while WE slept: USTs 'contained' w/i 6tick range; "...the recent rebound in risk sentiment would, all else equal, argue against more aggressive action..." -DB

Good morning … What is left to be written, read, seen and heard ahead of Friday’s Jackson Hole speech?

Serious question.

Follow up that question with another.

Can something you hear / read / see / hear between now and Friday morning change outcomes 3mo or 3yrs down the road OR are wheels already set in motion and signposts everywhere for us to see.

Or can that something change your mind and in turn, have you change your positioning?

I’m going to take the UNDER that can happen and will go out on a limb that JPOW & Co have little insight to offer in addition to what you may already know and have thought.

We came in to the year with bond jockeys pricing in 7 rate cuts. That was not ever going to happen.

Team Rate Cut is now reducing it’s bets to something far less…

DataTrek (Sunday): Jackson Hole “Drift”, Initial Claims, Fed Funds Odds

… Last week, the odds of at least one 50 basis point cut in the next 4 months dropped from 75 to 59 percent. Much of that decline was due to Thursday’s better than expected Advanced Retail Sales (+1.0 percent versus expectations of +0.3 pct) and Initial Claims report, as discussed above. Even with these reassuring datapoints, however, Futures still give slightly better than 50:50 odds of at least one 50 basis point cut later this year. In good news for both Chair Powell ahead of his Friday speech and markets, Futures don’t think the September meeting will see that large a reduction in rates (odds of just 25 percent). The debate over 25 or 50 basis point cuts can wait until later this year…

… Whatever the case may be, and being now far removed from the very day to day battles of markets (rates, stocks, 60/40 or 70/30 or whatever it’s become), I’ll continue to try — more oft than not in vein — to find something (of a chart or some words of wisdome from the sellside) of interest.

Perhaps an inflection point (outright, momentum shift readily apparent) and then … there are times like these when you wake up and long bonds are 4.124%, aggressively UNCH …

30yy: support up nearer 4.30 & 4.45% and resistance down closer to 3.97% …

… with momentum having crossed at / near lows in yield and now without an clear signal (unless I tried to over interpret it and then I’d say it continues to lean on upward pressure to yields …)

… and these prices / yields are, as always, a direct result OF some of the inputs … a sum of the parts, if you will, where one part was LEI …

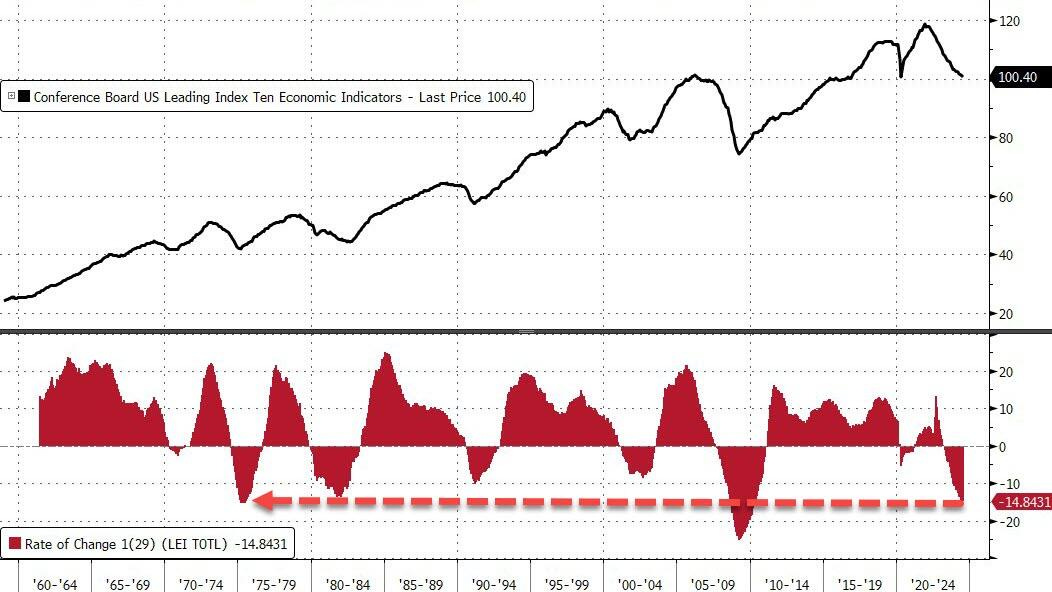

ZH: US Leading Economic Indicators Plunge For 29th Month - Worse Than COVID Lockdowns

… ...and the head of The Conference Board says 'nothing to see here'...

“The LEI continues to fall on a month-over-month basis, but the six-month annual growth rate no longer signals recession ahead,” said Justyna Zabinska-La Monica, Senior Manager, Business Cycle Indicators, at The Conference Board.

For context, outside of the great financial crisis, this is the worst decline in LEI since the mid '70s!!!

She goes on to explain just what a shitshow the data is...

“In July, weakness was widespread among non-financial components. A sharp deterioration in new orders, persistently weak consumer expectations of business conditions, and softer building permits and hours worked in manufacturing drove the decline, together with the still-negative yield spread."

… leading me to initially / knee-jerk ask … #GotBONDS?

That might have been almost true reflex and by days end yields ended down a touch (or virtually / aggressively UNCH, if you will) and stocks were bid, extending the winning streak … 8d in a row. Quite a feat!

US equities rallied for the 8th straight day today (amidst little major macro news here or abroad despite Leading Indicators slumping for the 29th straight month), with Nasdaq up 13% off its post-yen-carry-chaos lows - the longest win streak since Nov 2023 - as investors position ahead of Friday's scheduled speech from Fed Chair Powell and amidst a traditional low liquidity, vacation period for stocks in these last 2 weeks of summer…

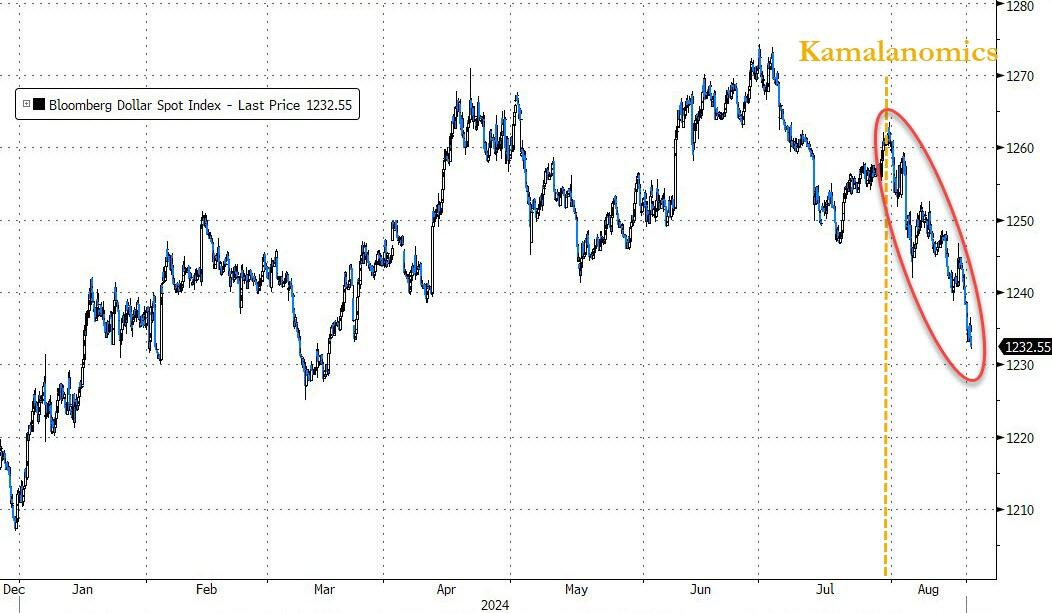

… The dollar continued its collapse, as the DNC unveiled its Kam-unist manifesto...

… given there is not much ‘there’ there on Global Wall Street trading desks OR, frankly, the buy side, as folks are making those annual trips to drop kids off at school and getting those last minute summers OVER holidays IN … and so, making too much of these moves and moments ahead of … well, September, really … likely only a for those who are extremely bored.

Which is likely what finds you here. Reading this … here is a snapshot OF USTs as of 655a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities take a breather following the prior day's strength, DXY flat & XAU makes a fresh ATH; Fed speak due … Bonds are incrementally firmer, Bunds dipped slightly on German Producer Prices but then edged higher as the morning progressed … USTs are contained within a thin six-tick range with the benchmark yet to lastingly deviate from the unchanged mark. Data docket remains light, but Fed speak sees Barr and Bostic later today.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

DB US Economic Notes - Data DBrief: Easier FCIs say easy does it to super-sized cuts

In this note, we use our high frequency version of the Fed's FCI-G to provide an update on recent moves in financial conditions and quantify their impact on expected growth. The recent market moves have, on net, more than unwound the tightening from the market turmoil after the weaker-than-expected July jobs report on August 2. Indeed, the baseline 3-year lookback version is now outright easy for the first time since June 2022.

Market participants will be looking to Chair Powell's speech at Jackson Hole on Friday for clues about the pace of rate cuts going forward. While there are good arguments on both sides for starting with 25bp cuts versus going with 50bps (see "Outlining the cut strategy: how much action in Jackson?"), the recent rebound in risk sentiment would, all else equal, argue against more aggressive action.

…Details within the CPI and PPI point to 0.15% core PCE print

HSBC: The Major bond letter (dated August 14 but still worth a look) #52. Turning points

… So, what does it all mean for bonds? The regional bank stress of 2023 shows bond yields quickly returned to their starting point just a few months after the first concerns became known (see chart). Investors are asking whether the carry trade unwind is the real deal, where yields keep falling in anticipation of a recession that is close, like in 2001, 2008, and 2020?

Two-year US Treasury yields fell a lot through these three recessions – all of which were preceded by an inverted curve, and whilst there may be some causal link in the first two, nobody is seriously claiming the inversion caused the shutdown of the global economy in 2020.

The point is that yields fell significantly. In the first of the three recessions this century, from a prior peak of 6.91% (18 May 2000), the two-year yield fell through the following three years, reaching a low of 1.08% (13 June 2003). For the second, it fell from 5.10% (12 June 2007) to less than 1.0% three years later. And, in the third, yields fell 100bp in two months and stayed there for over a year.

Historical total returns show that bonds can perform well when other asset classes do not. This is what they are supposed to do: provide an income from coupons that beats inflation and act as the hedge in a portfolio. Ideally, they should not be correlated to the other asset classes.

Using benchmark indices, the total return2 from the yield peak for the following one year in 2000 was +12.6% for bonds and -9.0% for equities. From 2007, the equivalent numbers were bonds +10% and equities -8.35%.

The outperformance of bonds versus equities belies the wider context. The first, which was based on overvaluation in one part of the stock market, didn’t ultimately hurt people’s wealth as much as the second, where the expensiveness of the property market was exacerbated by excessive leverage in some cohorts of it. The lesson is that bonds did well in two completely different economic scenarios, one where the recession turned out to be relatively benign (2001), and the other, a prolonged and painful downturn (2008)…

US politicians are politicking. At the margin, Vice President Harris’s endorsement of the proposed increase in US corporate tax rates might seem to be market relevant. However, listed companies are not always that sensitive to headline corporate tax rates. Otherwise, this is still mainly political theater (obviously, were Taylor Swift to do an impromptu concert in Chicago, the theater would become serious).

Oil prices fell a little on reports that Israel had agreed to the outline of a US proposed ceasefire. Hamas has not, as yet, agreed. The humanitarian consequences of any ceasefire are obviously important, the market consequences less so.

Ahead of the Jackson Hole central bankers’ summer camp, there are two Federal Reserve speakers (Barr and Bostic). The Fed is late in cutting rates, though this will not be publicly acknowledged. It is unlikely that either will change market expectations for a September rate cut, although they might influence expectations about the pace of rate reductions…

Wells Fargo: Mis-Leading Index? LEI Breaks Through Pandemic-Era Low

Summary The outlook for a soft landing is still in play, and the Leading Economic Index continues to signal otherwise. The LEI declined 0.6% in July, bringing the streak to 29 consecutive months without a gain. At 100.4, the index has now fallen below the prior cycle's low reached in April 2020

…The Coincident Index came in flat on the month at 112.5. The index, a gauge of how the economy is currently performing, has been consistently increasing on trend since it began recovering from the 2020 recession. The recent positive trend for the Coincident Index in tandem with the persistently pessimistic trend in the LEI has led the Coincident-to-Leading Index ratio to increase exponentially. Ratio values greater than one signal that the outlook for the economy is comparatively worse than current economic performance, and vice versa. The ratio sits at 1.12 in July, signaling that the outlook for the economy is significantly more negative than the present situation (chart). This is the highest the ratio has been since 2009 in the trough of the Great Financial Crisis. The ratio usually peaks at the end of a cycle prior to a rebound in economic growth, a signal that the economy could be poised for decent growth in the quarters ahead.

Source: The Conference Board and Wells Fargo Economics

Wells Fargo: Will Lower Mortgage Rates Ignite the Housing Market? Affordability Headwinds Stand to Keep a Ceiling on Activity

Summary Housing Market Outlook Brightening, but Clouds Still Present The adverse impacts of higher mortgage rates and increased home prices continue to reverberate across the housing market. The U.S. economy is still expanding, but home sales remain in a deep lull reminiscent of the aftermath of the Great Recession. A dip in mortgage rates as the Federal Reserve pivots to a less restrictive stance of monetary policy could improve affordability and provide a needed jolt to the residential sector. The recent National Association of Realtors settlement changing the way that buyer-agent commissions are set may also incentivize some buyers and sellers to emerge from the sidelines. A full-fledged rebound in home sales still seems improbable given affordability conditions are likely to remain unfavorable as a result of strong underlying demand, scarce supply and a less-robust macroeconomic environment.

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Global Stocks Set for Longest Win Streak of 2024: Markets Wrap Bloomberg: Oil Extends Drop as Middle East Push, China Demand Worries Weigh

… Oil has surrendered most of its year-to-date gains as the lift from OPEC+ supply curbs and expectations for lower US interest rates have been countered by China’s challenging outlook. The Organization of the Petroleum Exporting Countries plans to restore some barrels next quarter, although that could change if prices keep falling, and balances for next year look oversupplied.

Options are signaling the market is now anticipating a lower risk of futures spiking. Brent option skews have returned to their usual bias toward puts — which profit from lower prices — for the first time in two weeks.

Finally, me watching some of the speeches last night trying to infer something economical to it all …