Good morning … As the week draws to a close and fresh off heels of the long bonds birthday, I thought I’d start the day and end of the week with a slightly longer-term (WEEKLY) visual of 30yr yields …

30yy WEEKLY: resistance just beneath psychologically important 4.00% and we’re at / near resistance with momentum nearing an overBOUGHT condition …

… as bearish as the setup MIGHT seem otherwise (we’re back down TO … about where we were much of … 2016, 17, 18 … you get the point), one must keep in mind we’re down a couple bps on the week (so far) and if Fed CUTS with stocks high / rising (so, FCI easier and so, ‘easy does it to super-sized cuts’ and so, is current pricing of bullishness overdone?) will that in turn, reignite ‘flation and be long bonds kryptonite??

Clearly the world thinks anything NOT bond bullish here and now is to be crazy at this moment in time and, as always, I’d defer to those currently IN the game — CitiFX techAmentals noted HEREyesterday …

… US 30y yields: Yields are still holding above support at 4.06% (Feb low). Below that, the key support is at 3.94% (Dec 2023 lows).

… So many questions and so little time and my guess is the answer is NO (feel free to choose the question) and one thing I’m confident in is that the Fed rarely likes to disappoint the markets and will work this weekend on pricing for the upcoming meeting (18 Sep)…

… And as I’d imagine fewer and fewer eyeballs ‘round I’ll not labor the point / post too long as folks dropping kiddos off at schools and central bankers summer camp kicks off with Chair Powell’s welcome speech (KC Fed ‘itinerary posted last night and is HERE) and so, a quick look back at yesterday thanks TO …

ZH: Continuing Jobless Claims Hover Near 33-Month Highs (survey week so it matters and BERYL impacts fading … )

Initial jobless claims continues to drift along in the same range it has been in for three years (with NSA claims literally near record lows)...

ZH: 'Soft Landing Scenario Less Convincing': US Manufacturing PMI Plunges To 8-Mo Lows (so if NOT a soft landing then … ruh roh, RelRoy and why stonks headed … lower?)

… All told, by days end …

ZH: Stocks & Bonds Slammed Ahead Of J-Hole As FedSpeak Slows Rate-Cut Euphoria

...combined with commentary from FOMC members (as reported by media) that while they believe it’s appropriate for the US central bank to begin lowering interest rates soon, the pace of subsequent cutting should be “gradual” and “methodical.”

Boston Fed President Susan Collins said she’s not seeing any “big red flags” in the economy.

That’s the context in which I do see it soon being appropriate to begin easing policy,” she added.

“I think a slow, methodical approach down is the right way to go,” Philadelphia Fed President Patrick Harker says about the pace of interest-rate cuts.

“For me, barring any surprise in the data we’ll get between now and then, I think we need to start this process,” Harker says in a Reuters interview published Thursday, referring to the central bank’s upcoming September policy meeting.

...both of which suggest the path to lower rates may be a more gradual one than some in the markets may have been hoping for...

NEWSQUAWK: US Market Open: Equities gain whilst DXY & Bonds hold flat ahead of Fed Chair Powell … Bonds are in a holding pattern ahead of Fed Chair Powell … USTs are in a holding pattern into Powell, unchanged within a narrow range around the 113-10 mark and at the low-end of Thursday's 113-05+ to 113-27 band. Ahead of Powell, benchmarks have generally come under some very modest pressure as crude picks up to incremental session highs.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BARCAP: FOMC Minutes NLP Analysis: On the same page on many fronts, but important disagreement remains

Our NLP analysis points to participants being more aligned again: monetary policy agreement rose, confidence about disinflationary progress and labor market conditions was broad, but disagreement on a few important areas remains. Higher "other topic" count suggests FOMC monitors indicators for risks to the employment goal.

BARCAP: Existing home sales post first increase in five months

Existing home sales rose 1.3% m/m in July, to 3.95mn, the first increase since February, led by single-family home sales. That said, elevated mortgage rates remain a driving source of weakness for home sales, which continue to run under 4mn annualized despite July's uptick.

Fed speak at Jackson Hole will be key to fine tune policy expectations. Dovish price action across rates, equities and USD may see some travel & arrive. But the direction of travel is towards easier ed policy, which should preserve the soft landing narrative. Nvidia earnings next week will be another reality check for market

BARCAP: U.S. Equity Strategy: Food for Thought: Potential Catalysts to Watch

SPX forward volatility term structure illustrates how equity markets are keeping eyes on the Fed, jobs and inflation as a potential September rate cut looms. Despite some recent progress on 'broadening', we think heightened volatility around NVDA earnings indicates that Big Tech is not stepping out of the spotlight yet.

BMO Close: Dovish is in the eye of the beholder... (just ‘cuz … bearish front end bias ahead of JHOLE and weekend … interesting…)

…Treasuries cheapened on Thursday in a move that found justification in the economic data, although we expect that position-squaring was also an underlying motivation that saw 2-year yields edge back above the 4.0% threshold. Services PMI was the obvious trigger as the business sentiment measure surprised on the upside at 55.2 versus the 54.0 consensus. Moreover, the modest increase in jobless claims matched expectations at 232k and it was notable that there wasn’t a more significant spike for NFP-survey week. As the market settles into a holding pattern ahead of Friday’s Jackson Hole events, it strikes us that while rates are well off the lows, 10s remain comfortably below 4.0% and the shift in policy expectations which followed the July payrolls report appears to be holding for the time being.

We’re approaching Friday with a bearish bias for the front-end of the curve as the bar is now very high for Powell to outdo the dovish expectations evident in the magnitude of cuts priced in by the December meeting…

Bank of Japan Governor Ueda spoke to the Japanese Diet, and was inclined to be somewhat hawkish. There was an acknowledgement of the instability of financial markets, which is hardly surprising in the wake of recent volatility—including suggestions that BoJ action may have contributed to it. The yen strengthened modestly in the aftermath.

Central bankers’ Jackson Hole summer camp continues, with Bank of England Governor Bailey speaking. Bailey is already presiding over a rate easing process. The UK economy is more rate sensitive than some others (because of the mortgage structure) but less rate sensitive than in the past (because of demographics).

Federal Reserve Chair Powell is to speak on the “economic outlook”. That implies that Powell (or his speechwriters) will be forward-looking. Now would be a great opportunity to outline a medium-term vision. Powell’s track record suggests we will get “data dependency” and myopia…

Wells Fargo: Existing Home Sales Increase in July Lower Rates Enticed Buyers, but Sales Remained Sluggish Overall

Summary A Drop in Mortgage Rates Sparked Buyer Interest in July Existing home sales rose 1.3% in July, the first improvement in five months. This modest uptick was likely owed to a slip in financing costs the prior month. The 30-year fixed mortgage rate averaged 6.9% in June according to Freddie Mac, down from 7.1% in May. That said, resales are moving at a sluggish pace as elevated mortgage rates remain a prohibitive expense for buyers. Firm price appreciation is also adding to the affordability challenge. The median single-family resale price rose 4.2% annually in July, an acceleration from June's 4.1% growth rate. According to the National Association of Realtors, homebuyers in Q2-2024 needed household incomes of at least $108,600 to qualify for the median priced resale home, up from $57,888 in 2021. Single-family inventories, meanwhile, continue to grow. After seven consecutive monthly expansions, the count of homes for resale in July rose nearly 22% above its level one year ago.

Mortgage rates have retreated further in recent weeks as markets anticipate the Fed to start easing policy in September. The average 30-year rate dipped below 6.5% the first week of August, reaching its lowest level in 15 months. This downtrend may result in further bumps to existing home sales in the coming months. Yet as explored in our latest housing market outlook, affordability conditions are unlikely to improve drastically, and slowing job and income growth will likely limit the potential for a full-fledged housing market recovery. We expect mortgage rates will continue to decline once the Fed starts cutting interest rates this fall, however we do not forecast that they will dip much lower than 6.0% by the end of next year.

Source: NAR and Wells Fargo Economics

Wells Fargo: The Economics of College Football: 2024 Edition Conference Realignment and Expanded Playoffs Bring New Look to College Football

Summary That Chill in the Air Means College Football is Upon Us

Summer is winding down and fall is just around the corner. Before the tree leaves change color, temperatures dip and pumpkin spice finds its way into everything, what better way to mark the transition into autumn than to dive deep into the upcoming college football season and the regional economies the top teams call home?

Yardeni: US Economy Still on Bullish Track (so then where’s Team Rate HIKE?? or at least Team Cut LESS)

Stock traders took some profits today. They were probably nervous that Fed Chair Jerome Powell will be less dovish tomorrow than the markets are about the outlook for rate cuts beyond 25bps in September. We've been less dovish than the markets since mid-June because we've been more bullish on the economy and the labor market than the consensus.

Today's economic releases showed the US economy continues to chug along. The services-providing sector remains strong, and there are even green shoots sprouting in housing. Abroad, there's some optimism percolating that real growth may be improving in Europe. Nevertheless, we continue to favor the US over the Eurozone. The US has a much more compelling growth story, in our opinion. Here's more:

(1) Unemployment claims. We've been keenly focused on jobless claims, Challenger layoffs, and the JOLTS reports for confirmation that the labor market remains resilient. Today's jobless claims report was a good one for us. Initial claims rose 4,000 to 232,000 (sa) in the week ended August 17, while continuing claims fell 1,000 to 1.863 million (chart). The insured unemployment rate, which is based on state unemployment insurance claims remains at just 1.2%. The latest claims data cover the survey week for this month's employment report and raises the possibility that August's unemployment rate might surprise with a downtick.

(2) Purchasing managers surveys. Today's August flash PMI report from S&P Global for the US showed that the NM-PMI rose from 55.0 in July to 55.2 this month, while the M-PMI fell from 49.6 to 48.0. Prices charged for goods and services rose at their second slowest pace since June 2020. This all aligns with our view that the services economy's strength is still offsetting the rolling recession in goods, and that disinflation prevails…

… And from Global Wall Street inbox TO the WWW,

AAA: Pump Prices Plunge, But Plug-In Prices Persist (hmmm this would seem to ME to be anti green new deal am certain NOT something that will come up in the speech tonight OR be recognized as a thing … you know, like … the BLS)

… Today’s national average for a gallon of gas is $3.38, 12 cents less than a month ago and 47 cents less than a year ago.

BESPOKE: MORTGAS Misery (funtertaining look at high mortgage rates AND gas prices, combined)

… Combined, our MORTGAS Index currently sits at 10.2. As shown below, the index is down 1.46 points from its record high of 11.66 seen in late 2023, but it's still extremely elevated relative to the last 20 years. Looking on the bright side, the index is now back below its peak seen in 2008 during the Financial Crisis, but we're going to need to see significant further easing to get back to the 20-year average of 7.62. A drop like that would likely mean mortgage rates falling at least into the 4-5% range and gas prices remaining closer to a 2-handle than a 4-handle.

Bloomberg: Quantitative Tightening Goes Global for the First Time, in Test for Markets

Central banks have moved to slim their balance sheets

Investors on watch for volatility, see QT adaptation if needed

… “Problems could arise again at the Fed, while other central banks have not been tested yet,” said Steven Barrow, who’s worked as a foreign-exchange and fixed-income strategist for four decades and serves as head of G10 strategy at Standard Bank in London.

Many on Wall Street anticipate the Fed’s QT program only has months to go, as the US central bank shifts to cutting interest rates to help support the economy. The Fed already in June eased the pace at which it’s shrinking its bond portfolio…

Bloomberg: Money-Market Funds Have Lured $106 Billion So Far This Month

Total assets rose to record $6.24 trillion as of Aug. 21: ICI

Increase led by retail investors positioning ahead of Fed cuts

… US money-market funds lured another $24.9 billion in the week through Aug. 21, according to the latest Investment Company Institute data. That brings this month’s inflows to roughly $106 billion, pushing total assets to a series of all-time highs. In all, about $6.24 trillion of cash is sitting in the funds.

Much of the latest increase in money-market fund assets came from retail investors, which totaled $21.4 billion. Institutional investors added about $3.45 billion, offset by an exodus from the prime space — a response to a set of Securities and Exchange Commission regulations slated to take effect later this year, which has caused some funds to shutter and investors to shift around their allocations…

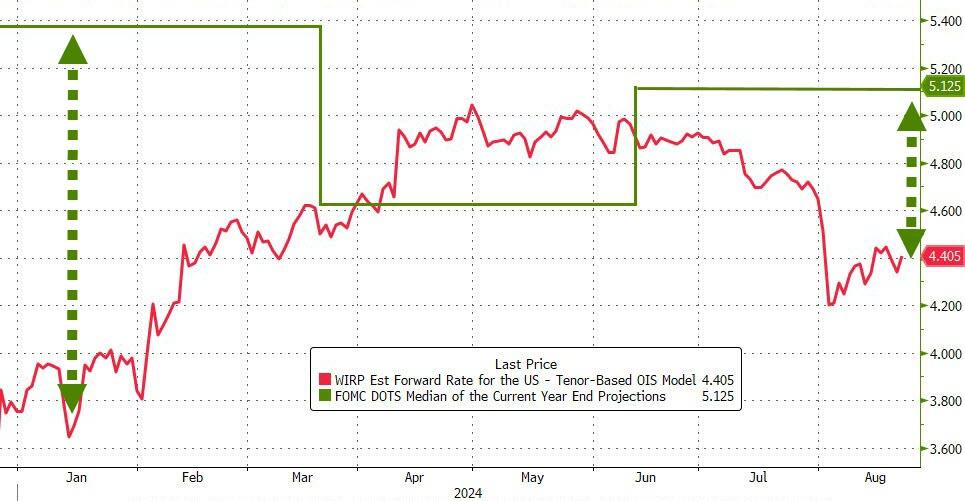

Market bets on when, and by how much, the Federal Reserve will be cutting interest rates this year have been rapidly shifting since investors last heard from Jay Powell on July 31.

As markets sold off on Aug. 5, odds quickly rose as high as 70% that there would be a 50 basis point interest rate cut by the end of the Fed's September meeting.

As of Thursday afternoon, markets were pricing in just a 25% chance the Fed cuts rates by that much next month.

Several economic updates showed rising recession fears may have been overdone in the wake of a weak July jobs report, which began the process of investors paring their bets.

Then on Thursday, after Philadelphia Fed president Patrick Harker told CNBC the Fed should ease rates "methodically and signal well in advance," the odds dropped further.

Still, markets are pricing in four cuts from the Fed this year, and there are only three meetings left. For those forecasts to come through, the 0.50% cut will have to be found somewhere.

We'll see what Powell has to say about that this morning.

Finally, a look at what happened to markets YESTERDAY (from ‘The Hole’) …

Gas price in my little corner of the world now (Susanville, NE CA) is $4.99. But after a brief 85 mi run to Reno Costco gas was $3.97 Tuesday. Always nice to avoid CA-gasflation taxes loved by our homegrown talents of Gavin & Komila :)

It's rather unsettling all of the Ivy League, U of Chicago & Stanford graduates on that agenda. Kamala's father was a Stanford Communist econ professor, who even knew such things were being taught in the US? Although I'd argue Keynesian is commie Econ by another name, Lord Keynes himself basically says so-IN GERMAN. However having the deposed former BoE semi-hawkish Chief Bailey speak at the hole' is quite the get!

Gas price in my little corner of the world now (Susanville, NE CA) is $4.99. But after a brief 85 mi run to Reno Costco gas was $3.97 Tuesday. Always nice to avoid CA-gasflation taxes loved by our homegrown talents of Gavin & Komila :)

It's rather unsettling all of the Ivy League, U of Chicago & Stanford graduates on that agenda. Kamala's father was a Stanford Communist econ professor, who even knew such things were being taught in the US? Although I'd argue Keynesian is commie Econ by another name, Lord Keynes himself basically says so-IN GERMAN. However having the deposed former BoE semi-hawkish Chief Bailey speak at the hole' is quite the get!