… MY view is I’m sympathetic as to the integrity of the institution at this point. MY guess is that he was SENT out here and I’m not as focused on timing (middle of year will make 6 cuts quite unlikely :) ) and his stressing of the price LEVEL not coming down, well, am not sure that was the message he might have been told to convey.

I’m NOT so sure that I would have read as much snark into it as ZH does but then again, that’s what we’re paying them for (?), right?

Still, having a hard time NOT sharing some of the sentiment offered …

ZH: Powell Tells 60 Minutes Fed "Not Likely" To Cut In March, Calls Americans Lazy

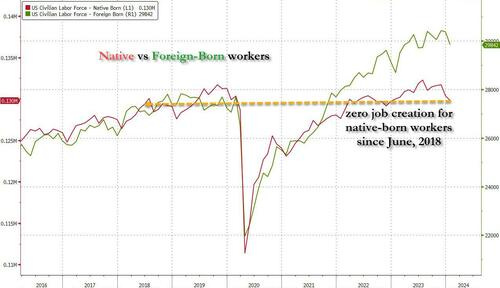

… Finally, we pointed out on Friday that all the job gains since 2018 have gone to immigrants (non-native born workers)...

... and here is Powell defending them:

PELLEY: Why was immigration important?

POWELL: Because, you know, immigrants come in, and they tend to work at a rate that is at or above that for non-immigrants. Immigrants who come to the country tend to be in the workforce at a slightly higher level than native Americans do. But that's largely because of the age difference. They tend to skew younger.

PELLEY: Why is immigration so important to the economy?

POWELL: Well, first of all, immigration policy is not the Fed's job. The immigration policy of the United States is really important and really much under discussion right now, and that's none of our business. We don't set immigration policy. We don't comment on it.

I will say, over time, though, the U.S. economy has benefited from immigration. And, frankly, just in the last, year a big part of the story of the labor market coming back into better balance is immigration returning to levels that were more typical of the pre-pandemic era.

PELLEY: The country needed the workers.

POWELL: It did. And so, that's what's been happening.

Translation: Immigrants (we hope he means legal immigrants here, not the flood of illegal immigrants) work hard, and Americans are lazy.

…Meanwhile, the ‘other interview’ where Trump eludes to perhaps MORE than 60% tariffs on China has led to yet another leg lower in China equities …

RTRS: China regulator vows to stabilise market after stocks hit 5-year lows

… The ongoing meltdown in Chinese equities underscores the challenges both for the country’s economy and for the authorities’ efforts to find a way to stabilize markets. The call over the weekend for a $1.4 trillion support fund may still show a lack of ambition, given that the nation’s market capitalization sank by just over $1 trillion in the space of 13 trading days.

The total value of the nation’s equities dipped under $8 trillion on Friday, from just above $9 trillion on Jan. 16. It is looking rather like the authorities’ hand-wringing about equity declines simply concentrated investors’ minds on the apparent lack of any solutions for the downturn. Indeed, the suggestion that “malicious” short sellers would face a crackdown could have added to existing concerns that market action can be driven more by regulatory whims than economic or earnings fundamentals.

It also could fuel investors’ willingness to sell any rallies that should break out.

… food for thought.

Moving along and in light of this weekend’s views from Global Wall (where one of the sellsides popular kids booked profits in ‘long duration’ via 5s and another sticking with it) AND we’ve got updated MONTHLY charts, I thought not a terrible idea to have a look at 5yy — aka ‘the BELLY of the bond best’ …

… I’ve tried to highlight not ONLY my ‘career’ as defined by 5yr DV01s but also a couple of overBOUGHT extremes that were, IN HINDSIGHT, good times to be short for a medium term trade … Not sure the current bearish crossing of momentum gives as much a quality SELL signal given we’re short of XTREME readings as we’ve had in the past … drilling down a touch and in WEEKLY context …

… breaking recent downtrend (green line) but holding, running in place, if you will. TIME at a price CAN work of overBOUGHT extreme (‘signal or noise’) and only ‘TIME’ will tell BUT I’d be willing to say and with some confidence, booking profits of a long NOT terrible idea and learned in my early years sitting on a desk … NEVER wrong to take a profit (although some of the best traders ever known ALWAYS swung for the fences and incurred HUGE losses along the way … )

This all brings us to here and now where — over the weekend — we learned there are differences OF views(one shop got OUT and another remains long) …

… and it may come down to your timeframe AND that in the fullness of time, BOTH will prove to be right. One thing I can say for sure is that they will always and forever say they ‘told us so’.

Meanwhile … here is a snapshot OF USTs as of 707a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower with the curve bear-flattening after Powell told 60 Minutes that with the US economy strong, the Fed can approach the rate cut timing question carefully (see links above). DXY is higher (+0.35%) while front WTI futures are lower (-0.9%, see attachments). Asian stocks saw weakness in China and mixed outcomes elsewhere, EU and UK share markets are mixed while ES futures are showing -0.2% here at 7:05am. Our overnight US rates flows saw good buying in intermediates from Aian real$ during Asia's 60 Minutes-related dip- with the session seeing very high volumes. During London's AM hours, yields hung out in 'choppy ranges' with buying still evident as 10's near 4.10% again. Most of the buying appeared concentrated in 5's to 7's. Overnight Treasury volume was solid at ~185% of average (2's at 234% of ave volume overnight).

… Next up we shift attention to Treasury 5-year notes and their ~3.80% to 4.10% range. Should the emerging bear correction gain fangs/momentum, we're thinking that the 4.30% support zone will act as a backstop if the 4.10% support fails to hold.

… and for some MORE of the news you can use » The Morning Hark - 5 Feb 2024 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

The January jobs data solidified Fed Chair Powell’s pushback against a March rate cut, reinforcing the narrative of impressive growth momentum carrying through into early 2024.

The average hourly earnings print emphasized the more notable risk to our US curve steepening bias: strong flattening is more likely to come from a return of inflation fears than firm growth. In Europe, a slower pace of supply should see focus shift to RV opportunities.

In FX, until the market re-embraces the theme of growth normalization or more Fed rate cuts, it will be challenging for the USD to weaken. EUR-funded carry is likely to outperform in this environment.

… For US rates, we think remaining March cut risk should decay with the passage of time. Some premium has to remain for the tail risk that “something breaks” (indeed, as Figure 1 shows, cut pricing got as far as ~20bp for March on Wednesday morning amid concerns around a return of regional bank stress), but each day that goes by without event should see the remaining roughly 15-20% of cut risk squeezed out. We think risks around May (and beyond) are a bit more dynamic; our view remains that the risk of a definitive range-break lies with a clear downside surprise in activity data, where sustained better activity data may exert a more gradual upward pull on yields.

… Though not a release that typically gets particularly high billing, Friday’s revisions to the CPI seasonal factors will garner attention. It was this update at the start of 2023 that materially dampened what looked to be a decisively improving inflation trajectory (Figure 2). Governor Waller specifically highlighted this piece of news as something he’d be watching to see if it confirms the progress on inflation. Following Friday’s report, we don’t see this as a release that could strengthen the case for sooner cuts, but a re-run of last year’s experience could incrementally raise the bar to what the Fed needs to see in the coming months to feel comfortable cutting.

DB: Early Morning Reid (snippet on yields and CHINA stocks)

Well, that was some week we just had. To very briefly front-run our own regular full weekly recap at the end, 2yr US yields rose +16.1bps on Friday (the largest since March), a March Fed cut pricing fell to 22% (from 50% a week earlier), the Magnificent Seven rose +5.45% on Friday alone with Meta adding the most amount of daily market cap ever ($197bn), this sent the S&P 500 to a fresh all-time high even though 73% of the Russell 2000 fell on Friday, while the US Regional Bank index fell -7.23% on the week. That opening para is enough to wear anyone out….

…Chinese stocks have been on a wild ride this morning with the small cap CSI 1000 down -8% at one point before halving those losses as I type. The Shanghai Composite was down over -3.5% but is now closing in on flat in a very volatile session. Small caps have been sold against large caps recently as the market views intervention as helping the larger indices. Perhaps some triggers or short covering came in to support the bounce back. This vol came even after the Chinese securities regulator (CSRC) vowed to maintain market stability on Sunday.

Goldilocks: Powell 60 Minutes Interview Raises Risk of Later Hike in the “Middle of the Year”

BOTTOM LINE: While the comments from Fed Chair Jerome Powell that were aired in a 60 Minutes episode tonight (Feb. 4) largely mirrored his comments from the January post-FOMC press conference, the interviewer reported that Powell “suggested to us the likely time for the first interest rate cut would be the middle of the year, a few months before the election.” The interviewer also told the audience that cuts “would likely be a quarter, maybe half, of a percentage point at a time.” We are not changing our forecast for the first cut to come in May at this time because we are unsure what exactly Powell said outside of the interview and because our inflation forecast is lower than the FOMC’s, but we now see a greater chance of a “later but steeper” path in which the first cut would come later than May.

Last week's better economic data and mixed earnings resulted in further narrowness and strong performance from large cap quality growth—our preferred pocket of the equity market. Small caps appear to now be exhibiting greater interest rate sensitivity than large caps …

… The bond market went with the stronger read of the data and traded sharply lower on Friday. It also pushed out the timing of the first Fed cut, taking the odds of a March cut all the way down to just ~20%. Recall that this probability was as high as ~90% around the end of last year. Perhaps the market is starting to take the Fed at their word—they aren't planning to cut rates in March despite the bond market's signal that the Fed is behind the curve ( Exhibit 7 ). The equity market looked through this rate move on Friday driven by large cap quality growth strength. We see quality growth continuing to outperform amid strong earnings revisions, particularly relative to lower quality cyclicals and small caps. For now, the internals of the stock market are suggestive of the idea that a stickier rate backdrop is a disproportionate headwind for stocks with poor balance sheets and a lack of pricing power—i.e., lower quality cyclicals and many areas of small caps.

MS: Global Economic Briefing: The Weekly Worldview: Much ado about productivity

Is productivity rising enough to ensure inflation is not a problem despite a strong job market and rising wages? The answer is not so straightforward.

… As Morgan Stanley Research has highlighted often, developments in artificial intelligence (AI) have the possibility of boosting productivity. But for now, we think it is too soon for those gains to manifest clearly in the macro data. Morgan Stanley’s tracking of AI and AI diffusion will be useful as a cross reference as we monitor the aggregate data. Another implication to consider is the frequent refrain that labor costs are rising too quickly to be consistent with central bank inflation targets. We have highlighted in the past that wage inflation tends not to drive much of consumer price inflation in general. And if productivity picks up, that fear can abate further. Indeed, if it is higher labor costs that are driving the productivity growth, the causality needs to be questioned.

MS Sunday Start | What's Next in Global Macro: Paying Attention to Global Tensions

Geopolitical conflict, and the pain and suffering it inflicts on people, is certainly not new to the world. But because financial markets and economies around the world have become more interconnected, we think such conflicts matter more for investors’ outlooks. The backdrop, in our view, is the ongoing transition to a multipolar world, where competition for global power is increasingly leading countries to protect their military and economic interests by erecting new barriers to cross-border commerce in key industries. As we've argued extensively over the past five years, this rewiring of the global economy will drive secular investment trends, with some sectors and regions incurring fresh costs to invest in new supply chain and end-market strategies, while others benefit from those investments (see our Investing for a Multipolar World podcast series for more)…

… Our key takeaways are: Disruptions to Red Sea shipping appear less disruptive than you’d think… EM credit and oil markets appear more resilient than they seem… Underperformance could continue in China equities relative to other Asia markets…

Summary Despite a flattening out in globalization trends over the past decade, U.S. trade with Europe has seen the fastest growth of any major trading partner in recent years. In fact, if recent trends continue, the U.S. trade deficit with the European Union (EU) is on track to eclipse the deficit with China as early as this year.

Europe is also in the process of expanding its carbon tracking and price provisions, which will cover the maritime shipping industry in and outside the bloc and soon require importers to also meet emissions allowances. The expansion will thus extend outside Europe. In other words, right around the time that the EU overtakes China as the biggest factor in the U.S. trade deficit, carbon programs will be coming into effect for this key trans-Atlantic trade relationship.

All told, the expansion of Europe's carbon regulations may cause more headache than harm. The U.S. imported nearly 20% of all goods imports from Europe in the first 11 months of last year, almost half of which arrived on ships. That means roughly a 9% (and growing) share of all U.S. goods imports may be subject to some EU carbon pricing within two years’ time. However, in this report we explain why the EU’s expanded mechanism to capture emissions will not likely have a big effect on U.S. exports to Europe and why the impact to U.S. imports from Europe may not be terribly consequential either. Despite mechanisms to price U.S. carbon by the EU and U.S. industrial policy that is not particularly popular in the EU, the trade relationship between the world’s two largest economies is flourishing.

Wells Fargo: Should We Worry About American Debt?: Time to Reconsider?

Summary

We wrote a series of reports in the summer of 2019 in which we concluded that angst about American debt was not really warranted at that time. However, the overall level of debt in the U.S. economy has risen by roughly $23 trillion (33%) over the past four years, and interest rates are significantly higher today.

The correct way to think about debt, which tends to grow over time, is to measure it relative to another variable that also grows over time. Because the size of the U.S. economy also grows over time, the correct way to think about American debt is to measure it as a percent of GDP.

Although the debt-to-GDP ratio of the American economy is a bit lower than it was in 2008, it is elevated when viewed in a historical context.

We will revisit our 2019 analysis in a five-part series of reports. We will discuss household debt in Part II before turning to the debt of the non-financial business sector in Part III. Part IV will analyze the debt of the federal government while Part V will offer some overall conclusions about U.S. debt.

… And from Global Wall Street inbox TO the WWW,

FT: Why central banks are reluctant to declare victory over inflation

Policymakers had begun laying the ground for interest rate cuts, but strong US labour data shows pressure on prices has not yet abated

… Eswar Prasad, an economist at Cornell University, says Friday’s data made declaring victory against inflation “a much more fraught” decision for central banks. “The reality is that, with these pressures, it’s going to be very difficult to keep inflation contained unless productivity growth remains strong.”

This is not to deny how dramatic the improvements in the inflation picture have been. A year ago, the Fed and its counterparts were in the midst of a brutal series of interest-rate increases that some feared would drive economies into recession.

Powell warned in February 2023 that officials still had a “long way to go” as they attempted to quell the “significant hardship” imposed by the highest inflation in 40 years. Since then, inflation has tumbled towards the Fed’s 2 per cent target across an array of different gauges…

… Continued progress in this disinflation story will hinge heavily on the fate of labour markets. While the initial declines in inflation were driven by external factors, progress now depends on the more difficult task of depressing domestically generated price growth. That will be harder if jobs and wage growth stay too robust.

… Powell himself sounded sceptical about the notion in December. “Inflation keeps coming down,” he said. “It’s so far, so good — although we kind of assume that it will get harder from here. But so far, it hasn’t.”

… Worries about other “upside risks” to inflation have added to central bankers’ caution. One obvious one stems from the continuing conflicts in the Middle East; the disruption to shipping from attacks by Houthi rebels on vessels in the Red Sea is widely cited as a factor that could push inflation higher than expected. Europe appears particularly exposed given the importance of the trade route for imports from China.

Hedgopia: January Barometer Bodes Well For S&P 500, Which Remains Extremely Overbought

January ended up 1.6 percent. Historically, an up January bodes well for the rest of the year. This may very well be the case this year, but one should not be oblivious of how overbought the S&P 500 is.

…Chart 1 plots the annual performance in the S&P 500 going back to 1951 – for a total of 73 years. The data is divided into four buckets: (1) years that finished up when January was up, (2) years that finished down when January was up, (3) years that finished down when January was down, and (4) years that finished up when January was down. The number of years corresponding to each bucket are put in parenthesis.

It turns out the January barometer’s success rate is strong when January ends in the green. Out of the 73, this occurred 38 times; there were only five years that ended down with an up January. This is a very high success rate. In contrast, the record of a down January is mixed right down the middle, with the year ending up or down 15 times each, which is nothing but a coin flip.

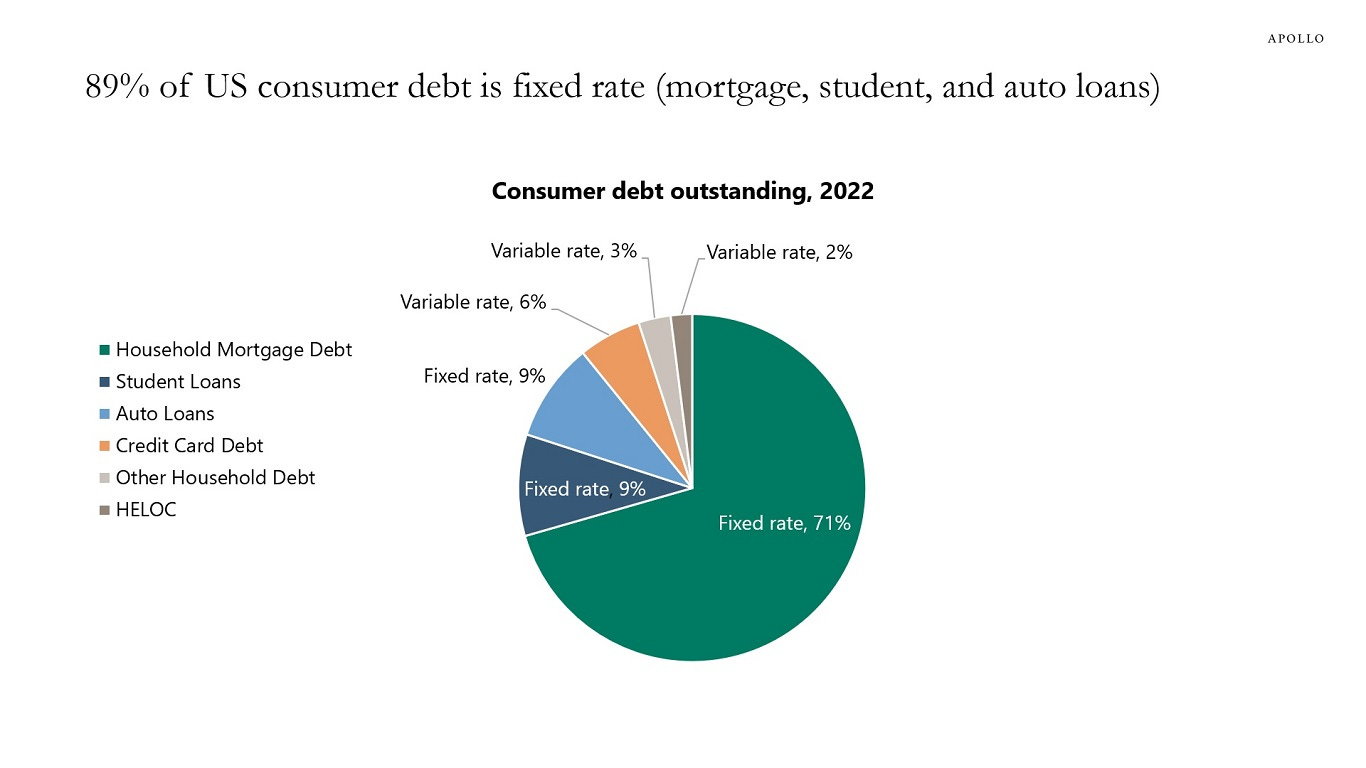

TKer by Sam Ro: Don’t confuse your relatives with your absolutes (good weekly recap and putting of it all together … NOTE chart below in similar fashion to what I attempt to do — is NOT his but rather, right from Apollo … just is what Global Wall tries to do — identify something smart someone ELSE says, rebrand and recycle — then sell it to you within wrapper of … TKer in this case …!)

… Why consumers aren’t getting crushed by higher interest rates. From Apollo Global’s Torsten Slok: “Eighty-nine percent of US household debt is fixed rate (mortgage, student, and auto loans) and 11% is floating rate (credit cards, HELOC, and other types of debt). As a result, the transmission mechanism of monetary policy has been weak. Combined with significant excess savings during the pandemic, Fed hikes have had a limited impact on the consumer.“

This comes as the Federal Reserve continues to employ very tight monetary policy in its ongoing effort to get inflation under control. While it’s true that the Fed has taken a less hawkish tone in 2023 and 2024 than in 2022, and that most economists agree that the final interest rate hike of the cycle has either already happened, inflation still has to stay cool for a little while before the central bank is comfortable with price stability.

Now that the latest meeting of the Federal Open Mouth Committee is over, we can expect lots of chatter from its members. They are likely to echo Fed Chair Jerome Powell's comments in his presser last Wednesday. In essence, he said that the Fed is done raising the federal funds rate further, but is in no rush to lower it either. According to the 12-month federal funds rate futures, this market still expects five rate cuts this year (chart). So Fed officials are likely to continue to push back against that notion of so much cutting.

The second week of each month tends to be light on economic indicators…

Very early into Covid I remember some podcast inflation debate, when someone mentioned, paraphrasing "the DEMS (I'd prefer UniParty) are very crafty, not only will increased immigration garner them Votes, but it'll lower wages too, countering to a degree MMT-QE...."

How much does DEI contribute to Native-Citizen born Quiet Quitting I wonder. It should be well known, that immigrants, weather legal, or especially Illegal, will typically Work Harder, Longer, For Less, With less Fuss, and demand less benefits, than native-born workers. Qui Bono?

Very early into Covid I remember some podcast inflation debate, when someone mentioned, paraphrasing "the DEMS (I'd prefer UniParty) are very crafty, not only will increased immigration garner them Votes, but it'll lower wages too, countering to a degree MMT-QE...."

How much does DEI contribute to Native-Citizen born Quiet Quitting I wonder. It should be well known, that immigrants, weather legal, or especially Illegal, will typically Work Harder, Longer, For Less, With less Fuss, and demand less benefits, than native-born workers. Qui Bono?

This was the only place I heard about Powell's comments on Immigration.

I had seen the chart about foreign workers before.

Wonder how they get those numbers and

how accurate they are?

J. Powell has really grown into that job

and learned from his mistakes.

Seems to have decided not to let the Hedge Funds push us back into easy money again.

He also called out the profligate spending of the Treasury, although not by

name.

Bully for him !!

As an independent voter and America

First patriot, 2 things bother me about President Trump.

The 60 % tariff idea is well, insane.

Some targeted tariffs on China, possible.

Trade wars have unforseen consequences.

He also needs to clarify his position

on EVs. Its one thing to be against Govt

mandates and subsidies; it's another to be against Progress and clean air.

Thanks for you work.

PS: listened to Jeff Gunlach's

Fed Day analysis. He's still looking

for that elusive Recession.

Even the great ones find this economy

a little hard to understand.