Blonde Money: On this day in 1840, a Pennsylvanian man called James L. Morris recorded in his diary that his German neighbours were celebrating Groundhog Day.

Groundhog Day (Pennsylvania German: Grund'sau dåk, Grundsaudaag, Grundsow Dawg, Murmeltiertag; Nova Scotia: Daks Day)[1] is a tradition observed in the United States and Canada on February 2 of every year. It derives from the Pennsylvania Dutchsuperstition that if a groundhog emerges from its burrow on this day and sees its shadow, it will retreat to its den and winter will go on for six more weeks; if it does not see its shadow, spring will arrive early.

Raining and overcast HERE in NJ but I’m just about 300mi away from Punxsutawney, PA …

With that, I should once again quit while I’m behind and suggest this is as good as this post will get and that you should simple move along and read something else of your choosing…

There will be plenty of NFP precaps below. These will then be followed BY the data and then, Global Wall be once again into overdrive rewriting narratives and once again marking the view TO the market …

That said, I’ll jump in offer a few words first

Good morning.

20s overbought?

Lower yields (cuz, you know, regional bank fire raging with NYCB and oh, yeah, Japan … CRE issues and HOPE for a really bad recession RAISE HOPE for … a recession and moar aggressive rate CUTS this year — March, anyone? — and so) rate CUTS for the WIN please …

Said another way and with a bit of local ‘pop culture’ in mind …

… where the regional banks are the dude on the LEFT, the economy’s the dude in the middle and JPOW is … the dude on the right.

This all STINKS to watch the evening news ‘round here and am still shaking head in disbelief at what has happened TO our fair city.

But I digress. BONDS seem to like it and so … while I may still view the DAILY as overBOUGHT …

… and the WEEKLY as having been overBOUGHT and correcting towards UN overbought (ie higher yields), we can clearly see on the WEEKLY, momentum having turned, crossed and once again favoring another overBOUGHT run at somewhat LOWER yields.

Be sure to scroll ALL the way down for more on just how it is that yields (viewed by AllStars using TYX) are set for largest weekly decline since early 2020 …

AND … good morning indeed, especially for those in the BAD news is GOOD camp …

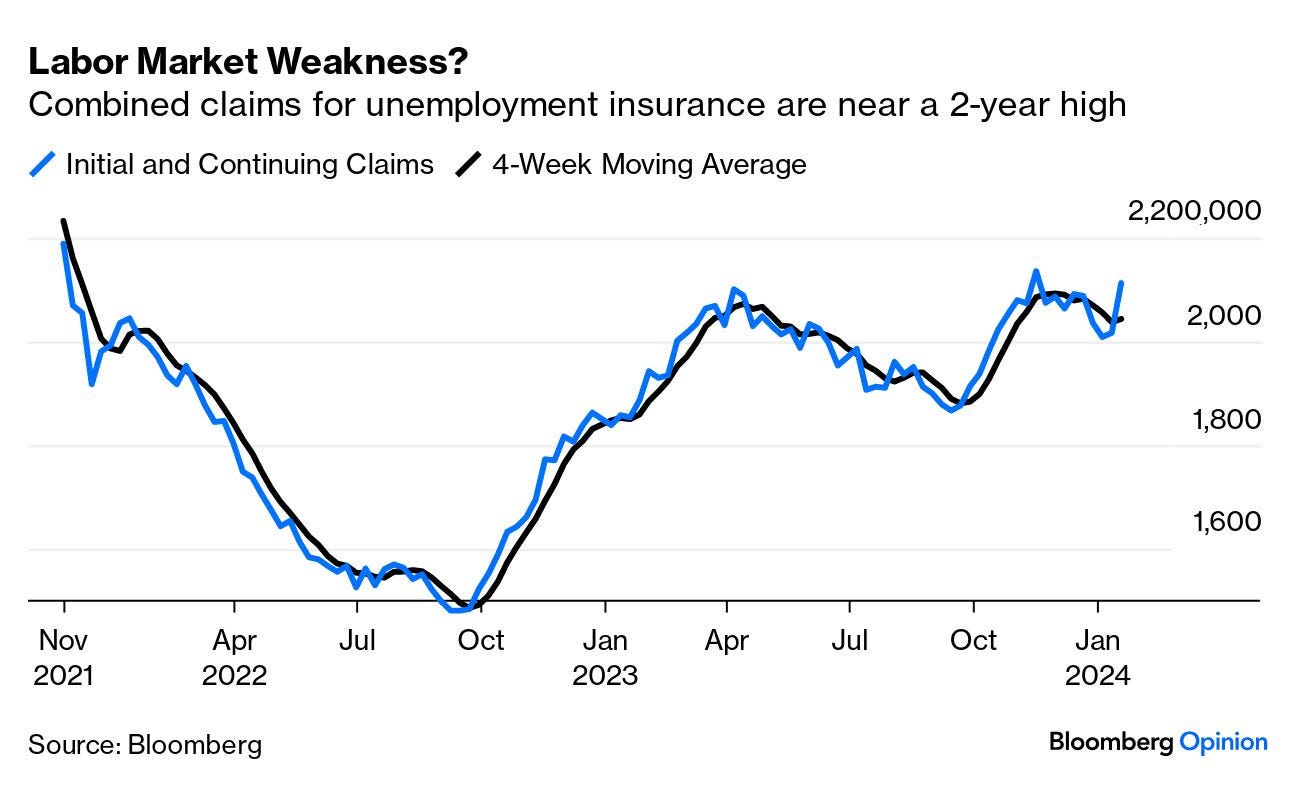

ZH: Initial & Continuing Jobless Claims Surge As Layoffs Accelerate

… This is the biggest two-week jump in initial claims since the start of 2022 (and this is not seasonal, as this data is already seasonally-adjusted)...

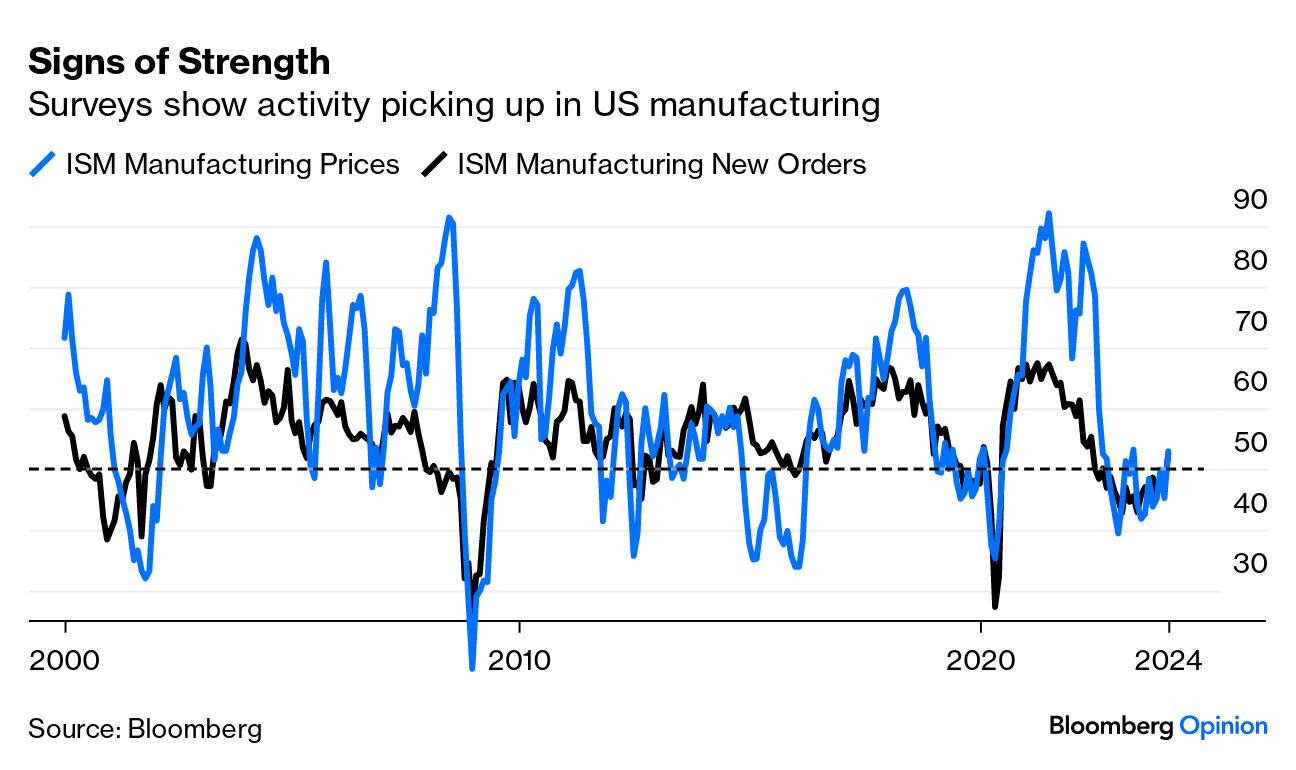

ZH: Manufacturing Surveys Show Rebound In January, But Prices Are Soaring

ZH: Stocks Soar Amid Hopes Regional Bank Crisis Will Lead To Early Rate Cut, More Fed Easing

… and by days end on into AFTER HOURS we’re only left talkin about MONSTER good news (AMZN and META) while talking … less so ‘bout AAPL.

See what you wanna see (should have stopped reading by now … sorry I warned you) and for now … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mixed with the curve twisting flatter (see attachments) around an UNCHD 10-year benchmark. DXY is modestly lower (-0.1%) while front WTI futures are +0.6%. Asian stocks were mixed (China lower, all others higher), EU and UK share markets are all higher (SX5E +0.7%) while ES futures are showing +0.6% here at 6:45am. Our overnight US rates flows saw better real$ buying in the long-end during Asian hours alongside a block buy of UXY futures that posted. During London's AM hours the bulk of our flow was curve-related with interest in 5s30s and 7s30s steepeners from fast$. We also saw real$ demand for 7's and other interest further out that supported prices. Overnight Treasury volume was about average overall...

… we show how front WTI prices (CL1) have been in a tactical up-channel since mid-December with daily momentum (lower panel) showing a local bearish bias. We mention this because the multi-month price pattern looks strikingly similar to that of Tsy 5-year yields- as we show next with an overlay of Tsy 5yrs and CL1. Do we need CL1 to fall back below the $72.50 area (channel uptrend intercept today) to hold 5-year yields under 3.80%??

… good question, indeed … and for some MORE of the news you can use » The Morning Hark - 2 Feb 2024 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … And to be frank with you, WHY it is some / many release NFP precaps the day before the number only to have to go right back TO the proverbial drawing board by weeks end is beyond me but with that said, if yer still here reading, you deserve this all and so …

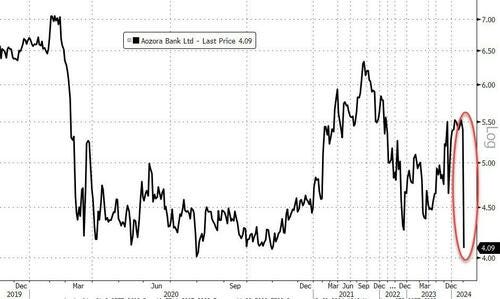

Macro markets have started worrying about US multi-family CRE, similar to last April's office CRE concerns. These fears are vastly overdone, in our view

… Bond markets did not agree with us for all of April. Even as late as early May, over six weeks after the banking crisis had first unfolded, the US front end was pricing in 100bp of cuts by the end of 2023. But eventually, sanity returned as it became clear that the effect of office CRE on banks’ health had been greatly exaggerated. Bond yields repriced sharply upwards, the market took out all the end-2023 rate cuts, and regional banks stocks staged a furious rally from Q4 last year…

… NYCB was idiosyncratic, not indicative of the banking system …

BARCAP U.S. Equity Strategy: Food for Thought: Risk Premia, Complacent or Prescient?

The equity risk premium has been historically low for some time now, but risk premia across rates and credit have also fallen significantly over the last few months. Is this a sign that stubbornly high equity valuations will continue to be justified by a remarkably strong macro backdrop, or is complacency growing?

BNP QTOW: Initiating US 10y short (interesting timing just ahead of NFP — either gonna be CHAMP or chump — likely by 835a …)

KEY MESSAGES

Initiating US 10y payer : MarFA™ Macro sees US 10y yields as 15bp (2 z-scores) too low (Figure 1). This suggests an attractive risk-reward opportunity to add short duration exposure, particulatly ahead of tomorrow’s NFP report. Our economists forecast NFPs tomorrow will have risen by 220k, above consensus at 185k (see US jobs preview: Layoff drought matters most in January dated 26 January).

In addition to this quant mis-pricing, next week we have the US Treasury’s 10y and 30y refunding auctions, meaning an elevated amount of duration supply to be absorbed. February, in particular, tends to be the high point for long-end duration supply owing to the intersection of nominal refunding (relatively larger 10y, 20y, and 30y auctions) and new 30y TIPS during the month (see US rates: A new high for duration supply dated 31 January).

The combination of potential upward momentum to activity data and increased supply next week could support a reversion back to MarFA™ fair value. A risk to this is an extension of the risk-off tone which appears to be centered around regional bank concerns.

Initiating US 10y short, entry 3.85%, target 4.08%, stop loss 3.64%, notional 20k DV01.

Recent rates moves have been favourable to trades in our quant portfolio (Quant Trades of the Week). We tighten stop loss on Poland 10y receiver to 4.75% and take profit on Canada 10y long (24bp), Hungary 10y receiver (36bp) and France 10s30s steepener (5bp).

BNP US rates: Hedging higher yields beyond the election

Investors concerned about a post-election resurgence of term premium may consider entering a high strike calendar spread on 10y tenors.

Our analysis of the last 60 years of US general elections suggests that a change in the party of the president tends to lead to a realized volatility impulse and wider trading ranges surrounding those elections.

While we see material risk of the 2024 election resulting in a divided government, a unified government may increase the likelihood of fiscal expansion.

We consider a few iterations of selling a high strike 10y payer swaption expiring about one month before the election while buying a 10y high strike payer expiring about three months after the election.

DB: Trading US Employment: Expected data errs USD and Carry positive (Ruskin)

DB: The moment of truth is nearing (what a relief THATs gonna be, right?)

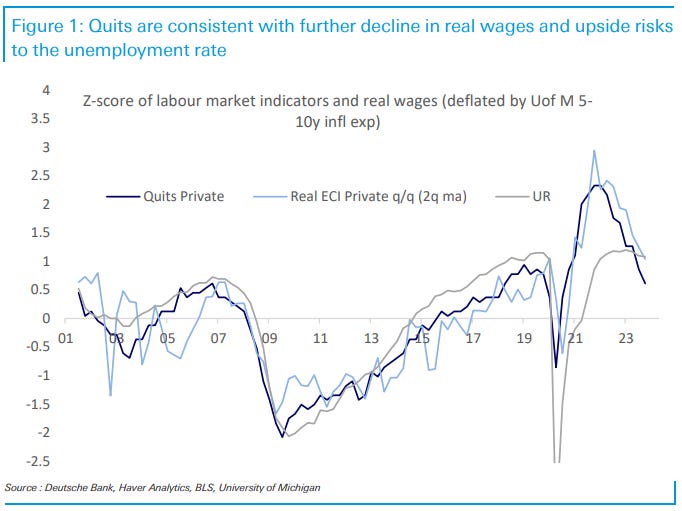

Ahead of NFP, other (more reliable) indicators are consistent with a labour market that continues to ease. More specifically, the private sector quit rate has confirmed its steady trend decline of ~0.1/quarter that started about two years ago. The quit rate remains a reliable leading indicator of real wages (as measured by the private industry ECI deflated by the University of Michigan inflation expectations) and the latter is tracking lower accordingly.

The current level of the quit rate is consistent with a further decline in real wages and upside risks to the unemployment rate. Moreover, if the current trend persists for another two quarters, the quit rate should reach 2.3% in Q2-2024. This would be consistent with an unemployment rate slightly above 4.5% on the basis of the pre-covid Beveridge curve that uses quits rather than openings.

In a nutshell, the moment of truth for the US labour market is nearing.

We expect a strong report, with a large underlying gain in employment partially offset by weather effects. We estimate nonfarm payrolls rose by 250k in January (mom sa)—above consensus of +185k—reflecting below-normal end-of-year layoff rates that more than offset a roughly 50k drag from cold, snowy weather during the survey week. We see a wide range of outcomes for the weather drag and expect this headwind will be visible in the construction and leisure and hospitality categories. Big Data employment indicators were mixed in the month but are also broadly consistent with low layoff rates and a potentially large weather drag…

… Tomorrow’s report will be accompanied by the annual benchmark revision to the establishment survey. The BLS’s preliminary estimate of the establishment survey revision suggested a downward revision of 306k to the level of March 2023 employment, which implies a 26k slower pace of average monthly job growth from April 2022 to March 2023.

Today both the FOMC statement and Chair Powell pushed back against expectations for a near-term rate cut. However, both the statement and the Chair opened the door for easing after the next FOMC meeting in mid-March. The statement indicated that “The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.” That could mean a lot of things, but Chair Powell narrowed it down a little when he said: “I don’t think it’s likely that the Committee will reach [that] level of confidence by the time of the March meeting.” While pushing back against March, the communications were not uniformly hawkish, as easier policy is clearly on the Committee’s mind. The statement noted that risks to growth and inflation were getting into “better balance”—a move to a neutral bias is presumably a precursor to moving to an easing bias. And Chair Powell readily confirmed that almost everyone on the Committee thinks rates should come down this year. One of the more dovish aspects of Powell’s remarks was the asymmetry on employment: strong employment gains won’t necessarily forestall rate cuts, but weak employment gains would “absolutely” hasten rate cuts. We are sticking with our call for a first cut in June. But after Powell’s remarks it’s not hard to see a configuration of employment and inflation data that gets the Committee cutting by May…

We estimate payrolls rose 215k in January, the unemployment rate was unchanged, and the participation rate rose 0.1pp. Earnings forecasted to increase on trend, 0.3%M. We also address last month's weakness in the household survey employment measures. Benchmark revisions to payrolls on tap.

The US reminds us that average earnings are not wages, and also publishes some other employment data. Today’s employment report will be a bit messy—US workers do not like cold weather, and the weather was cold. There is also the big set of benchmark revisions to past data, which are likely to reduce estimated payrolls.

The overall US labor market story is still soft-landing consistent. Middle income families have job security, which gives them the confidence to spend money on life’s essentials (like Taylor Swift concert tickets). Even if payrolls are revised lower, the reality of the 2023 labor market was that people spent money last year. Profit-led inflation has eroded living standards for lower income workers, and that has been reflected in an increase in numbers of multiple job holders…

Wells Fargo: Strong Productivity in Q4 Further Helps Fed's Inflation Fight

Summary Another solid quarter of output growth combined with a cooler pace of hiring in Q4 led to a robust quarter for productivity growth. Nonfarm output per hour worked increased at a 3.2% annualized pace in Q4, pulling the year-over-year rate up to 2.7%. The improved trend in productivity alongside cooler growth in nominal compensation costs has led to a sharp reduction in inflationary pressures emanating from the jobs market. Unit labor costs, which can be thought of as the productivity-adjusted cost of labor, rose 2.3% over the past year in another indication that labor cost growth is nearing the realm consistent with the Fed's 2% inflation target.

Wells Fargo: ISM Highlights the Resilience Paradox

Summary The ISM report is a case study in the task of maintaining price stability and maximum employment in today's variable speed economy. The ISM rose, but remains below 50. Prices hit a 9-month high, yet employment sunk deeper into contraction.

The FOMC stuck to its script this week, kicking the can and keeping rates steady.

Everyone was expecting the news. But the market wasn’t expecting Fed Chairman Jerome Powell (the man, the myth, the legend) to completely dash its hopes of a March cut.

Strangely enough, rates continue to fall on the news – even as markets adjust to the possibility of the initial rate cut now coming in May.

Before you run out to buy US treasury bonds, check out the overlay chart of the US 2- and 30-year yields:

There’s a big difference.

The 2-year yield is churning sideways, reflecting the market’s expectations of the FOMC’s next move – nothing in the foreseeable future.

On the other hand, the 30-year yield is turning lower. Unlike the short end of the curve, the long end gauges the prospect of long-term economic growth.

What do we do with this information?

Buy long-duration bonds! That’s a much better option than sitting around dreaming of an impending recession. It’s simple – and far more productive.

Plus, the 30-year yield tucked tail at a logical level:

Notice the 30-year stopped rising in the same vicinity as its Oct. ‘22 and Aug. ‘23 peaks – an excellent level to trade against.

But we don’t directly trade interest rates. We trade their corresponding bonds.

Honestly, I’m not crazy about buying bonds. But I can’t deny the bullish price behavior.

The 14-day RSI has completed a bearish-to-bullish reversal. And last fall’s long bond trade worked!

I like 30-year T-bond futures long above 123’00, targeting 133’00. (The comparable levels for the T-bond ETF $TLT are 100 and 109.)

To be clear, we can’t hold these assets if they fall below risk levels.

I might not like it, but long-duration bonds are triggering buy signals.

Legendary trader Peter Brandt navigates the markets with the mindset of strong opinions, weakly held.

Perhaps it’s time to drop last year’s opinions regarding bonds, take the trade, and manage risk.

AT SSTRAZZA (an ALLSTAR chartist … at least by name anyways … if you proclaim it and say it enough maybe at some point folks start to believe it and will pay for it? i wish I’d have tried it … oh well, maybe next time)

Yields are on pace for their largest weekly decline since bottoming in early 2020... and risk assets can't catch a bid $TYX

Apollo: Government Interest Payments Have Doubled since 2021 (this is bad … flat out NOT good, don’t care yer party affiliation)

In 2021, US government interest payments were around $350 billion, see chart below.

Because of the increase in interest rates and debt levels, annualized debt servicing costs are now above $700 billion.

Bloomberg: Blinded by the Light of Big Tech Earnings (Authers’ OpED)

With stocks on a tear, the bet is that US banks are not going to bring down the economy. The latest Magnificent Seven results strengthen that view.

Constructive Ambiguity Sometimes there’s no room for financial ambiguity. That seems to be true of the latest wave of results from Big Tech, with the first-quarter earnings of both Meta Platforms Inc. and Amazon.com Inc. received rapturously after Thursday’s market close. It’s not true of the broader fate of the global economy, where the latest data leaves much to interpretation.

If you want to predict that rates aren’t coming down as quickly as everyone seems to think, you could use the latest Institute of Supply Managers surveys of the manufacturing sector. In the US, new orders and prices unexpectedly turned up sharply, suggesting that the sector wasn’t contracting, and that some inflationary pressures might still be around. The proportion of businesses complaining about rising prices was the highest in nine months:

If you’d rather the Federal Reserve and other big central banks started to cut rates at the next opportunity, then you can use the data on claims for jobless insurance in the US. As good an up-to-date measure of layoffs as we have, it signals that total claims are rising again, and close to a two-year high. As the Fed obviously cares about the half of its mandate devoted to full employment, this looks like an argument to start easing:

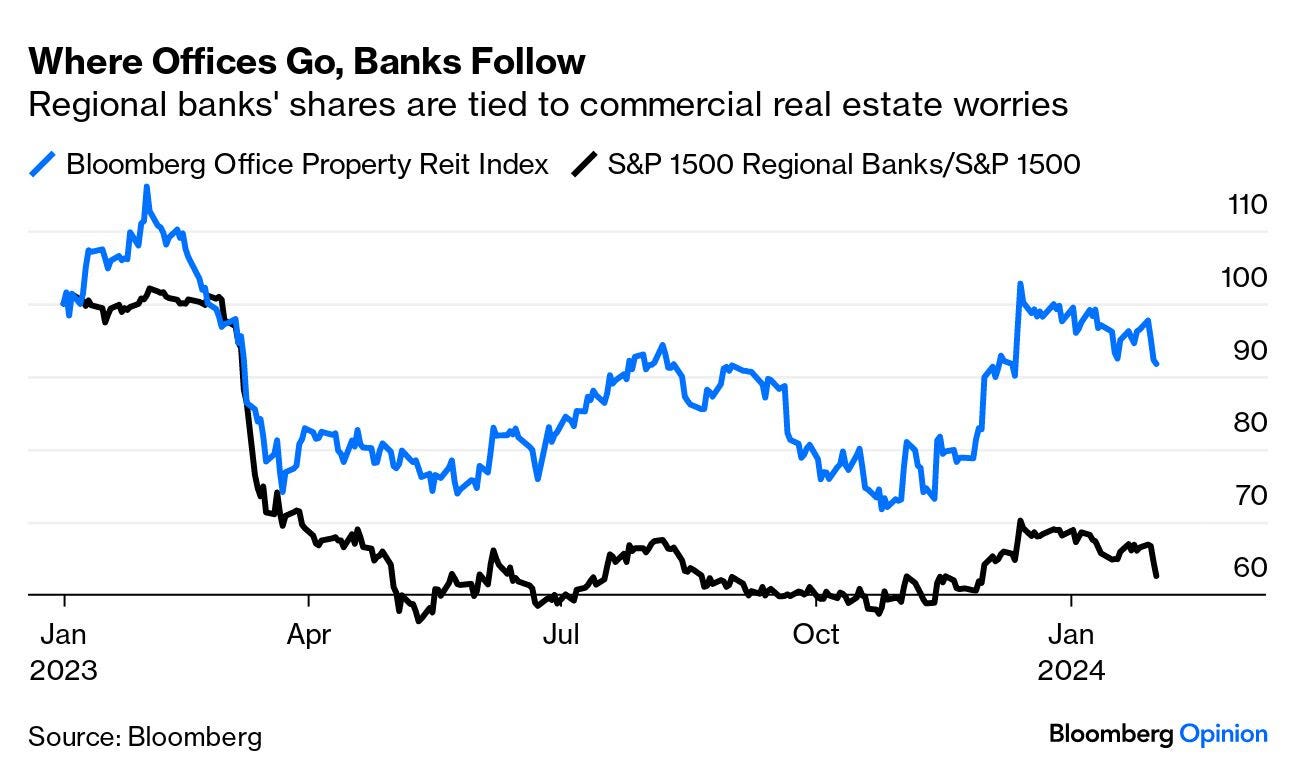

The US Non-Farm Payrolls data for January, due hours after this is published, could clarify things, but probably won’t. Meanwhile, commercial real estate — especially office property — is back as a cause of great angst, thanks to a shocking loan loss provision of $550 million from New York Community Bank earlier this week. Office property has led the relative performance of regional banks over the last year. Lenders tanked in March 2023 as Silicon Valley Bank (SVB) and others ran into trouble due to real estate loans, and their performance has moved in line with office property ever since:

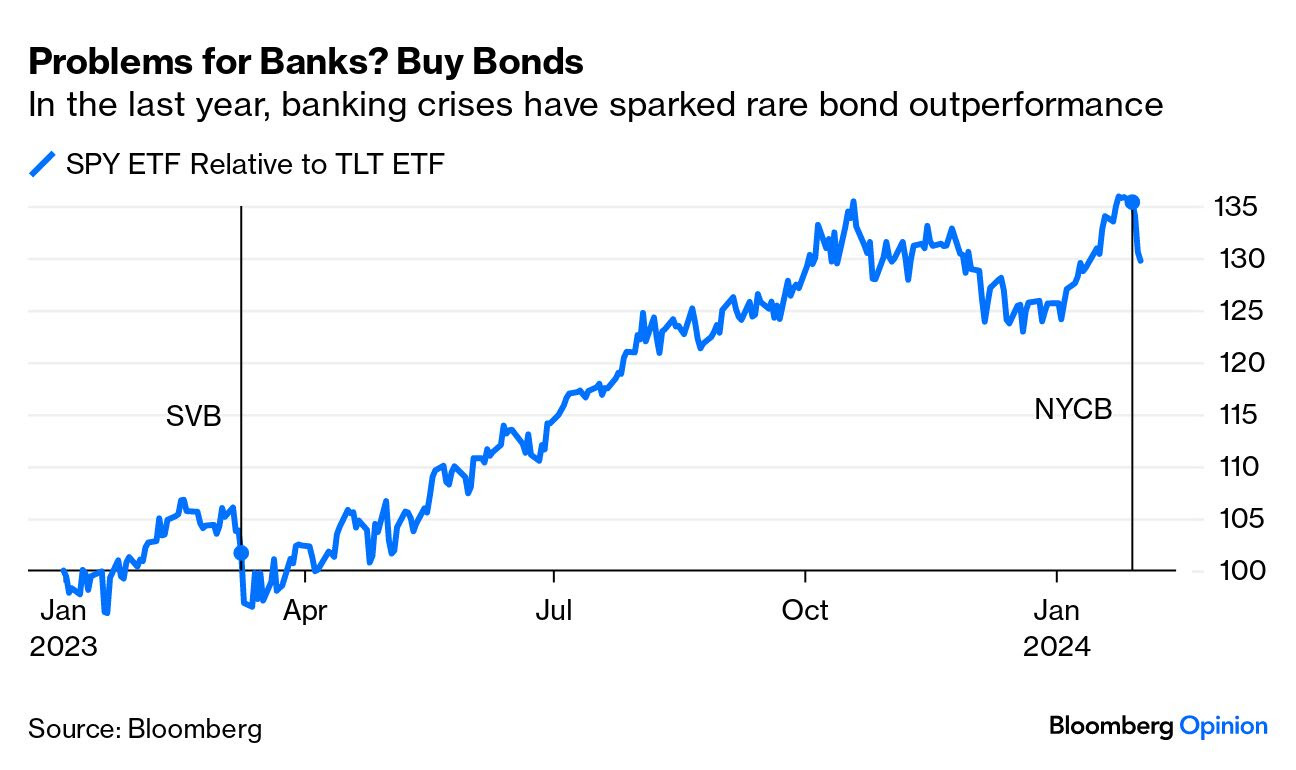

This has broader ramifications for asset allocation. Any problem for banks increases the chances of more liquidity from the Fed, which has only just discontinued the term lending support it gave them last year. All else being equal, emergency liquidity should be good for bonds relative to stocks. And so it has proved. The last few days have seen one of bonds’ strongest rallies since last March:

It’s not just NYCB. As Bloomberg reported,banks in Germany and Japan are also taking hits from their exposure to US commercial real estate. And the anecdotal evidence is that big institutions are washing their hands of the sector. Boston Properties Inc.’s earnings call earlier this week revealed that it had purchased a 29% interest in 360 Park Avenue South, an office block in a prestigious midtown Manhattan location, for $1, from its previous joint-venture partner Canadian Public Pension Investment Board. The pension fund, one of the most respected and influential in the world, had invested $71 million in the property. While this was doubtless good business for Boston Properties, it can only be alarming that a large institution is prepared to take a loss on such a scale to rid itself of a midtown Manhattan office block…

ING: Mixed messaging on US data still argues for a Fed delay until May

The US data continues to refuse to convincingly break one way or another. This will leave members of the Federal Reserve unconvinced there is enough evidence to justify cutting interest rates as soon as March. We favour a May start point, but when the cuts come we believe they will be significant

… finally before signing off for the day, a note about the weekend and some notes / thoughts ahead of Sunday nights open.

Federal Reserve Chair Jerome Powell will appear on CBS News’s 60 Minutes this Sunday and will discuss inflation risks, expected rate cuts and the banking system, among other topics, the network said. Powell last appeared on the program in April 2021. The Fed, which left interest rates unchanged at a policy meeting earlier this week, is in the midst of a policy pivot…

I did not KNOW he’d be on this weekend and I will be sure to gather family ‘round the radio as there is NO football on this weekend.

Nice timing, JPOW … Well done.

NOW at the same time, I’m NOT 100% sure there will be any output as I’m having a wisdom tooth out and while it may be an important weekend for those on Global Wall who are CREATING of narrative, in light of NFP and whatever else lurks (local community banks here or somewhere else) which in turn impacts the BAD IS GOOD reflexivity … I will do my best to have something BUT in the case I find it best to rest up for the week ahead, well, so be it.

Have ‘your gal call my gal’ for a reFUNd.

Oh wait, there is no cost and that you’ve made it all way down here … well, you’ve clearly got issues (too!). My apologies! :)

Have a great weekend and … THAT is all for now. Off to the day job…

Was wondering if someone else was missing football this wknd....I've got deep root cleanings & LaSEARED gums in my future next month I feel your pain bud....rather than J-POW may I suggest an hr w/the MASTER himself Lacy on Thoughtful Money! Just released yesterday, bring your Thinking Caps

Economic Ambiguity........bodes well for Fed ON HOLD.....indefinitely ????

Best of luck at the dentist....been there done that, with 4 wisdom teeth taken out years ago.

NFP script as usual...Headline: Higher than expected; later to be, quietly revised Down

Thanks for your work !!!

Was wondering if someone else was missing football this wknd....I've got deep root cleanings & LaSEARED gums in my future next month I feel your pain bud....rather than J-POW may I suggest an hr w/the MASTER himself Lacy on Thoughtful Money! Just released yesterday, bring your Thinking Caps