used in a less jingoistic way in markets to explain expectations for outperformance and divergence with the rest of the world: equity markets keep rising, even after a stellar run, and further dollar strength. In economic terms the US economy has doubled in size since the Global Financial Crisis (GFC, 2008), whilst the eurozone economy barely grew, and projections that China’s economy was on a path to overtake the US have been disappointed.

Bond market exceptionalism is when US Treasury yields rise whilst those in other countries fall. Our chart is one measure of this, plotting the divergence between market expectations of where policy rates will settle in the future, using comparable five year forward swap rates for China, the eurozone and the US. We see that 5Y1Y US-China and US-eurozone forward spreads widened 175bp and 69bp in 2024, respectively, confirming expectations of relative strength in the US economy compared with China and the eurozone.

Forward yields answer the question: What’s in the price? They say that, according to the market, US policy rates are likely to settle more than 100bp above the 3.0% median for the Fed’s longer-run dot (from the meeting on 18 December 2024), some 150bp above the pre-pandemic level.

Exceptionalism meets expected valuations. According to our chart, bond yields say a lot of this exceptionalism has been factored in to expected values, the market’s best guess on what an asset will be worth at some point in the future, a measure of everyone’s views given the available information…

… Our chart shows that only three years ago US forward yields sat between eurozone and China equivalents. Investors will note that the current levels of US yields are already relatively high. American exceptionalism is in the price.

… so rates are exceptional value? data weak ? I’m still unclear if the data was good or bad and seems that there’s not been any CONsensus out there (other than rates ticking higher into weeks end …

ING: US manufacturing shows encouraging signs of life

After languishing for much of the past two years, both the production and new orders components of the ISM manufacturing report have moved into growth territory. However, caution remains with the employment component suggesting jobs continue to be shed while tariff uncertainty remains a concern, particularly for those with international supply chains and those where exports are an important source of revenue

… another look at the economic week ahead, this time from Switzerland …

UBS: US Economics Weekly We expect a volatile 2025

Economic Comment: Projection update ...heading into a volatile 2025? Macroeconomic volatility is relative. The last three years we have published notes on why and in what ways the economic environment is more volatile than most of the post1990 era, which was dubbed "The Great Moderation." We also argued the change was not just due to the pandemic. Looking back at 2024, prevailing narratives proved shortlived. This week 2025 kicked off with a new Republican Congress, which by the end of the month will join a new Republican administration. In this week's Economic Comment we note updates to our economic projections made since our annual outlook note, though overall changes have been few. In 2025, we expect periodic labor market weakness to remind the FOMC that all is not clear, and we also expect that progress on inflation resumes. As a result we expect the FOMC keeps lowering the federal funds rate, projecting 100 bps of rate cuts, though the path may not be smooth. We also expect more uncertainty over trade and fiscal policy to become apparent as we roll through the first half of the year. The Economic Comment starts on the next page.

The Week Ahead: December minutes and payroll employment After two months of noisy weather and strike impacted employment reports, we expect a decent December employment report, though not devoid of noise of its own. We project nonfarm payroll employment expanded180K, accelerating from the preceding two months' average gains of 132K with the help of residual seasonality. The unemployment rate is expected to hold steady, while we estimate AHE expanded 0.26%. We preview the moving parts of the employment report starting on page 14. The minutes of the December FOMC meeting released Wednesday should reveal heightened concern over inflation. We also note in our preview that the minutes often reflect the range of views on the Committee, but at this juncture the Chair has been quite specific in some ways that may differ from that range, in particular views on tariffs. The usual run of other labor market data (JOLTS, ADP, Challenger, and claims) will also be released. The ISM non-manufacturing composite likely improved in December. Trade and inventory data are due out and the preliminary January release of the University of Michigan survey will be released Friday. The Week Ahead begins on page 12…

… you’ve made it this far and are likely no better off than when you began … here you are, stuck in this rut with me, trying to gain some insight from Global Wall on the days data …

Wells Fargo: ISM Manufacturing Ends 2024 the Way It Started It, Stuck in a Rut

Summary Few things were as consistent as the ISM Manufacturing Index in the past year. The index has been in contraction for the past nine-straight months and for 25 of the past 26. Uncertainty continues to hold back broad activity, though there are some signs of stabilizing demand amid industries.

… Moving along TO a few curated links from the internet which maybe useful …

First up, Torsten’s view remains consistent and he looks at different angles …

After the Fed started raising interest rates in March 2022, the banking sector started pulling back, and the decline in credit growth was magnified by the regional banking crisis in March 2023.

With the Fed signaling throughout 2024 that rate cuts are coming, banks are now showing more willingness to lend.

Our updated US banking sector outlook is available here. The charts below show that unrealized losses on investment securities are improving, the share of households reporting that it is harder to obtain credit than a year ago is declining, lending standards on consumer loans are improving, banks are more willing to lend, and loan growth is rising, driven by the large banks.

The bottom line is that tailwinds to the economic outlook in 2025 are driven not only by high stock prices, high home prices, low unemployment, and potential Trump economic policies, but also by banks easing credit conditions as a result of the Fed signaling lower rates ahead.

… this next one from the other day …

Apollo: Quantifying the Impact of the Fed Cutting 100 Basis Points Since September

… The bottom line is that Fed cuts and associated developments in financial markets will boost GDP over the coming quarters by 1 percentage point and boost inflation by 0.5 percentage points …

… here’s another note of caution from folks at Factset …

FACTSET: More S&P 500 Companies Issuing Negative EPS Guidance For Q4 Than Average

… The term “guidance” (or “preannouncement”) is defined as a projection or estimate for EPS provided by a company in advance of the company reporting actual results. Guidance is classified as negative if the estimate (or mid-point of a range of estimates) provided by a company is lower than the mean EPS estimate the day before the guidance was issued. Guidance is classified as positive if the estimate (or mid-point of a range of estimates) provided by the company is higher than the mean EPS estimate the day before the guidance was issued…

… this next note from Barry Knapp (former Lehman guy) worth a look IMO … made me stop and think ‘bout Apollo view and higher for longer and reason for bump higher in yields …

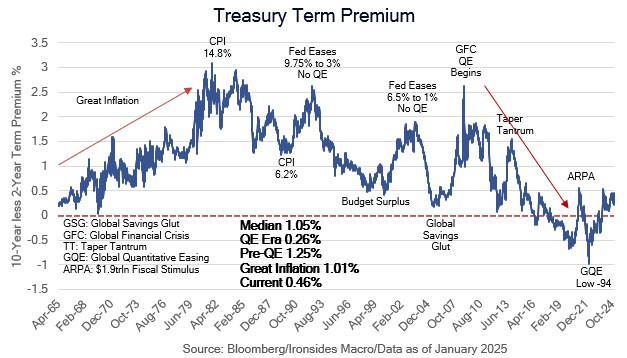

IRONSIDES MACROECONOMICS: Beware January Reversals Higher term premium, Business confidence bounce, China's liquidity trap, QT update, Beware January reversals

Treasuries Overvalued On New Years Eve, Apollo’s chief economist Torsten Slok in his widely followed Daily Spark, noted that the term premium of 10-year Treasuries increased 75bp over the last 3 months. Dr. Slok characterized the increase as follows: “10-year rates have increased an additional 75 bps more than what can be justified by changing Fed expectations, which is likely a reflection of emerging fears in markets about US fiscal sustainability.” From our perspective, the 75bp increase only retraced half of the rate suppression attributable to the Fed’s holdings and the Treasury Department’s reliance of bill issuance (Activist Treasury Issuance/ATI) as measured by the pre-QE era median level. We prefer to monitor the term premium 2s10s curve to further isolate the risk premium from monetary policy expectations. In short, the pre-QE era median level of the 10-year term premium was 1.89%, today it is 0.49%, for the 2s10s curve the pre-QE median was 1.25%, now it is 0.46%. Since the Fed began large-scale asset purchases in late 2008, the median 10-year term premium is -1bp and 26bp for the 2s10s curve. Prior to the QE era, the term premium of 10s or the 2s10s curve only approached zero twice, in late ‘69 prior to the end of the ‘60s expansion and during the global savings glut in early ‘06 prior to the Japanese unwinding BOJ QE1 in 2Q06. A negative term premium makes little sense, and the only plausible explanation is policy intervention. Further supporting our thesis that QE is suppressing term premium is the spike to 2.5% in the early ‘90s when the Fed eased aggressively without QE and again in the early ‘00s following budget surpluses that drove term premium below 0.5% in the late ‘90s.

We began our first note of the year with this modestly esoteric valuation discussion to underscore the largest global risk for early 2025, tighter financial conditions due to a further increase in inflation-adjusted longer maturity rates (TIPS yields). In our 2025 thematic note The Bill Comes Due, we discussed the overhang of Fed holdings, risky Treasury debt management and the deficit outlook. The incoming economic team is well qualified to deal with these issues, however there are no easy solutions and as we discussed earlier, the risk premium remains historically low. From a cyclical perspective, notwithstanding seasonal adjustment factors corrupted by the pandemic policy panic that are likely to boost January employment and inflation data, cooler housing services inflation and weak demand for labor from small businesses should help to stabilize the Treasury market and put the Fed back into easing mode. In short, increasing evidence the economy and inflation are growing only modestly as evidenced by 3Q24 GDI at 2.1%, Beige Book commentary and tepid earnings growth for the S&P 500 ex-technology and communication services, mid and small caps, should cap the increase in rates. Of course, this outlook is subject to government data capturing trends they struggle to measure and may not be apparent until well into 1Q25.

In the meantime, we expect additional pressure on rates as traders reset short positions after elevated year-end financing rates appeared to trigger some short covering during the last few trading sessions of ‘24. Next week’s auctions of 3s, 10s and 30s loom large. Recall the 5-year Treasury Inflation Protected Security auction following the December FOMC meeting had a 7bp tail, making it one of the weakest auctions in two decades. In this week’s note we will discuss the bounce in post-election business confidence bounce, weak demand for labor, China’s liquidity trap, outlook for QT and risk of some nasty countertrend moves in tech stocks, Treasuries and exchange rates this month.

… being a fan of charts and a visual learner, generally speaking …

Morningstar: 13 Charts on Q4’s Big Postelection Rally—and Late Stumble

…Interest-Rate Whiplash

The Fed cut interest rates by 0.25% at its November and December meetings but shocked markets in December with a major change to its projections for 2025.

The target range for the federal-funds rate is now 4.25%-4.50%, a full percentage point lower than before the central bank began its policy easing cycle in September. The Fed’s most recent projections suggest just two more 0.25% cuts in 2025, down from four in its projections from the third quarter.

Central bankers have made clear that with price pressures remaining sticky, they are in no hurry to cut interest rates too quickly or deeply. Strategists say investors should be prepared for an environment in which rates remain significantly higher than their prepandemic lows.

Q4 Bond Market Performance Bond markets saw a major selloff in the fourth quarter, sparked by the outcome of the US presidential election and the potential for stronger economic growth, inflationary policies, and more deficit spending in the years ahead. Yields on the 10-year Treasury note rose from 3.78% at the beginning of the quarter to 4.54% at the end of the year.

As yields rose, bond investors saw losses. The US Core Bond Index was down 3.04% for the quarter, though it’s still up 1.36% for the year. The biggest losses came from long-term Treasury bonds, which fell more than 8%. Investors in short-term core bonds escaped that kind of damage, with that category down less than 1% for the quarter.

Overall, analysts expect the bond market to remain volatile in 2025, but they don’t anticipate another dramatic runup in yields.

… once again, a reminder I’m always and forever a fan of charts and this weekends SPEEDRUN offered a couple …

… The disconnect between US yields and US economic data surprises is worth a look.

This suggests to me that there is risk premium in bonds for the Trump uncertainty, and I guess we can talk more about this in the Interest Rates section, but there are some scenarios now where 10-year yields are completely mispriced and trade quickly back to 3.70% in the next few months…

… Interest Rates

US yields have not made much progress post-FOMC, but they hold steady at high levels. You can see we are drifting back up towards the hallowed 5% level, where Bill Ackman and Janet Yellen announced the top in 2023.

AND before I go, a couple from ZH … First …

ZH: Small Banks Suffer Big Deposit Outflows As Money-Market Funds Hit Record Highs Into Year-End

… finally, an updated hot take of a legend on Global Wall … Bob Farrell — who had a knack for making the complex easy to understand and relate to …

ZH: The Investing Rules Of Bob Farrell – An Updated Illustrated Guide

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,