Good <China DEFLATION (goin’ global? notsofast) and Japan REflation> morning …

A funny thing happened to those betting on a reBOUNCE in China (PPI) flation…

CNBC: China producer prices dip in January for a 16th month; consumer prices see biggest drop since 2009

Reuters: China's consumer prices suffer biggest fall since 2009 as deflation risks stalk economy

… nobody actually bets on that, right? They may, on the other hand, ‘bet’ on idea we will be importing Chinas de / disinflation (UBS does NOT believe this to be the case … see below for more on THAT …)

In OTHER ‘good’ news overnight, the BoJ weighs in …

Reuters: BOJ rules out rapid rate hikes, signals ending risky asset buying

… so not an imminent rate HIKING cycle feared at least not any time soon … STILL this should and will remain ON the collective radar screen.

Attempting to bring this back home, there IS a liquidity event (30yr auction) later on this afternoon and so …

#GotBONDS …?

We can only HOPE (NOT a strategy) this afternoons long bond auction goes as well as 10s went …

ZH: Record Large 10Y Auction Sees Stellar Demand, First Stop-Through In 12 Months (better than good…at least it would appear)

… and after yesterday's mediocre 3Y refunding, there were some concerns that the sheer size of today's issuance could lead to severe market indigestion.

Those fears proved to be unfounded because moments ago the Treasury announced that the record amount of 10Y debt sold in a very strong auction, which priced at a high yield of 4.093%, up from 4.024% last month but stopped 1.2bps through the 4.105% When Issued. That was the first stop through for 10Y paper in a year, or since February, excluding the on the screws Sept 23 auction.

The bid to cover was also solid, and at 2.56 it was above the 2.52 six-auction average if below last month's 2.56, which in turn was the highest since Feb 2023.

The internal were even better, with Indirects awarded 70.1, the highest since last August, and solidly above last month's 66.1. And with Directs taking just 16.1%, the lowest since February 2023, that meant Dealers were left holding 13.0% of the auction the lowest since August ..

… Well THAT there is good news and so there’s demand (as long as there’s financial strife bubbling below the surface) and this afternoons REAL test of said demand for duration — well ahead of the next CPI (Tues) — certainly can and will flex influence on equity markets … IF it’s <good / bad > enough … please choose one which you desire.

Before I continue (and perhaps I won’t), lets have a look at the charts of long bonds …

… 10yrs of long bond yields, DAILY with momentum swinging from overBOUGHT to now, nearly overSOLD which brings yields TO levels which must HOLD … a break of the (green)TLINE and we are likely to see some additional UPSIDE in yields … Let the auction decide …

… And as far as WHO may be ready / willing / able buyers OF duration …

Hedgopia CoT: Large specs’ net shorts in 30-year bond futures ↑ 6.6% w/w to 3-week high, 18 weeks ago highest since Nov ‘20; 30-year yield ↓ 16bps

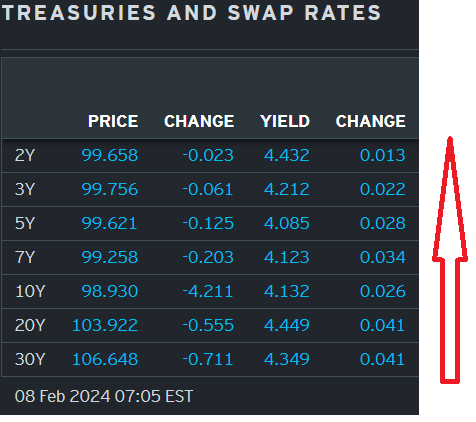

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly lower with the curve a hair steeper (same as yesterday at 7am) ahead of claims and a bond auction. DXY is higher (+0.15%) while front WTI futures are too (+1.0%). Asian stocks were mostly higher, EU and UK share markets are mostly higher (SX5E +0.5%) while ES futures are modestly lower at 7am (-0.15%). Our overnight US rates flows saw Treasuries try to keep pace with rallying JGB's (Uchida said big rate hikes unlikely after exiting NIRP) but fast$ sellers of intermediates has USTs on the lows into the London crossover. In London's AM hours, Treasuries drifted lower in quiet conditions with net selling out the curve from systematic names alongside continued real$ demand for the front-end. Overnight Treasury volume was quite weak at ~65% of average across the curve.

… We've relented this morning and dared to post a few freshened-up pics of duration benchmarks amid the ongoing ranges. The chart of Treasury 2yr yields is worthy of note because 2yr yields have recently shown respect for the bull trend in place since the move highs in 2y yields back in October. Short term momentum is drifting upward toward 'overbought' readings and the ~4.14% to 4.48% range is holding serve still even as 2's have worked off a severe overbought condition (too many longs) seen at the start of 2024. For the front-end longs, a break and daily close above the still-in-place-and-valid bull trendline (4.45% today) should be warning #1 while a close above 4.48% might be a tactical DEFCON #2 as we'd not be surprised to see 2y yields move swiftly toward the 4.70% area (mid-December high yield closes/openings) on such a support breech. Something to keep back of mind with 2's currently doing nothing wrong whilst holding supports where and when they should... It's always good to know where the exits are…

EXITS NOTED … and for some MORE of the news you might be able to use …

Newsquawk: US Market Open: European bourses firmer & US equity futures are flat, JPY softer after BoJ speak; US IJC & Fed speak due … Bonds are modestly weaker with specifics light into a US 30yr auction

Finviz (for everything else I might have forgotten …)

… Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … did NOT notice there are longs (MS) and some shorts (CoT above) in the long bond … interesting and away we go …

US 10y yields: Yields are increasingly looking like they are settling into a range between 3.79% (December 27 and February 1 low) - 4.20% (Jan 19, January 25, February 5 high, double bottom neckline and psychological resistance).

Why it matters: Both support and resistance looks strong with two touchpoints at the support and resistance. Given the strength of both, we think we are likely to trade within the range in the short term.

But be careful of higher yields: Slow stochastics indicators on both the daily and weekly chart show modestly rising momentum. That leaves yields with a slight chance of a break higher - with subsequent resistance at 4.29% (December 11 high). We also look for any weekly break above the 4.2% handle, since that is the neckline for a double bottom formation that would suggest an extended rise in yields.

Technical indicators:

Two touch points at resistance and support, with both levels being strong: 3.79% (December 27 and February 1 low) - 4.20% (Jan 19, January 25, February 5 high, double bottom neckline and psychological resistance).

Uptick in momentum (slow stochastics)

Potential double bottom formation

OTHER TECHNICAL DEVELOPMENTS WORTH NOTING US 2y yields: Yields have bounced off resistance at 4.48% (Jan high). While we also broke above the neckline of a double bottom formation at 4.42%, we note that we have not seen a weekly close above. For now, we think the range is 4.12% to 4.48%…

DB: January employment: A lot of jobs doing less work (sometimes a headline DOES truly grab you …)

… On balance, the details of the report were largely positive and point towards continued momentum in the labor market and increased likelihood of a soft landing. Even the breadth of job gains, which we have highlighted as being relatively narrow in 2023, expanded out beyond just private education and health services and leisure and hospitality, with every major industry contributing positive job gains except mining and logging. In fact, the one-month, three-month, and six-month diffusion indices all ticked up.

… Breadth of employment gains improved as the 3-month diffusion indexed rose in January

Continue to sit in the relative safety of the money markets or take the plunge into bonds? That’s the big question for bond investors today…

…The bond market provides investors and other market participants the choice between investing in short or long-dated maturities, in this case choosing between buying a 12- month Treasury Bill or a 10-year Treasury note. When they commit to one or the other, though, they’ll be cognizant that, like in the show, the opportunity might not arise again.

Bond investors know about opportunity cost, the consideration of alternatives foregone, and reinvestment risk, a function of what’s likely to be available in terms of yield in one year from now. It sometimes helps to consider the macro backdrop and will require a view on where central bank policy rates are heading.

If rates are going to fall quickly then it would be better to lock in the 10-year rate whilst the opportunity is there. Alternatively, those with a view that rates are on hold (or maybe about to go up) will stay with the bills and take the risk of reinvesting in a year from now.

There is information value in what we would do today compared with what we would have done in the past. And to capture this in a useful way we need to avoid hindsight bias and recall context and rationale behind a decision. Readers of this letter one year ago will recall that many investors chose the bills. They were the “soft landers”, or of the view that inflation was still not beaten, thereby requiring rates to go still higher. Those that chose Treasury notes were more likely to be “hard landers”, anticipating a market event or sharp slowdown in the data to justify significant rate cuts …

… Our chart shows that the difference between the two forward yields (right-side axis) puts the 10- year T.Note on top. Given this didn’t happen much recently, for those who like to go against the market, this favours the 10-year note over the 12-month bill. Just saying…

MS: Cross-Asset Playbook: Better Is the Enemy of Good (a few nuggets … morsels of interesting content and I’ll note just a bit…)

Welcome to the Good Place A US soft landing is still our base case, but recent data releases suggest GDP growth can surprise to the upside. While eurozone growth will be sluggish, and downside risks from a weak China recovery remain, the economy is good, which isn’t half bad.

Better Though Is…Bad? But for markets that are pricing to perfection a mid1990s Goldilocks policy pivot, hotter-than-expected macro may be too much to bear for rich valuations. Typically, data surprising to the upside close to an imminent Fed rate change has seen risk assets underperform.

Strategy: OW Fixed Income, for Better or Worse We maintain our fixed income > equities preference. Value continues to be hard to find in stocks, while high grade bonds offer good carry and good convexity; valuations are already cheap if growth heats up, and the asset class can outperform should macro cool significantly…

… Macro Debates | Who Will Buy Bonds?

… Asset Class Views | Global Rates Bullish on US duration; euro area to trade range-bound; neutral on UK

Unusual winter weather, combined with fading fiscal cash flows, leads our strategists to see downside risks to economic data. Growth surprises have sent yields climbing, ignoring progress on inflation. Buy the dip: go long duration in UST 5y…

… Top Trades | Long UST 30Y

UBS: China’s deflation – a local affair (bummer ey? guess we’re NOT gonna import it from there to here so … NO deflation means not nearly as many rate cuts for us? how ‘bout that CBO, now…)

China’s consumer prices have been in deflation since last July (producer prices for far longer). January consumer price deflation was the worst in over 14 years, but this is distorted. The lunar new year is (literally) a moveable feast—occurring in January 2023, and in February 2024. That distorts food price patterns, exaggerating deflation. Nonetheless, deflation trend is indicative of weak domestic demand.

The global impact is minimal. Food prices in Shanghai have no bearing on food prices in Seattle or Stuttgart. China’s consumer price data also reflect China’s pattern of consumption, which differs from developed economy consumers’ spending. The main way China’s deflation could impact developed economies is via the consequences of China’s future policy response.

The US Congressional Budget Office published some alarming projections on future deficits. This has some market relevance as investors can be quite puritanical about debt. However, debt is not automatically bad, and there is no magic level where it creates a problem. Structural changes also mean tax revenues and GDP tend to be higher than projected…

Summary Battle Between the Midwest and the West Coast

The San Francisco 49ers and the Kansas City Chiefs will clash this Sunday in Super Bowl LVIII. This is a rematch of Super Bowl LIV, played four years ago in Miami and won by the Chiefs in a thrilling fourth quarter comeback. The 49ers will look to redeem themselves and recapture the glory of the 80s and 90s when Joe Montana, Jerry Rice and Steve Young wore the red and gold. The Chiefs, the reigning champions, are making their fourth Super Bowl appearance in five years. A win this Sunday would cement Kansas City as an NFL dynasty in the same vein as the Tom Brady-led New England Patriots and the 1970s Pittsburgh Steelers.

This year's Super Bowl highlights the wide variation in economic conditions among different geographies and industry sectors within the United States. The championship will be held in fabulous Las Vegas, a city that has emerged as a premier sports destination recently alongside a sluggish recovery from the pandemic and drop-off in tourism. Compared to historical averages, Kansas City's economy has experienced a relatively hot pace of growth over the past few years, yet conditions now appear to cooling back to pre-pandemic trends. Meanwhile, San Francisco's economy looks to be having a more difficult time digesting higher interest rates.

Although significant economic differences exist, it is safe to say that most residents of these metro areas will be tuning in on Sunday night. So, when the confetti falls, which team will be hoisting the Lombardi Trophy?

… The Road Ends Here When the confetti falls, we expect the Kansas City Chiefs will be at the center of it all. The 49ers have shown grit and prowess in these playoffs, but the proven tandem of Andy Reid and Patrick Mahomes is a partnership that’s hard to bet against. The top seeded 49ers earned a bye in the first round, followed by two close games requiring second half comebacks to win. The Niners offense is stacked with talent and is scoring on par with its regular season average. Questions remain on defense, however. San Francisco was the third-ranked scoring defense in the regular season, averaging 17.5 points against, but has given up an average of 26 points per game in the playoffs. Purdy has proven his ability to lead comebacks, but a stingy Chiefs defense that locked down MVP-favorite Lamar Jackson in the AFC championship game could prove too challenging to overcome. Indeed, the old adage is “defense wins championships,” and the Chiefs defense is playing at a championship level. The Chiefs have given up an average of just 13.7 points per game in the playoffs, improving from their already solid regular season average of 17.3. The Chiefs conquered the Dolphins in the wild card round, followed by two tough road victories against the Bills and the top-seeded Ravens. Although the 49ers are favorites, the Chiefs experience on the biggest stage in football will prove a difference maker, and we expect Kansas City to capture a fourth Lombardi trophy in a 27-21 victory.

… And from Global Wall Street inbox TO the WWW,

ABNAmro: Global manufacturing strengthens as 2024 starts (so, NO rate cuts?)

Global manufacturing PMI rises by a full point in January. Significant improvements in the demand side. Is the recent sharp rise in container tariffs (almost) over yet?

… The pick-up of the global manufacturing PMI in January is in line with our expectation of a bottoming out in global manufacturing this year. Reflecting our growth views for the key economies (US, eurozone, China), ongoing US resilience (see here) and some stabilisation in China (see here ) will help this bottoming out, although all in all we still deem a very sharp rebound unlikely at the moment.

Bloomberg: 5 Things You Need to Know to Start Your Day: Asia (comments on cuts AND visual on stocks and bonds relationship)

… No cuts soon Despite what traders think, four more Federal Reserve officials suggested that they don’t see an urgent case for lowering interest rates at least until May. Governor Adriana Kugler, the Boston Fed’s Susan Collins, the Minneapolis Fed’s Neel Kashkari and Richmond’s Thomas Barkin were all noncommittal on when the US central bank can start easing policy. Investors have pared bets on a March cut and are setting their sights on the Fed’s May 1 meeting. Carlyle Group CEO Harvey Schwartz, who expects two to three rate cuts, warned investors against rooting for five reductions this year. “That would suggest an environment that actually requires a lot of attention from the Fed,” he told Bloomberg TV. “We should be hoping for fine-tuning.”

… Equities keep on climbing even amid geopolitical concerns and bond-market angst spurred by hawkish central bank rhetoric. There’s plenty of scope for further gains — especially with volatile China about to take more than a week off.

For stock investors, a key source of animal spirits is the ending of the most severe hiking cycle for 40 years. While bond traders fret as Federal Reserve Chair Jerome Powell and his peers push back against speculation for rapid rate cuts, what matters for risk assets is that those cuts are coming.

They are far less concerned about the timing — indeed there’s a case to be made that the longer the delay in policy easing the better things will look for equities. A long wait for lower cash rates implies a significantly softer landing for the economy remains in play, while bond traders positioning for cuts helps to ease financial conditions modestly already.

Perhaps expectations for about two rate cuts in the coming six months represent a “Goldilocks line.” Sustained bets on deeper reductions would signal imminent economic pain, while a shift toward no easing over such a time span would act to tighten conditions and bring the strains imposed by a high cash rate back to the fore.

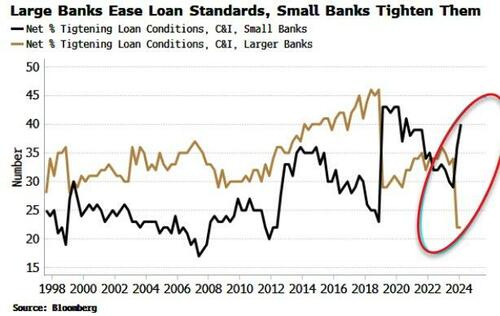

Bloomberg(via ZH): Big Banks Well Placed To Prosper From Smaller Rivals' CRE Distress (shocking precisely NOBODY to hear / read / see this … Jamie Dimon #WINNING)

… C&I loans are generally a conservative benchmark for all types of bank lending, as their standards tend to be the most stringent because the loans are often unsecured.

Here we see a marked divergence, with large banks easing standards for C&I loans, and smaller banks tightening them.

It’s probably fair to infer therefore that it is the larger banks who are easing lending standards for CRE loans and may be in a position to capitalize from small banks’ distress and the low valuations in the CRE sector.

Either way, large banks have started to outperform regional banks, especially since NYCB hit the skids, and it’s likely that trend will continue in the coming months.

[ZH: And as we have noted numerous times, if the large banks don't 'take' share, they will 'buy' share at pennies on the dollar from the FDIC after the small banks fail...]

"We looked at the larger banks' balance sheets, and it appears to be a manageable problem. There's some smaller and regional banks that have concentrated exposures in these areas that are challenged.

...

There will be expected losses.

It's a sizable problem... it doesn't appear to have the makings of the kind of crisis things that we've seen sometimes in the past.

I don't think there's much risk of a repeat of 2008. I also think, you know, we need to be careful about making proclamations about the.. future.

...

There will be certainly be some banks that have to be closed or merged out of, out of existence because of this. That'll be smaller banks, I suspect, for the most part.

You know, these are losses. It's a secular change in the use of downtown real estate. And the result will be losses for the owners and for the lenders, but it should be manageable."

Is NYCB the next canary 'mole' that needs to be 'whacked' by a Fed 'facility'?

I'm starting to view the members of the FOMC in likeness to the 9 Nazgul, although I'd actually prefer The Nine, for they promise immortality (Hell is relative lol) and talk much less. Those FOMC members appear to have been gifted Saruman's guile Tongue :(

I'm starting to view the members of the FOMC in likeness to the 9 Nazgul, although I'd actually prefer The Nine, for they promise immortality (Hell is relative lol) and talk much less. Those FOMC members appear to have been gifted Saruman's guile Tongue :(