while WE slept: USTs lower on light (hol) vol; Global Wall is, 'softening the SOFT LANDING f'cast'; others say 'FCI driven surge in growth means ... yields movin' on up; supply creates demand

Good morning … yesterday morning after hittin’ SEND, I tweeted how TLINE was turning YELLOW (ie caution warranted?) and it was after BARKIN (v) was barkin and claims … SOME context and snark

BonddadBlog: Initial jobless claims confirmatory of continued expansion CalculatedRISK: Weekly Initial Unemployment Claims Decrease to 218,000 ZH: Despite Mass Layoffs, US Jobless Claims Declined Last Week ZH: *BARKIN: DON'T HAVE TO BE IN ANY HURRY TO CUT RATES ZH: BARKIN: I AM CAUTIOUS ABOUT ACCURACY OF NUMBERS AT THE TURN OF THE YEAR

… and this all set the table for what was … a really GOOD auction (?) …

ZH: Stellar 30Y Auction Sees Surge In Foreign Demand, Biggest Stop Through In 13 Months

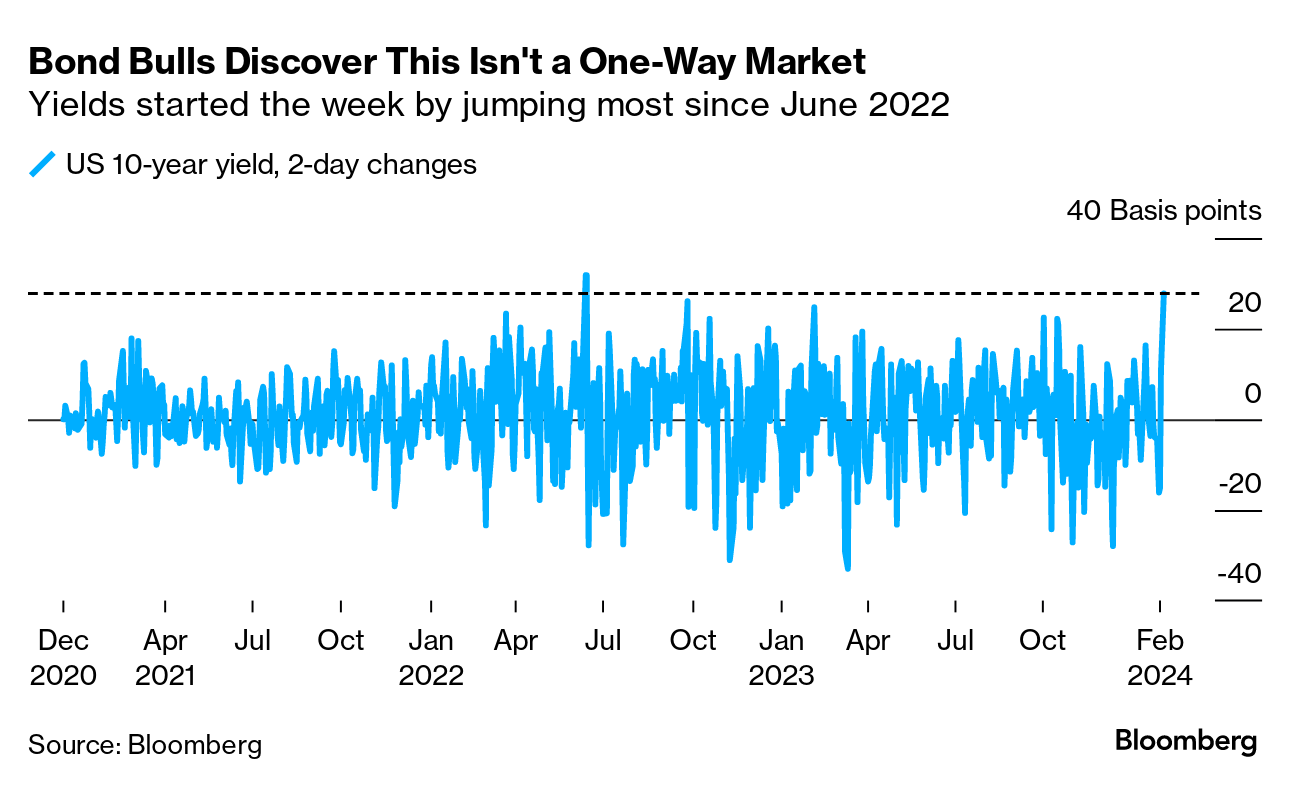

… and so here we are with 10yy closing LAST week in / around 4.02% and now are UP approx 15bps on the week …

… watching, as always, for somewhat longer-term WEEKLY context, this afternoons close — far more important than where we are here and now BUT the wheel here looks to be in motion … for somewhat more of the (weekly fix) context see LINK BELOW with this visual …

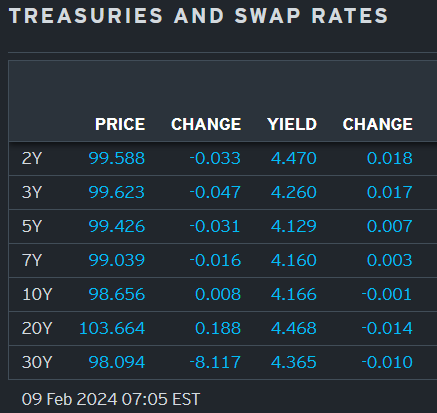

AND … here is a snapshot OF USTs as of 705a:

AND with aggressively UNCH prices in mind… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are just a touch lower amid little new news (Lunar New Year so much of Asia shut) and ahead of this morning's seasonal factor revisions to CPI that the Fed's Waller recently flagged. DXY and front WTI futures are each little changed too. Asian stocks that were open were little changed, EU and UK share markets are mixed while ES futures are showing +0.13% here at 6:35am. Our overnight US rates flows were predictably quiet with London seeing selling from systematic names alongside fast$ interest in 5s30s steepeners. Overnight Treasury volume was weak at ~65% of average (2's just 41% of ave turnover today).

… and for some MORE of the news you might be able to use…

Newsquawk: US Market Open: Equities marginally firmer, NZD bid and Crude remains at highs ahead of US CPI Seasonal Revisions … Bonds are around flat awaiting US CPI Revisions, German & UK 10yr yields notched fresh YTD peaks

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … ATTN K-MART SHOPPERS: another day and another WEEK comes to a close, another on Global Wall is out with an ‘updated’ (NOT as soft a soft landing as was previously f’cast … read on)

BARCAPU.S. Equity Strategy: Food for Thought: Are Earnings or Valuations Driving the Rally?

With 4Q23 results mostly in the books, NTM estimates are on the up and up. Upward revisions are driving higher valuations, which are most visible among Big Tech and their cohorts. SPX ex-Tech has actually seen no multiple expansion YTD, leaving some sectors more attractively valued vs. forward earnings.

DB: Updated US rates outlook - softening the forecast (marking f’cast to market keeping in mind, f’casts which were written in what, NOV, rewritten before years end then now 2mos in being UPDATED … )

We recently published a US rate forecast under an alternative soft-landing scenario, noting growth has remained strong, the labor market has continued to rebalance without a material rise in unemployment, and inflation has fallen rapidly. Earlier this week, DB’s US economics team updated their economic forecast to a soft-landing, highlighting these favorable dynamics along with easing credit and financial conditions, rising real incomes, and improving consumer and business sentiment.

In light of the evidence, our assessment now is that a soft-landing is more likely than not. Accordingly, we adopt it as our baseline and update our rate forecast.

The key features of our updated forecast are: (1) a path for inflation and unemployment that leads the Fed to cut at a measured pace back to but not below neutral, (2) a neutral nominal funds rate of 3.25-3.5%, above survey forecasts but in-line with market pricing; and (3) a rise in term premia from current low levels.

Relative to forward pricing, our forecast for yields out to 5y are in-line while forward rates and spreads further out the curve are moderately higher and steeper, respectively, driven by the expected increase in TP. The logical expression of the forecast – which we emphasize is a modal projection and doesn't account for upside/downside risks – is to pay term premia, pay far-forward rates, be in long-end steepeners, and receive the belly of the curve on the fly…

… With regards to those US CPI revisions, even though it might seem a bit technical, it’s something that could have pivotal implications for markets. In summary, new seasonal adjustment factors are coming out, which will be used to revise the last 5 years of CPI inflation data. Last year, they showed that inflation was proving more persistent than thought in late-2022 (lower in H1 22), with the 3-month annualised rate of core CPI revised up from 3.14% to 4.25%. So that complicated the near-term inflation picture for the Fed, and contributed to a sharp rise in Treasury yields around the same time. This is something the Fed are watching, and Governor Waller explicitly mentioned these revisions in his speech last month, so it’ll be an important one for the timing of any rate cuts. I don’t think there’s any analytic reason to believe the bias will continue to favour higher H2 inflation over H1 but the market is a bit nervous after last year that the same seasonal adjustment pattern could repeat. Remember also that we’ve then got the January US CPI print on Tuesday, so this is an important few days ahead for inflation…

We think core CPI decelerated to 0.26%M in Jan-24 (vs 0.31%M Dec-23, 0.3%M cons), bringing the annual rate to 3.7%Y. Core services inflation moves sideways and goods decelerate due to weak used cars. Energy prices drop bringing headline to 0.14%M (2.9%Y, Headline CPI Index NSA: 308.023).

… As we show in the chart below comparing the series with pre-Covid implied seasonality versus the current published data, the published series trended higher in the final months of 2023, as it did in 2022. With our estimates of pre-Covid seasonality, initial claims declined to 214K, while continuing claims increased to 1836K.

The calendar is quiet. The recent pattern of data deluge then data desert is unhelpful. In an increasingly complex world, overworked economists need time to examine the details of numbers to judge if they are reliable. Gaps in the calendar allow markets to speculate on irrelevant topics…

…US consumer price inflation is revised—especially exciting for economists who wrote a book on inflation. (Widely available. Ideal Valentine’s Day gift). However, revisions mainly change seasonal adjustment patterns, and seasonal adjustment by definition distorts economic reality. These revisions do not change US consumers’ past inflation experience…

Pushback Pain Bonds endured yet another rough week as central bankers from Sydney to London to Washington — and a range of points in-between — pushed back persistently against bets on a rapid pivot to interest-rate cuts. A lot of the damage came at the start of the week, when Treasury yields had their biggest two-day spike since last June, which was just before the Federal Reserve carried out its first three-quarter point hike in almost 30 years. This time the move was driven by the apparent end to bets that the first rate cut would come in March. The stunning January payrolls beat, and Fed Chair Jerome Powell’s prime-time interview, forced traders to slash wagers on a March cut to under 20% from 50% odds seen in late January.

The rout was the latest episode where bond bulls were forced to rapidly retreat from long positions. It also gave fresh life to the US dollar, which surged to its highest level since November.

Carlyle Group Inc. Chief Executive Officer Harvey Schwartz’s warned that investors shouldn’t bet on a slew of five rate cuts this year when the Fed is likely to only deliver two or three. Bill Gross said the better move would be to bet on the interest-rate curve returning to a more normal pattern, eliminating its persistent inversion.

Bloomberg(via ZH): Surprising (FCI-Driven) Surge In Growth Means Yields Are Going Up

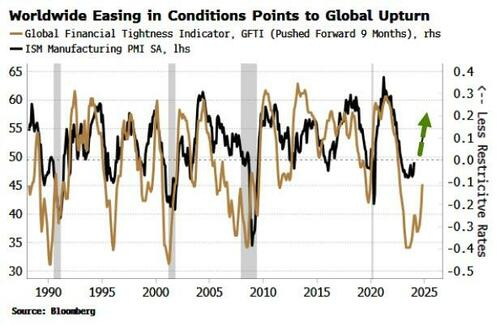

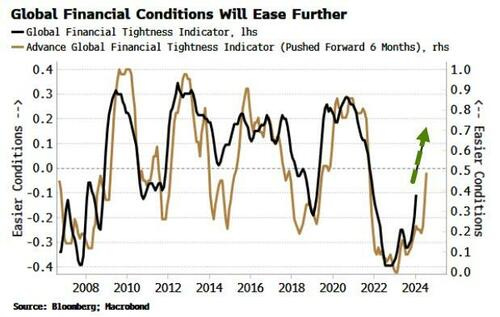

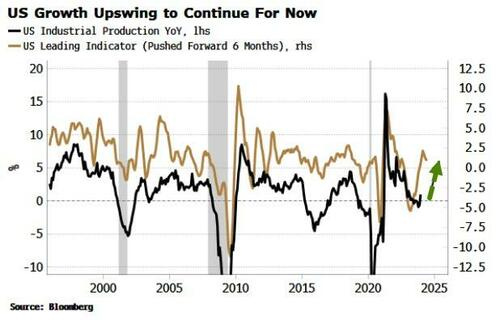

… It’s not just a US phenomenon. Global central banks reached their peak rate restrictiveness last summer. First, banks in the aggregate stopped hiking, then some started cutting. The Global Financial Tightness Indicator (GFTI) shown below — essentially a diffusion of central-bank rate hikes — captures this and is now clearly easing. That points to a continued rise in the US manufacturing ISM, itself a highly reliable indicator of a cyclical upswing in the global economy.

There’s more to come. The easing captured by the GFTI should continue for the time being, given that the Advanced GFTI — based on rate cuts anticipated by futures prices — leads the GFTI by about four months and is also heading higher. These are all highly reliable ex ante indicators of the nascent rise in global growth we see today.

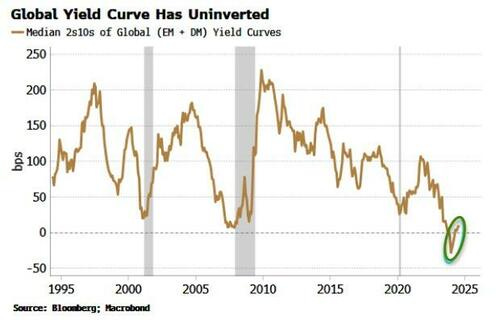

Looser conditions can also be seen in the recent disinversion of the global yield curve. Globally, shorter-term yields are no longer higher than long-term yields. Yield curves are likely to maintain their steepening trend.

The widespread easing in financial conditions is fueling a growth upturn in the US and around the world. The US leading indicator highlighted in October pointed to a fledgling upswing in growth. The indicator has started to turn lower, but from a relatively high level, signifying the growth upturn should persist for another few months.

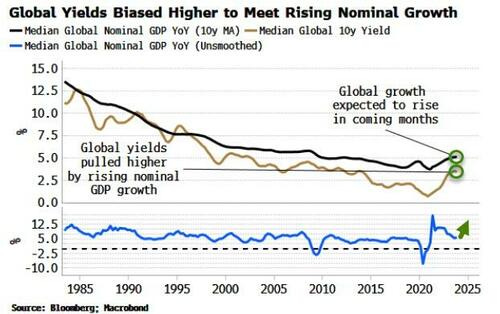

… Rising global growth and a likely re-acceleration in inflation means nominal GDP should rise, acting as a ineluctable pull higher on global bond yields, especially while the risk of an imminent US recession remains low.

An inflation revival later in the year is also likely to catch central banks – who have turned prematurely dovish – off-guard, leaving yield curves more prone to bear steepening.

The Fed, ECB et al are at risk of cutting rates right around the time inflation rears its head again. Fear of flip-flopping will make them less likely to reverse direction and hike rates aggressively, increasing the chance policy rates lag inflation-sensing longer-term yields.

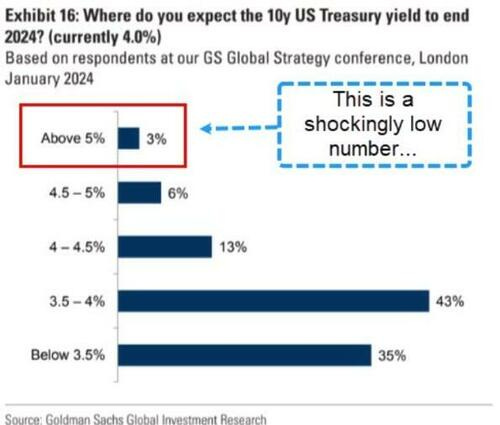

Higher yields, as exemplified by the outlook for the US, are anticipated by only a small proportion of professional investors.

Source: Goldman Sachs …

… PAUSE … how can I NOT mention it makes me think of …

… ok I feel better … continuing on with the WWW …

Bloomberg: 5 things to start your day: Europe (supply creates demand …)

… Treasuries should be able to digest rising amounts of supply without upwards pressure on yields.

A solid, record-sized 10-year sale Wednesday is the latest evidence of that. And Treasury Secretary Janet Yellen said that she sees no near-term threat of a mounting debt load causing investors to spurn the securities.

The chart below shows how a rapid increase in supply of the US marketable debt hasn’t stopped yields from falling over most of the past 40 years. The trend was snapped recently, but the latest rise in 10-year yields coincided with a surge in inflation that led the Federal Reserve to hike rates at the fastest pace since former Chair Paul Volcker in the early 1980s. That suggests it’s inflation and Fed policy — not supply — guiding yields at the moment.

Long-term demand for Treasuries should be kept alive by forecasts of muddling economic growth, coming Fed rate cuts and demand for haven investments from retiring Baby Boomers.

This week’s edition of “Three on Thursday” looks at where short-term interest rates in the U.S. could be heading in 2024. Inflation has continued to trend down, while unemployment has remained low and the economy has continued to grow, meaning rate hikes are a thing of the past. Chairman Powell, in the January U.S. Federal Reserve (Fed) press conference, mentioned that the incoming data aligns with the Fed’s criteria to initiate rate cuts. However, the Fed remains cautious, desiring an extended period of lower inflation to bolster confidence in achieving their 2% inflation target. With Chairman Powell all but ruling out a March rate cut, attention now shifts to when the Fed will commence cuts and how many cuts will unfold throughout the year. There exists a significant gap between the market’s expectations and the Fed’s projections for the number of cuts. To gain a little more context, we present the three tables and charts below…

… In our view, the FOMC’s median projection of three rate cuts in 2024 aligns with their overall economic outlook, indicating a trajectory toward a soft landing without a recession. However, the market has also embraced this soft-landing scenario, but anticipates five rate cuts this year. Notably, just before Chairman Powell’s press conference last week, the market anticipated six cuts with the first starting in March. Current expectations point to the first rate cut in May. If the economy remains healthy and keeps growing, it is very hard to imagine the Fed cutting short-term interest rates by the 125 basis points the market expects. We believe the Fed will cut interest rates six times this year, but due to a (mild) recession while inflation continues to decline.

AND with the RTRS morning bid visual of CRE loans in mind, another visual take

AND I’m done. Don’t forget to tip your waiters. Unsure of any production schedule this weekend as it’s Thing 3s bday on superbowl Sunday! Lots to do but will try. Have a GREAT weekend and … THAT is all for now. Off to the day job…

I'm starting to jive w/the Doug Casey/Jim Ricards mantra that we've been living in Greater Depression 2.0 since at least 2008-09 GFC. The tent-cities are rather rampant here in CA. 21st century 'Bidenvilles'? Ok that's not fair those truly got started post GFC....'Obamavilles' anyone? I'm rather confident the public school/Amazon/FCC approved textbooks will claim Orange-Manvilles....

At Walmart yesterday, a 1-pd pack of Blackforest sliced ham is $5.96, WAS $3.23 in 2021, that's over 18% annualized hamFlation, far surpassing CORE CPI or Truflation or WTF WHATEVER, but hey there's been a bumper corn crop in 2023 the big party bag of Doritos is down 60 cents so all is well if the latest 'booster' doesn't harden my arteries then Doritos will oh YEAH! Thanks everyone rant done go Chiefs enjoy the Big Game!!!

{kind=link}

{kind=link}

I'm starting to jive w/the Doug Casey/Jim Ricards mantra that we've been living in Greater Depression 2.0 since at least 2008-09 GFC. The tent-cities are rather rampant here in CA. 21st century 'Bidenvilles'? Ok that's not fair those truly got started post GFC....'Obamavilles' anyone? I'm rather confident the public school/Amazon/FCC approved textbooks will claim Orange-Manvilles....

At Walmart yesterday, a 1-pd pack of Blackforest sliced ham is $5.96, WAS $3.23 in 2021, that's over 18% annualized hamFlation, far surpassing CORE CPI or Truflation or WTF WHATEVER, but hey there's been a bumper corn crop in 2023 the big party bag of Doritos is down 60 cents so all is well if the latest 'booster' doesn't harden my arteries then Doritos will oh YEAH! Thanks everyone rant done go Chiefs enjoy the Big Game!!!

A Thing bday + SB party sounds like good times!