Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this <off scheduled> note …

SURPRISE!!

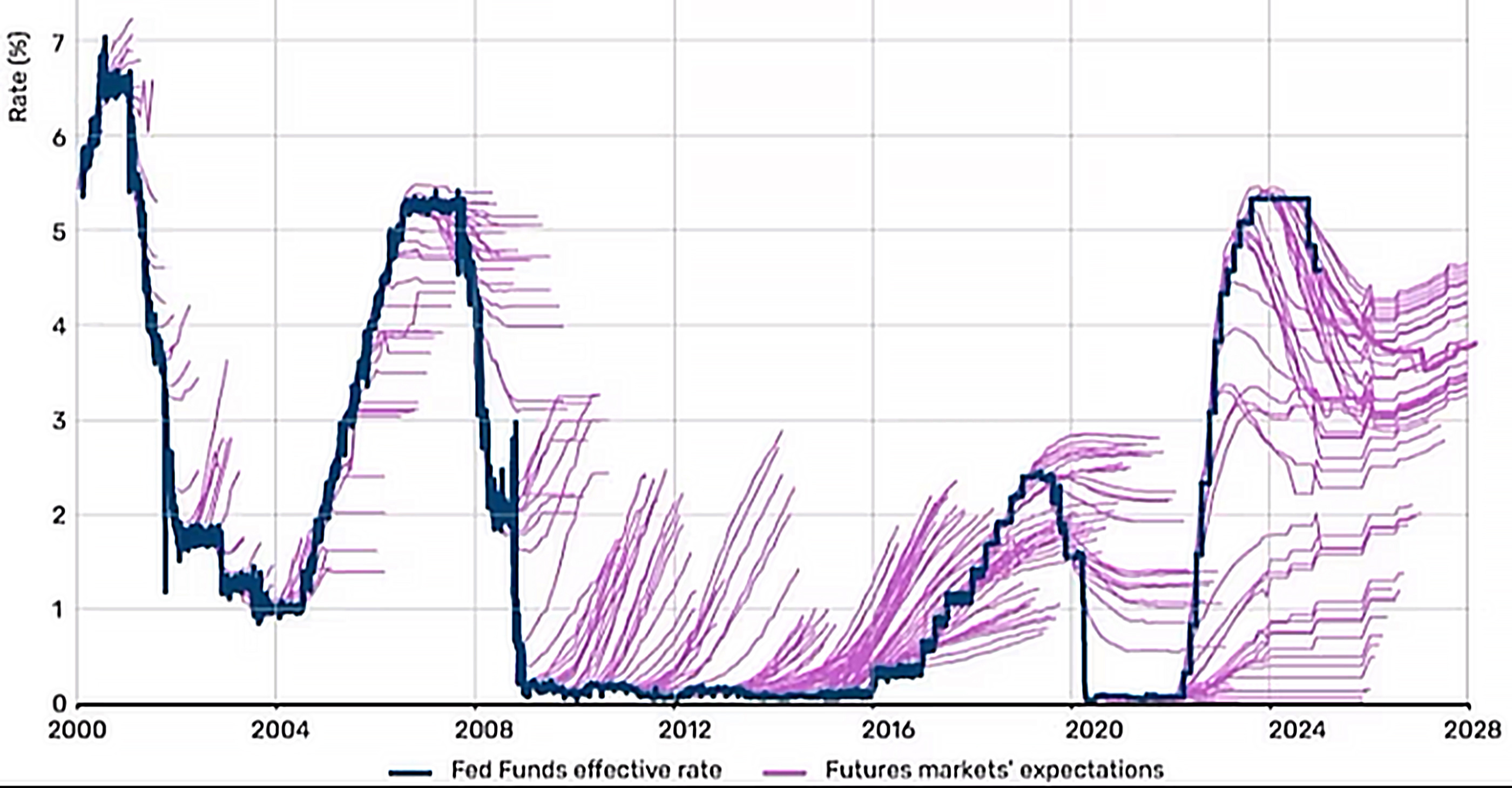

I needed to begin cleaning up the inbox and getting back in to some sort of swing of things so I’ve given the <trading view> Etch-A-Sketch a giant shake shake and gotten rid of all previous TLINEs in effort to have a fresh look at things … THEN I’ve drawn in some new and improved ones …

… The saying "an immovable object meets an irresistible force" — a paradox that describes a thought experiment about two contradictory forces — comes to mind here. The December UPtrend in yields appears to have broken as momentum rolling over and crossing bullishly.

MAY be a rental rather than a long-term buy / hold (famous last words?)

Granted these are not the most liquid of times so take any / all of this with a large grain of salt, washed down with a glass of champagne as you ring in the new year!!

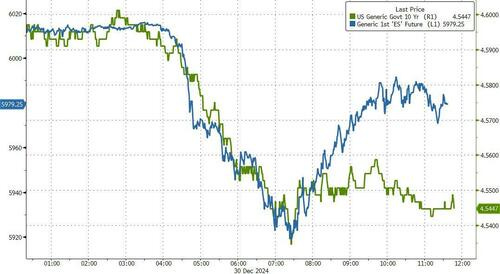

As far as the day that was todays trend break …

ZH: Markets Spectacularly Dump'n'Pump As Year-End Looms

…Bond yields did NOT bounce back higher along with stocks...

And while all yields were lower on the day, it was the belly once again that strongly outperformed...

However, today's strong bond rally needs to be put in post-election context...

Source: Bloomberg…

Dang context … And so … meet the new year, same as the old one …

… what else did I miss?

Ok, sorry, not sorry … Light volumes exaggerate price swings and many out there on Global Wall call these days into years end, ‘amateur hour’. Not to say these opportunities are less good than any others, it’s just that one always has had to keep their friends close and their stops closer, this time of year.

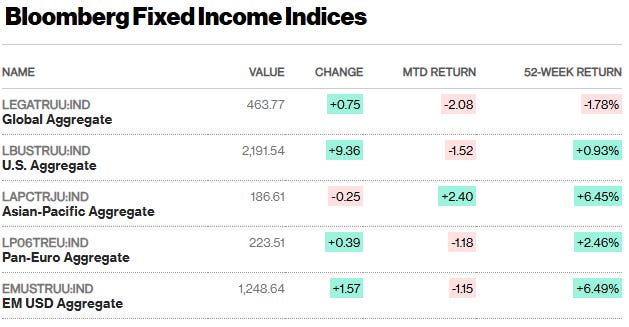

To make light of the absolutely stellar performance YTD (2yrs in a row!!) would be extremely short-sighted. Bloomberg …

STOCKS > bonds. I know, I know … Worst part ‘bout these stellar <equity)gains is there are hardly any tax losses to be harvested!!

I know, I know, first world problems!!

Soul searching a bit over the longest break from ‘the screens’ I’ve taken in years and STILL trying to figure out who and what I want this all to be when it grow up … I’ll just keep taking one day at a time and with that in mind, allow me to thank you once again for inviting me into your inbox as this journey continues.

I’ll strive to NOT waste much (more)of your time and continue to shape / shift presentation of these ‘materials’ best I can.

I’ll try to be more opinionated (easier to do with another turn ‘round the sun) and, with the new year upon us, I’ve wiped clean ALL my prior TLINES for what I hope will be an unfettered view going forward.

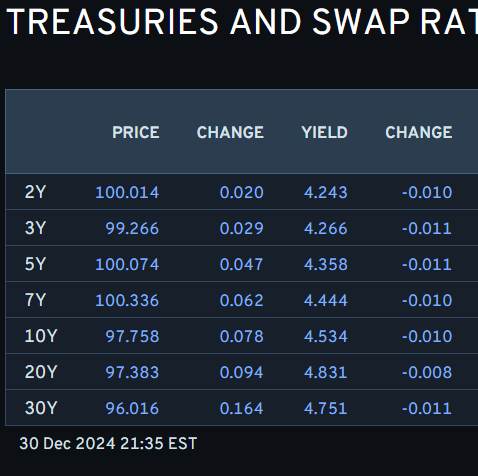

… here is a snapshot OF USTs as of 935p:

… and for some MORE of the news you might be able to use…here are some resources and curated links for your dining and dancing pleasure …

Opening Bell Daily: No bad days in 2025. No one on Wall Street expects a bad 2025. Every major forecaster sees the stock market climbing again next year.

Finviz (for everything else I might have overlooked …)

ZH: US Credit Card Defaults Soar To Crisis Highs As Inflation Storm Crushes Working-Poor

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

A fan favorite, Michael Cembalest doing what he does (from Dec 10th)…

I was visited by six ghosts recently warning me of dangers related to predictions, allocations, apparitions, legalizations, expurgations and ablations. Here’s what they said.

Every December, we publish our predictions for the year ahead. We believe these predictions have at least a 1-in-3 probability of materializing – making them realistic, while not necessarily being our base case expectations. We also ensure our predictions are not currently priced into the markets – making them surprises relative to investor positioning.

…5. 10-year US Treasury Yield trades in a range of 75bps or less

The new fiscal regime in the US has investors braced for another year of high interest rate volatility in 2025. So far in 2024, the 10-year US Treasury has traded in a range of over 100bps. Meanwhile in 2023 and 2022, the 10-year US Treasury traded in a ~150bps and ~250bps range, respectively, as the Federal Reserve (Fed) roiled the bond market with an aggressive rate hiking cycle after letting themselves get too far behind the inflation curve. Next year, the Fed may actually find itself at the right policy setting without having to do much at all! The last time the range was less than 75bps was in 2017 when the Fed was hiking at glacial pace and inflation was stable. Today, the Fed has eased 100bps already, taking the edge off the economy, but policy remains restrictive enough to counter any fiscal impulse. Meanwhile, with so much cash on the sidelines, we expect captive buyers to jump in on any meaningful backup.

… speaking of surprises …

MS: Top 10 Surprises for 2025 | Global Macro Strategist

A year without surprises would be a surprise itself. Given every year comes with some, we discuss 10 that would make investors think differently and move global macro markets.

Surprise #1: Fiscal fireworks shoot in different directions. Less impactive deficits in the US and more impactive deficits in China and Germany lead to convergence between US rates and those in Europe and China, and a dramatic depreciation of the US dollar.

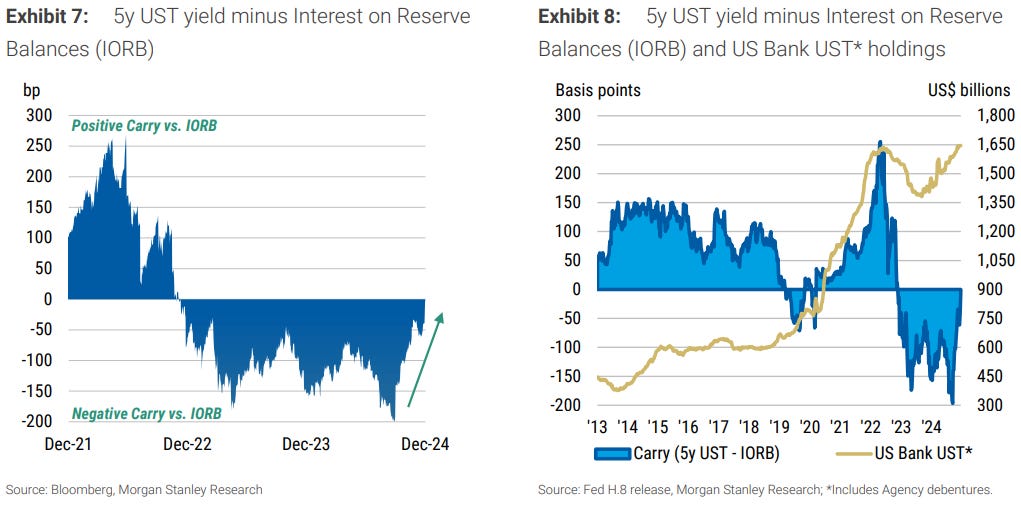

Surprise #2: A demand revival for US Treasuries. Demand for USTs is much stronger than many investors expect. Three main investor groups leading the charge: banks, foreign investors, and pension funds.

…More compelling outlook drives Bank demand: Less stringent regulation, QT ending, and more certainty around the path of Fed policy leads banks to increase Treasury holdings. A more favorable outlook supports bank demand in the belly, with market yields now more competitive against excess cash deposited at the Fed, earning IORB ( Exhibit 7 ).

…Sustained funding ratios above 1.00 continue to bring demand from pensions: As we have discussed, when pensions have a funded surplus, the market value of their assets exceeds the present value of future liabilities. So pensions may not need to assume the same degree of risk in investment portfolios to ensure distribution obligations are met.

Recent years have brought record-high equity prices, and we have observed likely rebalancing out of equities and into Treasuries. This is shown via a sustained cumulative decline in equity prices alongside lower long-end bond yields in the 30-minute window before the NY equity close ( Exhibit 11 ).

This relationship seemingly paused in the latter half of the year. But we think this incentive to de-risk out of equities (return enhancers) and into Treasuries (volatility reducers) remains in place in 2025, especially if long-end rates remain at elevated levels while equities continue to climb even higher. The conditions are in place for pensions to likely have a significant demand presence in the long end in 2025 ( Exhibit 12 ).

Surprise #3: The SOFR swap spread curve bull flattens. UST coupon issuance underwhelms and swap spreads widen. The Fed overweights front-end purchases as the balance sheet grows.

Surprise #4: The EUR 10s30s curve flattens While the macro backdrop favors re-steepening of the EUR 10s30s curve, a mild repricing of volatility could put the position at risk in the first months of 2025.

Surprise #5: The BoE cuts the easing cycle short. Persistent inflation constrains the BoE's ability to cut the Bank Rate further – limiting a rally in gilts and gilt outperformance cross-market.

Surprise #6: The JGB curve bull flattens, not bear flattens. The JPY rates curve bull flattens as the elusive US hard landing arrives or Japan's wage growth disappoints.

Surprise #7: The EUR shines brightly. Consensus is quite EUR-negative – and for good reason. But low expectations means there is greater scope for Europe to outperform expectations, particularly if private consumption fuels stronger growth and European capital rotates back home.

Surprise #8: The dollar shrugs off US tariffs. USD weakens after tariffs are imposed as growth in the US weakens more than in the rest of the world; the Fed's reaction function is more growth-sensitive than other central banks; and/or monetary authorities do not weaken their exchange rates in response.

Surprise #9: US inflation breakevens fall. Disinflation continues in the US, supported by weakness in shelter inflation and potential demand destruction by retaliatory tariffs.

Surprise #10: EM local bonds strike back. EM local outperforms materially in 2025. Material USD weakness sees EMFX trade very strongly. Long-end EM local currency bonds with high real yields benefit the most: Brazil, Mexico, Indonesia, and South Africa.

… The U.S. 10-year yield, which crossed 4.5%, remains a global standout. It is welcome that we finally have a yield curve with a positive slope. The normal term structure of interest rates could suggest the 10-year nominal bond at 100 basis points above the Fed Funds, which would currently imply a 5.3% 10-year yield. This adjustment is likely to continue normalizing with more Fed cuts and some pressure higher on the long end of the curve.

These elevated rate levels explain the ongoing strength of the dollar, which has neared parity with the euro in recent weeks. While this makes U.S. bonds increasingly attractive, it also exerts pressure on foreign economies that struggle to match the returns offered by U.S. sovereign debt. Nevertheless, a strong dollar, coupled with potential tax cuts and regulatory relief under a pro-business administration, continues to draw capital into U.S. markets.

The equity market, however, to date shows no signs yet of a definitive rotation from “growth” to “value”. After years of growth stock dominance, led by the so-called "Magnificent Seven," we may see a shift in 2025. The Fed’s “hawkish pause” triggered a pullback in momentum-driven names, with Tesla, in particular, facing notable profit-taking.

I expect broader market gains in 2025 to be more modest than 2023 or 2024, with the S&P 500 likely delivering returns in the 0-10% range, and a dip can’t be ruled out. Growth sectors may face headwinds from rising rates, and I can see a case where they are down 10%, while small-cap and value stocks, especially those tied to domestic production, could see a relative boost and have returns from 5-15%. However, all 12-month predictions come with a large standard error…

… from the professor TO the doctor … Dr Bond Vigilante weighin’ in …

Yardeni: Bond Vigilantes Pushing Back Against Reckless Monetary & Fiscal Policies

The 10-year Treasury bond yield is up 100bps since the Fed started lowering the federal funds rate (FFR) by 100bps on September 18 (chart). Even the 2-year Treasury yield is up about 75bps. We warned about this happening back in August. The Bond Vigilantes are sending a loud warning message. They aren't convinced Donald Trump, the new sheriff coming to town, will maintain fiscal law and order any better than the old sheriff. They are also losing their confidence in Jerome Powell, the deputy in charge of monetary law and order.

We still think that the 10-year yield should trade around 4.50% plus/minus 25bps in 2025. But we can't rule out a move back up to last year's high of 5.00% early next year (chart). That's another reason why we expect a stock market pullback/correction that might have started already. The S&P 500 peaked at a record 6090.27 on December 6…

… And from Global Wall Street inbox TO the WWW and a few curated links readily available to one and all …

First up, NYC econ (and so, a reflection of GLOBAL TOURISM ?) remains strong …

The average daily rate for a hotel in New York is at a record-high of $417, see chart below.

… technical hot take on Buffet’s indicator

AllstarCharts: The Buffett Indicator Flashing Signals

You may have heard by now. The so called, "Buffett Indicator" is flashing what we're being told are "warning signals" of an imminent market collapse.

It is the "Buffett Indicator" after all. And Warren Buffett is one of the all-time greats.

But let me fill you in on a little secret. The only people who actually care about this ridiculous excuse for a "market gauge" are journalists writing their glorified gossip columns and charlatans trying to do their best to scare you.

That's it.

They claim that the "Buffett Indicator" is this magical signal based on a ratio between the total market-cap of U.S. stocks relative to U.S. GDP.

It's so hilarious that even Charlie Munger came out and said that,"Just because Warren thought of something 20 years ago doesn't make it a law of nature. There is no natural correlation between GDP & Corporate Profits"

The "Buffett Indicator" is not a thing. Not even the guy who it's named after thinks it's relevant.

Meanwhile, here's a chart of Berkshire Hathaway chugging along in a strong uptrend making higher highs and higher lows.

But then why does Berkshire have so much cash? Doesn't that mean the market is going to crash.

Again, that's what the journalists want to write about. They think it's going to attract readers, no matter how much it hurts them. It's also exactly what the permabears want you to believe.

But nope.

Once again, Warren's high cash levels are historically great buying opportunities.

The last time Berkshire had this high percentage cash in its portfolio, the stock market immediately went on to have the greatest 52-weeks in American history. The time before that, the bull market in stocks lasted for 3 more years. The lowest percentage cash he's had at any time over the past decade is right when the S&P500 peaked at the end of 2021.

You're welcome to sell all your stocks. But I would encourage you to have better reasons to do that than a made up indicator that Uncle Warren doesn't even care about. His cash levels are a poor excuse for selling stocks as well, they have been for several quarters now...

I'll tell you when it's time to be running to cash. And it certainly hasn't been over the past couple of years. Any dip has been an opportunity to buy. One day that will change. And I'll be right here talking about it…

… CHARTS! I like charts and so here are 25 for ‘25 …

…2. The Fed managed to out-hawk the markets in the final FOMC meeting of the year, with futures pricing for 2025 cuts becoming a lot shallower. Yet expectations of trying to predict the Fed has rarely been accurate.

…8. Debt ceiling headaches are a short-term theme to carry over into January, but whether the fiscal problems remain a story for 2025 remains to be seen. One thing is for sure, the net interest payments are starting to add up (even with the GDP growth and yields relatively stable).

….21. Bond yields have surged since mid-September, with the 10-year yield rising from about 3.6% to 4.4%. This sharp increase is expected to dampen economic momentum in the coming months despite the Fed easing. Historically, there has been an inverse relationship between the U.S. Economic Surprise Index and the 10-year Treasury bond yields. The surprise index has fallen from +45 to +10, and if current trends continue, it could drop to around -10 by March.

… AND with rates UP was only matter of time until vigilantes become more popular …

Bloomberg: Bond Vigilantes Are Putting Governments on Notice

Yield increases show that investors are closely watching whether advanced economies have the ability to deal with high debt and rising borrowing costs.

…As part of the general move up, the US 10-year Treasury yield, a global benchmark, rose by 0.75 percentage point during the year to 4.63% last week, near its 2024 high of 4.70%. Only the UK came near the US, with its 4.63% yield having climbed by a more dramatic 1.10 percentage points despite considerably weaker growth dynamics and less intense inflationary pressures…

…The factors that contributed to these unexpected and, in some cases, unusual developments go well beyond changes in expectations for growth, inflation and monetary policy in two interrelated ways. This is particularly true for Europe.

First, bond markets have become more sensitive to debt dynamics, whether that’s high primary budget deficits or the self-reinforcing impact of higher borrowing costs on deficits and debt levels. This is most visible in productivity-challenged countries whose ability to grow out of debt faces stronger headwinds. Indeed, some have labeled 2024 as ushering in the return of “bond vigilantes,” a term that was widely used in the 1990s but was largely forgotten after that except for a limited time in 2012-2014 during the euro zone debt crisis.

Second, bond markets have been paying greater attention to domestic political developments. This is most apparent in the euro zone, where we’ve seen a dramatic reversal of the conventional wisdom of the past decade. This year, the market took note of the political instability that frustrated economic reforms in France, a core country, as well as the higher growth and budget calm enabled by a well-functioning government in the peripheral economy of Greece.

This greater focus on debt and political stability is likely to continue into 2025, as will the extent of dispersion between the US, euro zone and Japan. For investors, this is likely to impart both rate and currency volatility to what has otherwise become a more attractive environment for the sleep-at-night “carry trade” that can anchor a diversified portfolio with significant equity and credit exposure…

… up next are a couple where auther looks back and predicts the future w/precision …

Bloomberg: Trump Trades windfall for Hindsight Capital in 2024

Hindsight Capital LLC …With all that settled, here are the Trump Trades that Hindsight made on Jan. 1, in dollars (unless otherwise indicated).The charts, drawn up by Elaine He, show the percentage return on each trade, and have been updated to the close of play on Dec. 20.

Bet on Trump Himself Buy Polymarket Donald Trump for President Futures (Up 146%) …

Bet on Crypto Buy Bitcoin (Up 144% in Dollars, 192% in Brazilian reais) …

The Border Wall Trade Buy US Stocks/Short Mexico Stocks (Up 64%) …

Elon Shifts the Balance of Trade Long S&P 500 US Carmakers/Short MSCI Europe European Carmakers (Up 95%)…

China’s Problems Drive the Metals Market Buy Gold/Short Qingdao Chinese Iron Ore Futures (Up 76.3%)…

Bloomberg: Hindsight Capital 2024 Part II: World in Turmoil

… Boosting the Immaterial World Buy the Magnificent 7/Short Oil Drillers (Up 148.5%) …

Europe’s Fracturing Core Buy 5-Year Insurance Against French Default/Sell 5-Year Insurance Against a German Default (Up 101%)…

Brazilian Money Illusion Relocate to Brazil: World Stocks Up 51% in Reais, S&P 500 Up 60%…

The Beans Bonanza Buy Cocoa Futures and Short Soybeans (Up 242%)…

The Southern Core Buy Argentina Merval Index/Short Brazil Bovespa Index (Up 182%)…

…Bonus Trades Ominous Trade, If Only Hindsight Was Allowed to Lever Up: Long Chinese Government Bonds/Short JGBs (Up 20%) …

Buy When There’s Blood in the Street: A Tragic Way to Profit from War in the Middle East Long Bloomberg Israel Index/Short Al Quds Palestine Index (Up 58.2%)

STOCKS for the long run …

Kimble: Russell 2000 At Important Risk-On vs Risk-Off Crossroads!

… unless they are coming off a BIG year with loads of NEW HIGHS??

at subutrade

The S&P hit 57 all-time highs in 2024.

Only a few years topped 50 all-time highs: 2024, 2021, 2017, 2014, 1995, 1964, 1961

Historically, the S&P tends to struggle in the next year, especially in Q2. 2025 will be very different from 2024!

… dart throwing contests remain OPEN apparently … here’s a note from a well respected shop (which isn’t really going too far out on a limb) …

Morningstar: 2025 Bond Market Outlook: Yields Range-Bound but Volatile Sticky inflation, healthy economy could add up to a back-and-forth bond market.

… When it came to performance, 2024’s roller coaster has led to muted returns. The Morningstar US Core Bond Index—which tracks a mix of investment-grade government and corporate debt—is up just north of 1% in 2024, which followed a 5.3% gain in 2023. These positive but small gains come after bonds were hammered in 2022, with the core bond index down 13% in 2022 as the Fed jacked up rates to stamp out surging inflation…

… AND Jimmy Ps in the house with a slowing econ (so, BULLISH BOND) note …

Several economic & stock market Indicators are now suggesting a meaningful slowdown in real GDP growth during 2025. What does this imply for the stock market?

The Federal Reserve recently slowed its easing campaign because of concerns the pace of economic growth remains too strong, and inflation may again be lifting. Bond investors ostensibly have similar worries as the 10-year Treasury Yield surged to 4.63% last week. Although policy officials and investors appear increasingly anxious about the potential for overheated economic growth, I think the more likely outcome for 2025 is an unexpected economic slowdown.

Lagged Impact of Economic Policies Pointing to Weaker Economic Growth

As shown in chart 1, the U.S. economic surprise index (shown in blue) has already moderated significantly in recent weeks declining from a high of about 45 in mid-November to about 3 last Friday. The Citi Economic Surprise Index measures economic releases during the month relative to market expectations. A rise in this index means economic reports have been stronger than expected while declines indicate that economic momentum is trending weaker than expected.

Since 1970, the Fed has frequently began easing even though the CPI Inflation rate was rising. They should do so again today.

… As the accompanying chart shows however, since at least 1970, the Fed has often – indeed usually -- “eased into a rising inflation rate”. Of the 8 major easing cycles since 1968, during 5 of these previous cycles, the Fed began cutting the Funds rate only to see the annual rate of CPI Inflation accelerate. Sometimes these were fairly aggressive inflationary accelerations – e.g., 1974, 1980, 1990, and 2008. Despite easing into rising inflation, the Fed did not pause nor slow their easing campaigns during these past cycles as they have today. Fortunately, they kept easing because in every case during these previous 5 cycles, the economy ultimately headed into a recession despite ongoing Fed easing.

The most recent uptick in the annual rate of CPI inflation can only be seen in the accompanying chart if you squint with a magnifying glass. The current annual rate of inflation has increased to 2.7% in November from 2.4%. However, the CPI rate is still decelerating form July when it was 2.9%. The SPGSCI U.S. Commodity Price Index is off by almost 35% from its highs in mid-2022, both gasoline and crude oil prices are nearing a 3-year low, and the Atlanta Fed Wage Growth Tracker continues to steadily decelerate from its highs in early-2023. The 10-year Treasury Bond Yield has risen by more than 90 basis points since mid-September, the real trade-weighted U.S. dollar has spiked by more than 6% since September and is close to its all-time record high in 1984, and the annual rate of growth in the M2 money supply is only 3% which is 2% less than the rate of nominal GDP growth! Seemingly the Fed is currently being spooked by a nonexistent runaway U.S. inflationary problem. The Fed needs to give up the post-pandemic inflation ghost and see if they can keep the economy out of a recession.

The U.S. Citi Economic Surprise Index has recently dropped from about 45 in mid-November to only 10 currently and appears to be headed negative in the coming month. The current real Fed funds rate is still 1.6% compared to its average since 1960 of only about 1%. As it has during the previous 5 cycles when it began easing while inflation kept rising, the Fed should currently keep lowering the Funds rate. This time, if the Fed does not pause, there is a good chance a recession can still be avoided.

… Wolf weighed in …

WolfST: 10-Year Treasury Yield Rose 100 Basis Points since September as the Fed Cut 100 Basis Points. Why the Historic Divergence?

Treasury Yield Curve Steepens. Bond Market a Wee Bit Nervous?

WolfST: Who Bought and Holds the Recklessly Ballooning US National Debt, even as the Fed is Unloading its Treasury Securities?

A hot question for an iffy situation. So here are the holders as of Q3.

… finally, a couple from ZH …

ZH: Fed's Favorite Inflation Indicator Holds At 7-Month High

ZH: Dove-Driven Dead-Cat-Bounce Fails To Save Bonds, Stocks, & Crypto In 'Bad Data' Week

AND … I’m back. Nothing tomorrow but will be back in the new year (ie Thursday morning) and so, THAT is all for now …

Happy New Year, to all !!!

https://youtu.be/jbCMHZQPIOE?si=qyS5VSh_RLVfOU3q

BREAKING: IDF Destroys UNDERGROUND Iran Missile Site; Hamas Makes LAST STAND In Gaza | TBN Israel

This is an excellent source for news on Israel and the Middle East...