while WE slept: USTs higher, belly BID (middle east tensions flare) on strong volumes; Williams still sees them as 'bumps' (and so, SSGAs 50bps rate cut comin'?); demark 13 s/t exhaustion (10yy)

Good morning … NOT a bank earnings analyst so I’ll begin with an excerpt from a Goldilocks desk note …

… 8. in the context of the Fed, I’d pass along one observation. if there was a takeaway from client responses to last week’s note, it was the conviction and unanimity of this type of view: “given how strong growth remains and how far off their inflation target they are -- to say nothing of what the asset markets are clearly signaling -- is the Fed still serious about cutting several times this year?” I’m not saying this take was right or wrong -- and, I think there’s a big distinction between losing adjustment cuts and losing the availability of the Fed put -- but, if you had been stranded on a desert island for the past few years, you would be excused for asking about the necessity of rate cuts.

9. here’s where I’m going with all this: if you only told me three things contained within this email -- that the US labor market is remarkably healthy, that US equities have created an immense wealth effect and that US financial conditions were notably easy -- I might guess that S&P was within 1% of the highs, but I would NOT think that the Fed must be on the precipice of a cutting cycle. so, what we’re talking about is the removal of something that should always have been considered to be optional, and not something that was necessary to sustain economic momentum. I thought Mike Cahill put it well: “at some point, this is not just about the timing of 2024 cuts, but instead coming around to the view that the US economy appears to be able to operate rather well with a funds rate of 5.3%.”

10. here’s another way to frame things: would S&P have more potential upside if the Fed was easing into an acceleration? of course it would. are the implied cuts draining out simply because growth has been better-than expected? no, it’s more complicated than that, as three hot CPI reports in a row can’t be dismissed out of hand. does the mix of your portfolio need to be different today than it was three months ago? yes. if the economy continues to perform well, however, I just don’t think the absence of insurance cuts means the market needs to fall apart…

… the first <CHART> is our index of US financial conditions. even after the bruises of recent weeks, note where is stands compared to last October. my point here: while the adjustment cut debate has shifted a lot, this would have argued they weren’t all that critical to begin with. perhaps more pragmatically, if sustained, this easiness will be supportive of forward US economic growth:

-Tony Pasquariello

… meanwhile, 10yr yields remain NORTH of psychologically important 4.50% …

10yy: 4.50 target and then …

NOTE: momentum (slow stochastics) overSOLD so less of a reason to SELL and perhaps a reason to take a stab at a long esp when you consider demark 13 / exhaustion signal … below from Katie Stockton

Now over TO a few words from one of our collective ‘sponsors’, Williams of the FRBNY … These remarks came early yesterday (shortly after I hit SEND with some (updated calls) …

Federal Reserve Bank of New York Williams: Eclipse

… Like Monday’s eclipse, the Federal Reserve’s dual mandate has two goals that need to be in tune with one another: maximum employment and price stability. Restoring price stability is essential to achieving a sustainably strong labor market that benefits all. The overarching objective of monetary policy now is to properly balance restoring price stability and maintaining maximum employment, and the FOMC remains strongly committed to bringing inflation down to 2 percent over time…

… Inflation Over Time … Importantly, inflation expectations in the New York Fed’s Survey of Consumer Expectations are now again within their pre-Covid ranges at all horizons, consistent with other measures of inflation expectations.2

… Monetary Policy and the Economic Outlook Taking into account the effects of restrictive monetary policy, I expect GDP growth to be about 2 percent this year, reflecting the continued resilience of the economy and further improvements on the supply side. I expect the unemployment rate to peak at 4 percent this year and move gradually down to its longer-run level of 3-3/4 percent thereafter. I expect inflation to continue its gradual return to 2 percent, although there will likely be bumps along the way, as we’ve seen in some recent inflation readings. I expect overall PCE inflation to be 2-1/4 to 2-1/2 percent this year, before moving closer to 2 percent next year.

As has been the case since the onset of the pandemic, the outlook ahead is uncertain, and we will need to remain data-dependent…

…Closing I’ll close by saying that price stability is the bedrock upon which our economic prosperity stands. The economy has come a long way toward achieving better balance and reaching our 2 percent inflation goal. But we have not seen the total alignment of our dual mandate quite yet. I am committed to achieving maximum employment and price stability over the long term.

Therefore, I will remain focused on the data, the economic outlook, and the risks as we evaluate the appropriate path for monetary policy to best achieve our goals.

… I’m not sure if it was in fact these comments overwhelmingly optimistic which in turn gave Team Rate CUT a win for the day and so, helping stonks. Let us not forget the early data …

ZH: Producer Prices Rose At Fastest Pace In A Year In March ZH: "Literally Gas Lighting": The Hilarious Reason For Today's PPI Miss: Seasonally Adjusted Gas Prices

… and then, how ‘bout that long bond auction …

ZH: Ugly 30Y Auction Tails For First Time Since November, Lowest Foreign Demand Of 2024

… all told, added together by days end …

ZH: Stocks Surge, Goldgasms To Record High After "Adjusted" PPI Sparks Buying Frenzy

… Yet one place where there was little buying interest is arguably the most important asset for the market: 10Y yields rose as high as 4.59 and continue to trade in the redzone. Any breakout here and the next stop is 4.75%,

… and here we remain … 10yy > 4.50% as week winding down. Context is, as always KEY and so I’ll move along … here is a snapshot OF USTs as of 705a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher with the belly (and Bunds) outperforming as Middle East tensions rise markedly (see links above). DXY is higher (+0.55%) while front WTI futures are too (+1.35%). Asian stocks were mostly lower, EU and UK share markets are higher (SX5E +0.8%) while ES futures are showing -0.2% here at 6:45am. Our overnight US rates flows saw firmer prices during Asian hours with a 3.5k block buy in TYs that registered. But we did see sellers in the long-end with 30yrs lagging the rally a touch on the back of that. London's AM flows were unavailable. Overnight Treasury volume was ~110% of average overall with 7yrs (179%) seeing some out-sized relative average turnover this morning.

… Let's begin by noting that Treasury 2-year notes have tested and held our assumed support level (~4.98%) over the past few sessions; respecting the support on a closing basis so far. Moreover, short-term (daily) momentum is now into 'oversold' readings and looking quite ripe for a bull flip/turn at any time now- including at today's close if prices play along and extend their overnight rally even a little. There may also even be brewing bullish divergence (higher rate highs this week versus February's highs, potentially lower peak in momentum) here, so we're on point for the bull turn right now.

At the other end of the curve, Treasury 30yr yields are about as 'oversold' today as they were 'overbought' in early March- at the other side of their well-defined channel. The 4.70% channel top area should remain a solid support for bonds, from the looks of things. Buy any dip- especially into this support region?? On this, in our top section there is a link to a WSJ article saying that US homeowners have given up all hope for lower rates. Well, this is the exact sort of headline that the contrarian wants to see at a potential bull turning point... The thinking, of course, is that if there's no hope for higher bond prices, there is probably a limited long base that could be a headwind for a bullish reversal...

… and their visuals far better than mine … MOVING ALONG through to some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Stateside futures tentative ahead of US bank earnings, DXY bid and Bunds outperform; Fed speak due … Fixed complex higher with Bunds outperforming as markets digest Thursday’s ECB announcement and Fed divergence

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … I will just say up front that a couple / few which follow, specifically from a rather large German institution, not just contain an (updated call) but also connect dots clearly as to the impact on YIELDS which they forecast … again, like weatherman or dart throwers blindfolded … you decide if you have faith IN the forecast or not …

Small business optimism is stuck at recessionary levels, even amid a robust expansion. Using published aggregates, we infer that this sector has been in a deep slump since Q1 22. While this is unlikely to derail the expansion, the sector's fortunes in coming quarters may influence the upcoming election.

… Our data show that the pessimism of small businesses is consistent with the hard data. According to our measures, small businesses are have been mired in a deepening downturn since early 2021, reflecting the squeeze from increased labor costs, diminished productivity, and limited power to pass cost increases to customers …

… We believe that the struggles of small businesses could be a contributing factor to the low approval ratings of the Biden Administration. If so, the fortunes of this sector in the lead-up to the election could influence the presidential outcome…

Our translation of this week's March CPI and PPI estimates points to a 0.28% m/m (2.6% y/y) increase in headline PCE prices and a 0.27% m/m (2.7% y/y) increase in the core component. The core reading would be nearly identical to February's elevated pace, likely keeping the Fed on hold in May and June…

… With a third-consecutive firm core PCE inflation print likely undermining the FOMC's confidence that inflation is on course for a sustained return to 2%, we retain our expectation that the Fed will cut rates once this year, by 25bp, in September. We continue to expect four cuts in 2025, timed at SEP meetings, placing the end-25 funds rate at a range of 4.00-4.25%.

DB: US Economic Notes - March inflation recap: Strike three...cuts out

The March readings for both headline (0.38% vs. +0.44% in February) and core (+0.36% vs. +0.36%) CPI came in much stronger than expected. Taken together, the year-over-year rate for headline rose by three-tenths to 3.5%, while that for core increased 4bps to 3.80%, the first increase in twelve months. Shorter-term trends have also firmed, with the three- and six-month annualized rates picking up to 4.5% and 3.9%, respectively.

At the component level, the story is a similar one to those seen over the last couple months: slight decreases in core goods prices paired with sticky services inflation. Core goods posted a relatively broad-based 15bps decline, more than unwinding February's 11bp increase, while core services inflation remained elevated, posting another 0.5% gain. A large part of the stickiness is rental inflation, which has essentially moved sideways over the last couple months.

The PPI data were relatively neutral, so taken together with the CPI data, we think that March core PCE should increase +0.30% m/m, which would have the year-over-year rate tick down a tenth to 2.7%.

We have raised our forecasts on rents. Our initial read on the April core CPI data is that it should come in at +0.33% m/m, with the year-over-year rate remaining at 3.7%. We now expect core CPI to end the year six-tenths higher at 3.6% (Q4/Q4). Further out, our 2025 expectation has come up a tenth to 2.6% while 2026 remains at 2.4%. The pass-through of rents to our core PCE forecast is a little more moderate, with both 2024 and 2025 increasing by two-tenths to 2.7% and 2.2% respectively. We still foresee the Fed getting back to its 2.0% target by 2026.

These forecast changes have caused us to reevaluate our Fed view. As we discussed in our recent note (see "(Pushed) Back to December") we now expect only one rate cut this year, at the December FOMC meeting followed by modest further reductions in 2025. A reduction in July is possible, though it likely requires a string of more favorable inflation prints than we currently forecast.

In recent months we have argued that it is appropriate to frame the Fed cutting cycle as a two-stage process in which the Fed first delivers insurance cuts (or a mid-cycle adjustment) and further reductions would require evidence that the economy is weakening (see “(Mid-cycle) Adjusting the Fed’s narrative around cuts”). Recent developments – namely, upside inflation prints, solid labor market data, and easing financial conditions – have clearly diminished the case for commencing rate cuts.

Accounting for these developments, we have materially adjusted our Fed view for this year. We now expect only one rate cut this year at the December FOMC meeting followed by modest further reductions in 2025. Beyond next year, we expect the Fed to guide the policy rate back towards a neutral level that is likely just below 4% by the end of 2026. A reduction in July is possible, though it likely requires a string of more favorable inflation prints than we currently forecast.

Risks to this view are two-sided. Further disappointing inflation data or an election outcome that delivers fiscal stimulus and / or policies that could lift inflation (e.g., trade or immigration policies) would argue for no rate cuts this year and into 2025. Conversely, higher-for-longer raises the risks of financial stability events or a more aggressive tightening of financial conditions that could trigger a sharper slowdown in the economy that eventually necessitates more significant policy easing.

DB: What does DB’s revised Fed rate call imply for UST yields? (updated call as it relates TO yields…)

Earlier today our colleagues in US Economics published an updated Fed rate forecast, calling for later and more gradual cuts to a higher nominal neutral rate. Here we assess the implications for UST yields and the curve.

Using our standard forecasting approach, we find that the revised policy path produces a significantly higher and flatter nominal curve, with the 2y yield at the end of this year at 4.7%, nearly a percentage point higher than in our previously published forecast, and the 10y yield 50bp higher, at 4.65%. The revisions to front-end yields reflect the dramatic shift in the timing and quantum of cuts, while the moves at the long-end primarily reflect the increase in nominal neutral. With these revisions, yields across the curve are modestly above forwards and the curve is somewhat steeper at the long-end, reflecting our view that term premia remain too low.

Recent developments reinforce the view that term premia should be higher by supporting a continued negative correlation between yields and equities and increasing upside risks to longer-run inflation. If realized, a higher neutral policy rate would also reduce the likelihood of future Fed QE and should boost term premia over time.

Separately, with the sharp rate moves post-CPI, we have stopped out on our recommended SOFR-U5U7 steepener. Contrary to the rationale for the trade, the market is pricing Fed rate cuts well beyond 2025 and term premia haven’t risen alongside the upwardly revised short-rate trajectory.

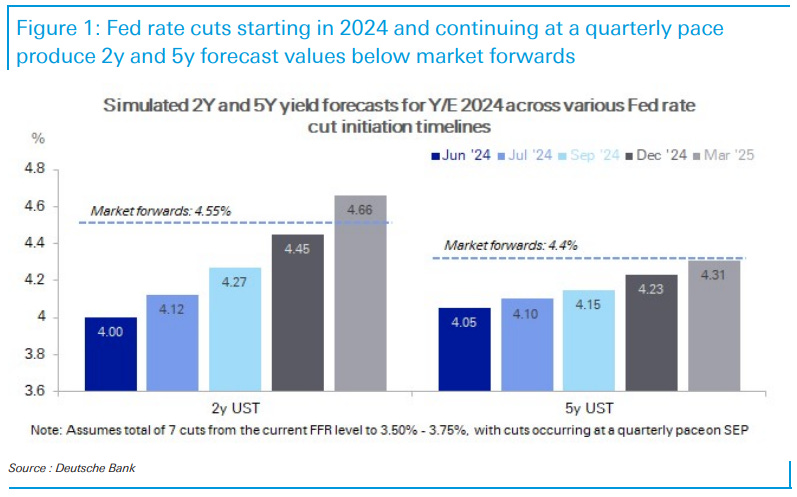

On the back of our recent blog on implied UST yields based on DB econ’s new Fed rate call, we simulate 2y, 5y and 10y yields under a variety of inputs in our forecast machinery. We then examine the 2s10s slope forecast relative to market forwards. We conclude with brief trading insights derived from the simulation…

Goldilocks: Core Producer Prices in Line with Consensus Expectations; Lowering Our March Core PCE Estimate to 28bp; Initial Claims Decline

BOTTOM LINE: Core producer prices increased in line with consensus expectations in March, as the PPI excluding food and energy and the PPI excluding food, energy, and trade services both increased by 0.2%. Based on details in the PPI and CPI reports, we now estimate that the core PCE price index rose 0.28% in March (vs. 0.29% previously), corresponding to a year-over-year rate of +2.73%. Initial jobless claims declined by slightly more than expected.

MS: US Economics: We Forecast Core PCE at 0.246% After PPI

… Noisy data makes it harder for the Fed to separate signal from noise. The downside print in PPI helped offset some of the re-acceleration from the CPI report, but this is still above the threshold we see as convincing evidence that inflation is moving in the right direction. Without much signal to gain from this week's data the core PCE print at the end of this month is critical and at any rate may be too little too late…

… There is an important central bank event today, which markets will likely ignore. Former Federal Reserve Chair Bernanke’s report on Bank of England forecasting is due. The UK central bank perhaps faces a bigger challenge than some other central banks—parts of the UK economy have been experiencing very rapid structural change, resulting in more dramatic revisions to data.

Yesterday’s US producer price data highlighted another data challenge. The motor insurance component rose 6.5% y/y, while in consumer price data it rose over 22% y/y. Different measurement techniques lead to wildly different visions of inflation. Import and export prices are due today (US export prices are in deflation).

US Michigan consumer sentiment offers another insight into the degree of political polarization in the US. Looking at unaligned voters’ sentiment may be useful; with a third of the metropolitan US experiencing food price deflation, sentiment (free of political bias) might improve.

Wells Fargo: Caution to the Wind: What Happened to the Saving Rate?

Summary Household saving dynamics have faded in importance, yet revised data show remaining liquidity isn't as concentrated as previously thought. Liquidity remains elevated across the wealth-spectrum. But households saved at the lowest rate in 14 months in February, and data suggest lower-income consumers are struggling to save at all. Saving less on a monthly basis in order to sustain spending can continue to add to an already robust spending trajectory this year, but it raises the vulnerability of the household sector generally.

Today's PPI report threw some cold water on yesterday's hotter-than-expected CPI. Our opinion is that the Fed won't be lowering interest rates this year because the economy and labor market will remain strong. Yesterday's CPI confirmed our conclusion based on the wrong premise. We aren't expecting inflation to get stuck above the Fed's 2.0% target. We think it will continue to moderate closer to that goal by the end of this year. So we don't expect that the Fed will have to start thinking about thinking about raising interest rates again. Consider the following …

… And from Global Wall Street inbox TO the WWW,

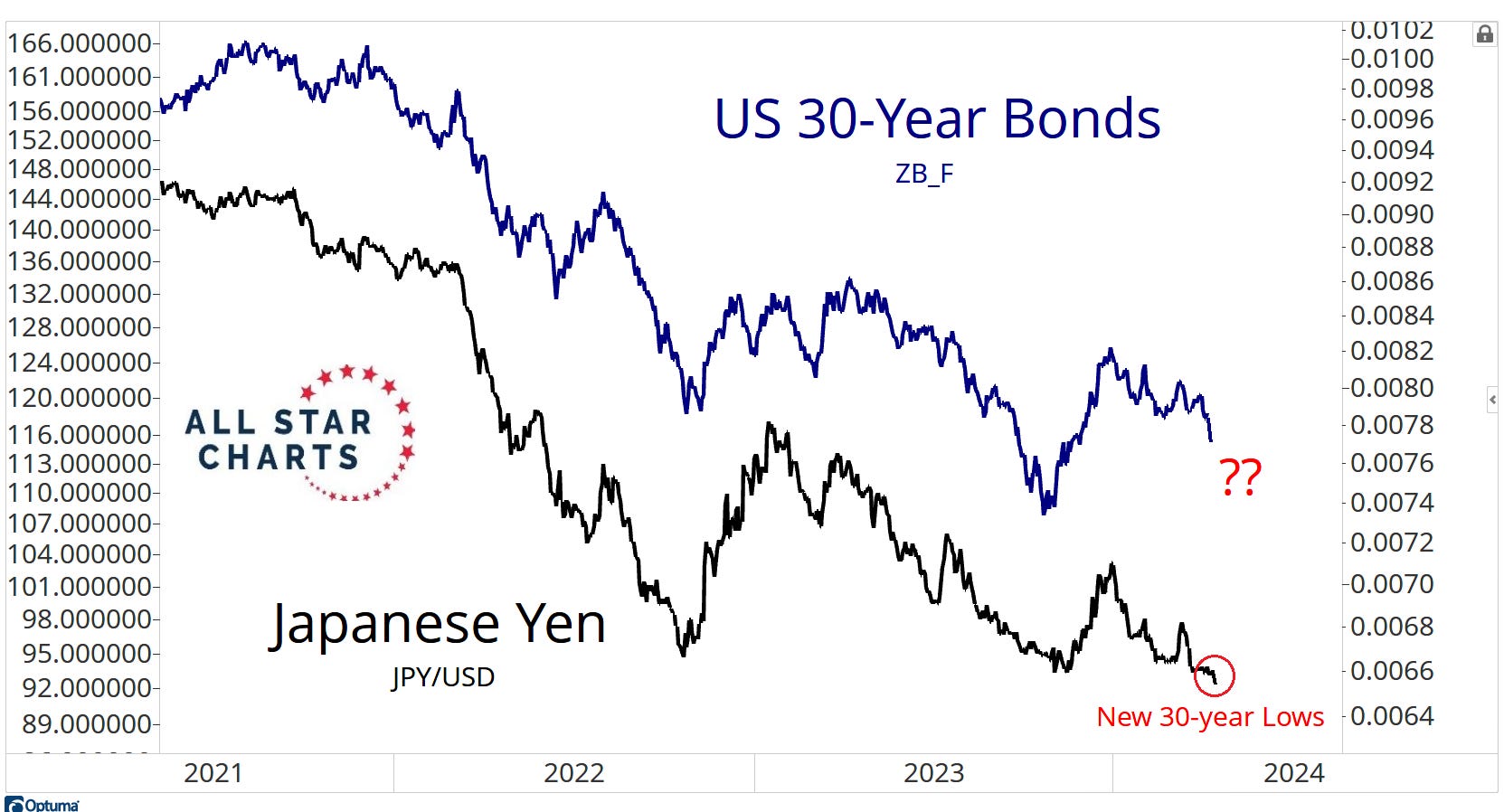

AllStarCharts: The Bond Crash Continues (thanks guys … thanks for that)

… Are you betting that the blue line doesn’t follow the black line?

If you’ve been following along, we’ve been talking about higher interest rates all year.

That’s been sending bonds crashing.

Stocks are not what we want to buy in that environment. Commodities and commodity-related stocks are what have been working.

Things started to change in February. And then they really changed in March.

Look at the stock market, for example.

Bloomberg: Big bets on Fed rate cuts look like fantasies: The Weekly Fix

State Street Versus Everyone Else This week’s big call came from State Street Global Advisors.

The asset manager expects the Federal Reserve to unleash a half-point cut at the central bank’s June meeting, en route to delivering a total of 150 basis points of easing in 2024. The logic is two-fold: not only is the US economy not as strong as it seems — signals such as credit card delinquencies point to a second-half downturn — but the Fed will likely want to front-load cuts ahead of November’s presidential election.

“The market is underplaying the likelihood of deeper cuts,” Lori Heinel, State Street’s Boston-based chief investment officer, told Bloomberg’s Alice Atkins. “There’s a lot to suggest that this is still a very fragile recovery despite the fact it continues to look resilient on the surface.”

That call — printed Tuesday — looks like fantasy following the Wednesday release of March’s inflation figures, which surprised to the upside across the board for the third straight month. Wall Street has been quick to recalibrate amid a barrage of strong data: just two Fed cuts are priced in for 2024, compared to six in January. Economists from Goldman Sachs to Deutsche Bank to Bank of America have pushed back their forecasts for cuts.

Meanwhile, former Treasury Secretary Lawrence Summers said markets “have to take seriously” the chance the central bank’s next shift is a hike. While the likelihood of such a move is in the 15% to 20% range, it’s clear that a rate cut in two months time would be a mistake, he said.

Bloomberg (via ZH): The Case For Owning Treasuries Is Evaporating

… Investors pondering where Treasury yields may top out will be turning toward economic analysis even more fervently than usual. With the Fed insisting it can be patient about long-awaited interest-rate cuts as long as the economy shows resilience, many bond investors have been bruised mightily this year precisely because they used policymakers’ forward guidance on rates as their guiding star.

After the Fed pivoted in December by holding its cash-rate target and forecasting three rate cuts in 2024, so did fixed-income traders. The idea that the economy is likely to crack given the central bank expects to start an easing cycle, the market moved rapidly to price in a traditional, rapid drop in the target cash rate. Then, after officials pushed back against bets on what they said would be an excessive level of easing, many seemed to think they were on more solid ground when the rates market came back into line with the Fed’s forecast.

That didn’t work out all that well so far, because the economy is palpably outperforming policymakers’ projections. The potential is brewing that the current sell-off has gone too far, with the back-up in yields now looking excessive relevant to the pace and scope of US data surprises. Still, it might take a few serious downside beats at this stage to set off a rebound in the short term.

McClellan: Doctor Copper Has A Message On Inflation - Chart In Focus

April 11, 2024

One trite Wall Street saying is that copper is the only metal with a PhD in economics. This is because copper is an industrial metal, the demand for which waxes and wanes with economic growth and shrinkage. So falling copper prices can be a sign that economic trouble lies ahead, and the converse is also true…

… The latest posting for CPI just out on April 10 caught many by surprise, but it reflects an up move which already started in copper from its December 2023 low. And the most recent jump to above $4/pound says that inflation is not yet done rising.

There is room to question the legitimacy of that message, since part of the rise in copper prices may have come from speculative trading in China. The Shanghai Stock Exchange just recently imposed trading limits on futures contracts for both gold and copper, in an effort to tamp down on that trading. So if this spike disappears rapidly, then one may be able to put a thumb over that point on the chart and disregard it. For now, though, the message is that inflation is going to be rising for at least the next 2 months.

Our morning note was titled "Yields Show Exhaustion" inspired by the DeMARK Indicators on the chart of 10-year #yields which show a short-term counter-trend signal near resistance, supporting an immediate pullback after yesterday's upswing

WolfST: Two Things about the PPI Today: The March Seasonal Adjustments Were Huge, and the 3-Month Rates All Jumped

Including by 7.9% annualized for the not-seasonally adjusted PPI, worst since June 2022. So we’ll take a look.

…HOPE to have something out over the weekend but THAT is all for now. Off to the day job…

The Fed Whisperer.....

https://youtu.be/f2c-wQ5rotg?si=CHnlGyZxI7U5iv3c