while WE slept: USTs little changed (on avg volumes) DESPITE NVDA; do you believe in miracles (hockey fans and N225 investors do); positioning STRETCHED; soft landings

Good morning … Most of what follows will be in some way / shape / form related TO some inputs we got from during the trading day (FOMC minutes HEREand the 20yr auction results) as well as shape shifting post op after NVDA …

First up … on this day in 1989, Japan’s N225 made it’s all time high … more in a sec as we just closed ABOVE these highs but seriously speaking on this day in 1989 …

History.com: In one of the most dramatic upsets in Olympic history, the underdog U.S. hockey team, made up of college players, defeats the four-time defending gold-medal winning Soviet team at the XIII Olympic Winter Games in Lake Placid, New York. The Soviet squad, previously regarded as the finest in the world, fell to the youthful American team 4-3 before a frenzied crowd of 10,000 spectators. Two days later, the Americans defeated Finland 4-2 to clinch the hockey gold…

… Do yourself a favor and pause to watch the final minute including Al Michaels call …

… and so I ask (just as the folks invested in N225 are asking this evening), ‘Do you believe in miracles' … seriously, though, I don’t remember much ‘bout my UTE but watching this as a 10yr old … well, certainly makes one a proud American as well as a hockey fan … There are all sorts of overlays and stoopid puns about how this relates TO ones Fed call or how the FOMC may very well see the upcoming economic landing (of macro econ developments and flation, etc) but fact remains that since Feb 22 1989, there are few TRUE miracles and on this day, the single one on ICE (as well as last nights financial markets miracle in Japan) are likely a couple more of the important ones …

Moving on to a couple / few other important developments yesterday …

ZH: Yields Surge After Terrible 20Y Auction With Biggest Tail On Record (pick / choose whichever narrative you preferred — both a bullish DAILY and bearish WEEKLY were offered HERE yesterday so that either way, the price action told us so …?)

… Moving on then TO …

CalculatedRISK: FOMC Minutes: "Most participants noted the risks of moving too quickly to ease the stance of policy"

CNBC: Fed officials expressed caution about lowering rates too quickly at last meeting, minutes show

“Most participants noted the risks of moving too quickly to ease the stance of policy” and that rate cuts wouldn’t be “appropriate…. until they had gained greater confidence that inflation was moving sustainably toward 2%”

ZH: FOMC Minutes Show 'Most Officials Fear Risk Of Cutting Too Quickly', Staff Mention Financial Stability Issues

… and that — important and FUNduhMENTAL as it all may be, pales in comparison TO the big news of the day …

CNBC: Nvidia posts revenue up 265% on booming AI business RTRS: Nvidia stock surges as revenue forecast tops estimates, AI demand continues

… and all THIS then set the table for …

NikkeiAsia: Japan's Nikkei Stock Average closes above 1989's all-time high (there is a longer - term annotated visual here which was nice but I also like the one just below by CitiFX)

… In as far as WHY any / all this (esp N225) stuff matters to an OLD rates guy well … they did lead us all down the rabbit hole of ZLB (see more from FRBSF below) and while the world has HIKED they have not. The world (USA) is on verge of having hiked SO much they’ve gotta CUT rates (and through thick and thin, BOJ aggressively UNCH) and so, watching any / all this along side whatever it is they do / don’t do.

Clearly MARKETS continue to price in UNCH and CUTS and last nights N225 move will make my view extremely difficult to change. For better or worse, with / without AI, markets remain very susceptible TO perceptions of Global CBs ‘next move’ …

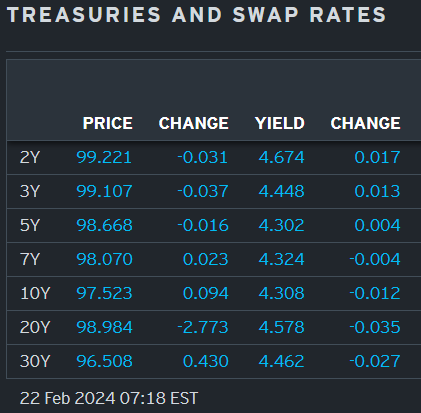

AND … here is a snapshot OF USTs as of 718a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mixed and little changed despite a sharp rebound in global stocks (ES +1.3%) overnight after some blowout Tech/AI earnings were released late yesterday. DXY is lower (-0.3%) while front WTI futures are little changed. Asian stocks were solidly higher, EU and UK share markets are solidly higher (SX5E +1.3%) while ES futures are solidly higher (+1.3%) here at 7am. Our overnight US rates flows saw a modest early rally and then a dip after stronger than feared EU PMI data. We saw selling out the curve from systematic names and relatively more flow interest in curves versus duration this morning. Overnight Treasury volume was about average overall...

… and for some MORE of the news you might be able to use…

NEWSQUAWK: NVDA earnings boost market sentiment with Equities & Antipodeans bid whilst USD dips; US PMI & IJC due … Bonds are divergent, with EGBs choppy on the morning’s PMI data

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … one part FOMC minutes reCAPathon and another for other stuff …

The minutes of the January FOMC meeting did not provide new information about the timing of rate cuts, but they presented valuable color on the breadth of the concerns among FOMC participants about easing policy too quickly. We retain our baseline call of a first rate cut in June.

The minutes of the January FOMC meeting reiterated the message of the post-meeting statement that "participants generally" thought it would not be appropriate to cut rates "until they had gained greater confidence that inflation was moving sustainably toward 2 percent."

The minutes made clear that "several participants" pointed to the risk of financial conditions being too loose at the time of the meeting, and that "most participants" noted the risks of easing policy too quickly.

We retain our baseline rate call: We expect the FOMC will initiate an every-other-meeting rate cutting cycle in June, implying three 25bp cuts in 2024 to a target range of 4.50-4.75%, and four more cuts in 2025. This is predicated on a gradual moderation in inflation measures in coming months.

BloombergBNP US January FOMC minutes: Optimistic but cautious (interesting FOMC voting member ‘scorecard’ which are 100% subjective)

KEY MESSAGES

The January FOMC minutes reinforced our view that the Fed will take a cautious approach to cutting rates.

Despite increasing optimism on the inflation front, most Fed officials remain wary of moving too quickly to ease policy.

We still expect the cutting cycle to start in June.

The minutes point to a multi-step process in tapering QT and as a result we are shifting our QT taper call by one meeting, to a May announcement with implementation in June.

CitiFX: Techs - A stocks stocktake (uptrend in tact BUT … for the longer term look at N225 … )

Post NVDA earnings, we take a look at equities tech charts (S&P, NASDAQ, HSI and NKY). In short: we expect the uptrend in stocks to continue, though resistance levels are close by on the horizon.

… NKY: Price is testing resistance at 38957 (1989 and ATH). IF we break above, next resistance is at the 40000 psychological level

DB: Early Morning Reid - Macro Strategy (on NVDA, FOMC, 20yr auction and Barkin all as they relate TO rate CUT expectations)

…On the rates side, a key story yesterday were the FOMC minutes, which reinforced the narrative that the Fed was in no rush to ease policy. According to the minutes, “most participants noted the risks of moving too quickly to ease the stance of policy and emphasized the importance of carefully assessing incoming data in judging whether inflation is moving down sustainably to 2 percent”, while “several participants mentioned the risk that financial conditions were or could become less restrictive than appropriate“. Meanwhile on QT, the minutes confirmed plans to begin in-depth balance sheet discussions at the March meeting, though this came with a view “to guide an eventual decision to slow the pace of runoff”, so not just suggesting that a change on QT is imminent.

The minutes came an hour after a 20yr Treasury auction, where weak demand helped to push up yields further, as the share of indirect bidders fell to its lowest since May 2021. Moreover, there was some hawkish commentary earlier in the day, which further contributed to the bond selloff. For instance, Richmond Fed President Barkin said in an interview (recorded on Tuesday) that “You do worry that when the goods price deflation cycle ends, you’re going to be left with shelter and services higher than you like it”. And over in Europe, the ECB’s Wunsch said “I believe one should not discard a scenario in which monetary policy stays tight for longer than currently expected”.

Collectively, that led investors to dial back their expectations for rate cuts again. In fact, the chance of a rate cut at the Fed’s March meeting was down to just 7%, which is the lowest in over three months. Bear in mind that a cut by March was fully priced at the start of the year, so we’ve seen a significant turnaround in expectations so far this year. And looking further out, the amount of cuts expected by the December meeting was down to just 86.7bps by the close, the lowest in more than three months, and a major decline from the 168bps expected less than six weeks ago…

DB: Party rules or policy rules? A look at Fed policy in election years

One question arising with increased frequency is whether the upcoming US election will impact Fed policy and in particular the FOMC’s rate decisions over late summer and fall. Using policy rules, we examine whether post-Volcker Fed policy has been set differently during presidential election years. We find it has not.

To start, Figure 1 shows the history of the fed funds rate target over the past 40 years, with the timing of presidential elections captured by the vertical lines. As we see it, there’s no clear pattern. During election years, the Fed has variably been in the midst of a tightening campaign (1988, 2004, 2016); on the eve, in, or at the end of an easing cycle (1992, 2000, 2008, 2020); or in an extended rate pause (1996, 2012)…

Goldilocks: January FOMC Minutes Emphasize Risk of Easing Prematurely

BOTTOM LINE: The minutes to the FOMC’s January meeting noted that while the risks to achieving the FOMC’s goals “were moving into better balance,” the Committee “remained highly attentive to inflation risks.” “Most” FOMC participants emphasized the risk that the Committee would move “too quickly to ease the stance of policy,” while “a couple” of participants stressed downside risks to the economy from “maintaining an overly restrictive stance for too long.” That being said, the minutes also noted that 6-month annualized headline PCE inflation was “near 2 percent” and core PCE inflation was “just below 2 percent.” As a result, participants observed that they “would be carefully assessing incoming data in judging whether inflation was moving down sustainably toward” the Fed’s 2% target. While participants expected inflation to continue to move down toward the FOMC’s 2% target, “several” participants noted that “the risk that financial conditions were or could become less restrictive than appropriate” could “cause progress on inflation to stall.” “Many” participants suggested that the Committee start “in-depth discussions” at the March meeting to “guide an eventual decision to slow the pace of runoff.” We expect the FOMC to begin tapering the pace of runoff in May and end balance sheet runoff in 2025Q1.

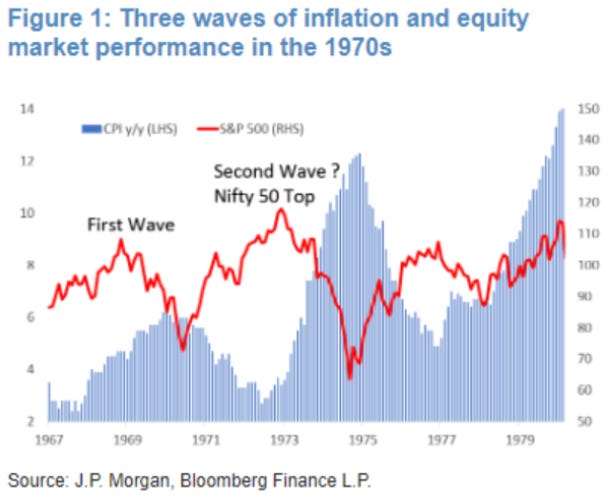

JPM: Market and Volatility Commentary (Marko Kolanovic, PhD AC)

1970s and Risk of a Second Wave, Elections and Markets, Positioning

… The increase of CPI and PPI last week and some weaker economic data from the US and abroad cast some shadows on the most optimistic scenarios. With the Nasdaq index rallying ~70% in a year, tight labor markets, and high immigration and government fiscal spending, it wouldn’t be a surprise that inflation may stop declining or move higher. Can one get inflation under control with stock and crypto markets adding trillions of paper wealth, and tightening aspects of QT neutralized by treasury issuance? For instance, just one tech company’s recent gains added the equivalent of the market capitalization of the bottom 100 companies in the S&P 500, and the size of the crypto market doubled since last fall. Can the Fed lower inflation with these developments that are loosening monetary conditions? Historically, loose monetary conditions are a significant driver of upside in CPI readings (Granger Causality Test shows that US Core CPI is driven by Financial Conditions (1-Pvalue) with 99.7% confidence). These inflation considerations are separate from geopolitical considerations such as currently low oil prices (with risk of an upside shock), shipping disruptions in the Middle East, and risk of East Asia supply chain disruptions as a result of geopolitical conflicts or an outcome of US elections. We believe Investors should be open-minded that there is a scenario in which rates need to stay higher for longer, and the Fed may need to tighten financial conditions. The ~25% stock market rally since October was predicated on a repricing of the Fed (from cutting only 2 times in 2024, to cutting ~7 times in January). While most of those incremental cuts are now priced out, the stock market did not correct at all. Volatility has been unusually low, and risk positioning has increased substantially over the past year (see below). Many investors pursue momentum strategies on a cross-asset basis (e.g. heavily overweight equity), or cross-sector momentum themes (such as long mag 7 and short Russell 2000). While momentum strategies most of times make money, reversion points can erase years or performance in short periods of time.

The FOMC minutes revealed policymakers strayed far from focusing solely on near term policy and discussed a range of macro topics including immigration, labor supply, productivity, BNPL. This is a Committee with plenty of time on its hands to determine its next move.

'Good' data are usually bad for risk assets the closer we get to a Fed decision, and we expect markets to be choppy from here, preferring to stay close to home in bonds and equities. PMIs potentially back >50 in the next few months might not be that significant for performance this cycle round.

Key takeaways

Rates and equity vol to stay elevated, with markets reacting more than usual to bumps and surprises in the data given investors' growing uncertainty on the Fed.

Good data are good for risk assets generally when 1) a hike/cut is far away or 2) there's certainty in an imminent rate hike/cut.

Equities have historically seen worse average returns in the 'good data are bad' scenario, while fixed income responds less.

We caution against building a bull case on PMIs returning >50. Historically, this has not meant significantly better or worse future returns for major markets.

Markets have largely ignored PMIs this cycle, meaning 'good news' may not be sufficient in supporting risk asset returns, or dampening uncertainty and vol.

MS US Economics: Our Inflation Forecasts - A Round Trip (inflation call UPdated yet affirming JUNE CUTS)

We update the inflation path to fold in our Jan core PCE forecast of 0.43%M. We also incorporate the recently published seasonal factors for 2024. We now expect core PCE one-tenth higher at 2.3% (Q4/Q4) for 2024. Our bumpy inflation call remains, and continues to underpin our view of a June start to cuts.

… Also in Today’s Report – 1) Among the largest, AAPL most vulnerable and GOOGL on watch; 2) Big test for global yields at resistance; 3) More turns / breakouts in Healthcare…

… THE KEY QUESTION… RESUMPTION OF TREND, OR A “RIGHT SHOULDER”

… Overall the risks to waiting appear low "Most participants noted the risks of moving too quickly to ease the stance of policy and emphasized the importance of carefully assessing incoming data in judging whether inflation is moving down sustainably to 2 percent. A couple of participants, however, pointed to downside risks to the economy associated with maintaining an overly restrictive stance for too long," note the minutes. Out of 19 participants, a couple means just two, as Janet Yellen used to say.

Participants noted the risk that momentum in the economy may be stronger than currently assessed "especially in light of surprisingly resilient consumer spending last year." Several noted financial conditions were or could become less restrictive. Plus, upside risks to inflation cited included geopolitical developments, elevated wage growth and supply side improvements running their course. Altogether, these could stall inflation's improvement. Positive developments on the supply side including unfolding immigration and labor force participation were noted, and a few pointed to improved productivity growth.

A lot of positives supported the tone to be careful, watch and wait. Other than the lone "couple" the FOMC appeared to see little risk in waiting and much more risk in moving too soon. "While the inflation data had indicated significant disinflation in the second half of last year, participants observed that they would be carefully assessing incoming data in judging whether inflation was moving down sustainably toward 2 percent," said the minutes…

The Federal Reserve minutes offered some clarity on future Fed policy. The tone is consistent with rate cuts and a soft economic landing. The Fed does not want rising real interest rates with a slowing economy. Disinflation trends were discussed (economists selectively adjust data to better identify these trends).

The ECB policy meeting account is less likely to offer clarity. Eurozone fundamentals support rate cuts—perhaps even more so than in the US. However, the cumbersome decision-making and weak leadership mean easing rates will take time. Today’s release will be examined for signs of, which could delay policy action.

Japan’s equity market hit a new high, exceeding the 28 December 1989 level. In December 1989, “Back to the Future II” was playing across cinemas, in which Japanese corporations were (problematically) depicted as dominating the year 2015. Equity strategists will be excited by the drivers of the current equity high. Economists might reflect on the dangers of extrapolating from past economic trends when forecasting future economic success.

China’s policymakers have reportedly banned large institutions from reducing equity positions at the start and end of each trading day. This is of course an asymmetric policy—there is no suggestion that firms would be banned from buying equities.

… And from Global Wall Street inbox TO the WWW,

AllStarCharts: 140-year Old Strategy Is Working (DOWn THEORY)

Decades after his death, these indexes were renamed the Dow Jones Industrial Average and Dow Jones Railroad Average. The latter was ultimately renamed again to the “Transportation” Average, as by then there were other methods of delivery outside of Railroads.

And so here we are today.

Charlie would be so proud of us.

The chart below shows the Dow Jones Industrial Average making new highs, as recently as last week. But the Dow Jones Transportation Average has not been able to do that at all.

Here’s the Dow Theory Divergence in real time that Charlie Dow was writing about almost 140 years ago:

If you’ve gone back and studied major turning points in markets over the years, you’ll notice how often this divergence is front and center.

You saw it right before the GFC in 2008. You saw it right before the Tech bubble peaked in 2000. You even saw it before the COVID crash in 2020.

And now you’re seeing it again.

So if it was just one divergence among an ocean of bullish characteristics, then that would be one thing.

But it’s not…

Apollo: The Fed Is the Reason the Last Mile Is Harder

Since the Fed pivot on December 13, consumers have become much more optimistic about the economic outlook, see chart below. Combined with record-high IG issuance, high HY issuance, and more IPO and M&A activity since December, it is not surprising that employment and inflation rebounded in January and jobless claims remain low.

The last mile is harder not because of some structural feature in the economy, but because of the Fed turning dovish too soon, triggering a reacceleration in growth and inflation. That is why the Fed will keep rates higher for longer than markets expect.

The share of private consumption spent on services is still 2 percentage points below its pre-pandemic level, see chart below.

The implication for markets is that there is still more upside for growth in consumer services, i.e., spending on airlines, hotels, restaurants, concerts, sporting events, etc.

JPMorgan’s Treasury client positioning survey is starting to look STRETCHED:

-Net longs lowest since April 2023 -Neutrals most since Sept. 2011 -Outright long lowest since Feb. 2023 -Outright short lowest since 2012

Bloomberg: T-Bills Without Tax Bills? This Fund Says It Cracked the Code

A fast-growing exchange-traded fund uses an old loophole in a new way.

Bloomberg: JPMorgan’s Kolanovic Bucks Consensus by Seeing Stagflation Risks

Hotter CPI, PPI cast a shadow over economic optimism, he says

Market is similar to when equities were flat from 1967 to 1980

… Markets have recently dialed back expectations for Fed rate cuts this year after faster-than-expected inflation readings and pushback from policymakers. Fed officials last month held interest rates steady as they nursed concerns over the risks of easing policy too prematurely.

Investor hopes of “parabolic stock markets” and “platinum-locks” — an even more optimistic version of Goldilocks — reflect excessive optimism. The strategist also disagreed with a theory that stocks can trade higher because the neutral rate of interest, or so-called R-star, is making financial conditions easier.

“This sounds to us like a stretch, and consumers who can’t afford the new mortgage rate or a car loan payment are not deciding based on theoretical changes in r-star,” he wrote.

Shortly after the recovery from the pandemic recession began, the U.S. economy entered a period of high inflation as surging demand, severe supply disruptions, and worker shortages combined to create large imbalances and inflationary pressures in the economy. Have these pressures moderated for local businesses in the New York–Northern New Jersey region? The New York Fed’s February business surveys asked firms about increases in their costs and prices.

FRB SanFran: Understanding Persistent ZLB: Theory and Assessment

We develop a theoretical framework that rationalizes two hypotheses of long-lasting low interest rate episodes: deflationary-expectations-traps and secular stagnation in a unified setting. These hypotheses differ in the sign of the theoretical correlation between inflation and output growth that they imply. Using the data from Japan over 1998:Q1-2019:Q4, we find that the data favor the expectations-trap hypothesis. The superior model fit of the expectations trap relies on its ability to generate the observed negative correlation between inflation and output growth.

… Conclusion In this paper, we formally test two hypotheses of stagnation: deflationary expectations traps and secular stagnation. We entertain both models within a unified framework using a modified Euler equation with discounting. Because both theories differ in their local determinacy properties, we show analytically that the correlation of output growth and inflation can distinguish the two hypotheses in the data.

We leverage the Japanese experience at the ZLB to empirically assess our theory using a quantitative New Keynesian model that embeds both hypotheses. We offer a summary measure of the likelihood of each hypothesis using Bayesian prediction pools. We find evidence that Japan’s experience is consistent with the expectations trap model, but making such an assessment is subject to substantial uncertainty in the early part of the estimation sample. Consistent with our theory, the negative correlation between output growth and inflation is the key empirical moment that ultimately shifts the balance in favor of the expectations-trap hypothesis in Japan. Our quantitative findings extend to models that deviate from rational expectations, models that use inflation-expectations data, and more elaborate medium-scale models of the Japanese economy

Hedgopia: March Dot Plot Can Surprise Markets (nice visual of various QTs and FF)

… Until recently, fed funds futures traders priced in the easing cycle to begin in March. They now expect the first cut to occur in June, with December-meeting odds just about 50-50. By that meeting, they are betting on three 25-basis-point cuts (Chart 1). This would be in line with the December FOMC dot plot, in which members telegraphed three cuts in 2024, up from two during the September meeting.

… The Fed itself is confused. Minutes of the January 30-31 meeting were released Wednesday, and the officials indicated that they were in no hurry to cut rates. This is a slight change in tone from what was conveyed by Jerome Powell, chair, at the December-meeting press conference.

Since that meeting, the members have had an opportunity to consider several fresh data. Not only are economic data coming in stronger than expected but January’s CPI (consumer price index) and PPI (producer price index) both were hotter than expected, although the year-over-year disinflation trend in headline and core CPI since reaching four-decade highs in 2022 is intact (Chart 3).

WolfST: Mortgage Rates Rise Back to 7%, Housing Market Re-Freezes, Buyers’ Strike Continues. Prices Are Just Too High

WolfST: The Fed Wants to Drive QT as Far as Possible Without Blowing Stuff Up, and it’s Working on a Plan: FOMC Minutes

Finally, a live look at one group (expecting many rate cuts) view of a ‘SOFT LANDING’

I can't wait for Google-Gemini-AI to modernize the 1980 Miricle on Ice to 2024 WOKE Ideologies and reimagine those hockey players in a much more Diverse & Inclusive & Equitable fashion :)

I can't wait for Google-Gemini-AI to modernize the 1980 Miricle on Ice to 2024 WOKE Ideologies and reimagine those hockey players in a much more Diverse & Inclusive & Equitable fashion :)