Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP lets deal with a couple / few things items from yesterday …

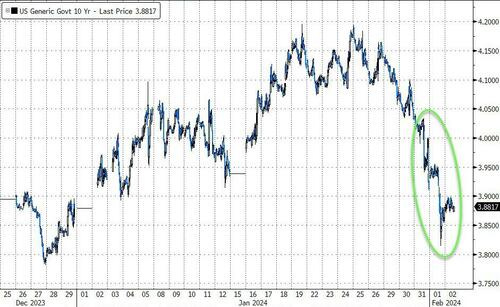

… yields holding on for dear life, hanging by a thread (far better than my now former wisdom tooth did earlier today!!).

… AND on a MONTHLY (so, a longer term perspective) momentum had moved into overBOUGHT territory and appears to be crossing BUT … from not deeply overBOUGHT enough territory to feel comfortable ‘pounding table’ to be short.

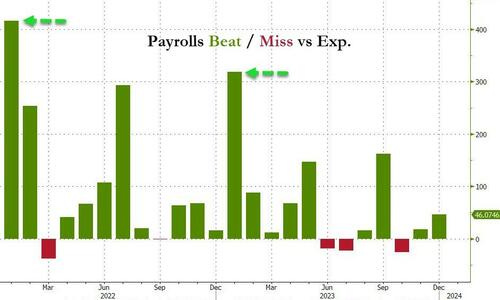

Jumping in to deal with mostly all things NFP related and as ZH (et al) put it right at 830a …

BOOM!

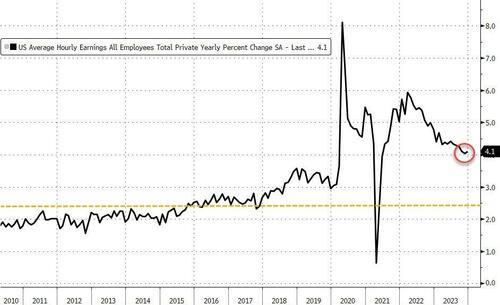

Data BEAT, upwardly revised and oh, yea ‘bout those disinflationary wages ??

GONE … ?

Bids for long bonds (recall DAILY and WEEKLY views HERE — overbought indeed)

Best we can do now is head back to regularly scheduled regional bank collapse in HOPES that something out there bad enough to be good, at least as far as econ goes so as we can continue to press HOPE // BETS on rate CUTS…?

Meanwhile, back at the ranch, why it is that when one grows up one wants to be either a weatherman OR an economist — latter on full display here via BBG (and ZH) graphic posted in aftermath …

ZH: Payrolls 4-sigma beat: 53K above the HIGHEST wall street estimate

ZH: Inside The Most Ridiculous Jobs Report In Recent History

… you can hear the narrative creation machines starting up early and to continue often just as they — Global Wall Street (details below) — have had to update / REWRITE year ahead notes / thoughts before middle of JAN!

Will USTs have looked PAST this data point (as BBGs Ven Ram posed before the data? see below for HIS rant / reasoning) is now known, in fullness of time … initially, though …

ZH: Gold & Bonds Dump, Dollar Jumps As Payrolls Spark Plunge In Rate-Cut Hopes (not so much in the looking past TO JPOW this weekend…)

ZH: January Jobs Shocker: Payrolls Explode By 353K, Double The Expected And Higher Than All Estimate As Wages Surge

Academy(via ZH): "The Fed Has To Pay Attention" To This 'Simply Stunning' Payrolls Report

… Bottom Line If you believe the numbers, price in few cuts, start later, and push longer term yields much higher.

I expect only a portion of that move will get priced in, because the numbers are so stunning they are almost unbelievable!

The one thing that gives me a degree of confidence that the numbers might be realistic, is because of the confidence and spending data we’ve been seeing, which has surprised to the upside, but maybe it shouldn’t have been a surprise if jobs are back to plentiful and raises are the norm.

… AND there is plenty more ‘out there’ for our consumption but in spirit of trying to move along (and now having much LESS wisdom than I did before I lost my last remaining wisdom tooth), I’ll ALSO note …

ZH: UMich Inflation Exp Slows, Sentiment Hits Highest Since 2021 (make any / everything you might like of that there report…)

… Ok I’ll move on AND right TO the reason many / most are here …some WEEKLY NARRATIVES… some of THE VIEWS you might be able to use.

The SHORT version is that somehow NOW with the fullness of time and data in mind, everyone ‘out there’ seems to be coalescing in and around MAY for the first cut.

THIS WEEKEND, a couple / few things which stood out to ME this …

BAML weekly, “Confidence test” (stay short 10s > 3.78, stop if below

BMOweekly, “Coalmine Canary or Idiosyncratic Episode?” (booked profits 2s/10s and get into steepener ahead of bond auction)

JPMs FI weekly (booked profits 5s add back on dips)

Dovish Fed supports lower yields, but technicals and supply are a near term headwind … We took profits on 5-year duration longs and remain neutral for now, as the combination of positioning and supply dynamics could extend the post-NFP move to higher yields

…Revised rate call: No March cut, year end 25 bps higher … we pushed back our expectation for the first rate cut from March to May, where we expect a 25 bp rate cut. There is some risk of June too, since the early May FOMC meeting date leaves only the February and March employment reports to provide some sense that the December and January gains were not representative of the trend pace. By July we forecast that the economy will look much weaker, and the FOMC will see more need to remove restrictive policy. By the end of this year, we expect the Committee will have taken the target range for the federal funds rate back down to 2.75% to 3.00% out of fear over the economic expansion.

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

Apollo: $10 Trillion in US Treasuries Coming to the Market in 2024

A record $8.9 trillion of government debt will mature over the next year, see the first chart below. The government budget deficit in 2024 will be $1.4 trillion according to the CBO, and the Fed has been running down its balance sheet by $60 billion per month.

The bottom line is that someone will need to buy more than $10 trillion in US government bonds in 2024. That is more than one-third of US government debt outstanding. And more than one-third of US GDP.

This may be a particular challenge when the biggest holders of US Treasuries, namely foreigners, continue to shrink their share, see the second chart.

More fundamentally, interest rate-sensitive balance sheets such as households, pension, and insurance have been the biggest buyers of Treasuries in 2023, and the question is whether they will continue to buy once the Fed starts cutting rates.

Our updated outlook for Treasury demand is available here.

2-year Treasury yields up ~17 basis points, biggest move higher since last March

Bloomberg(via ZH): Treasuries May Look Past Non-Farm Payrolls To Powell's Interview

… The labor market has traditionally fared well in the first month of the year, with the actual headline number coming in way higher that forecast over the past two January iterations.

A better-than-forecast reading today won’t tell the Fed anything that it doesn’t already know about the strength of the labor market.

… Hourly wage earnings are still growing at a 4%+ clip, which is largely incongruent with the Fed’s overall inflation target.

That is perhaps one reason why Chair Jerome Powell suggested earlier this week that policymakers are “looking for more good data on inflation” and need continued evidence price pressures are waning.

Absent a shocker from today’s jobs report, Treasuries may decide to march to a drumbeat that has been dictated by concerns about the health of the banking industry.

The bid tone has also been pronounced ahead of Powell’s upcoming TV interview over the weekend, where, as colleague Mark Cranfield points out, the chatter seems to be focused on the Chair using the opportunity to persuade wavering voters within the FOMC that it is time for a rate cut.

Kimble: 2-Year Treasury Bond Yields Near Important Fibonacci Support! (written BEFORE NFP - HERE - and when he says SUPPORT he means resistance but then, he’s NOT a bond guy … he’s just a CHART guy and … nevermind… support. resistance. whatever, you all get the point …)

The Federal Reserve has paused its interest rate hikes and inflation data seems to be leveling off. We’ll see.

All in all, bond yields (interest rates) are pulling back and investors are hopeful that we have a soft landing.

Looking at today’s long-term “monthly” chart of the 2-year treasury bond yield, it’s important to note that short-term interest rates are nearing an important decision point.

Very similar to 2006, the 2-year yield topped at (1) with an RSI divergence. So I humbly ask: Are 2-year yields following the pattern of the 2006 top?

Could this be a double top 18-years later?

The current decline has taken 2-year yields to 61% Fibonacci support level at (2).

If the 61% Fib fails to hold, then look for a sizable decline to follow! Stay tuned!

WolfST: Great to Have a Good Job Market with Surging Wages, but Rate-Cut Mania Takes a Hit. And We Fret about Inflation Reheating

The employment data today poured some cold water on the raging Rate-Cut Mania: The 10-year yield spiked by 17 basis points within a couple of hours.

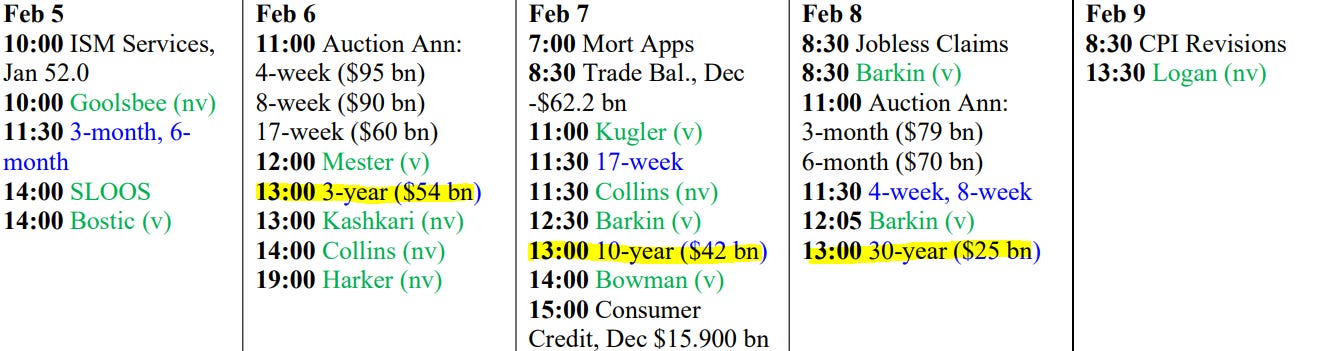

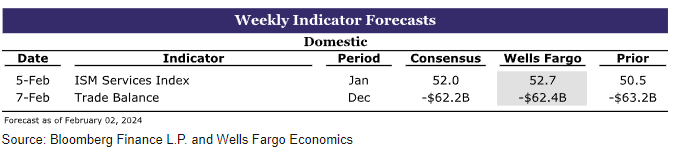

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,