On this day in 2020 just as Initial Jobless Claims were coming out — and no bueno — PPI was weak — the Fed dug deep into its bag of tricks (aka yer and my back pocket — which totally seemed like a great idea at the time) and found yet another set of ‘tools’ to use, buying junk bonds, munis and more. Some links for historical context …

Bloomberg: Fed Is Seizing Control of the Entire U.S. Bond Market

In a dramatic move, the central bank extends its reach into munis, fallen angels and more.

… Calling the Fed’s actions “throwing the kitchen sink” at the bond markets seems like a huge understatement. It’s extending its reach into everything, which is probably fine for now. The tricky part will be knowing when and how to let go.

ZH: The Day The Fed Nationalized The Bond Market: The Complete Summary Of Everything The Fed Did Today …

… Until we wait here is a complete summary of everything the Fed announced this morning, when it released the details of the $2.3 trillion in loans and purchases to "support the billionaires economy", which will consist of:

Main Street Lending Program,

Paycheck Protection Program Lending Facility,

New Municipal Liquidity Facility,

Expansion of existing primary and secondary corporate bond buying facilities.

These Fed's loans and facilities are based on the additional capital the Treasury has made available under the CARES Act (see below). Of the total $454bn that Congress appropriated to backstop Fed facilities, this morning’s announcements commits $195bn, leaving the majority of funds available for other purposes - like stocks - or to expand these programs if necessary. That said, the programs the Fed announced this morning cover essentially all of the areas in which we have expected the Fed to act, so we do not expect the Fed to announce any further facilities for the time being…

3yy DAILY: momentum on verge of BULLISH CROSS, watching 4.75% (psychologically important ‘round number’) and a ‘good’ CPI would then bring bigger resistance (4.65%) into play … WATCHING

… A similarly BULLISH setup can be viewed on a WEEKLY chart and so, suffice it to say, CPI matters … and you likely didn’t need ME to guess that.

That said, we’ll have to wait ‘til tomorrow for that but earlier today …

NFIB (March): Small Business Optimism Reaches Lowest Level Since 2012

The NFIB Small Business Optimism Index decreased by 0.9 of a point in March to 88.5, the lowest level since December 2012. This is the 27th consecutive month below the 50-year average of 98. The net percent of owners raising average selling prices rose seven points from February to a net 28% percent seasonally adjusted.

“Small business optimism has reached the lowest level since 2012 as owners continue to manage numerous economic headwinds,” said NFIB Chief Economist Bill Dunkelberg. “Inflation has once again been reported as the top business problem on Main Street and the labor market has only eased slightly.”

Key findings include:

The net percent of owners who expect real sales to be higher decreased eight points from February to a net negative 18% (seasonally adjusted).

Twenty-five percent of owners reported that inflation was their single most important problem in operating their business (higher input and labor costs), up two points from February.

Owners’ plans to fill open positions continue to slow, with a seasonally adjusted net 11% planning to create new jobs in the next three months, down one point from February and the lowest level since May 2020.

Seasonally adjusted, a net 38% reported raising compensation, up three points from February’s lowest reading since May 2021…

… INFLATION The net percent of owners raising average selling prices rose 7 points from February to a net 28 percent seasonally adjusted. Twenty-five percent of owners reported that inflation was their single most important problem in operating their business (higher input and labor costs), up 2 points from February. Unadjusted, 13 percent (down 3 points) reported lower average selling prices and 43 percent (up 6 points) reported higher average prices. Price hikes were most frequent in the finance (61 percent higher, 10 percent lower), retail (54 percent higher, 6 percent lower), construction (51 percent higher, 4 percent lower), wholesale (50 percent higher, 17 percent lower), and transportation (44 percent higher, 0 percent lower) sectors. Seasonally adjusted, a net 33 percent plan price hikes in March (up 3 points).

… AND … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher and tracking gains in Gilts and Bunds this morning ahead of this afternoon's first leg of the Treasury mini-refunding. DXY is modestly lower (-0.10%) while front WTI futures are little changed (+0.2%). Asian stock were mostly higher, EU and UK share markets are mostly lower (SX5E -0.85%) while ES futures are showing -0.1% here at 6:45am. Our overnight US rates flows saw good action in the front-end during Asian hours (TU->TY block flattener posted) but little in the way of cash flows. During London hours, dip buyers re-emerged and concentrated on 7's out to the long-end- helping to flatten the curve. Overnight Treasury volume was ~115% of average overall and quite high in 2yrs (235%), relative average basis.

… Up above there is an article discussing how the recent buoyancy in commodity prices may reflect still-percolating US growth while adding upside impetus to inflation. Our first attachment shows the Bloomberg Commodity Index (BCOM) in a long-term, monthly chart format. We've posted and discussed this picture recently, but we wanted to hammer home how we believe that commodities may have begun a sustainable rally in recent weeks. We infer that from the momentum set-up in the lower panel where the once chronically oversold, medium-term momentum study (Slow Stochastics) has begun to flip upward, confirming a multi-year trend reversal. This is a great-looking, long-term chart and one of the few long-term charts with a clear signal right now.

On duration, this daily chart of Treasury 2yr notes looks like those for its benchmark peers. 2yr rates are holding above their former range support (~4.735%, as drawn in) but beginning to get tactically oversold (lower panel) in doing so. Such a set-up is a tricky one tactically, but what can't be denied is that the bear trends in place since late last year continue to dominate the price action... On this, bond bulls really want these multi-month bear trendlines taken out before dreaming about a sustained push to lower rates... Absent that, 4.735% to 4.98% may be your new range for 2's, for now.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: DXY nears 104.00 after BoJ sources, XAU at ATHs; docket ahead sparse … Fixed income benchmarks bid with EGBs outperforming, no reaction to supply but latest ECB BLS perhaps factoring

In this note, we discuss why the Fed will likely need to see 0.2% core PCE prints over the next few months to deliver an initial rate cut in June. We also discuss the potential implications of firmer near-term inflation prints for the broader prospects of rate cuts in 2024 and 2025. This builds on our work framing this cycle as a two-stage process beginning with insurance cuts or a mid-cycle adjustment (see "(Mid-cycle) Adjusting the Fed's narrative for rate cuts").

… So what does the Fed need to see to be comfortable cutting rates in June? The March SEP provides a reasonable starting point for this assessment. The median forecasts showed an expectation for three rate cuts this year – though this was clearly a close call with one dot determining the outcome – with core PCE inflation ending the year at 2.6%. That latter outcome is consistent with a 19bps run rate through year end.

While there is a caveat that the details of these prints will matter for rate cut timing (e.g., the Fed will be more concerned if elevated inflation if driven by shelter or super core than volatile spikes in core goods items), we do not think that 0.3% prints over the next two months would be consistent with a rate cut at the June FOMC meeting. Instead, we think the Fed needs to see core PCE prints that are at least as good as 0.2% monthly readings over the next few months to have sufficient confidence to reduce rates in June.

There are a few reasons for our view:…

DB: Mapping Markets: What last week can tell us about the quarter ahead

Last week was an eventful one for markets, which included fears of a geopolitical escalation along with growing concerns about inflation. In response, markets had a weak performance, and the S&P 500 posted its worst week since January, whilst the 30yr Treasury yield saw its biggest rise since October

… In light of this, we look at some lessons that last week holds for the quarter ahead.

1. Markets are clearly very concerned about the prospects of a geopolitical escalation and an inflation shock …

2. Although rate cuts are being priced out, the main question is still around how quickly any cuts might happen, rather than if there’ll be another hike. 3.There are growing signs that the global economy is starting to accelerate again. 4. Although the US CPI release for March is in focus this week, it won’t necessarily provide a resolution about the prospect of a June cut.

5. Last week added to signs that an ECB rate cut could happen in June, but we know from history they don’t have to follow the Fed. 6. Finally, we know from Q1 that the first week of the quarter doesn't necessarily signal where things are headed for the rest of the quarter.

We expect a 0.27% increase in March core CPI (vs. 0.3% consensus), corresponding to a year-over-year rate of 3.70% (vs. 3.7% consensus). We expect a 0.29% increase in March headline CPI (vs. 0.3% consensus), which corresponds to a year-over-year rate of 3.37% (vs. 3.4% consensus). Our forecast is consistent with a 0.28% increase in CPI core services excluding rent and owners’ equivalent rent and with a 0.21% increase in core PCE in March. We will update our core PCE forecast after the CPI is released and again after the PPI is released.

We highlight three key component-level trends we expect to see in this month’s report. First, we expect airfares to decrease by 3.0% following last month’s 3.6% jump, reflecting somewhat lower jet fuel prices and a decline in our airline team’s real-time measure of airfares. Second, we expect both used and new car prices to decline in March, reflecting rebounding promotional incentives and declining used car auction prices. Third, we expect shelter inflation to slow somewhat relative to last month (we forecast rent to increase by 0.37% and OER to increase by 0.45%), as the gap between rents for new and continuing leases continues to close.

Going forward, we expect monthly core CPI inflation to slow to 0.20-0.25%. We see further disinflation in the pipeline in 2024 from rebalancing in the auto, housing rental, and labor markets, though we expect small offsets from a delayed acceleration in healthcare and single-family rent growth continuing to outpace multifamily rent growth. We forecast year-over-year core CPI inflation of 3.0% and core PCE inflation of 2.4% in December 2024.

A broadening in cyclical leadership suggests the market is moving to the "no landing" scenario. We recommend staying up the quality curve within cyclicals and reiterate our OW stance on Energy, which we recently upgraded. Equities are becoming increasingly correlated to yields into CPI this week.

… Rates Have Pushed Higher; What Does It Mean for Equities?...Three weeks ago, we noted that ~4.35% on the 10-year US Treasury yield would be an important technical level to watch for signs that rate sensitivity may increase for equities. On Tuesday of last week, the 10-year yield pushed above that level for the first time this year and equities' rolling correlation to bond yields did drop further into negative territory as stocks sold off. Small caps and low quality stocks underperformed on the day and the week, supporting our view that these areas of the market continue to exhibit greater rate sensitivity than large caps particularly in upside moves in yields. In our view, while rate sensitivity would likely increase more broadly if we were to see a sustainable move above 4.35-4.40 on the 10-year, we would still expect large cap, quality equities to outperform on a relative basis.

… Three weeks ago, we noted that 4.35-4.40% on the 10-year US Treasury yield would be an important technical level to watch for signs that rate sensitivity may increase for equities. On Tuesday of last week, the 10-year yield pushed above that level for the first time this year and equities' rolling correlation to bond yields did drop notably as stocks sold off. Small caps underperformed on the day and the week, supporting our view that small caps continue to exhibit greater rate sensitivity than large caps particularly in upside moves in yields. The 10-year finished the week right around 4.40% making this dynamic a focal point of near-term price action ahead of Wednesday's CPI release.

The market calendar is mainly noise. Quite a lot of that noise has come from Federal Reserve members. Investors can pick whichever view they want, to confirm whatever preconceived policy views they hold. Recent remarks offer a choice of three rate cuts, vigilance against inflation, or too soon to cut rates. The range of views matters less than in the past, given the Powell Fed’s weird unanimity of decision-making…

…The US NFIB small business sentiment poll is run by an organization that lobbies politically. In an increasingly polarized US society, political bias is an increasing risk for survey-based evidence. The level of sentiment is typical for a Democrat White House.

The number of people going to Broadway shows has been rising faster than normal in recent weeks, likely driven by the strong labor market and strong household gains in financial wealth and housing wealth.

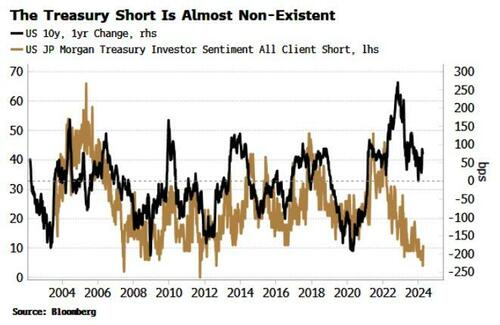

Bloomberg(via ZH): Hardly Anyone Is Short Treasuries; Perhaps They Should Be

… JP Morgan’s Treasury Survey tracks their clients’ positioning in Treasuries, asking them whether they are long, neutral or short. The net of the positions is close to flat, but outright shorts are unusually low, with the number of clients saying they are positioned that way near the nadir for the 20-year history of the survey.

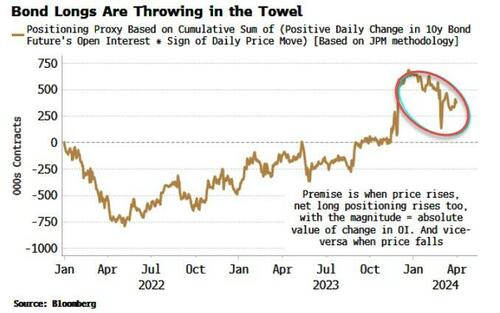

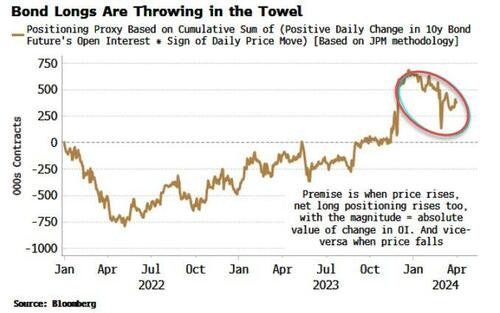

The Commodity Futures Trading Commission’s Commitment of Traders data has speculators net short Treasuries, but this is hugely distorted by basis trading (i.e. cash bonds versus futures). However, a position proxy for bond futures (see here) shows positioning is falling but is still net long.

(This proxy, whose methodology is explained in the chart, circumvents the distortion to Commitment of Traders data from the basis trade, i.e. trading the cash bond versus the future.)

Bloomberg(another from ZH): Yields To Stay Elevated As Inflation Emboldens Short Bond Trade

… Another proxy for bond positioning shows that longs in 10y notes have been falling quite rapidly from their highs at the end of the last year. Furthermore, JP Morgan’s Client Treasury Survey shows outright shorts at almost series lows.

The overall message is that bond traders have been reducing longs as recession risk has receded, but they have not yet gone net short en masse. However, the inflation picture is likely to soon change that.

This week’s inflation data has a risk tilt, in that a lower-than-expected print is unlikely to prompt a stampede of fresh longs, but data that is above expectations could see any lingering doubts about going short bonds adamantly put to one side.

Bloomberg: Food Prices Are Up. What Else Is New? (Authers’ OpED … just one of his charts ahead of tomorrows CPI)

Still, it’s a stretch to think Biden can do much about them when no president before him could, either. Plus: Blackstone and REITS; China demand

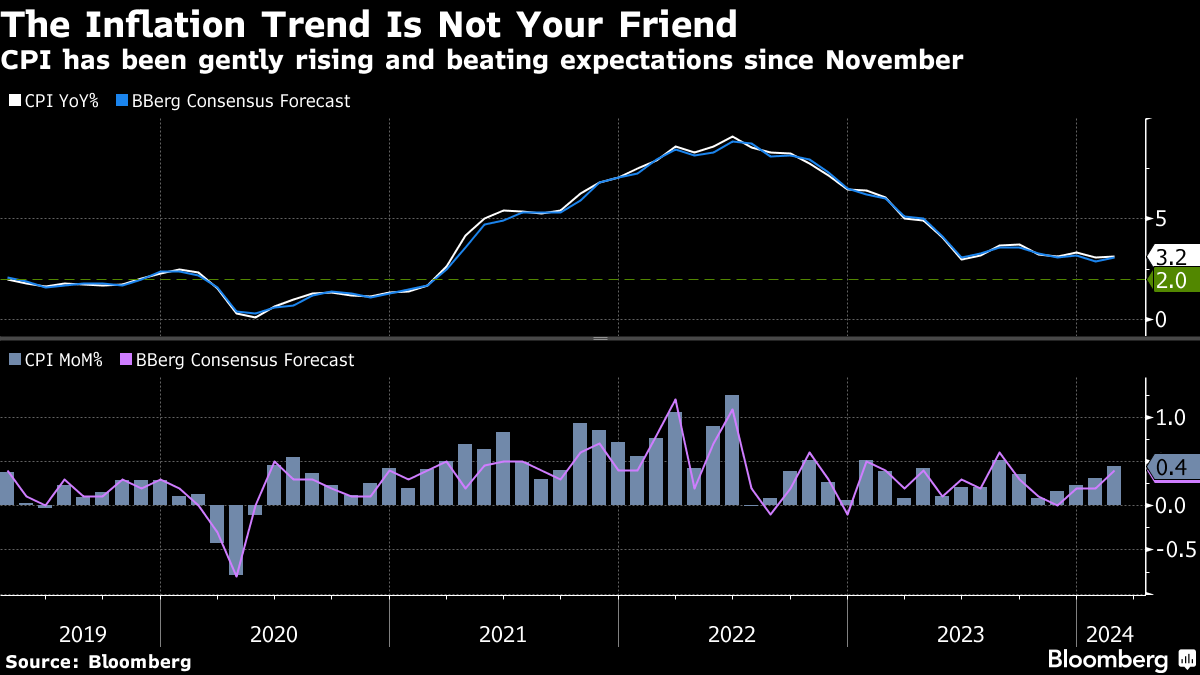

… That’s a shame because there is a recent distressing trend of rising month-on-month inflation that beats expectations, as illustrated here with a terminal chart:

Despite the way the world was taken unaware by the spike in inflation that took shape in the year after the pandemic, forecasters have done a better job than many realize…

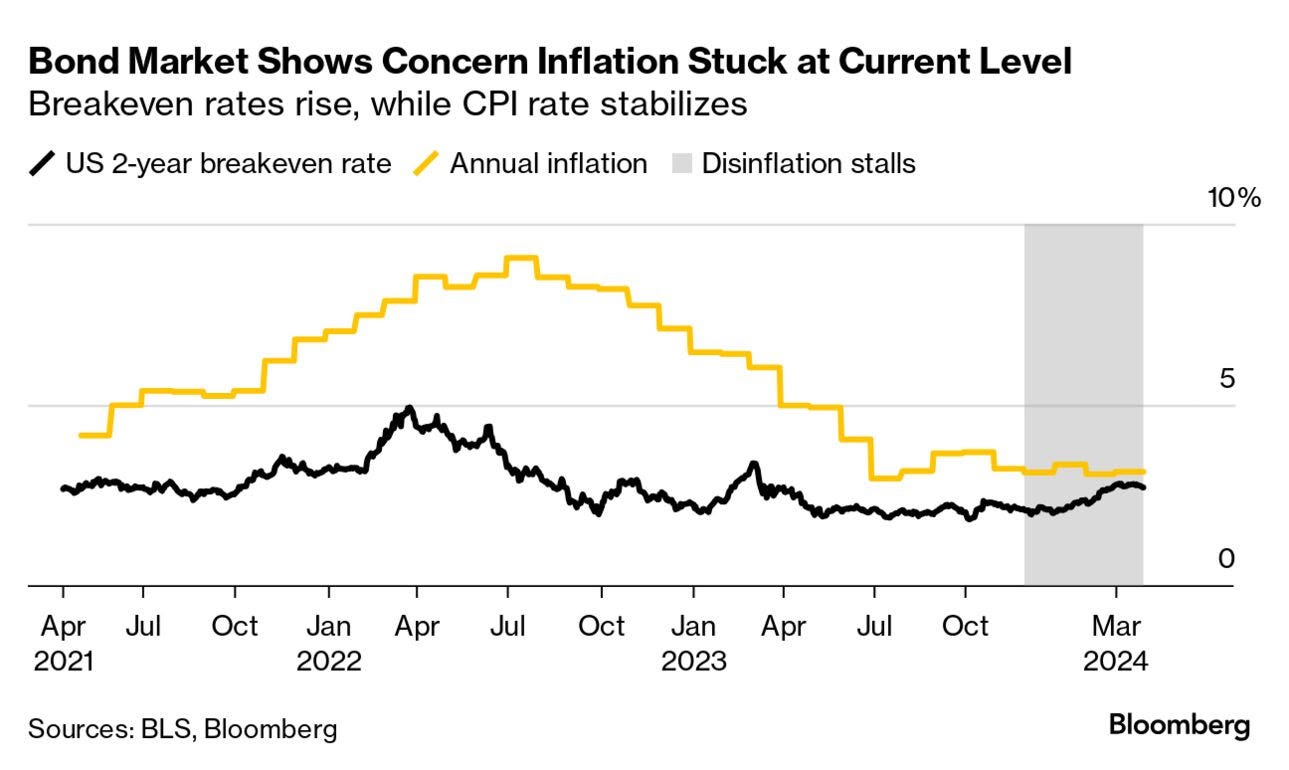

Bloomberg: 5 Things You Need to Know to Start Your Day (Asia — chart of 2yr breaks)

… The Treasury market is palpably on tenterhooks going into this week’s inflation release, especially after payrolls joined the long list of data reports to come in stronger than expected. There’s plenty at stake, and it would take a substantial miss to the downside to restore calm.

Yes, the pace of consumer-price gains is expected to ease, but only slightly, and even the most optimistic forecast still sees headline annual inflation remaining above 3%. That underscores concerns that the last mile or two of the Federal Reserve’s efforts to tame cost pressures will prove to be not only “bumpy” (as Chair Jerome Powell puts it), but long. Surging oil and other commodity prices aren’t helping, and the same goes for supply disruptions that threaten to undo the goods disinflation that has helped cool costs in the economy.

Annual headline inflation briefly touched under 3% last June and has since held above that level, while the pace at which gauges are descending also lost momentum. And at the same time, this year in particular has seen the bond market’s main measures of inflation expectations pop right back up. The two-year breakeven rate — the gap between yields on two-year Treasury Inflation Protected Securities and those on regular notes of the same maturity — is sitting at 2.84%. If average inflation does come in at that level then it’s possible the Fed doesn’t reach its target in that time frame. That casts doubt on the capacity of policymakers to deliver on their projected six rate cuts through the end of next year.

FirstTrust: Monday Morning Outlook - Is the Fed Tight, or Not?

… Think of it this way: imagine you’re trying to freeze water, at sea level. A thermometer shows the temperature is 25⁰F and the water isn’t freezing. Does this mean the laws of chemistry and physics have been repealed? Of course not! Any sensible person would think that the thermometer must be broken, or maybe the liquid you’re trying to freeze isn’t water after all.

Which brings us to one signal of monetary tightness that hasn’t been triggered yet. History suggests that interest rates should be roughly equal to “nominal” GDP growth (real GDP growth plus inflation) – a cousin to what is called the “Taylor Rule.” Nominal GDP is up 5.9% in the past year and a 6.5% annual rate in the past two years. Yet, the federal funds rate is just 5.4%. That’s not tight money! Maybe that’s the measure of tightness we should have been following all along.

In other words, maybe one of the reasons we haven’t yet experienced economic turbulence is that monetary policy hasn’t been as tight as most investors thought. If so, it could take much longer to bring inflation down to 2.0% than the Fed expects, which means short-term rates could stay much higher for much longer.

In turn, that would mean more economic pain ahead than most investors currently expect. Some calls are hard to make no matter how much time is left in the game.

Hedgopia: Unless Bond Bears Get Motivated By Budget Deficit/Federal Debt/Interest Payments, Bulls Could Find Rally In 10-Year Yields Tempting

The 10-year T-yield just poked its head out of 4.30s resistance. Economic data in recent weeks have come in much stronger than expected. Although it is hard to argue the rally in rates will have staying power – unless, of course, bond bears are finally focused on the chronic issue of the government’s budget deficit, federal debt and the soaring interest payments.

The 10-year treasury yield has a spring in its step. Since bottoming last December at 3.79 percent, it has rallied with higher lows. On Monday, it ticked 4.46 percent intraday before closing out the session at 4.42 percent.

Yields are still substantially below last October’s five percent – the highest since July 2007 – but nudged past horizontal resistance at 4.30s last week (Chart 1)…

I'm beginning to be unsettled by Gold's continued strength. Is this the 'canary in the coal mine'? For I genuinely feel that something's BREAKING. WTF is it that's breaking? Some say golds pricing has left the west (NATO) and is now in the hands of the east-China & friends.

I'm beginning to be unsettled by Gold's continued strength. Is this the 'canary in the coal mine'? For I genuinely feel that something's BREAKING. WTF is it that's breaking? Some say golds pricing has left the west (NATO) and is now in the hands of the east-China & friends.

This substack is gold. GOLD, JERRY!!!